Week of Feb 22 2019 Weekly Recap & The Week Ahead

Monday, February 25th, 2019“ . . . A man has rigged up a turkey trap with a trail of corn leading into a big box with a hinged door. The man holds a long piece of twine connected to the door that he can use to pull the door shut once enough turkeys have wandered into the box. However, once he shuts the door, he can’t open it again without going back into the box, which would scare away any turkeys lurking on the outside. One day he had a dozen turkeys in his box. Then one walked out, leaving eleven. ‘I should have pulled the string when there were twelve inside,’ he thought, ‘but maybe if I wait, he will walk back in.’ While he was waiting for his twelfth turkey to return, two more turkeys walked out. ‘I should have been satisfied with the eleven,’ he thought. ‘If just one of them walks back, I will pull the string.’ While he was waiting, three more turkeys walked out. Eventually, he was left empty-handed. His problem was that he couldn’t give up the idea that some of the original turkeys would return . . . ” — Fred C. Kelly

1. Europe Trans-Atlantic Trade in Question — European Commission chief Jean-Claude Juncker spoke in Stuttgart – the hometown of Daimler (OTCPK:DDAIF) – after the U.S. Commerce Department sent a report to President Trump that could unleash steep tariffs on imported vehicles. “Trump has given me his word that there will be no car tariffs for the time being,” Juncker declared. “I believe him. However, should he renege on that commitment, we will no longer feel bound by our commitments to buy more U.S. soya and liquid gas.”

2. Payless Bankruptcy to Begins shuttering U.S. stores — Payless ShoeSource began closing its 2,700 U.S. stores on Sunday and filed for its second bankruptcy in two years. The latest retail victim may point to storm clouds hovering over the industry, or possible positive developments for Caleres (NYSE:CAL) and DSW (NYSE:DSW) due to a narrowed shoe store field. Toys “R” Us, Shopko, FullBeauty Brands, Charlotte Russe, Things Remembered and Gymboree (OTC:GMBEQ) have all filed for bankruptcy in the past year.

3. Facebook Plans to Develop AI Chips — FB also wants to develop its own artificial intelligence chips that go beyond what’s currently on the market, according to Yann LeCun, Facebook’s (FB) chief AI scientist. While the company is already creating its own custom ASIC (application-specific integrated circuit) chip, the idea is to provide faster computing that Facebook (needs in order to achieve new AI breakthroughs including digital assistants imbued with enough “common sense.”

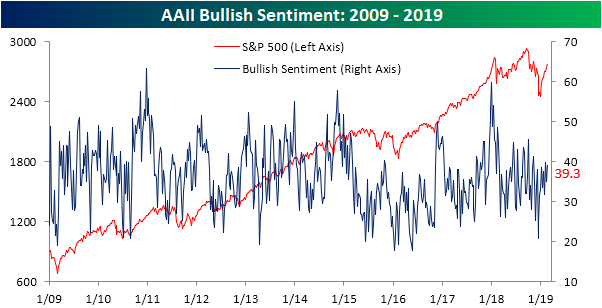

4. AAII Investor Sentiment Latest Survey — in the latest survey, investor sentiment showed growing optimism but nothing extreme. Bullish sentiment was up a little over 4% to 39.32%, and while not particularly high, the percentage of bulls now sits at the upper end of the range the sentiment reading has been at over the past couple months.

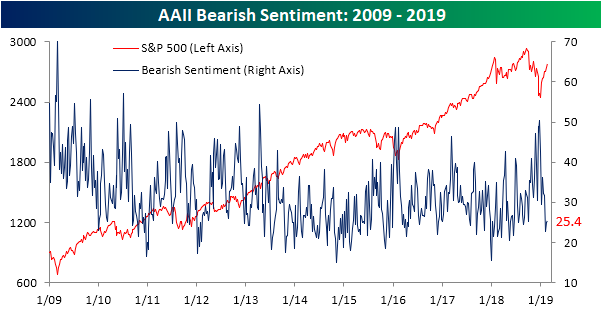

Meanwhile, bearish sentiment held steady, rising ever so slightly to 25.39% from 25.07% last week. The percentage of bearish investors has come way off of its highs from the late 2018 sell-off and is sitting at the lower end of the range that has been observed in the past year.

5. Latest Fed Minutes Show Division on Rate Hikes — the latest minutes from the Fed’s last meeting reaffirmed that the U.S. central bank would be “patient” with respect to further interest rate hikes. Most FOMC officials also indicated they were ready to stop shrinking the central bank’s $4.1T asset portfolio this year and believed an action plan should be released soon.

The week ahead — Economic data from Econoday.com: