Week of Nov 22 2019 Weekly Recap & The Week Ahead

Tuesday, November 26th, 2019“When you learn to let go of the need to be right, being wrong gradually lose its power to disturb you.” — unknown

1. Boeing Tried for Deals at Dubai Air Show — Emirates and Boeing are reportedly on the verge of striking a compromise deal for the Middle East’s biggest carrier to order around 30 787 Dreamliners, but fewer 777X jets as part of a delayed order. Boeing (NYSE:BA) has only landed about a third of the orders scored by Airbus (OTCPK:EADSY, OTCPK:EADSF) at the biennial event. Meanwhile, FAA Administrator Steve Dickson stated on the sidelines of the show that the FAA will be tougher on the certification of the Boeing 777X and isn’t following any specific timeline for the return to service of the grounded 737 MAX model. Overall, Airbus (OTCPK:EADSY) scored 220 plane orders during the closely-watched industry event, while Boeing (NYSE:BA) lagged behind with 95 agreements for commercial jets. Boeing still managed to garner sales for its troubled 737 MAX, scoring a total of 50 deals from Air Astana, SunExpress and an unidentified customer. The French planemaker has been ahead for most of 2019. At the end of October, Airbus had posted 542 net orders vs. Boeing’s 45.

2. Disney Sees $100M ‘Frozen 2’ Debut — Disney (NYSE:DIS) is forecasting a hot debut for long-awaited sequel Frozen 2 when it opens on Friday. The company expects the film to draw $100M or so domestically in its first weekend, while some Hollywood estimates are ranging to as high as $105M. The film is set to debut in more than 4,400 theaters in North America. The first Frozen film is the 2nd highest-grossing animated movie of all-time with a global box office haul of $1.29B.

3. FCC Calls for Public C-band Auction — FCC Chairman Ajit Pai announced his support for a public auction to free up C-band spectrum, a key band currently used for delivering video content for next-generation 5G wireless networks. The news sent Intelsat’s (NYSE:I) stock crashing 40%. Major satellite service providers, which hold existing C-band licenses, had proposed selling the spectrum privately to wireless carriers, arguing a private sale would make the spectrum available for 5G faster.

4. China Invited U.S. for More Trade Talks — Beijing’s chief trade negotiator late last week proposed a new round of face-to-face talks, according to people briefed on the matter, as both sides are struggling to strike a limited deal to help de-escalate tensions.

5. FedEx Discontinues Pension for New Hires — Joining the growing ranks of large U.S. companies phasing out guaranteed retirement benefits, FedEx (NYSE:FDX) said it would close its pension plan to new U.S. hires starting in 2020. The shipping giant instead will launch a new 401(k) plan at the start of 2021 with a higher company match (contributing up to 8% of employee salaries, if employees provide 6% of their salary). Just 22% of Fortune 50 companies and 11% of transportation companies offer pensions to new employees.

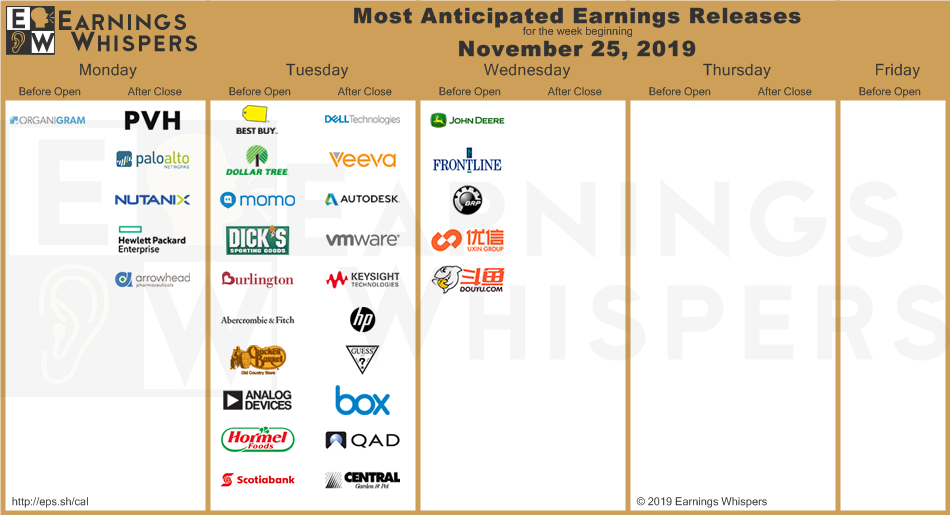

The week ahead — Economic data from Econoday.com: