May 14th, 2010

The major indices continued to sell-off after a quick bounce back, based on news of EU TARP-like bailouts. At this juncture, we continue to remain cautious, as we believe the selling is not yet over. Below are the major events which occurred this week.

1. UK – David Cameron won the election and the Conservative replaced the Labour Party.

2. The Chinese market now officially in Bear Market territory (correction of more than 20%); Recent figures point to inflation and manufacturing slowdown;

3. EU/IMF announced a US TARP-like bailout to the tune of $1 trillion dollars; The ECB/IMF will buy EU countries’s government Bonds if needed; It was reported that the French President Sarkozy threatened to pull-out of the EU if the Germans did not support Greece bailout.

4. Portugal & Spain announced their own austerity measures to prevent a Greece-like catastrophy.

5. Gold hits new high at $1,248 an ounce.

6. NY Attorney General to investigate the major investment banks for misleading CDO’s practices.

7. US Government also announced its own investigation into Morgan Stanley over Mortgage Derivative Products; Goldman Sachs is already under government scrutiny.

8. The Senate Finance Committee to investigate Home healthcare company practices of overbilling Medicare — related companies effected were (AFAM, GTIV, AMED, LHGC…)

Here are the major events for the next week:

1. 5/18 — PPI (Producer Price Index)

2. 5/19 — CPI (Consumer Price Index)

3. — Greece $8Bil Redemption

Attached is an interesting chart from the European Commission about the PIIGS countries’s public debts.

Posted in Weekly Summary | No Comments »

May 11th, 2010

Below is a stock with good fundamentals:

InterDigital,Inc.(IDCC) looks appealing at the current multiple:

This near $27. stock has $11 per share in cash and short term investments. InterDigital’ s revenue increased (ttm vs prior ttm) 41.2%. Revenue for the 3/10 quarter was $116.m. The sales increase was due to higher recurring patent licensing royalties. Lower selling, general & administrative expenses contributed to higher earnings in the March 10 quarter.

Growth Rate:

YEAR REVENUE E.P.S.

2008 act. 228.5m 0.57

2009 act. 303.8m 1.73

2010 est. 363.0m 3.20

For the trailing 4 quarters, ending 3/10, the return on equity is 93.6%. The debt to capital ratio at 3/10 is 2.4%.

IDCC is positioned nicely in the shift from 2G to 3G tele-communications. They have already established a strong licensing position for LTE (read conference call 4/29/10). In addition, they have over 50% of the emerging cellular machine to machine market under license.

In summary: IDCC’s low debt, high return on capital, good annual earnings growth, low P.E. ratio of 8.6 and considering that 40% of the stocks selling price is in cash and short term investments, we believe it warrants consideration when the technicals are right.

J. Passalacqua

Possible buy around $25.30 price range.

Posted in Stock Research | No Comments »

May 7th, 2010

The major indexes (US & Abroad) sold-off this week based on fear of Greece “Contagion” spinning out of control.

We believe the sell-offs have not finished and are “watching” the market for a possible entry point.

Other negative events that occurred this week:

1. China raised rates to clamp down on real estate prices and manufacturing slowed.

2. Greek parliament voted through the auterity measure; Riots broke out that resulted in the death of 3 bankers. The Greek market continued selling pick up momentum as the ECB refused to buy Greek Bonds;

3. Gulf of Mexico oil spill worsened — Congress talked about raising the cap on damages.

4. EU at risk from the Greece “Contagion” — costs to insure Portugal & Spain spiked higher this week as the EUR hits 1-year low vs USD. This problem seems to resemble the Lehman problem that led to its insolvency in the fall of 2008;

5. VIX spiked upward — spiked to 42 from the low of 15.5 (as noted on April 16 Blog)

6. Australia imposed a “profit” tax of 40% to “resource” companies

7. UK election resulted in a Conservative win with a majority of the votes.

8. NASDAQ corrected 10%+ for the week (from the high on Apr 23).

Next Week

1. G-7 conference call announcement about the “Greece Contagion”

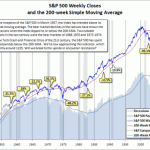

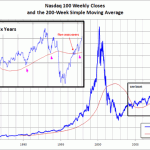

Below is the chart of the S&P500; We are expecting a re-test of 1,095 next week.

Tags: Weekly Summary

Posted in Weekly Summary | No Comments »

May 6th, 2010

As expected, the EU/IMF approved Greece’s bailout package to the tune of over $140 billion. However, the problem now has spread to Portugal & Spain as costs to insure Portugal & Spain spiked upward.

The New York Times posted a nice chart detailing the contagion with the PIIGS countries.

Tags: PIIGS Problem

Posted in Daily Commentary | No Comments »

May 3rd, 2010

The market dropped sharply the week of Apr 30, 2010 due to the following:

1. GS is now under criminal investigation; This further compounds their problem (civil fraud charge) by the SEC. GS possible buy around $110 area;

2. Oil spill spreads to the fishing ground and wildlife areas of the Gulf of Mexico; BP, RIG & CAM sold-offs; (Similar to the Exxon Valdez oil spill in Alaska – 1989); See WSJ comparison

3. Greece awaiting bailout package by May 3rd, 2010; The amount exceeds $100 billion; Next, Portugal’s debt is coming due and Spain’s unemployment exceeds 20%; An indepth and detailed report from Weldon Research regarding Greece, Portugal & Spain.

4. Unemployment assistance phases out at the 99-week limit ;

5. Home Buyer Tax Credit expires Apr 30, 2010

6. Investor Bullishness hits high

For the following ahead,

1. Berkshire annual meeting on Weekend of May 1 & 2.

2. Mon, May 3 — Greece bailout expected by the EU/IMF

3. Tues, May 4 — factory orders

Tags: Weekly Recap

Posted in Weekly Summary | 1 Comment »

April 29th, 2010

Posted in Uncategorized | No Comments »

April 26th, 2010

The market continues to move up on lower volume based on blow-out earnings from AAPL, GS, BAC, WDC….

We remain cautious for a number of reasons:

1. Nearly 40% of companies reported earnings; Most companies beat last year ‘s comparisons;

2. ObamaCare stocks continue to sell-off; Notably HMOs, Insurance Cos, and Biotechs; (i.e. WLP, HUM, AET, etc..)

3. Major indices (RUSSELL 2000, SPX, DJIA) are hitting 200-sma and are nearing Aug 2008 high

4. Greece is ready to tap the IMF for emergency loan of $18 bil due May 18;

5. Portugal CDS exploded higher; this implies that the Euro will weaken against the USD; Commodities move in the inverse direction of the USD;

6. GS in the government’s cross-hairs; The Obama Admin. is pushing for financial regulations and is using GS as a target;

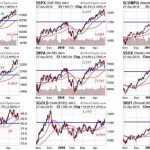

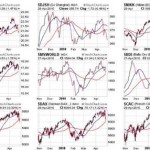

Below are a number of charts to consider:

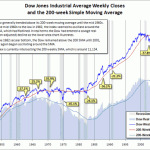

1. SPX — (S&P500)

2. DJIA — (Dow Jones 30)

3. WLP — (Wealthpoint Health)

4. GS

5. US Dollar

Posted in Uncategorized | No Comments »

April 16th, 2010

Weekly Summary

GS is being charged by the SEC with civil fraud, this resulted in a market sell-off on higher volumes. Greece may head toward a bailout by the EU/IMF. The USD strenghened against the EUR and thus, commodities sold-off as well.

Multiple negative catalysts are in-play for next week:

1. Continuation of Greece’s problems; Portugal & Greece CDSes moved up –> more expensive for them to borrow.

2. Sell the news — earnings had been good with INTC, JPM, UPS, GOOG, CSX.

3. GS spill-over to other big money center banks that originated CDOs — C, BAC, JPM

4. VIX multi-year lows (15 — May 2008)

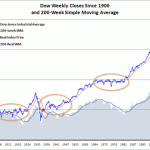

5. Major indices hit major resistance (200-SMA)

6. Bullish Index hits 52-wk high (SPX — 87)

7. Retail investors getting bullish

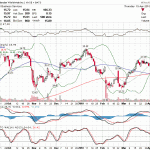

Major Indexes

S&P500 — Approaching 200-SMA resistance at 1,224;

Short-Term –> Expect pullback toward 1,126 (20-SMA)

Medium-Term –> Expect pullback toward 1,050 (50-SMA)

DJIA

Nasdaq

Russell 2000

Posted in Uncategorized | No Comments »

April 15th, 2010

We are following 2 stocks that bounced off 50SMA in higher vol with catalysts. Note that we MIGHT have a very quick selloff anyday.

AN — Autonation (Car Sales)

MWW — Monster Worldwide (Temp Agency)

Posted in Daily Commentary | No Comments »

April 13th, 2010

2010 – Surprises

1. The US economy grows at a 5% real rate and unemployment drops below 9%.

2. The Federal Reserve hikes the fed funds rate to 2% by year-end.

3. Ten year treasury yields rise above 5.5%.

4. The US dollar rallies against the yen and the euro.

5. The S&P rallies to 1300 in the first half of the year, declines to 1000, then settles around 1115.

6. Japan becomes the best performing market.

7. President Obama endorses nuclear power development.

8. The Obama administration becomes energized via US economic improvement.

9. Financial service legislation will be passed (but in a softer form than originally feared).

10. Civil unrest in Iran peaks.

2009 — 2009

1. The Standard and Poor’s 500 rises to 1200. It made it to 1115. Close enough for me, as it was up over 20% on the year. Given the index bottomed at 666 in March, this rally is clearly related to the stimulus.

2. Gold rises to $1,200 per ounce. It did make that magic number. Again, I see this as a stimulus-related call as there has been a rush into commodities due to worries about dollar weakness on the back of the flood of money from the Fed.

3. The price of oil returns to $80 per barrel. Another accurate prediction. The call he makes here is a more bullish version of my view of a structural supply constraint at present prices. This supply constraint creates price whiplash and forces oil up even in a weak economic environment.

4. The yen goes to 75 and the euro to 1.65. Too dollar bearish. Wien underestimated the weakness of Japan and the Eurozone.

5. The ten-year U.S. Treasury yield climbs to 4%. This too is accurate, as the 10-year made it to 3.93% in June. Obviously, this call was predicated on recovery, which we now have. You should note that Treasuries have really been clobbered since November when the Ten-Year yield reached a low of 3.20%.

6. China’s growth exceeds 7% and its stock market revives. Accurate. Growth was even higher, actually. This prediction, which depended on economic recovery.

7. Falling tax revenues from the financial sector cause New York State to threaten bankruptcy and other states and municipalities follow. This is head-scratchingly bearish given his other views. New York took its lumps, but the real damage was in California (especially given the market-induced tax implications of Wall Street bonuses for New York). This story is not over, though.

8. Housing starts to reach bottom ahead of schedule in the fall, and house prices stabilize after dropping 15% from year-end 2008 levels. The Obama stimulus program proves effective and a slow growth recovery begins before year-end. Third and fourth quarter real gross domestic product numbers are positive. This is what happened.

9. The savings rate in the United States fails to improve beyond 3%, as most economists expect. The concept of thrift seems to have vanished from American culture. Peak job insecurity and negative growth drive increased savings early in the year, but spending resumes as the economic growth turns positive in the second half, making Christmas 2009 the best ever. Exactly.

10. Barack Obama …meaningfully increases U.S. military presence… In a hawkish speech he states that the threat of terrorism forces the United States to maintain a strong military force in this strategic area. Pretty much on the money.

Tags: Byron Wien --2010 Surprises

Posted in Notable Experts | No Comments »