Week of Jan 24, 2020 Weekly Recap & The Week Ahead

Tuesday, January 28th, 2020“The secret to being successful from a trading perspective is to have an indefatigable and an undying and unquenchable thirst for information and knowledge.” — Paul Tudor Jones

1. A Newly Identified Virus Originating in Central China has Spread Between Humans — with a diagnostic test available, the number of confirmed cases more than tripled to 218—including in Beijing, Shanghai and Shenzhen—with three deaths from the pneumonia the virus causes. The prospect of human-to-human transmission, rather than just animal-to-human, comes as tens of millions of Chinese crisscross the country for the Lunar New Year holiday—commonly called the world’s largest annual human migration—though more are staying put this year. The virus has already spread outside China, and appeared in South Korea for the first time.

2. France, U.S. Declare Digital Tax Truce — averting another trade war – for now – the U.S. and France have agreed to put aside their digital tax dispute until the end of 2020. Negotiations at the OECD will continue during that period as France postpones the levy and the U.S. delays retaliatory tariffs. The measure had imposed a 3% tax on digital revenues of companies like Google (GOOG, GOOGL), Apple (NASDAQ:AAPL), Facebook (NASDAQ:FB) and Amazon (NASDAQ:AMZN) – which have more than €750M in global revenue, including at least €25M in France – while the U.S. had threatened to place duties of up to 100% on $2.4B of French imports.

3. The Chinese Government Locked Down Cities in an Effort to Stop the Spread of a New Coronavirus — the government locked down Wuhan, the city of 11 million people where the new virus originated. Authorities announced later that nearby Huanggang, with 7.5 million people, was slated for lockdown at midnight. Ezhou, another neighboring city with just over a million residents, said it would enact similar restrictions. Under the lockdowns, all outbound flights, trains, long-distance buses and ferries are halted, and public transportation is shut. Markets, movie theaters and other public places have been closed or had access restricted. The lockdowns constitute a dramatic escalation in the battle to contain a pneumonia outbreak that has killed at least 17 people.

4. Boeing CEO Updates — the new Boeing (NYSE:BA) CEO said the planemaker will not cut its dividend despite the extended grounding of the 737 MAX and expects to resume MAX production “months” before the mid-year return to service. The latest delay was triggered by the company’s recommendation that pilots should undergo simulator training. He’ll also “start with a clean sheet of paper” on a decision whether to launch a new midsize airplane seating 220-270 passengers, effectively halting current plans worth $15B-20B.

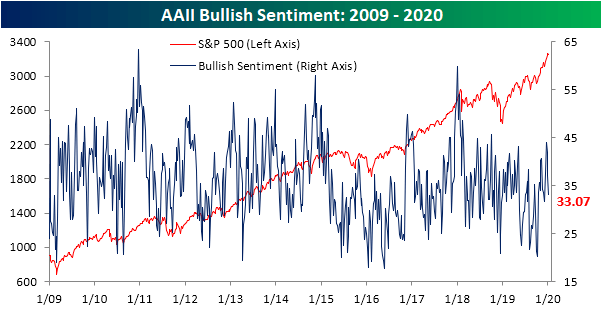

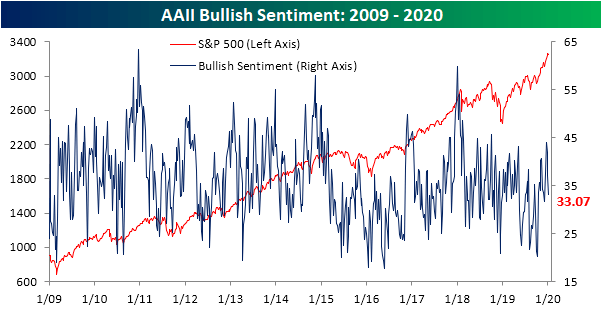

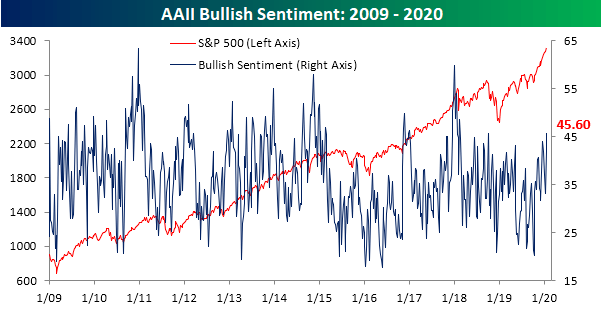

5. AAII’s Investor Sentiment Survey — In the span of just two weeks, the percentage of respondents in AAII’s investor sentiment survey reporting as bullish has risen from the middle of the past few years’ range of 33.07% to 45.6% (and from 41.83% last week), the highest reading since early October 2018. Back then, bullish sentiment peaked out just slightly higher at 45.66%, before turning lower as stocks sharply sold off.

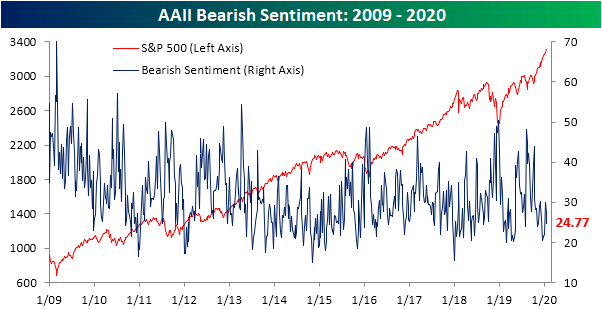

In spite of the strong bullish reading, bearish sentiment was actually lower in the final weeks of 2019 and the first week of this year. Now at 24.77%, bearish sentiment is low but still within a normal range of one standard deviation of the past year’s average of 30.04%.

The week ahead — Economic data from Econoday.com: