Week of Oct 20, 2023 Weekly Recap & The Week Ahead

Monday, October 23rd, 2023“If you can keep your wits about you while all others are losing theirs, and blaming you. The world will be yours and everything in it…” — Rudyard Kipling

1. Retail sales rose 0.7% in September, much stronger than estimate — Retail sales rose 0.7% on the month, well above the 0.3% Dow Jones estimate, according to the advance report the Commerce Department released Tuesday. Gas station sales helped propel the headline number, rising 0.9% as prices at the pump accelerated.

Excluding autos, sales were up 0.6%, also well ahead of the forecast for just 0.2%. The so-called control group, which strips out items such as auto dealers, gas stations, office supply stores, mobile homes and tobacco stores and is used for the department’s GDP calculation, rose 0.6% as well. Sales gains were broad-based on the month, with the biggest rise coming at miscellaneous store retailers, which saw an increase of 3%. Online sales climbed 1.1% while motor vehicle parts and dealers saw a 1% increase and food services and drinking places grew by 0.9%, good for a yearly increase of 9.2%, which led all categories.

2. US Existing-Home Sales Sink to Lowest Level Since 2010 — Sales of previously owned US homes fell in September to the lowest level since 2010 as affordability worsened even further. Contract closings decreased 2% from a month earlier to a 3.96 million annualized pace, National Association of Realtors data showed Thursday. The median estimate in a Bloomberg survey of economists called for a reading of 3.89 million. The resale market remains historically depressed under the weight of decades-high mortgage rates. Not only are prospective buyers discouraged, but homeowners who previously locked in lower mortgage rates have no incentive to move, putting pressure on inventories and therefore prices.

3. The 10-Year Treasury Yield Came Close to 5% — The 10-year yield was down 0.05 percentage point on Friday, to 4.94%, after closing at 4.99% on Thursday then pushing closer to 5% in overnight trading. The yield has climbed 1.2 percentage points since July alone, as investors have increasingly priced in the likelihood that the Federal Reserve will lift interest rates higher than expected and leave them there longer. Data showing strength in the labor market, retail sales, and elsewhere in the economy have lifted expectations for inflation, prompting investors to factor in tighter monetary policy later into 2024. The higher yields on offer today are an attractive opportunity for investors looking for some greater risk-free income, but reaching them has been painful for those already holding bonds in their portfolios. Bonds’ prices fall as their yields rise.

4. Jim Jordan Is Removed as GOP Nominee After Third Loss in Speaker Vote — Rep. Jim Jordan was ousted as the GOP’s nominee to be House speaker, as colleagues voted to start over fresh next week after the fiery Ohio conservative failed for the third time to win a majority on the House floor. Jordan has faced opposition from GOP colleagues worried about how he would manage spending talks and avoid a government shutdown; allies of other party leaders who were pushed aside in favor of Jordan; and moderates from Democratic-leaning regions who see him as too stridently conservative.

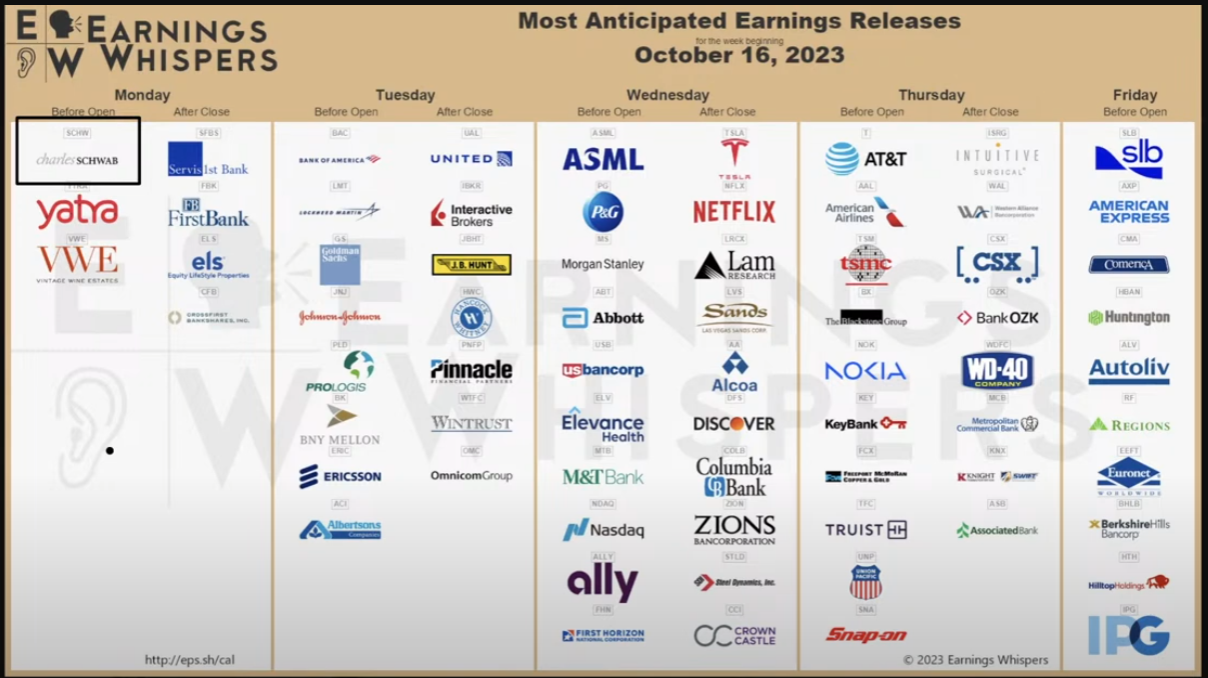

The week ahead — Economic data from Econoday.com: