Week of Sept 21 2018 Weekly Recap & The Week Ahead

Monday, September 24th, 2018“Always something new, always something I didn’t expect, and sometimes it isn’t horrible.” – Robert Jordan

1. U.S. LNG Deliveries to Germany by 2022 — U.S. companies expect to begin delivering LNG to Germany in four years at the latest, according to deputy U.S. energy secretary Dan Brouillette, and will challenge Russia which now accounts for 60% of German gas imports. In July, President Trump accused Germany of being a “captive” of Russia due to its energy reliance and urged it to halt work on the $11B, Russian-led Nord Stream 2 gas pipeline.

2. Aurora Cannabis(OTCQX:ACBFF) on talks with Coca-Cola on CBD drinks — Coca-Cola (NYSE:KO) said it was closely watching the fast-growing marijuana drinks market for a possible entry. Molson Coors (NYSE:TAP) has already announced a joint venture with Hydropothecary to develop cannabis drinks, while Diageo (NYSE:DEO) is in talks with at least three Canadian cannabis producers about a possible deal.

3. SEC subpoenas Goldman, Silver Lake in Tesla probe — the tension continues to build at Tesla (NASDAQ:TSLA) as a DOJ probe runs alongside a wide-ranging SEC investigation. Subpoenas have already been received by Goldman Sachs and Silver Lake, the two firms hired by Tesla to help the company explore Elon Musk’s go-private plan.

4. US/China Tarriff Escalate — President Trump ordered another $200 billion in 10% tariffs on Chinese goods, which could rise to 25% by year end. China retaliated with $60 billion in tariffs at 5% to 10% and Trump threatened $267 billion more.

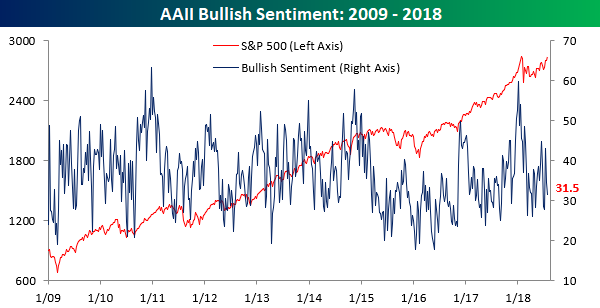

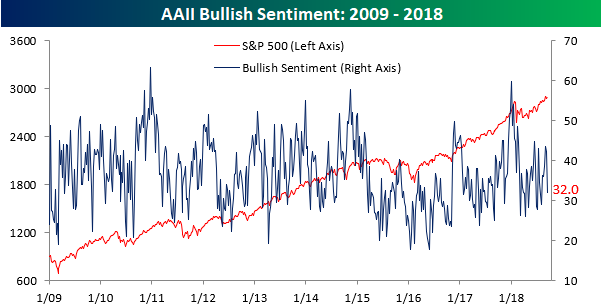

5. AAII Weekly Investor Sentiment — in the latest survey of individual investor sentiment from AAII, bullish sentiment declined (ever so slightly) for the third straight week, dropping from 32.09% down to 32.04%.

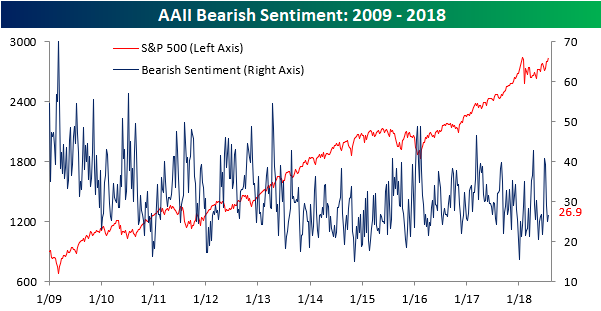

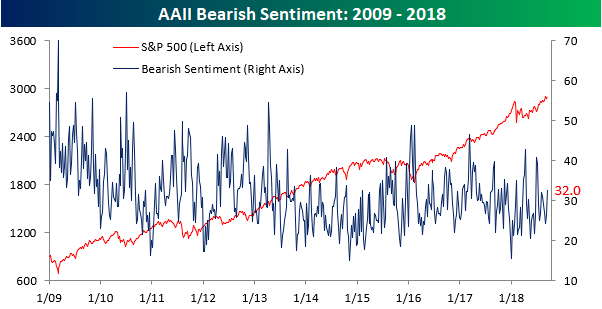

Meanwhile, bearish sentiment came in at the exact same level as bullish sentiment this week, dropping from 32.84% down to 32.04%. The last time both gauges of sentiment were at the exact same level was in June 2016.

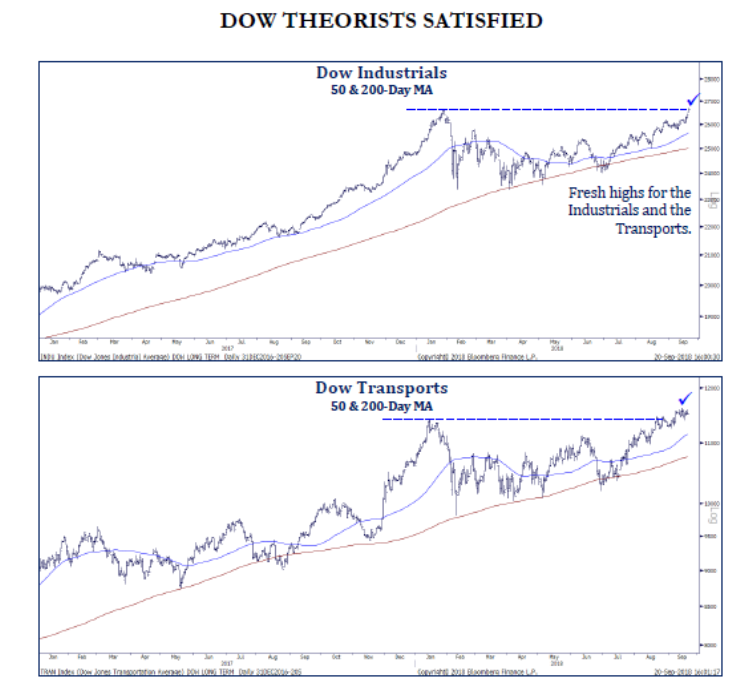

6. Dow Theory Generates Buy Signal for the Dow Theorist Followers — this occurs when the Dow Industrials sets a new high following a new high for Dow Transports. This happened over the last two weeks as industrials set their high on September 21 following transports on September 14. This signal did not work in 2008 as Dow Transports was the last average to peak when it topped out in May 2008 while Dow Industrials peaked in October 2007.

The week ahead — Economic data from Econoday.com: