Week of May 22-29 ’26 Weekly Recap & The Week Ahead

June 2nd, 2026“There will not be any posting for the week of May 22nd – 30th, 2025. We are away for some needed R&R.” — Have a good week.

The week ahead — Economic data from Econoday.com:

| Market Outlook |

| Equity Guidance Blog — Financial Market Overview |

“There will not be any posting for the week of May 22nd – 30th, 2025. We are away for some needed R&R.” — Have a good week.

The week ahead — Economic data from Econoday.com:

“The market doesn’t reward the smartest traders. It rewards the most disciplined ones.” — Igor Arapov

1. US Inflation Accelerates as Gas, Rent and Food Prices Climb — The consumer price index rose 3.8% from a year earlier, according to Bureau of Labor Statistics data out Tuesday, the most since 2023. After adjusting for inflation, wages fell for the first time in three years. The figures show how the impact of the Iran war is hitting the US economy as energy costs surge. The BLS report indicated gas prices rose almost 28% over the past two months. Grocery prices, rents and airfares also saw large increases from a month earlier. A sustained pickup, especially in the cost of essentials, could lead consumers to cut back on spending. The overall CPI advanced 0.6% in April. Grocery prices rose 0.7%, the most in almost four years. Meats, dairy, fresh fruits and vegetables all posted notable gains. Food prices have been a major contributor to affordability concerns in recent years and could play into Americans’ views of the economy heading into midterm elections.

2. US Producer Prices Rise Most Since 2022 on Energy Costs — The producer price index rose 6% from a year ago, according to Bureau of Labor Statistics data out Wednesday. That topped all estimates in a Bloomberg survey of economists. The monthly gain was also the sharpest since 2022. A core measure of wholesale inflation that excludes food and energy increased 5.2% from April 2025 — the biggest advance in more than three years. The PPI data likely reinforce Federal Reserve officials’ views that inflation should remain their top concern in the face of the war-driven surge in oil prices that’s starting to ripple through to other parts of the economy.

3. Xi’s Taiwan Warning to Trump Highlights Tensions in Beijing Summit — Xi’s remarks, while in line with China’s longstanding position, threatened to dim the mood of a visit both countries hoped would stabilize ties. The meetings that began Thursday morning at the Great Hall of the People in Beijing were billed as a gathering of superpowers to quell economic and trade disputes.

Those topics were indeed raised, including discussions of trade ties, U.S. access to the Chinese market, Beijing’s investment in U.S. industries and its purchases of American agricultural products.

The week ahead — Economic data from Econoday.com:

“If you can learn to create a state of mind that is not affected by the market’s behavior, the struggle will cease to exist.” — Mark Douglas

1. Private Employers Add 109,000 Jobs in April, the Fastest Pace of Job Growth Since January 2025 — The U.S. added 109,000 jobs to private payrolls last month, the fastest pace of job growth since January 2025, according to the ADP National Employment Report released Wednesday morning. Healthcare continued to drive job growth, but April’s robust hiring was also helped along by a rebound in trade, transportation, and utilities. During the first quarter, private employers added an average of 46,300 jobs on a monthly basis. In fact, the private sector has managed to post positive job growth every single month so far this year. That’s in contrast to total nonfarm payroll data produced by the Bureau of Labor Statistics, which posted a massive decline in job growth in February in the combined private and public sectors.

2. Corporate Layoffs Are Down 10% This Year, but the AI Reckoning Has Come for Tech — Layoffs in the first four months of the year totaled 300,749, according to outplacement firm Challenger, Gray & Christmas, a level 50% lower than the same period last year when enormous federal-worker job cuts dominated the start of President Trump’s second term. Private-sector layoffs were 10% lower than this time last year.

Now AI is upending workplaces in ways both real and whitewashed. Tech has been hardest-hit, with firms letting go of more than 85,000 employees so far this year, a 33% increase over the same period in 2025, Challenger data show. The cuts keep coming, with fresh announcements in May of thousands more workers cut at PayPal and the elimination of “pure managers” at Coinbase.

3. U.S. Debt Tops 100% of GDP — As of March 31, the country’s publicly held debt was $31.265 trillion, while GDP over the preceding year was $31.216 trillion, according to data released Thursday. That puts the ratio at 100.2%, compared with 99.5% when the last fiscal year ended Sept. 30. That figure will likely climb for the foreseeable future because the federal government is running historically large annual deficits of nearly 6% of GDP, which add to the debt. The government also becomes more sensitive to interest rates as debt grows. One in seven dollars of federal spending now goes to interest. A 0.1 percentage-point interest-rate increase would cost $379 billion over 10 years, according to the Congressional Budget Office.

4. US Jobs Rise 115,000 in Strongest Two-Month Gain Since 2024 — Nonfarm payrolls rose 115,000 last month after an even bigger surge in March, marking the strongest two-month increase since 2024, according to Bureau of Labor Statistics data out Friday. The unemployment rate was unchanged at 4.3%. The advance in hiring was led by healthcare, which has been the primary driver of job growth over the last year. Transportation and warehousing and retail trade both added the most jobs since 2024. Employment in couriers and messenger services added almost 38,000 jobs, the most since 2020. Manufacturing employment fell slightly.

The week ahead — Economic data from Econoday.com:

“The consistency you seek is in your mind, not in the markets.” — Mark Douglas

1. Home Price Growth Unexpectedly Slowed in February. Blame High Mortgage Rates — Prices in an index tracking 20 of the nation’s large metropolitan areas rose 0.9% from a year ago, according to S&P Cotality Case-Shiller index data. That’s down from a 1.2% gain in January and slower than the 1.3% increase economists had anticipated, according to FactSet.

Prices nationally increased 0.7% from the year prior, slower than their 0.8% gain in January. Prices dropped most in Denver, where they fell 2.2%. Close behind were Tampa, Florida, where prices dropped 2.1%, and Seattle, where they fell 2%. Prices rose most in Chicago, New York, and Cleveland, with gains of 5%, 4.7%, and 4.2%, respectively.

2. Divided Fed Officials Hold Rates; Powell to Stay as Governor — Federal Reserve officials left interest rates unchanged, but revealed a deepening division over the outlook for policy amid increased uncertainty caused by the conflict in the Middle East. In what will be his last press conference as Fed chair, Jerome Powell said he intends to remain at the central bank as a member of its Board of Governors. He said Justice Department officials had assured him over the weekend they wouldn’t restart a controversial criminal investigation into the central bank unless the Fed’s internal watchdog recommended that.

3. Trump Says He Rejects Iran Hormuz Offer, Keeps Blockade — Trump said he had rejected a recent proposal from Iran to reopen the strait but that would have delayed talks on the nuclear issue until later. While Trump said he’d stick with the blockade, US military commanders have prepared a plan for a short and powerful wave of strikes on Iran to raise pressure on the regime, Axios said, citing people with knowledge of the preparations.

4. Core inflation rate hit 3.2% in March as first-quarter growth disappointed at 2% — The core personal consumption expenditures price index, which excludes food and energy, accelerated a seasonally adjusted 0.3% for the month, pushing the 12-month inflation rate to 3.2%, the Commerce Department reported Thursday. The readings matched the Dow Jones consensus estimates. Core inflation hit its highest level since November 2023. In other economic news , the Commerce Department reported that gross domestic product grew at a 2% seasonally adjusted annualized pace in the first quarter, up from 0.5% in the fourth quarter of 2025 but lower than the 2.2% estimate. The modest growth rate came despite a seeming surge in spending on artificial intelligence and what should have been a boost from the end of last year’s government shutdown.

The week ahead — Economic data from Econoday.com:

“A good trader watches his capital as carefully as a professional scuba diver watches his air supply.” — Anonymous

1. Trump Extends Iran Cease-Fire Indefinitely With Peace Talks in Limbo — President Trump said that the U.S. will extend its cease-fire with Iran and continue the blockade of the country’s ports until its leaders present “a unified proposal.” The move came after Vice President JD Vance canceled plans to travel to Pakistan on Tuesday for negotiations with Iran over ending the war, highlighting uncertainty about future peace talks. The official Telegram account of Iran’s supreme leader published threats to attack U.S. and Israeli forces.

Israel and Hezbollah traded accusations that the other side was violating an Israel-Lebanon cease-fire, ahead of a second round of negotiations set for Thursday in Washington.

2. US Says No Firm Deadline for Iran Proposal Amid Hormuz Standoff — President Donald Trump said the truce agreed April 7 would stay in place indefinitely while Washington waits for Iran to submit a new peace proposal, though Tehran says it has no plans to take part in negotiations imminently. Vice President JD Vance had been prepared to fly to Islamabad to resume discussions, before it became clear Iran would not send its own delegation. The US maintained a naval blockade on ships going to and from Iran’s ports to pile pressure on the Islamic Republic, in a move Iranian Foreign Minister Abbas Araghchi called a violation of the ceasefire. Iranian President Masoud Pezeshkian said in a post that while Iran welcomes talks, the

3. Virginia Voters Narrowly Approve Measure to Boost Democrats in Midterms — The Virginia delegation to the U.S. House is currently split almost evenly—six House Democrats to five Republicans—closely reflecting the blue lean of the state, which elected Democrat Abigail Spanberger as governor last year and sided with Kamala Harris over President Trump in 2024. Democrats pushed for new, temporary district lines intended to make the map 10-1 in their favor. Backers have said the gerrymandering is needed to counter efforts by Trump and Republicans in Texas and other states to create more red seats in the closely divided House. Opponents have said the proposal undermines Virginia’s past efforts at fair representation. Virginia was following the lead of California, which voted overwhelmingly last year to redraw its lines to create several more blue districts.

4. Hormuz Traffic Grinds to a Halt After Iran Seizes First Vessels — Only one ship, bulk carrier LB Energy, was seen moving through the waterway early Thursday, with none seen entering. Products tanker Ocean Jewel is currently idling at the entrance to the corridor, having aborted a transit not long after Iranian forces began firing at three ships.

Two of those attacked vessels, the MSC Francesca and the Epaminondas, were subsequently boarded by Iranian forces, marking a new stage in Tehran’s efforts to exert control over traffic through Hormuz. US forces say they have turned around 31 ships since its warships began barricading Iran’s coastline on April 13, most of them oil tankers.

5. DOJ Drops Powell Probe, Smoothing Path for Warsh to Lead Fed — The Justice Department is ending a controversial investigation into building-renovation cost overruns at the Federal Reserve, potentially clearing a path to confirmation for Kevin Warsh, President Donald Trump’s pick to be the next chair of the central bank. Pirro served subpoenas to the central bank in January as part of a criminal investigation into the cost overruns and congressional testimony Powell provided on the matter. The subpoenas prompted a sharp response from Powell who accused the administration of launching the investigation in response to the Fed’s refusal to lower interest rates to Trump’s satisfaction.

The week ahead — Economic data from Econoday.com:

“The most nerve-wracking trading moment isn’t when you’re in the red. It’s when you’re just one step from your target, and the stock decides to U-turn right back to your stop loss!”

― Jayesh thakkar

1. Nasdaq Logs Longest Winning Streak Since 2021 as Investors Look Beyond War — War worries haven’t gone away. The Dow Jones Industrial Average’s energy-hungry components have the blue-chip index lagging behind other major benchmarks, on Tuesday notching a 0.7% gain. But with the nation’s largest banks reporting that consumers continue to borrow and spend, many think that the prospect for strong corporate earnings can outweigh the risks of a war-fueled slowdown. Tech has been a major beneficiary of the shift. A computing-power arms race among the biggest artificial-intelligence companies is driving huge demand for hardware like chips, servers and memory, and minting big winners in the stock market.

2. Trump Says Israel and Lebanon Agreed to 10-Day Ceasefire — US President Donald Trump said that Israel and Lebanon had agreed to a 10-day ceasefire, a move that would ease broader tensions between Washington and Tehran. Fighting between Israel and Hezbollah in southern Lebanon had threatened to derail the two-week ceasefire between the US and Iran and the potential for that truce to be extended.

3. US Probes Suspicious Oil Trades Made Before Trump Pivots – The Commodity Futures Trading Commission is leading the probe into trading of oil futures contracts on platforms belonging to CME Group Inc. and Intercontinental Exchange Inc., said the people, who asked not to be identified as the information is private. Both exchanges were asked to hand over data, the people said. The CFTC is looking into at least two instances over a period of about two weeks where trading volumes surged shortly before major announcements, the people said. Data requested from the exchanges include the so-called Tag 50 identifications of the entities behind the trades, the people said. On March 23, oil and stocks futures worth billions of dollars were traded 15 minutes before Trump said previously threatened strikes on Iranian energy infrastructure would be delayed. The president’s comments in a Truth Social post sent crude prices plummeting and equities soaring. A similar pattern was observed ahead of Trump’s April 7 announcement of a two-week ceasefire with Iran. Futures activity increased in the hours before the news, which caused both oil and gas prices to plunge.

The week ahead — Economic data from Econoday.com:

“There is a time to go long, a time to go short and a time to go fishing.” – Jesse Livermore

1. Hegseth Declares ‘Decisive’ Victory as Cease-Fire Begins — The U.S. and Iran agreed to a cease-fire on Tuesday. But it’s still unclear whether the negotiations set to start Saturday and led by Vice President JD Vance will be based on the U.S.’s 15-point plan or Iran’s diametrically opposed 10-point plan. Israel said it had halted attacks on Iran but was continuing military operations in Lebanon against Hezbollah, prompting protests from Iran. Oil-tanker traffic was halted in the Strait of Hormuz after the Israeli attacks, according to Iran’s semi-official Fars News Agency, and Iran told mediators its participation in talks with U.S. officials in Islamabad is conditional on a cease-fire in Lebanon.

2. Trump Team Explores Punishment for NATO Countries That Didn’t Support Iran War — The proposal would involve moving U.S. troops out of North Atlantic Treaty Organization member countries deemed unhelpful to the Iran war effort and stationing them in countries that were more supportive. The proposal would fall far short of President Trump’s recent threats to fully withdraw the U.S. from the alliance, which by law he can’t do without Congress. The U.S. has around 84,000 troops stationed across Europe, though the exact number varies from military exercises and rotational deployments. U.S. bases in Europe serve as a critical hub of global U.S. military operations, as well as provide an economic boon to the host country through investment. Bases in Eastern Europe also serve as a deterrent against Russia. Beyond repositioning troops, the plan could also involve closing a U.S. base in at least one of the European countries, possibly Spain or Germany, according to the two administration officials.

3. US Consumer Sentiment Drops to Record Low on Price Concerns — The preliminary April sentiment index slumped to 47.6 from 53.3 in March, according to the University of Michigan data out Friday. The survey period includes responses from March 24 to April 7. That was below all but one estimate in a Bloomberg survey of economists. They saw costs rising at an annual rate of 3.4% over the next five to 10 years, up slightly from a month earlier. Gasoline prices, well above $4 a gallon and the highest since 2022, could persuade consumers to cut back on discretionary spending. Such an erosion of purchasing power risks slowing the economy at a time when employment prospects are limited and Americans are already anxious about a high cost of living.

4. Inflation Soared to 3.3% in March, Driven by Higher Gasoline Costs — Consumer prices were up 3.3% in March from a year earlier, the Labor Department said Friday, much hotter than February’s gain of 2.4%. Prices excluding food and energy categories—the so-called core measure economists watch in an effort to better capture inflation’s underlying trend—rose 2.6%, slightly below forecasts for a 2.7% increase. Energy prices jumped by 12.5% from a year earlier, a dramatic acceleration from 0.5% in February. Gasoline prices jumped 18.9% and fuel oil surged by 44.2%. The cost of transportation services, which is affected by fuel costs, rose 4.1% from a year earlier in March, a much faster increase than in February.

Friday’s report offers the first snapshot of how the Iran war affected U.S. inflation. The closure of the Strait of Hormuz snarled shipping and sent the price of crude oil and gasoline surging last month.

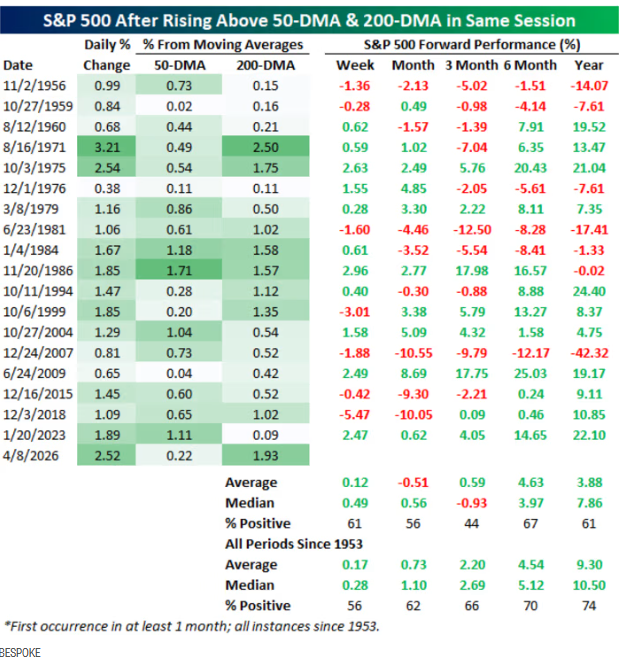

5. S&P 500 Smashes Back Above Two Key Moving Average Statistics — according to the team at Bespoke, Since 1953, when the modern five-day trading week was first adopted, this has only happened 18 times previously when the index break back above both trend lines on the same day is a pretty rare occurrence. hree months later, the index has been positive less than 50% of the time. And while returns six months and one year later have generally been strong, they have lagged the returns during all periods since 1953. “With all of this in mind, we would highlight that six-month and one-year performance following these instances has generally been positive since the 1990s,” the Bespoke team said in a note. See chart below.

The week ahead — Economic data from Econoday.com:

“Trading doesn’t just reveal your character, it also builds it if you stay in the game long enough.” ― Yvan Byeajee

1. Trump Tells Aides He’s Willing to End War Without Reopening Hormuz — Trump and his aides assessed that a mission to pry open the chokepoint would push the conflict beyond his timeline of four to six weeks. He decided that the U.S. should achieve its main goals of hobbling Iran’s navy and its missile stocks and wind down current hostilities while pressuring Tehran diplomatically to resume the free flow of trade. If that fails, Washington would press allies in Europe and the Gulf to take the lead on reopening the strait, the officials said. Trump on Tuesday morning urged other countries to launch their own operation to wrest control of the strait from Iran, blaming countries like the U.K. for not joining the U.S.-Israeli mission against the Islamic Republic.

2. Trump Tries to Sell Americans on War in Iran’ — In a 20-minute address from the White House, Trump said he still aims for a diplomatic agreement to end the war. But in the meantime, he vowed to hit Iran “extremely hard” in the coming weeks and pummel the country “back to the Stone Ages, where they belong.” The Strait of Hormuz, the war’s most notable flashpoint, would “open up naturally” once the war ended, Trump claimed. “They’re going to want to be able to sell oil,” Trump said of Iran, “and the gas prices will rapidly come back down, stock prices will rapidly go back up.” Trump’s decision to deliver the prime-time speech reflected a desire by his advisers to explain the war’s objectives and tamp down concerns that the conflict would become one of the “forever wars” that the president campaigned against.

3. Blue Owl Investors Seek to Pull $5.4 Billion From Two Private-Credit Funds — Investors in two of Blue Owl Capital’s biggest private-credit funds asked to pull out some $5.4 billion in the first quarter, adding to the growing stream of capital leaving the once-hot corner of Wall Street.

The redemptions amounted to 22% of Blue Owl Capital’s giant $36 billion private-credit fund and 41% of a separate technology-focused fund. Such large redemptions are dangerous for investment firms like Blue Owl because they threaten the key driver of their share prices: the amount of money they manage and collect fees on. The firms built their funds to withstand prolonged bear markets, but outflows may continue for months or even years.

4. Trump Administration Unveils Up to 100% Tariff on Branded Drugs — The 100% tariff will apply to patented imported pharmaceuticals from companies that haven’t committed to invest in the U.S. and haven’t entered into “most favored nation” agreements to match their U.S. prices to the lowest they charge in other developed countries, a senior administration official said Thursday. But the full 100% tariff might apply to only a few drugmakers or none at all. If a company pledges to invest in U.S. drug manufacturing in the coming years, its tariff rate will fall to 20%, the senior administration official said. The company would have to complete the factory by the end of President Trump’s term in the White House, the official said, or tariffs could be increased.

The week ahead — Economic data from Econoday.com:

1. Prices Paid to US Producers Increase by More Than Forecast — The producer price index rose 0.7% after a 0.5% gain in the prior month, according to Bureau of Labor Statistics data out Wednesday. An underlying gauge of wholesale inflation that excludes food and energy increased 0.5%.

The producer price data follow recent figures that showed underlying consumer inflation slowed in February from a month earlier. But that was before the Iran war, which has driven up energy prices and started to dent consumer sentiment. More than half of the increase in the PPI last month was due to a 0.5% advance in services costs, according to the BLS. That includes rising costs for traveler accommodation, food wholesaling and investment services. Food prices climbed by the most since mid-2021, partly due to a nearly 49% surge in fresh and dry vegetables.

2. Fed Expected to Hold Rates, Weigh Oil Shock — Officials are expected to hold their benchmark interest rate steady for a second consecutive meeting in a range of 3.5% to 3.75%. But policymakers are likely having a robust discussion over the ways the war in the Middle East could put pressure on both sides of their mandate — and whether responding to the threat of slower growth could add fuel to inflation that’s been above the Fed’s target for five years running. Data released since the Fed’s January gathering showed inflation remained elevated even before the conflict in the Middle East caused oil prices to surge. And news on the labor market has been mixed: A strong January report was followed by a surprising drop in payrolls in February.

3. U.S. Leading Indicators Forecast Further Slowdown — The U.S. economy is expected to slow further amid continued headwinds, while conflict in the Middle East further clouds the growth outlook, according to a basket of monthly economic indicators. The index fell 1.3% over the six months between July and January, compared with a 2.6% contraction over the previous six-month period, according to the report.

The latest data doesn’t reflect the impact from war in Iran, Monica said, adding that The Conference Board was therefore cutting its growth forecast by 0.1 percentage point to 2.0% for 2026.

4. The Well-Timed Trades Made Moments Before Trump’s Policy Surprises — According WSJ, Most recently, there was a mysterious flurry of trading activity in oil and S&P 500 futures about 15 minutes before Trump de-escalated tensions with Iran with a Monday morning post on Truth Social, which sent oil prices tumbling and stocks rallying. March 23, 2026: Early Monday, Trump announced in a Truth Social post that he was postponing strikes on Iranian power plants thanks to “productive” talks with Iran. About 15 minutes before the post, a sudden burst of activity hit the oil-futures market. During the two-minute period from 6:49 a.m. to 6:51 a.m. ET, more than $760 million worth of Brent and West Texas Intermediate oil futures changed hands, according to Dow Jones Market Data. A similar burst of activity took place at the same time in S&P 500 futures.

The week ahead — Economic data from Econoday.com:

“The market doesn’t reward the smartest traders. It rewards the most disciplined ones.” — Unknown

1. G-7 Tasks IEA With Preparing Scenarios for Oil-Stockpile Release — The G-7 wants to be ready to deploy oil reserves if needed, and tasked the International Energy Agency with studying the volumes that could be released, French Finance Minister Roland Lescure told reporters in Paris on Tuesday. France holds the current G-7 presidency. The IEA, which oversees the use of OECD oil reserves, will discuss the process at a board meeting later meeting.

2. US Core Inflation Slowed as Expected Before War With Iran — The consumer price index, excluding food and energy, rose 0.2% from January, according to Bureau of Labor Statistics data out Wednesday. From a year ago, it was unchanged at 2.5% — the slowest pace in nearly five years. The report showed lower prices for used cars and motor vehicle insurance helped keep inflation in check last month, despite higher costs for gasoline and groceries including fresh vegetables and coffee. Federal Reserve officials are expected to leave interest rates unchanged at their policy meeting next week, a prediction that preceded the latest events in the Middle East. With the war threatening to push up inflation — at least in the near term — some investors now see a chance the central bank will remain on hold for longer. However, officials also need to be mindful of lingering fragility in the labor market.

3. Deutsche Bank Flags $30 Billion Exposure to Private Credit — Deutsche Bank AG flagged a €26 billion ($30 billion) exposure to private credit, an asset class that’s grappling with fund redemptions, scrutiny of underwriting standards and the impact of AI on some borrowers such as software makers. In its annual report published Thursday, the lender said it is not exposed to “significant risks” related to non-bank financial institutions, but that it could face potential indirect risks through interconnected portfolios and counterparties. While identifying private credit as a “key risk,” the report did not mention any losses or provisions tied to the private credit exposure, which represents about 5% of its loan book.

Deutsche Bank, which also flagged a potential $1 billion litigation risk on Thursday, fell 7.2% at 3:31 p.m. in Frankfurt trading, putting it on track for the biggest one-day drop since April.

4. Fourth-quarter GDP revised down to just 0.7% growth; January core inflation was 3.1% — Gross domestic product, a measure of all the goods and services produced across the sprawling U.S. economy, rose at a seasonally and inflation-adjusted annual rate of just 0.7% in the fourth quarter, according to the department’s Bureau of Economic Analysis. The first revision of the GDP reading was a sharp step down from the previous estimate of 1.4% and well below the Dow Jones consensus forecast for 1.5%. It also marked a considerable slowdown from the 4.4% gain in the prior period. The personal consumption expenditures price index, the Fed’s primary forecasting tool for inflation, posted a seasonally adjusted gain of 0.3% for the month, putting the annual rate at 2.8%. Economists surveyed by Dow Jones had been looking for respective readings of 0.3% and 2.9%.

The week ahead — Economic data from Econoday.com:

© Copyright 2026 Market Outlook All Rights Reserved

Design by EGS

Sponsored by Equity Guidance LLC