Week of Dec 27 2019 Weekly Recap & The Week Ahead

Monday, December 30th, 2019‘Taken together, conditions today are characteristic of those that precede a Minsky Moment, in which excessive speculation and taking on additional credit risk during stable markets leads to a tipping point that leads to a period of instability.’ — Scott Minerd, Guggenheim Partners

HAPPY HOLIDAY & WISHING OUR VIEWERS A HAPPY, HEALTHY AND PROPEROUS NEW YEAR

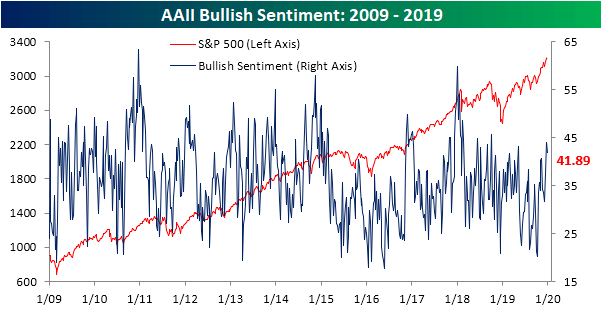

1. AAII Weekly Sentiment — as the major indices continue to establish fresh record highs in the past week with the Nasdaq eyeing an eleventh consecutive up day today, sentiment has actually not shared in moving higher. The reading on bullish sentiment from the AAII fell this week, down to 41.89% from 44.1% last week. Although it is still elevated, currently in the 96th percentile of the past year’s readings, bullish sentiment is less extended than last week and is now back within one standard deviation of its historical average.

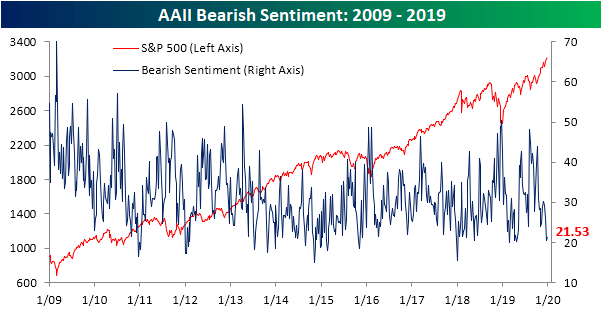

Meanwhile, Bearish sentiment rose just about 1 percentage point this week to 21.53%. As with bullish sentiment, while off of the lowest levels, bearish sentiment is still low relative to where things have stood recently, with this week’s print in the bottom decile of the past year’s readings.

2. Boeing CEO Resigned, Counselor Retires — J. Michael Luttig, who has been managing legal matters associated with the Lion Air and Ethiopian Airlines crashes, will retire from Boeing (NYSE:BA) at year-end. Luttig served as the planemaker’s general counsel since 2006 and assumed his current responsibilities in May 2019. While earlier in the week, CEO Dennis Muilenburg resigned in the wake of the 737 MAX crisis. “The board decided that a change in leadership was necessary to restore confidence in the company moving forward as it works to repair relationships with regulators, customers, and all other stakeholders,” according to a press release. Muilenburg will be replaced by Boeing Chairman David Calhoun, effective January 13, 2020 (CFO Greg Smith will serve as interim CEO during the brief transition period).

3. Super Saturday Sales Top Black Friday by 10% — U.S. consumers are setting more holiday shopping records, as job growth and fatter wallets, along with stronger household finances, have put many in a buying mood this season. Marking the biggest single day in U.S. retail history, Super Saturday (12/21) sales reached $34.4B, topping Black Friday’s $31.2B by 10%, according to Customer Growth Partners. Figures were paced by the ‘Big Four’ mega retailers – Walmart (NYSE:WMT), Amazon (NASDAQ:AMZN), Costco (NASDAQ:COST) and Target (NYSE:TGT) – while online spending this season has so far accounted for 58% of sales growth from a year earlier.

4. China to Cut Tariffs on Range of Goods — China said it will reduce tariffs from Jan. 1 on more than 850 goods, including frozen pork, high-tech components and vital medicines, leading the Shanghai Composite Index to tumble 1.4% overnight. It will also cut import levies for more than 8,000 products for 23 countries and regions that have free-trade agreements with China, known as “most favored nation” rates. While the tariff reduction is not directly linked to the American trade war, it will likely guarantee that the coming Phase One trade deal with the U.S. doesn’t invite complaints from other trading partners.

The week ahead — Economic data from Econoday.com: