Week of Oct 25 2019 Weekly Recap & The Week Ahead

Thursday, October 31st, 2019There will not be any Weekly Re-Cap for the week of Oct 21 to Oct 25 2019. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

| Market Outlook |

| Equity Guidance Blog — Financial Market Overview |

There will not be any Weekly Re-Cap for the week of Oct 21 to Oct 25 2019. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

“Big money is made on the stock market by being on the right side of major moves. The idea is to get in harmony with the market. It’s suicidal to fight trends. They have a higher probability of continuing than not.” – Martin Zweig

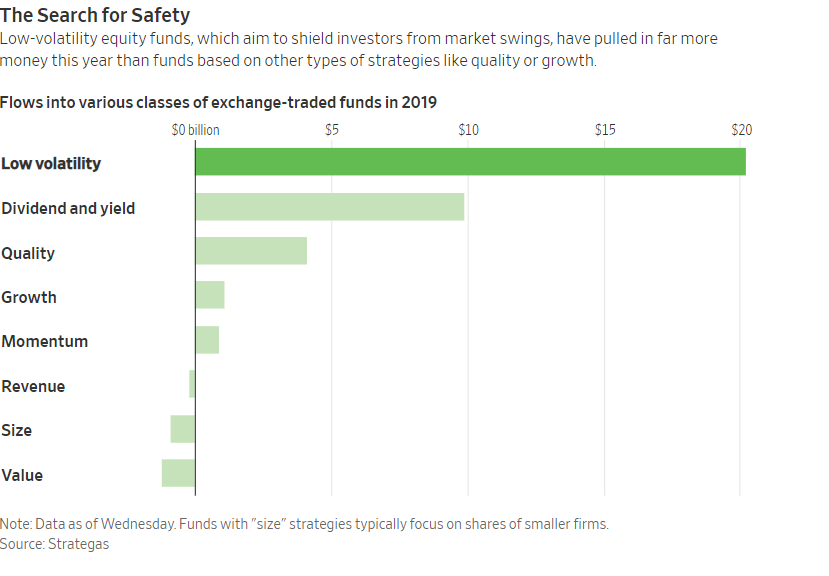

1. Stocks’ Path Toward Records Led by Defensive Plays — much of the gains over the past month have been driven by parts of the market that investors tend to gravitate toward when they are looking for safety, as well as an attractive yield. The S&P 500’s real-estate and utilities sectors, often considered bond-like because of their relatively hefty dividend payouts, have climbed 1.3% and 1.9% respectively over the past month while the broad index has fallen 1%. That makes them by far the best-performing groups in the broad index over that time, followed by technology shares. Exchange-traded funds that aim to minimize investors’ exposure to market swings have also gained popularity, with flows into low-volatility equity ETFs surpassing $20 billion this year—nearly 20 times that of growth stocks, according to Strategas.

2. The U.S. Imposed Sanctions and Raised Steel Tariffs on Turkey — President Trump threatened harsher financial penalties if Turkey continued its offensive in northern Syria, launched after he decided to withdraw U.S. troops from the region. The withdrawal decision was widely criticized on Capitol Hill for leaving Kurdish militias—allies in the U.S.-led fight against Islamic State—open to attack. Mr. Trump also spoke with Turkish President Recep Tayyip Erdogan, calling on him to stop the invasion and negotiate an end to the violence, Vice President Mike Pence said late Monday.

3. U.K., EU Agree on Draft Brexit Deal — Britain and the European Union agreed to new terms for the U.K.’s exit from the bloc late last week, paving the way for a high-stakes vote in the British Parliament.Following days of intense talks more than three years after Britain voted to leave the EU, the two sides struck a compromise intended to ensure a border doesn’t appear on the island of Ireland. It was the main sticking point in negotiations aimed at smoothing Britain’s split with its largest trading partner.

4. UAW Reaches Tentative Labor Deal With GM — the United Auto Workers struck a tentative labor deal with General Motors Co. GM -1.26% on Wednesday, a critical step in ending a monthlong strike that has brought more than 30 GM factories in the U.S. to a standstill. As part of the new deal, GM has committed to invest around $7.7 billion in its U.S. factories over the four-year contract period, which would create or preserve about 9,000 jobs, according to people familiar with the agreement. The company also separately has joined with outside companies to invest another roughly $1.3 billion in facilities near its Lordstown, Ohio, assembly plant, which the company hopes to sell to a startup electric-truck maker, the people said.

The week ahead — Economic data from Econoday.com:

“I think investment psychology is by far the more important element, followed by risk control, with the least important consideration being the question of where you buy and sell.” — Tom Basso

1. US/China Up the Ante with Trade Dispute / Adds Chinese Firms to Blacklist — the U.S. added 28 Chinese entities to an export blacklist, citing their role in Beijing’s repression of Muslim minorities in northwest China. The decision came days before high-level trade talks are set to resume in Washington. The U.S. said the action isn’t related to trade talks, but it is likely to disturb Chinese officials already incensed over what Beijing sees as U.S. support for the pro-democracy movement in Hong Kong. Trade negotiations have made little progress since hitting an impasse in May. The one recent bright spot has been Chinese agricultural purchases, including more than 1.5 million metric tons of U.S. soybeans in the last week of September alone.

2. Boeing Suffers Setbacks — the effort to return 737 MAX jets to service has hit a new snag because of heightened European safety concerns about portions of proposed fixes to flight-control systems. Separately, the pilots’ union at Southwest Airlines sued Boeing, alleging that the plane maker rushed the 737 MAX to market and misrepresented the plane as safe. Boeing called the suit “meritless.”

3. US/China Trade Talks Resume — Senior U.S. and Chinese officials will square off for trade talks Thursday at a pivotal moment in the countries’ relationship, with higher tariffs looming if negotiators fail to break a five-month stalemate. China is looking to narrow the scope of its negotiations with the U.S. to trade matters only and put thornier issues—such as U.S. national security concerns over Chinese telecom giant Huawei Technologies Co.—on a separate track in a bid to break the deadlock. Business groups want Mr. Trump abandon plans to raise tariffs to 30%, which is set to happen Oct. 15. They also want him to drop plans to impose new tariffs of 15% on $156 billion in smartphones, apparel and other consumer goods starting Dec. 15.

4. Fed to Increase Supply of Bank Reserves — the Federal Reserve will soon increase its purchases of short-term Treasury securities to avoid a recurrence of the unexpected strains experienced in money markets last month, Fed Chairman Jerome Powell said in a speech in Denver. Fed officials stopped shrinking the assets on their balance sheet in August but never said when they would allow the balance sheet to grow again. As a result, bank deposits held at the Fed—a crucial liability on the balance sheet—have continued declining. Stresses in very-short-term funding markets recently suggested banks have grown reluctant to lend those reserves.

5. US/China Agreed to a Trade Truce — the US/China agreed to a initial tentative agreement on Friday. Mr. Trump said China will make some $40 billion to $50 billion more in agricultural purchases over two years and has promised to better protect intellectual property and welcome more foreign financial services. In return the U.S. won’t increase tariffs to 30% from 25% on $250 billion of Chinese goods next week as Mr. Trump had planned. The two countries also agreed to keep talking toward what Mr. Trump called a “phase two” agreement that would include the tougher issues such as Chinese technology theft and predatory regulation against American companies. There will also be a new consultation process to address disputes and monitor enforcement. The implication is that if progress continues, Mr. Trump will cancel the tariffs planned for December on more Chinese goods.

The week ahead — Economic data from Econoday.com:

“Reaching any goal in trading requires specific domain knowledge and technical skills. But then, after that, it’s all mindset management. Yet most people ignore that —they automatically think they have that last part all figured out, and it’s a mistake.” ― Yvan Byeajee,

1. U.S. Factory Activity Contracted Again in September — the Institute for Supply Management reported earlier last week its U.S. manufacturing index fell to 47.8 in September from 49.1 in August. The reading is the lowest since June 2009 and represents a continuation of the slowdown seen in August, when the index contracted for the first time since August 2016. The deeper contraction in the manufacturing sector is the latest sign that the escalated trade war between the U.S. and China is taking a big bite from the economy. Manufacturing was once considered a big winner under the Trump administration with improvement in employment and activity over the past few years.

2. Charles Schwab Ending Online Trading Commissions on U.S.-Listed Products — Charles Schwab Corp. said it would eliminate commissions on trades made on its mobile and web channels, rattling the online brokerage industry. Charles Schwab said the move, which is effective Oct. 7, is aimed at making online investing more affordable. It noted that new firms entering the market often use zero or low commissions as a lever. Companies effected are: SCHW, AMTD, ETFC, IBKR.

3. U.S. Factory Activity Contracted — U.S. factory activity contracted for the second straight month in September, hitting a 10-year low and triggering concerns about the economy. Surveys of purchasing managers in Europe and Asia, also released Tuesday, pointed to deepening declines in factory activity last month, as a slowdown in exports hit factories.

4. Online Gaming Flutter Entertainment agreed to buy PokerStars owner Stars Group for about $6 billion — FanDuel owner Flutter Entertainment agreed to buy PokerStars owner Stars Group for about $6 billion. The deal creates an online-gambling giant as internet and app-based betting is taking hold in the U.S. It also connects FanDuel with Fox Corp., which owns a minority stake in Stars and recently launched its own betting app, Fox Bet. Fox Corp. and WSJ parent News Corp share common ownership.

Flutter, based in Dublin and listed in London, owns bookie brands in the U.K. including Paddy Power and Betfair. Flutter’s FanDuel, in addition to its fantasy-sports site, offers online and retail betting in New Jersey and Pennsylvania. Nasdaq-listed Stars Group, based in Toronto, owns popular online poker brands such as PokerStars and Sky Betting & Gaming.

The week ahead — Economic data from Econoday.com:

If a speculator is correct half of the time, he is hitting a good average. Even being right 3 or 4 times out of 10 should yield a person a fortune if he has the sense to cut his losses quickly on the ventures where he is wrong. -Bernard Baruch

1. UK Court Decided Suspension of Parliament Unlawful — Prime Minister Boris Johnson acted unlawfully when he suspended Parliament this month for five weeks, according to the British Supreme court, opening the door to new challenges to his Brexit strategy. Sterling rose nearly 0.4% on the back of the decision to trade at $1.2478. The President of the Supreme Court, Brenda Hale, said there was no justification for the government taking such extreme action, but that it was for parliament to decide what to do next.

2. FAA Announces 737 Max Return Up to Individual Countries — each country will make “its own decision” on when the Boeing (NYSE:BA) 737 MAX returns to service, according to FAA Administrator Steve Dickson, who has not yet set a timeline on when to allow the jets back in U.S. skies. The planes have been grounded worldwide since mid-March after two crashes within five months of each other killed 346 people. On Monday, Boeing also announced that it will pay $144,500 to each of the victims’ families from a $50M financial assistance fund.

3. Juul Under Criminal Investigation — Federal prosecutors in California are conducting a criminal probe into e-cigarette maker Juul (JUUL), in which tobacco giant Altria (NYSE:MO) owns a 35% stake, WSJ reports. Regulators have criticized Juul for fueling a teen vaping “epidemic,” while lawmakers have urged the FDA to pull most e-cigarettes off the market. It follows an outbreak of a deadly lung disease linked to vaping that has sickened at least 530 people and killed eight. Massachusett is imposing a four-month ban on sales of all vaping products amid a national health emergency that so far has been linked to nine deaths and has sickened at least 530 people. T

4. Pelosi Announces Impeachment Inquiry into Trump Amid Alleged Abuses of Power — the House started an impeachment inquiry into President Donald Trump as a swell of Democrats denounce the president over alleged abuses of power, House Speaker Nancy Pelosi. Based on past history of Clinton impeachment, the S&P 500 fell as much as 4.9% on October 8, 1998, the day the House voted to begin impeachment proceedings against President Clinton, before trimming losses to end the day down 1.2%. By the time Clinton was acquitted by the Senate in February 1999, the index was up 28%. Markets shrugged off an impeachment inquiry against President Nixon on February 6, 1974, but the S&P 500 fell around 30% until his resignation. There were other forces at play, however, including Nixon’s decision to suspend the gold standard and a recession following the oil shock of late 1973.

5. Amazon Pilots Care Clinics — building on previous healthcare efforts, a new pilot is being launched for Amazon (NASDAQ:AMZN) workers in the Seattle area, offering a virtual primary care clinic with an option to send nurses to employees’ homes. Amazon has already partnered with JPMorgan (NYSE:JPM) and Berkshire Hathaway (BRK.A, BRK.B) – on an effort called Haven – which explores how to move the needle on healthcare expenses for their combined 1.2M employees. In addition, the company has a pharmacy division under PillPack and an R&D group sometimes referred to as Grand Challenge or 1492.

6. IPO Market Weakens — the IPO market took another hit as Endeavor Group Holdings yanked its planned offering and Peloton Interactive’s shares skidded on their first day of trading. The entertainment company became the second big casualty of the IPO market’s recent chill after WeWork’s parent company pulled its offering earlier this month. It is the second time Endeavor has hit the brakes on its IPO this year. Part of the reason Endeavor pulled its deal, according to people familiar with the matter, was the poor performance of Peloton in its debut. Investors soured on shares of Peloton, the startup known for its exercise bikes that allow users to join along in virtual spin classes from home, pushing them 11% below their IPO price of $29.

The week ahead — Economic data from Econoday.com:

© Copyright 2026 Market Outlook All Rights Reserved

Design by EGS

Sponsored by Equity Guidance LLC