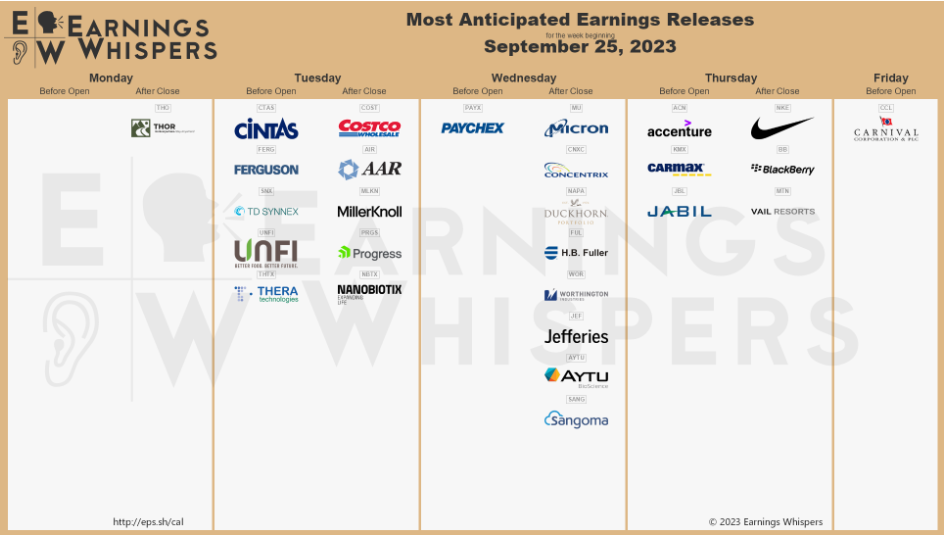

Week of Sept 22, 2023 Weekly Recap & The Week Ahead

Tuesday, September 26th, 2023“If you can keep your head when all about you are losing theirs …

If you can wait and not be tired by waiting …

If you can think – and not make thoughts your aim …

If you can trust yourself when all men doubt you …

Yours is the Earth and everything that’s in it.” — Warren Buffett

1. Kevin McCarthy Hits New Hurdles With Holdout Republicans — House Republican leaders worked to salvage a short-term spending bill that sparked angry disagreements among the party’s rank-and-file, but they remained short of the support needed to pass the measure and show the party could unite to avert a government shutdown. The short-term proposal outlined Sunday by leaders of the hard-right Freedom Caucus and more-centrist Main Street Caucus would fund the government past Sept. 30 and contains an 8% cut in discretionary nonmilitary spending and a border-security provision. But about a dozen lawmakers, some from the Freedom Caucus itself, immediately called the deal a nonstarter, raising questions of whether the proposal would move ahead.

2. Fed Leaves Rates Unchanged, Signals Another Hike This Year — With economic activity stronger than anticipated, most officials also expected they would need to keep interest rates near their current level through next year, according to projections released Wednesday at the conclusion of their two-day policy meeting. Fed officials raised their benchmark federal-funds rate at their previous meeting in July to a range between 5.25% and 5.5%. They began lifting rates from near zero in March 2022.

3. House recesses after Defense bill, government funding plan implode — the House failed to pass a measure that would have set the rules for debate on a Pentagon funding bill, which had been expected to come to the House floor for a final vote later Thursday. During that meeting, Republicans had largely agreed on the rough outlines of a CR that would slash topline government funding well below the levels McCarthy and President Joe Biden agreed to last summer during high-stakes debt ceiling talks.

4. US Existing-Home Sales Fall to Seven-Month Low on Rates, Supply — Sales of previously owned US homes declined in August to the lowest since the start of the year, restrained by limited inventory and historically high mortgage rates.

Contract closings decreased 0.7% from a month earlier to a 4.04 million annualized pace, National Association of Realtors data reported. The median estimate in a Bloomberg survey of economists called for a pace of 4.1 million. Borrowing costs are now hovering around the highest levels in decades, discouraging existing homeowners — many who previously locked in lower mortgage rates — from moving. The combination of high financing costs, diminished inventory and elevated prices has created one of the least affordable housing markets on record.

The week ahead — Economic data from Econoday.com: