Week of May 20, 2022 Weekly Recap & The Week Ahead

Tuesday, May 24th, 2022“Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” — Warren Buffett

1. Pfizer’s Covid-19 Booster Cleared for 5- to 11-Year-Olds — the Food and Drug Administration reported that children between the ages of 5 and 11 years old can get a booster dose of BioNTech SE and Pfizer Inc.’s PFE, 1.32% COVID-19 vaccine. Children in this age group should wait at least five months after getting the primary series of shots. The regulator authorized a booster of the BioNTech/Pfizer vaccine for teens back in January. The FDA’s advisory committee did not meet to discuss whether the benefits of a third dose of the BioNTech/Pfizer vaccine outweigh the risks for this age group because the companies’ request for authorization in 5 to 11 year olds “did not raise questions that would benefit from additional discussion by committee members,” according to the regulator.

2. U.S. Retail Sales Grew 0.9% in April — Retail sales—a measure of spending at stores, online and in restaurants—rose a seasonally adjusted 0.9% last month compared with March, the Commerce Department said Tuesday. That marked the fourth straight month of higher retail spending. Consumers spent more at restaurants and bars and boosted expenditures on vehicles, furniture, clothing, and electronics. They cut spending sharply on gasoline in April as pump prices pulled back briefly from a run-up related to the war in Ukraine. In another sign of economic momentum, the Federal Reserve said industrial production, a measure of factory, mining and utility output, increased a seasonally adjusted 1.1% in April—also a fourth month of gains.

3. Treasury Likely to Prevent U.S. Investors From Receiving Russian Debt Payments — the U.S. has carved out an exemption, set to expire on May 25, in its sanctions campaign against Russia to allow for sovereign debt payments. Without it in place, banks and investors won’t be able to process and receive bond payments made by the Kremlin, likely prompting Russia’s first default on its foreign debts since 1918. Russia has managed to stay current on over $2.5 billion in foreign debt payments since the onset of the war with Ukraine, largely thanks to the sanctions carve-out, although the U.S. has steadily tightened Russia’s ability to make payments, including new sanctions in April that cut off the Kremlin’s access to U.S. bank accounts for sovereign debt payments.

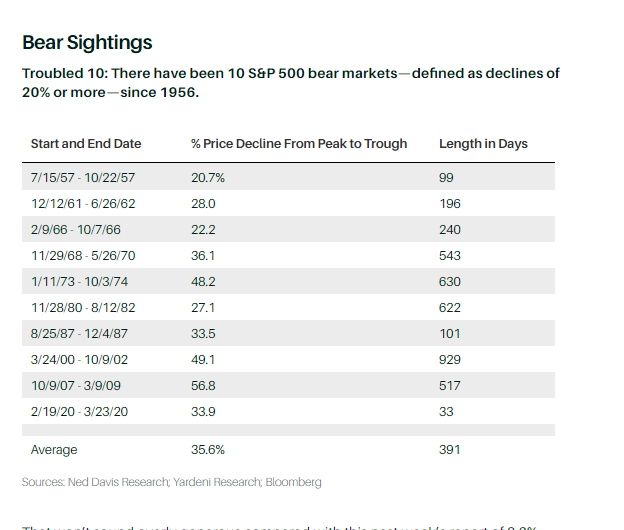

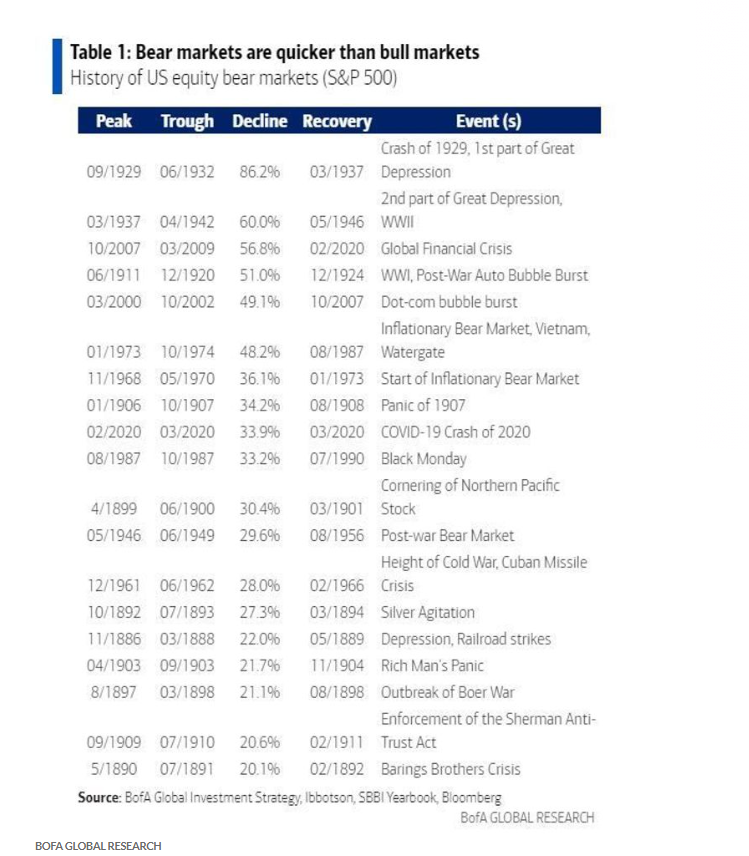

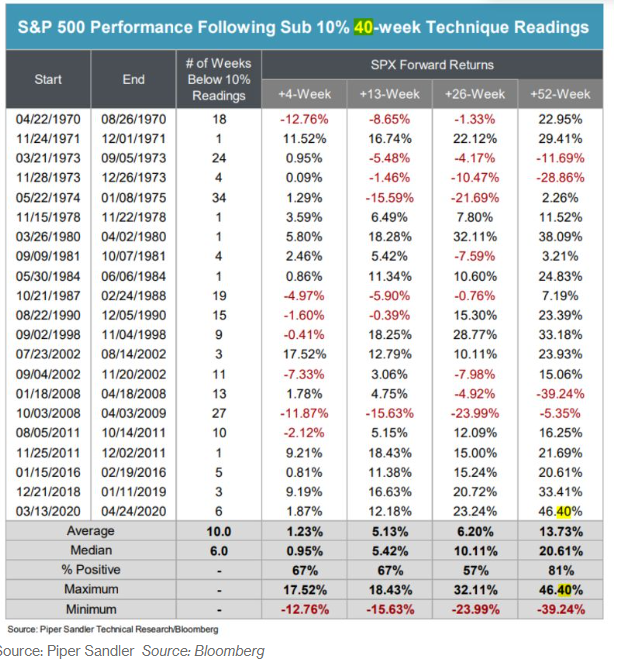

4. S&P 500 Pares Losses After Hitting Bear-Market Territory — the S&P 500 slid so far it was on track to close at least 20% below its January peak—what would have been considered a bear market. A comeback in the final hour of the trading day pushed the index higher. It has been decades since stocks have fallen for such a prolonged period. The Dow industrials notched their eighth straight weekly loss, their longest such streak since 1932, near the height of the Great Depression. The S&P 500 and Nasdaq had their seventh straight weekly loss, their longest such streak since 2001, after the dot-com bubble burst. All three indexes finished the week down at least 2.9%. Below is a chart of SPX performance following Sub 10% corrections.

The week ahead — Economic data from Econoday.com: