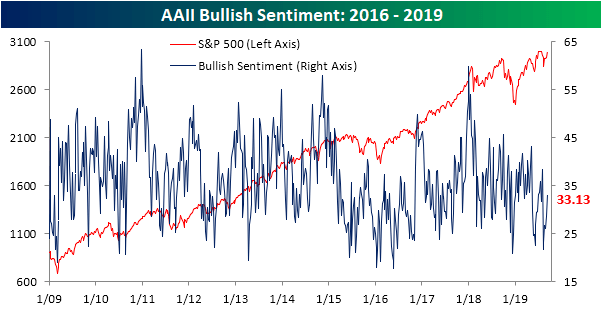

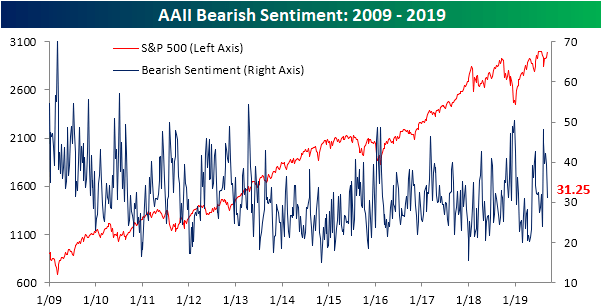

Week of Sept 21 2019 Weekly Recap & The Week Ahead

Monday, September 23rd, 2019“In this business if you’re good, you’re right six times out of ten. You’re never going to be right nine times out of ten.” -Peter Lynch

1. Index Funds Had More Assets by Value Than Stock-Picking Rivals — Funds that track broad U.S. equity indexes hit $4.27 trillion in assets as of Aug. 31, giving them more money than stock-picking rivals for the first-ever monthly reporting period. Funds that try to beat the market had $4.25 trillion as of that date. In the past decade, $1.32 trillion fled actively managed U.S. equity mutual funds and exchange-traded funds as nearly $1.36 trillion was added to low-cost funds that mimic market indexes. That shift lowered the price of investing for individuals, reduced the influence of stock pickers and turned a handful of Wall Street outsiders into the biggest power brokers in the industry.

2. General Motors Factory Workers Headed to Picket Lines in 10 States — the United Auto Workers union called on thousands of workers to walk off the job in an effort to secure better pay, more job security and other benefits. The walkout is one of the largest private-sector work stoppages in decades. The UAW further announced it will pay striking workers $250 a week, but that does not go very far, especially when they need to cover their own health insurance. GM’s credit rating could also topple into junk bond status if the strike lasts more than a week or two, according to Moody’s.

3. S.Korea Downgrades Japan Trade Status — South Korea is following through with plans to drop Japan from a list of countries receiving fast-track approvals in trade, a reaction to a similar move by Tokyo to downgrade Seoul’s trade status. The dispute between the nations began in July when Japan imposed tighter export controls on three chemicals South Korean companies use to produce semiconductors and displays for smartphones and TVs, which are major import items for South Korea. The escalating row is rooted in wartime history and could cast uncertainty into the global supply chain and economy.

4. The Federal Reserve Cut Its Benchmark Interest Rate — the Federal Reserve cut its benchmark interest rate by a quarter-percentage point for the second time in two months, as Chairman Jerome Powell left the door open to more cuts. Three officials voted against the decision, with two saying rates should have been left unchanged, and one supporting a bigger cut. Mr. Powell repeatedly cited the costs of rising trade-policy uncertainty.

5. NY Fed to Conduct Third Repo Operation — the New York Fed is offering an overnight repurchase agreement operation for the third day in a row, injecting $75B into a vital corner of finance to restore order in the banking system. The temporary liquidity follows the Fed’s reduction in the interest rate on excess reserves, or IOER, another attempt to quell money-market stresses. The prior operations have soothed markets, with repo rates declining Wednesday to more normal levels after jumping to 10% on Tuesday, four times where they were last week.

6. Pentagon Weighs Sending More Military Assets to Mideast — President Trump is weighing responses to the attacks on Saudi oil facilities, and U.S. military officials are considering sending more antimissile batteries, a squadron of jet fighters and added surveillance capabilities, as well as possibly committing an aircraft carrier and other warships to the region.

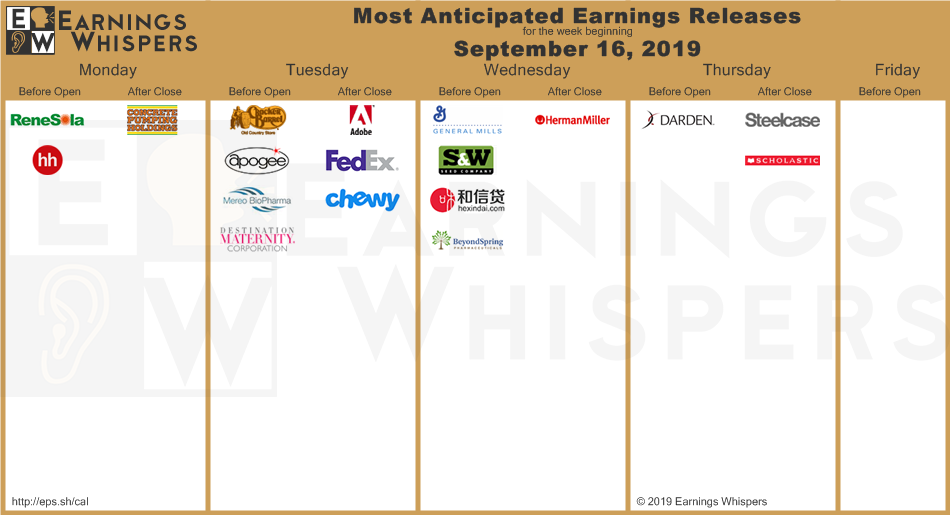

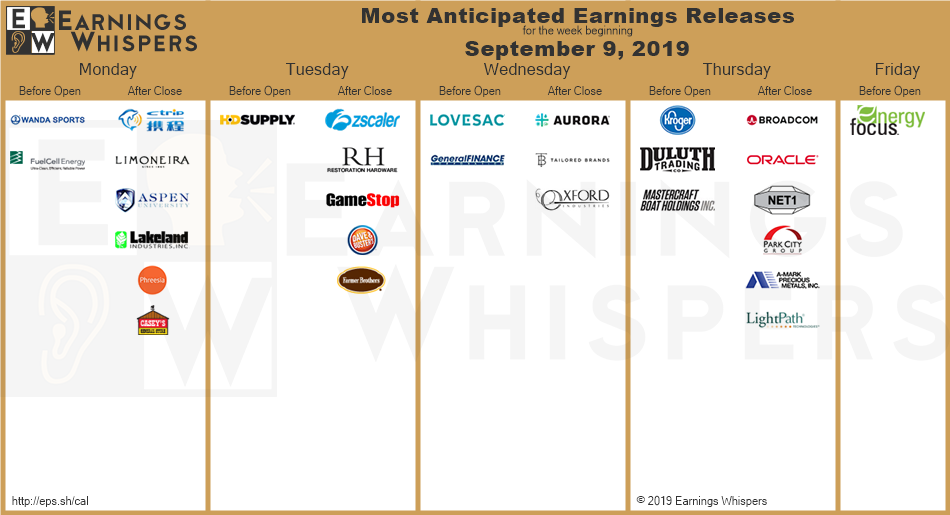

The week ahead — Economic data from Econoday.com: