October 10th, 2024

“The goal of a successful trader is to make the best trades. …” — unknown

1. Iran Launches Ballistic Missiles at Israel as US Vows to Defend — The Israeli military on Tuesday said Iran fired more than 100 ballistic missiles directly at the country, an escalation in the battle between the Middle Eastern rivals fought mainly so far through proxies. Iranian state TV said the Islamic Revolutionary Guard Corps launched “tens of ballistic missiles” at Israel in retaliation for the killing of Hamas and Hezbollah leaders and an Iranian general. It targeted “important security and military sites” and threatened “more devastating attacks” if Israel responded.

2. US Services Activity Expands at Fastest Pace Since Early 2023 — The Institute for Supply Management’s index of services advanced 3.4 points to 54.9 last month, the group said Thursday. Readings above 50 indicate expansion, and the latest figure exceeded all projections in a Bloomberg survey of economists. The group’s new orders gauge jumped 6.4 points, the most since the start of 2023. Combined with a four-month high in a measure of business activity, which parallels the ISM’s factory output gauge, the data suggest the economy was on solid footing at the end of the third quarter. Twelve industries reported growth last month, led by real estate, management of companies and support services, and accommodation and food services.

3. US Hiring Tops All Estimates, While Jobless Rate Falls to 4.1% — Nonfarm payrolls increased 254,000 in September, the most in six months, following an upwardly revised 72,000 advance over the prior two months. The unemployment rate fell to 4.1% and hourly earnings increased 4% from a year earlier, according to Bureau of Labor Statistics’ figures released Friday. Combined with data earlier this week showing that demand for workers is still healthy while layoffs remain low, the payrolls report is likely to alleviate concerns that the labor market is deteriorating. The figures also showed fewer Americans were working part-time for economic reasons and people who recently lost their jobs were able to find work elsewhere. The gain in hiring last month was driven by leisure and hospitality, as well as health care and government. The payrolls diffusion index, which measures the breadth of changes in private employment, rose to the highest since the start of the year. Manufacturers, however, cut jobs for a second month.

4. Food Prices Rose at Fastest Rate in 18 Months in September, UN Says — The FAO’s food price index, which tracks global prices for a basket of staple foods, averaged 124.4 points in September, up 3.0% from August and 2.1% higher on year. The index increased at the fastest on-month rate since March 2022. In August, food prices stood at 120.7 points. Sugar prices rose 10.4% in September, driven by falling Brazilian crop prospects on prolonged dry weather and fires in August, and worries that India’s decision to lift ethanol production restrictions on sugarcane could hit export availabilities. Cereal prices rose 3% on higher wheat and corn export prices. International wheat price increases largely reflect concerns of excessively wet conditions in Canada and the European Union, albeit partially offset by competitively priced supplies from the Black Sea region.

5. Port strike ends as workers agree to tentative deal on wages and contract extension — A major union for U.S. dockworkers and the United States Maritime Alliance agreed on Thursday to a tentative deal on wages and have extended their existing contract through Jan. 15 to provide time to negotiate a new contract. ILA wages will increase 61.5% over six years under the tentative agreement, sources told CNBC. For every day of a strike, it can take up to a week to unwind the congestion and delays that build up within the supply chain. According to Everstream Analytics, this three-day all-out strike will likely take minimum three weeks to return to normal operations at U.S. ports.

The number of container ships waiting outside of U.S. Gulf and East Coast ports had decreased from Thursday night to Friday morning, down to 54, according to Everstream, as ships moved into the ports of Savannah and Charleston ahead of terminal reopenings. But its data showed that at the Port of New York-Newark, there had been an increase in ships at anchor. In all, 386,000 twenty-foot equivalent container units were waiting to be moved into ports.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 1st, 2024

‘Buy on the cannons, sell on the trumpets’ — Nicholas Vardy

1. China Tries to Jolt Ailing Economy — The People’s Bank of China cut its benchmark interest rate and lower the amount of cash that banks need to hold in reserve—a bid to free up more resources for lending. It also said it would cut the interest rate payable on existing mortgages and lower down payments for second homes. At a press conference in Beijing, PBOC Gov. Pan Gongsheng said further easing is in the pipeline, with another reduction in bank reserve requirements expected before year-end.

The central bank also announced it would offer 500 billion yuan in loans, equivalent to roughly $70 billion, to funds, brokers and insurers to buy Chinese stocks as part of an effort to lift the country’s ailing stock market. It said it would put up another 300 billion yuan to finance share buybacks by listed companies.

2. Key Fed inflation gauge at 2.2% in August, lower than expected — The personal consumption expenditures price index, a gauge the Fed focuses on to measure the cost of goods and services in the U.S. economy, rose 0.1% for the month, putting the 12-month inflation rate at 2.2%, down from 2.5% in July and the lowest since February 2021.

Economists surveyed by Dow Jones had been expecting all-items PCE to rise 0.1% on the month and 2.3% from a year ago. Excluding food and energy, core PCE rose 0.1% in August and was up 2.7% from a year ago, the 12-month number 0.1 percentage point higher than July. Fed officials tend to focus more on core as a better measure of long-run trends. The respective forecasts were for 0.2% and 2.7% on core.

3. Netanyahu Pledges to Continue Fight Against Hezbollah in U.N. Address — Israeli Prime Minister Benjamin Netanyahu vowed to continue his country’s military campaign against Hezbollah in Lebanon, amid U.S.-led efforts to seek a diplomatic solution before all-out war breaks out. Netanyahu’s comments came after Israel shot down a missile that was fired from Yemen by the Iran-aligned Houthi rebels. It was the third time in the past two weeks that Israel’s central area—where a majority of its population resides—has been targeted and signaled the risk of a widening conflict as the fighting in Gaza and Lebanon continues. The Biden administration is pressing for Israel and Hezbollah, a U.S.-designated terrorist group, to pause their escalating attacks, hoping to avert a ground war that could escalate into a regional conflagration. The U.S. and France, backed by allies, in a joint statement called for a 21-day pause in the fighting on the Israel-Lebanon border.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

September 25th, 2024

1. US Retail Sales Post Surprise Gain, Helped by Online Stores — The value of retail purchases, unadjusted for inflation, increased 0.1% after a revised 1.1% gain in July, Commerce Department data showed Tuesday. Excluding autos and gasoline stations, sales advanced for fourth month. Five of the report’s 13 categories posted increases, while others such as electronics and appliances, clothing and furniture fell. E-commerce merchants posted a solid 1.4% gain. Receipts at gasoline service stations decreased, reflecting cheaper prices at the pump.

The retail sales report showed so-called control-group sales — which are used to calculate gross domestic product — rose 0.3% in August. The measure excludes food services, auto dealers, building materials stores and gasoline stations.

2. Fed Cuts Rates by Half Point in Decisive Bid to Defend Economy — The Federal Reserve lowered its benchmark interest rate by a half percentage point Wednesday, an aggressive start to a policy shift aimed at bolstering the US labor market. Projections released following their two-day meeting showed a narrow majority, 10 of 19 officials, favored lowering rates by at least an additional half-point over their two remaining 2024 meetings. Seven policymakers supported another quarter-point rate reduction this year, while two opposed any further moves. The Federal Open Market Committee voted 11 to 1 to lower the federal funds rate to a range of 4.75% to 5%, after holding it for more than a year at its highest level in two decades. It was the Fed’s first rate cut in more than four years.

3. Jobless Claims: Weekly jobless claims remained stable, suggesting a strong labor market.

4. Consumer Spending: Retail sales saw moderate growth, reflecting healthy consumer spending, though some sectors raised concerns about potential slowdowns.

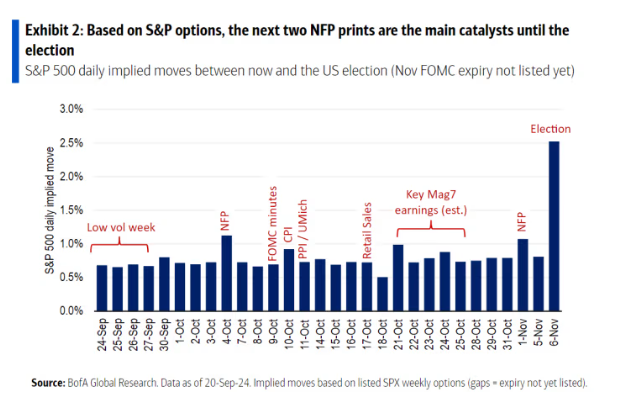

5. The Most Volatile Days for Stocks Before the Election, According to the Options Market — according to a team of strategists at Bank of America, who plotted what options traders are expecting each day before expiry. Traders anticipate swings of more than 1% in either direction on Oct. 4 and Nov. 1, when the September and October jobs reports are due to be released. Two other economic reports also have notable market-moving potential: the September CPI report, due Oct. 10, and the September retail sales report, on Oct. 17.

Options are also bracing for a roller-coaster ride during the week that starts on Oct. 21, one of the busiest of the coming third-quarter earnings reporting season. The week will feature results from Alphabet Inc., Microsoft, Meta and Amazon.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

September 17th, 2024

A peak performance trader is totally committed to being the best and doing whatever it takes to be the best. … Unknown

1. Core US Inflation Picks Up, Damping Odds of Outsize Fed Cut — the so-called core consumer price index — which excludes food and energy costs — increased 0.3% from July, the most in four months, and 3.2% from a year ago, Bureau of Labor Statistics figures showed Wednesday. The three-month annualized rate advanced 2.1%, picking up from 1.6% in July, according to Bloomberg calculations.

Economists see the core gauge as a better indicator of underlying inflation than the overall CPI. That measure climbed 0.2% from the prior month and 2.5% from a year ago in August, marking the fifth straight month the annual measure has eased and dragged down by cheaper gasoline prices.

2. Battery Maker Northvolt to Cut Jobs Amid Cooling EV Market — the Swedish battery maker is facing a challenging time as the adoption of EVs in Europe has slowed sharply on concerns over new trade tariffs, the withdrawal of some government incentives and a sluggish rollout of charging infrastructure. Meanwhile, European automakers are also facing increasingly stiff competition from lower-cost Chinese rivals, which have priced their vehicles aggressively and gained a foothold across Europe. The tougher backdrop recently saw BMW cancel a 2 billion euro ($2.22 billion) battery order, prompting Northvolt to reassess its growth strategy.

3. US Producer Prices Pick Up Slightly After Downward Revisions — the producer price index for final demand increased 0.2% from a month earlier following a flat reading in July, according to a Bureau of Labor Statistics report released Thursday. The median forecast in a Bloomberg survey of economists called for a 0.1% gain. Compared with a year ago, the PPI rose 1.7% — the least since early in 2024. A measure of producer prices excluding volatile food and energy categories climbed 0.3% in August from the prior month, and 2.4% from a year ago.

4. ECB Cuts Rates Again as Inflation Fades and Economy Stumbles — The European Central Bank lowered interest rates for the second time this year with inflation receding toward 2% and concerns about the economy building. The key deposit rate was cut by 25 basis points to 3.5% — as all analysts polled by Bloomberg predicted. The ECB reiterated that it can’t commit to a specific course for borrowing costs. Like its global peers, the ECB is getting more confident that consumer-price growth is returning to target following its historic spike. The euro zone’s 20-nation economy, meanwhile, is losing momentum. Households are failing to support the rebound that began earlier in the year and manufacturers remain in the doldrums due to soft demand from outside the single currency area.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

September 10th, 2024

When in doubt, get out and get a good night’s sleep. I’ve done that lots … When you get out, then you can think clearly again. Michael Marcus

1. US Job Openings Decline to Lowest Level Since January 2021 — US job openings fell in July to the lowest since the start of 2021 and layoffs rose, consistent with other signs of slowing demand for workers. Available positions decreased to 7.67 million from a downwardly revised 7.91 million reading in the prior month, the Bureau of Labor Statistics Job Openings and Labor Turnover Survey, known as JOLTS, showed Wednesday. The figure was lower than all estimates in a Bloomberg survey of economists. After July’s disappointing jobs figures and a large downward revision to payrolls in the past year, Fed officials and market participants are paying close attention to the August employment data due Friday — especially if another weak report could prompt an outsize rate cut.

2. Fed’s Beige Book Shows Stagnant, Declining US Economic Activity — Economic activity was flat or declining across most regions in the US in recent weeks, the Federal Reserve said in its Beige Book survey of regional contacts. Employment levels were generally flat to up slightly, according to the report released Wednesday. While reports of layoffs were rare, some firms noted cutting shifts and hours, leaving advertised positions unfilled or reducing headcount through attrition. The number of districts reporting flat or declining activity rose to nine in recent weeks, up from five in the prior period. Economic activity grew in three districts. Contacts, however, generally expected economic activity to remain stable or improve somewhat in coming months.

3. August payrolls grew by a less-than-expected 142,000, but unemployment rate ticked down to 4.2% — Nonfarm payrolls expanded by 142,000 during the month, up from 89,000 in July and below the 161,000 consensus forecast from Dow Jones, according to a report Friday from the Labor Department’s Bureau of Labor Statistics. At the same time, the unemployment rate ticked down to 4.2%, as expected. The labor force expanded by 120,000 for the month, helping push the jobless level down by 0.1 percentage point, though the labor force participation rate held at 62.7%. An alternative measure that includes discouraged workers and those holding part-time jobs for economic reasons edged up to 7.9%, its highest reading since October 2021. The household survey, which is used to calculate the unemployment rate and is often more volatile than the survey of establishments, showed employment growth of 168,000. The balance, though, tilted toward part-time employment, which increased by 527,000, while full-time fell by 438,000.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

September 3rd, 2024

When in doubt, get out and get a good night’s sleep. I’ve done that lots of times and the next day everything was clear… While you are in [the position], you can’t think. When you get out, then you can think clearly again. — Michael Marcus

1. US Economy Expands at Revised 3% Rate on Resilient Consumer — Gross domestic product rose at a 3% annualized rate during the April-June period, up from the previous estimate of 2.8%, according to Bureau of Economic Analysis figures published Thursday. The economy’s main growth engine — personal spending — advanced 2.9%, versus the prior estimate of 2.3%. The other main gauge of economic activity — gross domestic income — rose a more moderate 1.3% in the government’s first estimate for the period, matching the first-quarter gain. Whereas GDP measures spending on goods and services, GDI measures income generated and costs incurred from producing those same goods and services. The average of the two growth measures was 2.1%.

2. US Pending Home Sales Gauge Drops to Lowest on Record — A National Association of Realtors index of contract signings fell 5.5% to 70.2 last month, the lowest in data back to 2001, the group said Thursday. The drop was larger than all estimates in a Bloomberg survey of economists and reflected declining sales in all four major regions. “The positive impact of job growth and higher inventory could not overcome affordability challenges and some degree of wait-and-see related to the upcoming US presidential election,” NAR Chief Economist Lawrence Yun in a statement.

The previously owned home market has been hamstrung by high borrowing costs and lean inventory for nearly two years. While mortgage rates have declined this month to the lowest in over a year, high prices and limited inventory are deterring prospective buyers who might still be holding out for cheaper rates.

3. Apple, Nvidia Are in Talks to Invest in OpenAI — The investment would be part of a new OpenAI fundraising round that would value the ChatGPT maker above $100 billion, people familiar with the situation said. The Wall Street Journal reported Wednesday that venture-capital firm Thrive Capital is leading the round, which will total several billion dollars, and Microsoft MSFT 0.61%increase; green up pointing triangle is also expected to participate. It couldn’t be learned how much Apple, Nvidia or Microsoft will invest into OpenAI this round. To date, Microsoft has been the primary strategic investor in OpenAI. It owns a 49% share of the AI startup’s profits after investing $13 billion since 2019. Apple in June announced OpenAI as the first official partner for Apple Intelligence, its system for infusing AI features throughout its operating system. The new AI will feature an improved Siri voice assistant, text proofreading and creating custom emojis.

4. Fed Favored Inflation Gauge’s Mild Gain Sets Stage for Rate Cut — The so-called core personal consumption expenditures price index, which strips out volatile food and energy items, increased 0.2% from June, according to Bureau of Economic Analysis data out Friday. On a three-month annualized basis — a metric economists say paints a more accurate picture of the trajectory of inflation — it advanced 1.7%, the slowest this year. While spending picked up, income growth was much more sluggish and the saving rate declined. That may raise questions about the durability of consumer spending going forward. Friday’s report supports the view that it’s time to begin unwinding the restrictiveness of monetary policy. Combined with emerging cracks in the labor market, the sustained cooling in inflation explains why Fed Chair Jerome Powell said last week “the time has come” for central bankers to start lowering borrowing costs, likely next month.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

August 27th, 2024

If you can’t take a small loss, sooner or later you will take the mother of all losses. — Ed Seykota

1. US Payrolls Marked Down by Most Since 2009 in Preliminary Data — The number of workers on payrolls will likely be revised down by 818,000 for the 12 months through March — or around 68,000 less each month — according to the Bureau of Labor Statistics’ preliminary benchmark revision. It was the largest downward revision since 2009. Before the report, the BLS’s initial payrolls figures indicated employers added 2.9 million total jobs in the period, or an average of 242,000 per month. Now the monthly pace is more likely to be around 174,000 assuming the change is distributed proportionately, still a healthy rate of hiring but a moderation from the post-pandemic peak. Benchmark revisions are done every year, but they were particularly scrutinized this year by markets and Federal Reserve watchers for any signs that the labor market may be cooling faster than originally reported. Several economists said the initial payrolls data may have been impacted by a number of factors, including adjustments for the creation and closure of businesses and how unauthorized immigrant workers are counted.

2. Fed Minutes Showed Officials Discussed July Rate Cut, Ready to Cut in September — “All participants supported maintaining the target range for the federal funds rate at [5.25% to 5.50%,] although several observed that the recent progress on inflation and increases in the unemployment rate had provided a plausible case for reducing the target range 25 basis points [a quarter of a percentage point] at this meeting or that they could have supported such a decision,” read the minutes from the Federal Open Market Committee’s July 30-31 meeting. Ultimately, while noting a better balance of risks to achieving their employment and inflation goals, officials decided to wait for more data before changing interest rates. Markets are betting the FOMC will vote to cut interest rates at their next meeting on Sept. 17-18.

3. U.S. Home Sales Edged Up in July, Prices Still Near Record Highs — Mortgage rates have fallen in recent weeks, which helped boost sales modestly in July. But the volume of existing-home sales has been stuck at low levels all year, and the spring selling season, usually the busiest time of year for the housing market, was a flop. Sales of previously owned homes in July rose 1.3% from the prior month to a seasonally adjusted annual rate of 3.95 million, the National Association of Realtors said Thursday. That was the lowest level for any July since 2010. On an annual basis, existing-home sales, which make up most of the housing market, fell 2.5%.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

August 21st, 2024

“Systems don’t need to be changed. The trick is for a trader to develop a system with which he is compatible.” — Ed Seykota

1. US Producer Prices Rise Less Than Forecast — The producer price index for final demand increased 0.1% from a month earlier, according to a Bureau of Labor Statistics. The median forecast in a Bloomberg survey of economists called for a 0.2% gain. Compared with a year ago, the PPI rose 2.2%. The PPI excluding the volatile food and energy categories was unchanged in July from the prior month, the tamest reading in four months. The core PPI rose 2.4% from a year ago. Against a backdrop of dissipating inflationary pressures, weak July jobs figures prompted economists to pencil in a series of Federal Reserve interest-rate cuts beginning next month.

2. Core US Inflation Eases a Fourth Month, Sealing Fed Rate Cut — The so-called core consumer price index — which excludes food and energy costs — increased 3.2% in July from a year ago, still the slowest pace since early 2021. The monthly measure rose 0.2%, a slight pickup from June’s surprisingly low reading, Bureau of Labor Statistics figures showed Wednesday. Economists see the core gauge as a better indicator of underlying inflation than the overall CPI. That measure also climbed 0.2% from the prior month and 2.9% from a year ago. BLS said nearly 90% of the monthly advance was due to shelter, which accelerated from June. Inflation is still broadly on a downward trend as the economy slowly shifts into a lower gear. Combined with a softening job market, the Fed is widely expected to start lowering interest rates next month, while the size of the cut will likely be determined by more incoming data.

3. US Retail Sales Beat Forecasts, Defying Calls of Weaker Consumer — The value of retail purchases, unadjusted for inflation, increased 1% in July and helped by a sharp snapback in car sales, Commerce Department data showed Thursday. Excluding autos and gasoline stations, sales were up 0.4%. Ten of the report’s 13 categories posted increases. Car sales bounced back strongly after a cyberattack on auto dealerships led to a sizable drop in June. Electronics and appliances also posted solid gains. E-commerce sales rose at a modest clip, potentially reflecting heavy discounting in the period by Amazon.com Inc.’s Prime Day and other promotions from Walmart Inc. and Target Corp.

4. Harris Calls for Expanded Child Tax Credit, 3 Million New Housing Units — Vice President Kamala Harris called for a substantial expansion of the child tax credit, set a goal of building 3 million new housing units and pledged to penalize companies that engage in price gouging, while warning that former President Donald Trump’s trade policies would raise prices. The vice president sought to contrast her approach with Trump’s, criticizing the former president for proposing an across-the-board tariff of at least 10% on imports.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

August 13th, 2024

1. Harris Picks Minnesota Gov. Tim Walz as Running Mate — Vice President Kamala Harris on Tuesday picked Minnesota Gov. Tim Walz, an avuncular former high-school teacher with a progressive streak, as her running mate in a move that added a white man to the first-ever ticket led by a woman of color. A two-term governor and current chairman of the Democratic Governors Association, Walz could be especially helpful in the battleground states of Wisconsin and Michigan. He is already well known in western Wisconsin because it shares media markets with Minnesota, while Michigan has some economic and cultural similarities with the state he now governs.

2. Bank of Japan Walks Back Talk of Rate Increases After Roiling Markets — The pledge by Bank of Japan Deputy Gov. Shinichi Uchida led to a sharp recovery in Tokyo stock prices and a fall in the yen. That moved markets closer to where they were before the July 31 news conference by Gov. Kazuo Ueda, in which he suggested he wanted to keep raising rates despite lackluster consumer spending in Japan. The Bank of Japan lifted its policy interest rate to 0.25% on July 31. Combined with Ueda’s hawkish comments and the prospect of Federal Reserve rate cuts soon, the move pushed up the yen sharply.

That in turn pushed down Japanese stocks, and the Nikkei on Monday suffered its biggest single-day percentage loss since 1987. Global stock markets including the U.S. followed suit.

3. US Initial Jobless Claims Decline by Most in Nearly a Year — Initial claims decreased by 17,000 to 233,000 in the week ended Aug. 3, according to Labor Department data released Thursday. That was helped by fewer applications in states that had registered large increases in recent weeks, such as Michigan, Missouri and Texas. The decline in initial applications may help reassure markets that the workforce is simply reverting to its pre-pandemic trend rather than rapidly deteriorating. That was the consensus until last week, when the jobs report showed employers substantially scaled back hiring in July and the unemployment rate rose for a fourth month, triggering a key recession indicator.

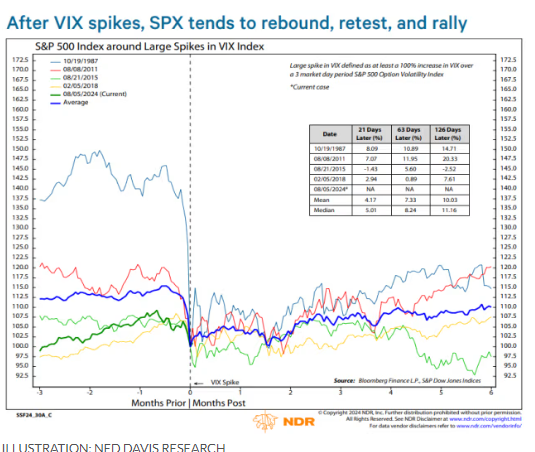

4. Stock market may retest Monday lows in 4-step recovery process, history suggests — based on past history from the past VIX volatility shock, history suggests a retest of those Monday lows is likely in order. The good news is that the market is likely to regain its mojo in the coming weeks, as long as a recession remains at bay and the latest episode proves to be nothing more than an economic growth scare based on Ned Davis Research. Chart below displays the result of the research.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

August 1st, 2024

“It Ain’t About How Hard You Hit, It’s About How Hard You Can Get Hit And Keep Moving Forward.” — Rocky

1. US Labor Costs Rise Less Than Forecast as Inflation Eases — The employment cost index, which measures wages and benefits, increased 0.9% in the April-to-June period, after rising by the most in a year at the start of 2024, according to Bureau of Labor Statistics figures out Wednesday. The median estimate in a Bloomberg survey of economists called for a 1% rise. The figures corroborate recent data that show the labor market is moderating toward its pre-pandemic trend. Other measures also point to cooling wage growth, as well as a slower pace of hiring and rising unemployment.

2. Powell Says Fed Could Cut Rates ‘As Soon As’ September Meeting — Federal Reserve Chair Jerome Powell said an interest-rate cut could come as soon as September after the US central bank voted to leave its benchmark at the highest level in more than two decades. His comments followed a Federal Open Market Committee decision to leave the federal funds rate in a range of 5.25% to 5.5%, a level they have maintained since last July. Policymakers also made several adjustments to the language of a statement released after their two-day meeting in Washington, signaling they are closer to reducing borrowing costs. Notably, the committee shifted to saying it is “attentive to the risks to both sides of its dual mandate,” rather than prior wording focused just on inflation risks.

3. U.S. Hiring Slowed Sharply, With 114,000 Jobs Added in July — ob growth slowed sharply in July and the unemployment rate rose to its highest level since 2021, adding to evidence that a labor market whose strength is fading could actually be on its way to weakness.

America is still adding jobs, but no longer at a red-hot pace. The Labor Department reported on Friday that employers added 114,000 jobs last month, missing expectations. The unemployment rate jumped to 4.3%—its highest level in nearly three years, when the labor market was still clawing its way back from the pandemic.

4. Intel has worst day on Wall Street in 50 years, falls to lowest price in over a decade — Intel

shares plunged the most in 50 years on Friday, reaching a price not seen since 2013, after the chipmaker reported a big earnings miss and announced a massive restructuring.

The stock plummeted 26% to $21.48 at the close. It was the second worst day ever for the shares, behind only a 31% drop in July 1974, which was three years after Intel’s IPO. The company’s market cap is now below $100 billion. Intel said it won’t pay its dividend in the fiscal fourth quarter of 2024 and lowered its forecast for full-year capital expenditures by over 20%. The company said it would lay off more than 15% of its employees as part of a $10 billion cost-reduction plan.

Posted in Weekly Summary | No Comments »