Week of June 5 ’26 Weekly Recap & The Week Ahead

Thursday, June 11th, 2026“Do More of What Works and Less of What Doesn’t” — unknown

1. Trump Begins Rebuilding His Tariff Wall, Citing Forced Labor — The US is proposing new tariffs of at least 10% on imports from 60 trading partners in President Donald Trump’s biggest move to rebuild his protectionist wall since his earlier levies were struck down by the Supreme Court. Products from other major economies, including China, India, Japan, South Korea, Brazil and Switzerland, would be subject to a 12.5% levy. Beijing denied the allegations and criticized Trump’s move, while an official in Tokyo said Japan is in close contact with counterparts in Washington about the matter. The EU called it unjustified and added that the bloc would respect the terms of its trade accord with the US.

2. US Small Business Hiring Plans Drop to Lowest Since May 2020 — A seasonally adjusted 9% of owners plan to create new jobs in the next three months, down 4 percentage points from April, and the share reporting they had job openings they couldn’t fill fell by 5 percentage points to 29%, the NFIB said in a release Thursday. Both measures were the lowest since May 2020. The NFIB figures are at odds with Bureau of Labor Statistics data released Tuesday showing US job openings jumped in April to the highest level in almost two years — led by a record monthly increase in postings by establishments with fewer than 10 employees. The report suggests rising energy costs and economic uncertainty amid the ongoing Iran war may be weighing on expansion plans.

3. US Hiring Surged in May, Boosting Bets on Fed Rate Hike — Nonfarm payrolls increased 172,000 last month after upward revisions to the prior two months, according to Bureau of Labor Statistics data out Friday. That marked the strongest three-month advance in more than two years. The figures boosted bets that the Federal Reserve will consider an interest-rate increase this year in order to contain inflation. The report suggests the labor market is firming across multiple sectors after near-zero job growth last year, despite more recent concerns about rising energy prices that have driven consumer sentiment to a record low..

4. SpaceX IPO Is Said to Draw More Orders Than Shares Available — The IPO for Elon Musk’s rocket, satellite and artificial intelligence company is oversubscribed after one-on-one meetings between the company and institutional investors, one of the people said, asking not to be identified as the information isn’t public. The Starbase, Texas-based company is offering about 555.6 million shares at $135 each in a deal that could value it at roughly $1.8 trillion. The deal is expected to price June 11 and begin trading the following day, and remains very early in the marketing process, the people said. Deliberations are ongoing and details could change, the people said. A spokesperson for SpaceX didn’t immediately respond to a request for comment.

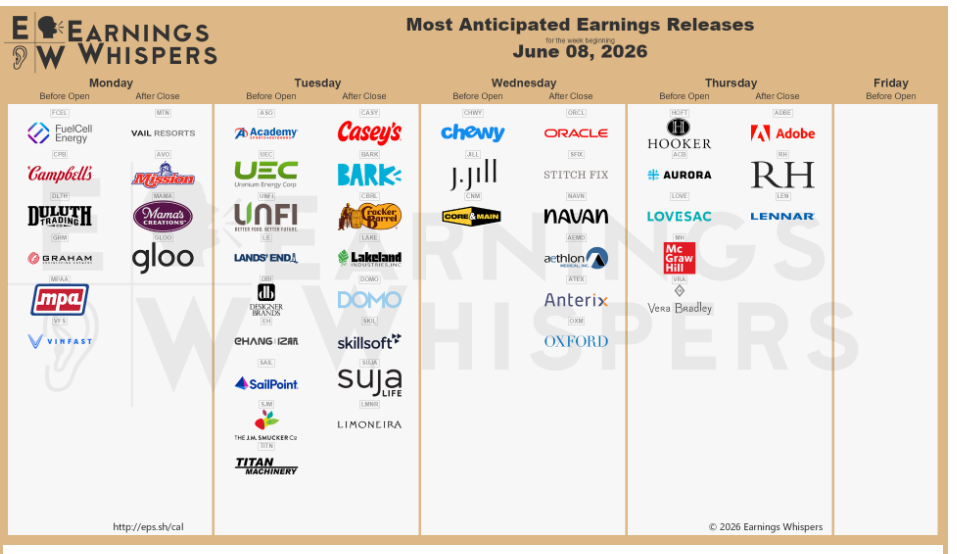

The week ahead — Economic data from Econoday.com: