July 30th, 2024

In order of importance to me are: 1) the long term trend, 2) the current chart pattern, and 3)picking a good spot to buy or sell.

Ed Seykota

1. U.S. Home Prices Hit Record in June for Second Consecutive Month — the spring home-buying season, usually the busiest time of year for the housing market, was a dud this year. Home sales declined in June for the fourth straight time on a monthly basis. The combination of high prices and elevated mortgage rates has made homeownership less attractive to renters and deterred current homeowners from moving. But low inventory of homes for sale in much of the country is pushing prices higher. The national median existing-home price in June rose to $426,900, a record in data going back to 1999 and a 4.1% increase from a year earlier, the National Association of Realtors said Tuesday. Prices aren’t adjusted for inflation. Sales of previously owned homes in June fell 5.4% from the prior month to a seasonally adjusted annual rate of 3.89 million, NAR said. On an annual basis, existing-home sales, which make up most of the housing market, also fell 5.4%.

2. US New-Home Sales Unexpectedly Decline to a Seven-Month Low — Contract signings on new single-family homes decreased 0.6% to a 617,000 annual pace, the slowest since November, according to government data released Wednesday. The figure compared with a 640,000 median estimate in a Bloomberg survey of economists. The latest figures follow a topsy-turvy first half of the year, with sales gaining ground throughout the spring before slumping in May by the most in nearly a year. Thirty-year mortgage rates have dipped below 7% in recent weeks, but remain double what they were at the end of 2021, encouraging many builders to offer sales incentives such as buying down customers’ mortgages. Meantime, builders have continued to add supply, with inventory edging up to 476,000 homes in June, still the most since 2008. At the current rate of sales, that inventory would last 9.3 months, the longest since October 2022.

3. US Economy Grew Faster Than Expected Last Quarter on Firm Demand — Real gross domestic product, a measure of all the goods and services produced during the April-through-June period, increased at a 2.8% annualized pace adjusted for seasonality and inflation. Economists surveyed by Dow Jones had been looking for growth of 2.1% following a 1.4% rise in the first quarter. Consumer spending helped propel the growth number higher, as did contributions from private inventory investment and nonresidential fixed investment, according to the first of three estimates the department will provide. Personal consumption expenditures, the main proxy in the Bureau of Economic Analysis report for consumer activity, increased 2.3% for the quarter, up from the 1.5% acceleration in Q1. Both services and goods spending saw solid increases for the quarter.

4. U.S. Inflation Data Keeps Door Open For September Interest Rate Cut — the Department of Commerce said Friday its personal income expenditures inflation gauge rose 2.5% in June compared to a year earlier, slowing for its 2.6% pace in May. Excluding volatile food and energy prices, PCE inflation rose 2.6%, the same as in May. Following the data release, Treasury yields declined in an indication of investors’ increasing expectations that monetary easing is about to start. The 10-year yield was recently at 4.20%. The Federal Reserve targets 2% inflation and the PCE is its preferred gauge. The U.S. central bank is widely expected to keep rates at current high levels next Wednesday, while opening the door wider for a cut in September.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

July 22nd, 2024

“Great traders aren’t born or made overnight. It takes patience, discipline and consistency to master the art of trading” — unknown

1. US Retail Sales Excluding Autos Rise by Most in Three Months — Retail purchases less motor vehicles rose 0.4% last month after an upwardly-revised 0.1% advance in May. Total retail sales were unchanged, restrained by a 2% slide in receipts at auto dealers. The figures aren’t adjusted for inflation. Of the 13 categories tracked by the Commerce Department, only three registered declines. Those included sales of gasoline, reflecting lower prices in the month. Sales at sporting goods stores also edged lower. Excluding receipts at filling stations and auto dealers, retail sales jumped 0.8% — the most since the start of 2023. Non-store retailers led the gains, recording their strongest advance in three months. Sales at health and personal care stores rose by the most since October, while sales at building material and garden equipment stores increased by the most since February.

2. Fed’s Beige Book Shows Slight Economic Growth, Cooling Inflation — The US economy grew at a slight pace heading into the third quarter, with a number of regions noting flat or declining activity, the Federal Reserve said in its Beige Book survey of regional business contacts.

Employment also increased only slightly, according to the report Wednesday. Labor turnover declined, and contacts in several districts expect to be more selective about who they hire and not backfill all open positions. Of the districts, five noted flat or declining economic activity — three more than the prior period. Looking ahead, businesses expected the slowing to continue.

3. ECB Holds Rates Steady With More Data Needed for Next Cut — The deposit rate was kept at 3.75% on Thursday — as all 55 economists in a Bloomberg survey predicted. The ECB reiterated that borrowing costs will remain “sufficiently restrictive for as long as necessary” to ensure inflation returns to 2%. The ECB is weighing whether euro-zone inflation is cooling sufficiently to allow further monetary loosening. Last month saw a small dip to 2.5% from 2.6%, and while underlying pressures held firm and the advance in services costs again topped 4%, the ECB on Thursday cited “one-off factors” in explaining the move.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

July 16th, 2024

“You need to know very well when to move away, or give up the loss, and not allow the anxiety to trick you into trying again.” – Warren Buffett1.

1. Powell Inches the Fed Closer to Cutting Rates — Federal Reserve Chair Jerome Powell made a subtle but important shift that moved the central bank closer to lowering interest rates when he suggested Tuesday that a further cooling in the labor market could be undesirable. Powell conceded that he wouldn’t have arrived at such a judgment as recently as two months ago—and indeed, the Fed leader was more measured in comments made at a conference in Portugal last week, before the release of the June employment report by the Labor Department. Behind the shifting outlook is labor-market data showing a slowdown in hiring and a mild but steady increase in the share of Americans looking for work amid an increase in the workforce, due partly to more immigration.

2. Biden Tightens Trade Rules for Steel, Aluminum From Mexico — The U.S. will levy a 25% tariff on Mexican imports containing steel from China and a 10% duty on products made with aluminum from the country, the White House said. Products from Mexico typically enter the U.S. duty free as part of a trade agreement with Canada and Mexico. Steel and aluminum must be melted and poured in the U.S., Mexico or Canada to qualify for duty-free treatment, according to the White House.

U.S. steelmakers and other manufacturers have complained that China is circumventing the existing tariffs on steel and aluminum by routing the metals through Mexico. The U.S. government has said steel and aluminum exported from China are unfairly priced and benefit from unlawful government subsidies.

3. Milder Inflation Opens Door Wider to September Rate Cut — The consumer-price index, a measure of goods and services costs across the economy, fell slightly from May, dropping the year-over-year inflation rate to 3%, which was the lowest since June 2023. Core prices, which exclude volatile food and energy items and are seen as a better gauge of underlying inflation, rose just 0.1% since May. That was the mildest increase since January 2021, when large swaths of the economy were still frozen by the pandemic.

Altogether, the report showed prices cooled broadly in the second quarter and were below economists’ expectations—the reverse of what happened in the first three months of the year, when inflation was surprisingly brisk. The report keeps the door wide open to a September interest-rate cut. Earlier this week, Fed Chair Jerome Powell laid the groundwork to cut by suggesting the labor market is slowing in a way that has diminished a major source of inflation and risks further weakness that wouldn’t be desirable.

4. Wholesale prices rose 0.2% in June, slightly hotter than expected — The producer price index climbed 0.2% last month, the Labor Department’s Bureau of Labor Statistics reported Friday. Economists surveyed by Dow Jones were expecting a 0.1% increase for the index. The PPI is now up 2.6% over the past year.

The PPI is a gauge of prices that producers can get for their goods and services in the open market. In June, a rise in the price for services offset a decline for goods. The hotter-than-expected PPI reading runs counter to recent data that shows inflation declining, though economists and investors tend to put more weight on the consumer-focused inflation readings. The central bank’s next policy meeting is at the end of July, where it is widely expected to hold rates steady. Traders have increasingly dialed in on the September meeting as the likely time for the first rate cut.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

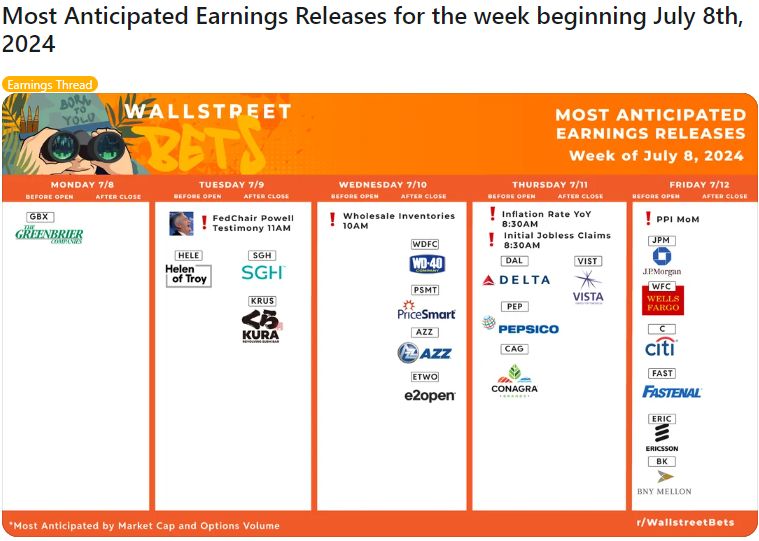

July 9th, 2024

“Happy July 4th On This Shorten Holiday Week — Do More of What Works and Do Less of What Doesn’t”

1. Private payrolls grew by just 150,000 in June, less than expected — Private payroll growth edged lower in June, according to a report Wednesday from ADP that indicates a potential slowdown in the U.S. labor market. Companies added 150,000 jobs for the month, below the upwardly revised 157,000 in May and the Dow Jones consensus estimate for 160,000. The total was the lowest monthly gain since January.

Without the surge in leisure and hospitality hiring, the total would have been considerably lower. The sector added 63,000 jobs, easily the biggest gain among the categories that payrolls processing firm ADP measures.

2. U.S. economy added 206,000 jobs in June, unemployment rate rises to 4.1% — Nonfarm payrolls increased by 206,000 for the month, better than the 200,000 Dow Jones forecast though less than the downwardly revised gain of 218,000 in May, which was cut sharply from the initial estimate of 272,000. The unemployment rate unexpectedly climbed to 4.1%, tied for the highest level since October 2021 and providing a conflicting sign for Federal Reserve officials weighing their next move on monetary policy. The forecast had been for the jobless rate to hold steady at 4%. A broader unemployment rate which counts discouraged workers and those holding part-time jobs for economic reasons held steady at 7.4%. Household employment, which is used to calculate the unemployment rate, rose by 116,000. The household survey also showed a decrease of 28,000, in full-time workers and an increase of 50,000 in part-time workers.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 30th, 2024

“The biggest investing errors come not from factors that are informational or analytical, but from those that are psychological. Investor”

― Howard Marks

1. US Consumer Confidence Declines on Weaker Outlook for Economy — The Conference Board’s gauge of sentiment decreased to 100.4 from a downwardly revised 101.3 reading in May, data out Tuesday showed. The median estimate in a Bloomberg survey of economists called for a reading of 100.

June’s measure of expectations for the next six months fell nearly 2 points to 73, while present conditions increased from a downwardly revised May reading. Confidence has been subdued over the past few years as consumers contend with a higher cost of living, elevated borrowing costs and, more recently, a softening in the labor market. Only 12.5% of consumers expect business conditions to improve in the next six months, the smallest share since 2011.

2. McDonald’s Says Plant-Based Test Didn’t Pan Out in US — A test of its McPlant burger in San Francisco and Dallas “was not successful in either market,” Joe Erlinger, the chain’s US chief, said at the Wall Street Journal’s Global Food Forum in Chicago. That test wrapped up in 2022, the company said following the remarks. Instead of plant-based options, McDonald’s is investing in its chicken offerings as consumers lean toward that protein. The company sells more chicken than beef these days, he added.

3. GDP growth at slowest since 2022 — the American economy expanded at a 1.4% annual pace from January through March, the slowest quarterly growth since spring 2022, the government said Thursday in a slight upgrade from its previous estimate. Consumer spending grew at just a 1.5% rate, down from an initial estimate of 2%, in a sign that high interest rates may be taking a toll on the economy. The Commerce Department had previously estimated that the gross domestic product — the economy’s total output of goods and services — advanced at a 1.3% rate last quarter. After growing at a solid annual pace of more than 3% in the second half of 2023, consumer spending decelerated sharply last quarter. Spending on appliances, furniture and other goods fell by a 2.3% annual rate, while spending on travel, restaurant meals and other services rose at a 3.3% rate.

4. Slowing U.S. Inflation Fuels Expectations of Interest Rate Cuts — The core Personal Consumption Expenditures Price Index, which excludes volatile energy and food prices, increased 2.6% from a year ago, slowing from April’s 2.8% pace. The reading met the consensus of economists surveyed by The Wall Street Journal.

Core PCE inflation rose 0.1% in the month, compared to a 0.2% increase in April. The headline 12-month reading was 2.6%, slowing from April’s 2.7% pace. In the month, the PCE was flat after rising 0.3% in April, marking the first time consumer prices didn’t go up in six months. June PCE inflation is due July 26, just ahead of the next rate-setting Fed meeting on July 30- 31.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 24th, 2024

Do more of what works and less of what doesn’t.

1. US Retail Sales Stall, Showing Signs of Consumer Strain — Sales rose just 0.1% on the month, one-tenth of a percentage point below the Dow Jones estimate, according to a Commerce Department report Tuesday that is adjusted for seasonality but not inflation. However, the result was slightly better than the downwardly revised 0.2% decline in April.

On a year-over-year basis, sales rose 2.3%. The sales number was worse when excluding autos, with a decline of 0.1% against the estimate for a 0.2% increase. The report comes with investors on edge about the direction of the economy and what that will mean for the future of monetary policy at the Federal Reserve. Consumer spending is responsible for about two-thirds of all economic activity, so any weakness could signal a retrenchment in growth while also pushing the Fed to begin cutting interest rates.

2. Biden Gives Legal Status to Immigrant Spouses of U.S. Citizens — President Biden announced a new immigration program Tuesday that provides a path to citizenship for hundreds of thousands of immigrants in the country illegally who are married to U.S. citizens. Biden plans to promote the announcement at the White House alongside members of Congress, immigration advocates and U.S. citizens who, because of arcane immigration rules, haven’t been able to sponsor their spouses for green cards. The program has the potential to benefit immigrants who have been living in the country at least a decade, offering them work permits, deportation protections—and a route for them to apply for green cards, which is the pathway to citizenship.

3. New US Home Construction Plunges to Slowest Pace Since June 2020 — New home construction in the US slumped in May to the slowest pace in four years, as higher-for-longer interest rates sap the housing industry’s momentum from earlier this year. Housing starts decreased 5.5% to a 1.28 million annualized rate last month, according to government data released Thursday. The figure was below all but one estimate in a Bloomberg survey of economists.

Building permits, which point to future construction, fell 3.8% to a 1.39 million annual rate, also the weakest since June 2020. The declines in starts and permits were broad across multifamily and single-family units. Authorized permits for single-family homes dropped for a fourth straight month to the slowest pace in a year.

4. U.S. Business Activity Grows as Europe Recovery Slows — The S&P Global U.S. Composite Purchasing Managers Index—which gauges activity in the manufacturing and services sectors—rose to 54.6 in June from 54.5 in May, marking a 26-month high. A level over 50 indicates expansion in private-sector activity. S&P Global’s composite Purchasing Managers Index for the eurozone, a measure of activity in its services and manufacturing sectors, fell to 50.8 in June from 52.2 in May. A reading above 50.0 points to an increase in activity, while a reading below that threshold points to a decline.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

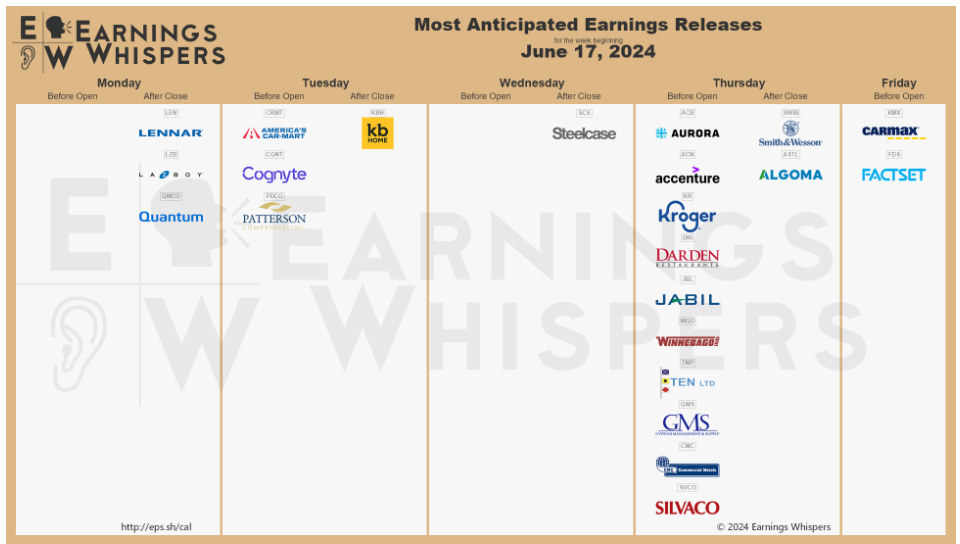

June 18th, 2024

“Yesterday’s home runs don’t win today’s games.” …

1. Inflation slows in May, with consumer prices up 3.3% from a year ago — The CPI, a broad inflation gauge that measures a basket of goods and services costs across the U.S. economy, held flat on the month though it increased 3.3% from a year ago, according to the department’s Bureau of Labor Statistics. Excluding volatile food and energy prices, core CPI increased 0.2% on the month and 3.4% from a year ago, compared with respective estimates of 0.3% and 3.5%. Though the top-line inflation numbers were lower for both the all-items and core measures, shelter inflation increased 0.4% on the month and was up 5.4% from a year ago. Housing-related numbers have been a sticking point in the Federal Reserve’s inflation battle and make up a heavy share of the CPI weighting.

Price increases were held in check, though, by a 2% drop in the energy index and just a 0.1% increase in food. Within the energy component, gas prices tumbled 3.6%. Another nettlesome inflation component, motor vehicle insurance, saw a 0.1% monthly decline though was still up more than 20% on an annual basis.

2. Fed Projects Just One Cut This Year Despite Mild Inflation Report — Federal Reserve officials penciled in just one interest-rate cut for this year, indicating most are in no hurry to lower rates, even after a widely watched report Wednesday showed inflation improved last month. The central bank also held its benchmark rate steady, in a range between 5.25% and 5.5%, a move that was widely expected. New economic projections showed 15 of 19 officials expect the Fed to cut rates this year, with that group roughly split between one or two rate cuts. The median, or midpoint, of those projections reflected expectations of one rate cut.

3. Import prices fall sharply in another sign of fading U.S. inflation — The import price index dropped 0.4% last month. Economists polled by the Wall Street Journal has forecast no change. Lower gasoline prices played a big role, but if energy is excluded, import prices still fell 0.3, the government said. The cost of imports shot up in the first four months of the year after a long period of decline, contributing to a mini-surge in U.S. inflation.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

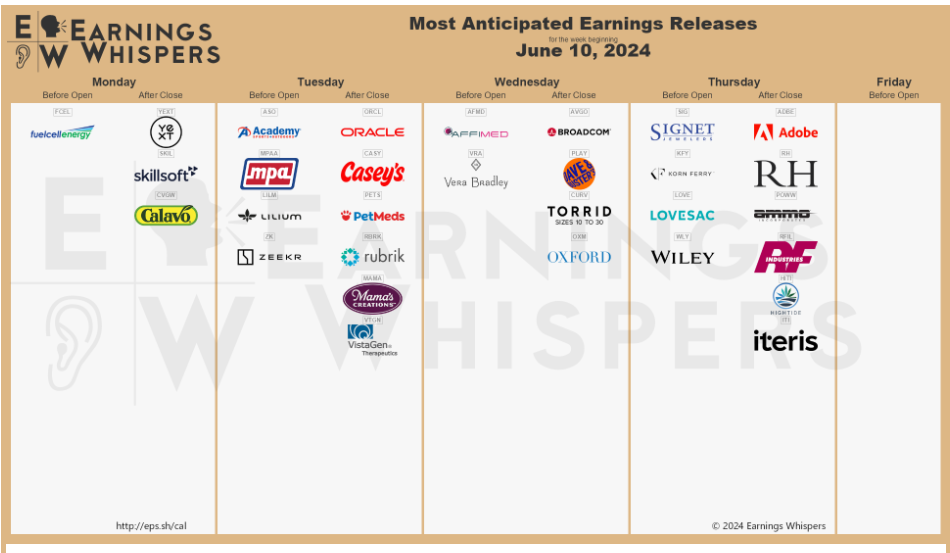

June 11th, 2024

“Wide diversification is only required when investors do not understand what they are doing.” – Warren Buffett

1. Job openings fall to lowest level since February 2021 — latest data from the Bureau of Labor Statistics released Tuesday showed there were 8.06 million jobs open at the end of April, a decrease from the 8.35 million job openings in March. March’s figure was revised lower from the 8.48 million open jobs initially reported. Economists surveyed by Bloomberg had expected the report to show 8.35 million openings in April. The Job Openings and Labor Turnover Survey (JOLTS) survey also showed 5.6 million hires were made during the month, little changed from March.

2. Boeing’s Starliner Launches NASA Astronauts After Setbacks — the space capsule, carrying astronauts Barry Wilmore and Sunita Williams, was launched Wednesday at 10:52 a.m. ET from Cape Canaveral, Fla. A NASA livestream showed Starliner shooting toward space after the flight began. The launch marked a major step forward for a program that had been slowed by repeated technical problems, and exacted a financial toll on Boeing. A successful mission would pave the way for NASA to have a second U.S. option for handling astronaut missions to the International Space Station, with Elon Musk’s SpaceX carrying out crewed flights for the agency since 2020. Starliner’s next steps include docking with the space station and, as soon as June 14, returning to Earth under parachutes. “There’s a lot of phases to this mission, and we just completed the first one,” Mark Nappi, a Boeing vice president overseeing the Starliner program, said at the briefing.

3. ECB Cuts Interest Rates for First Time Since 2019 — the ECB said it would reduce its key interest rate to 3.75% from 4%, its first rate cut in almost five years. Future interest-rate decisions will be based on incoming economic data, the bank said in a statement. The ECB’s rate-setting committee “is not pre-committing to a particular rate path,” the bank said. The rate cut is a significant moment for investors and the world economy. It marks an inflection point in recent monetary policy and sends a signal that relief is on the way for households, indebted governments and businesses that have reined in investments in the face of high borrowing costs.

The cut also potentially puts the ECB and the Fed on different tracks and widens an existing gap in borrowing costs between the U.S. and Europe. While this could boost Europe’s growth in the short term, the gap could also complicate the work of policymakers, especially in Europe.

4. Hiring Defied Expectations in May, With 272,000 New Jobs — Total nonfarm U.S. jobs increased a seasonally adjusted 272,000 jobs in May, the Labor Department reported on Friday, more than in April and well above the 190,000 that economists had expected. Average hourly earnings also topped forecasts, rising 4.1% from a year earlier. In a report that was otherwise strong almost across the board, the one caveat was the unemployment rate, which ticked up from 3.9% in April. It was the first time in more than two years that the jobless rate hit 4%.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 4th, 2024

There will not be any re-cap for the week of May 24th through May 31st, 2024. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

Posted in Weekly Summary | No Comments »

May 20th, 2024

“If you have an approach that makes money, then money management can make the difference between success and failure… … I try to be conservative in my risk management. I want to make sure I’ll be around to play tomorrow. Risk control is essential.” – Monroe Trout

1. Biden Announces Tariffs on $18 Billion of Chinese Imports — The Biden administration said it would impose new tariffs on $18 billion of Chinese imports—a move it says will protect U.S. businesses but could put new pressure on prices as the election looms. The tariff rate on certain steel and aluminum products will increase to 25% from a range of zero to 7.5%. Tariffs on semiconductors will double to 50% by 2025, while those on solar cells will do the same this year. The levy on Chinese electric vehicles will quadruple to 100% in 2024, while those on lithium-ion batteries will increase to 25% from 7.5%. Medical products, such as syringes and needles, and ship-to-shore cranes will also see new or increased tariffs.

2. US Producer Prices Top Forecasts — The producer price index for final demand increased 0.5% from a month earlier, driven largely by services and following a downwardly revised 0.1% drop in March, Bureau of Labor Statistics data showed Tuesday. Compared with a year ago, the PPI rose by the most since April 2023. Among those, the cost of hospital outpatient care fell 0.1% and airfares dropped 3.8%. Prices for physician care rose modestly. At the same time, prices for portfolio management services increased 3.9%. The April PCE price gauge is due later this month.

3. Inflation Eases as Core Index Hits Lowest Level Since 2021 — The consumer-price index, a gauge for goods and service costs across the U.S. economy, rose 3.4% in April from a year ago, the Labor Department said Wednesday. So-called core prices that exclude volatile food and energy items climbed 3.6% annually, the lowest increase since April 2021. Both figures were in line with economists’ expectations. Because it will likely take another two reports to shore up officials’ confidence that inflation can return to the lower levels that prevailed before the pandemic, the Fed might not be ready to cut interest rates before September. Price pressures remain for millions of Americans. Gasoline prices pushed up overall inflation, while consumers continued paying more for housing in April. But year-over-year rent increases slowed from a month earlier, a key sign for economists that a big driver of inflation in recent years is slowly easing.

Costs of groceries and vehicles also edged lower in April from the previous month, while price increases for medical care slowed.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

Posted in Weekly Summary | No Comments »