Week of May 30, 2025 Weekly Recap & The Week Ahead

June 3rd, 2025“There will not be any posting for the week of May 30th, 2025. We are away for some needed R&R.” — Have a good week.

| Market Outlook |

| Equity Guidance Blog — Financial Market Overview |

“There will not be any posting for the week of May 30th, 2025. We are away for some needed R&R.” — Have a good week.

“Do more of What Work and Do Less of What Doesn’t” — unknown

1. U.S. and China agree to slash tariffs for 90 days in major trade breakthrough — The trade agreement means that “reciprocal” tariffs between both countries will be cut from 125% to 10%. The U.S.′ 20% duties on Chinese imports relating to fentanyl will remain in place, meaning total tariffs on China stand at 30%. The breakthrough comes after U.S. and China trade representatives held high-stakes talks in Switzerland over the weekend. The pause will begin Wednesday. Both China and the U.S. said they will continue discussions on economic and trade policy.

2. Monthly Inflation Ticked Up in Early Hints of Tariff Effects — The consumer-price index rose a seasonally adjusted 0.2% in April, the Labor Department said Tuesday. That matched the forecasts of economists polled by The Wall Street Journal. However, it was a turnaround from March, when month-over-month prices fell 0.1%. Year-over-year inflation cooled to a 2.3% increase in April, below the 2.4% that economists had expected and below March’s annual rate. A big decline in gasoline prices versus a year earlier helped pull that rate lower. Prices excluding food and energy categories—the so-called core measure that economists watch in an effort to better capture inflation’s underlying trend—rose 2.8%. That matched forecasts by economists.

3. US Producer Prices Fell Unexpectedly in April as Margins Shrank — The 0.5% decrease in the producer price index followed no change in March, Bureau of Labor Statistics data showed Thursday. The median forecast in a Bloomberg survey of economists called for a 0.2% gain. Excluding food and energy, the PPI declined 0.4% — the most since 2015. Stripping out food, energy and trade, a less-volatile measure favored by many economists, prices fell 0.1%, the first decline in five years. Compared with a year ago, the gauge rose 2.9%. The figures suggest American manufacturers and service providers are so far refraining from passing along higher US duties on imports. The impact on consumers has also been modest even as producers are feeling the pinch from aggressive levies on imported materials and other inputs.

4. US Retail Sales Barely Rise, Suggesting Some Spending Pullback — Growth in US retail sales decelerated notably in April, reflecting consumers pulled back spending on cars, sporting goods and other categories of imported goods amid concerns about rising prices from tariffs.

The value of retail purchases, not adjusted for inflation, increased 0.1%, Commerce Department data showed Thursday. That followed a a revised 1.7% gain in March, which was the largest in two years. Seven of the report’s 13 categories posted decreases, also restrained by apparel — another good which is largely imported — as well as gasoline. Car sales declined slightly after a buying spree in the previous month. Spending at restaurants and bars, the only service-sector category in the retail report, rose firmly for a second month.

The week ahead — Economic data from Econoday.com:

“Do More of What Works and Less of What Doesn’t” — unknown

1. U.S. Trade Deficit Hits Record as Companies Front-Load Pharmaceuticals — The U.S. trade deficit ballooned 14% to a record $140.5 billion in March, as businesses stockpiled goods to get ahead of sweeping tariffs that President Trump imposed the following month. The value of imported goods totaled $346.8 billion, according to Census Bureau data, continuing a sharp increase that began in January. Nearly all of the $22.5 billion surge in imported consumer goods for March were pharmaceutical products, which the Trump administration is currently considering to hit with tariffs. Imports of computer accessories, automobiles, and car parts and engines also increased.

2. Fed Warns of Rising Economic Risks as It Leaves Rates Steady — The Federal Reserve warned that the economy faced growing risks of higher unemployment and higher inflation due to tariff increases when officials agreed to hold interest rates steady on Wednesday. Tariffs represent a shock that can decrease an economy’s ability to supply goods or services while sending up prices. The unpredictable rollout of increased duties on imported goods threatens to sap profits and chill new investment until businesses have more clarity on their underlying cost structure. Expectations of a rate cut at the Fed’s next meeting in mid-June declined when Powell said officials felt like the costs of waiting to learn more about the economy were “fairly low.”

3. US Productivity Drops for First Time Since 2022 as Output Falls — Productivity, or nonfarm employee output per hour, decreased at a 0.8% annualized rate after a revised 1.7% increase in the fourth quarter, data from the Bureau of Labor Statistics showed Thursday. Because of the decline in productivity, unit labor costs — what businesses pay employees to produce one unit of output — jumped 5.7% in the January-March period, the most in a year. The retreat in productivity was largely due to a 0.3% decline in business output, foreshadowed by data last week showing a trade-related slide in gross domestic product, even as worker hours climbed. Over the near term, productivity gains may suffer somewhat as companies reconsider investment plans until there’s more clarity about US trade and tax policy.

4. Trump Hails UK Trade Framework as First of Many Tariff Deals — Under the agreement, Trump said Thursday the UK would fast-track US items through their customs process and reduce barriers on “billions of dollars” of agricultural, chemical, energy and industrial exports, including beef and ethanol. The British government said auto tariffs would be reduced to 10% and metals duties to zero. Trump and UK Prime Minister Keir Starmer said final details of the pact would still be negotiated over the coming weeks and statements from both governments made clear that many specifics were left to be resolved later.

The week ahead — Economic data from Econoday.com:

“It takes 20 years to build a reputation and five minutes to ruin it.” — Buffetts

1. U.S. Economy Contracts at 0.3% Rate in First Quarter — the Commerce Department said U.S. gross domestic product—the value of all goods and services produced across the economy—fell at a seasonally and inflation adjusted 0.3% annual rate in the first quarter. That was the steepest decline since the first quarter of 2022. Net exports, the difference between imports and exports, were a large drag on growth in the first quarter, stripping 4.83 percentage points from headline GDP. Imports increased at a 41.3% pace in the first quarter as businesses tried to get ahead of tariffs that began to come into effect during the first three months of the year and were dramatically increased in the current, second quarter. The GDP report is the first major economic scorecard for the January-to-March quarter, a period in which the White House changed hands from President Joe Biden to President Trump. January—most of which was before Trump took office—was hit by wildfires in Los Angeles and disruptive winter storms in many parts of the country.

2. US Manufacturing Activity Shrinks by the Most Since November — The Institute for Supply Management’s factory gauge eased 0.3 point to 48.7, data out Thursday showed. The group’s production index stumbled more than 4 points to 44. Readings below 50 indicate contraction. Prices paid for inputs, however, accelerated slightly. The figures illustrate an industrial sector struggling for traction as US tariffs and general uncertainty surrounding trade policy interrupt expansion plans. Orders shrank for a third month and backlogs retreated at a faster pace, consistent with subdued demand.

3. US Consumer Spending Jumps While Key Inflation Gauge Slows Down — Inflation-adjusted consumer spending climbed 0.7% last month, according to Bureau of Economic Analysis data out Wednesday. That was the most since the start of 2023 and suggested households spent aggressively to get ahead of new tariffs.

Meantime, the Federal Reserve’s preferred inflation gauge — the personal consumption expenditures price index — stagnated from a month earlier for the first time in nearly a year. Excluding food and energy, the so-called core PCE was also unchanged, the tamest in almost five years. The data round out a quarter in which the US economy contracted for the first time since 2022 on a monumental pre-tariffs import surge and more moderate consumer spending. The report earlier Wednesday also showed core PCE inflation accelerated to a 3.5% pace in the first quarter — the most in a year.

4. U.S. payroll growth totals 177,000 in April, defying expectations — Nonfarm payrolls increased a seasonally adjusted 177,000 for the month, slightly below the downwardly revised 185,000 in March but above the Dow Jones estimate for 133,000, the Bureau of Labor Statistics reported Friday. The unemployment rate held at 4.2%, as expected, indicating that the labor market is holding relatively stable. The survey of households, which is used to calculate the jobless rate, showed an even stronger gain, with an increase of 436,000 in those who reported holding jobs on the month.

A broader unemployment gauge that includes discouraged workers and those holding part-time jobs for economic reasons, or the underemployed, edged lower to 7.8%. The labor force participation rate ticked higher to 62.6%. The strong report led traders to push out expectations for an interest rate cut until July, according to the CME Group’s FedWatch gauge of futures pricing.

The week ahead — Economic data from Econoday.com:

“Do more of what works and less of what doesn’t” — Unknown

1. Trump U-Turns on Powell, China Follow Dire Economic Warnings — Trump entered office with a steadfast desire to reshape the global economy. But his resolve has appeared to waver in the face of turmoil in equities and bonds and pleas from powerful executives who fear his sweeping tariffs and interference with the Federal Reserve could set off an economic calamity. Trump on Tuesday said he had no intention to fire Powell — despite days of criticism over the central bank’s policies — and said he believed a deal with Beijing would significantly reduce the sweeping tariffs he’s posted on Chinese goods. After a report that the US would be willing to phase in lighter tariffs on Beijing over five years on Wednesday, Trump told reporters that China was “going to do fine” once talks had settled.

2. March home sales drop to their slowest pace since 2009 — Sales of previously owned homes in March fell 5.9% from February to 4.02 million units on a seasonally adjusted annualized basis, according to the National Association of Realtors. That’s the slowest March sales pace since 2009. Sales were 2.4% lower than March 2024 and slumped across all regions month-to-month. They fell hardest in the West, the priciest region of the country, down more than 9%. The West, however, was the only region to see a year-over-year gain, due to strong activity in the Rocky Mountain states where job growth is strong.

3. Economy Orders for big-ticket items like autos and appliances surged 9.2% in March in rush to beat tariffs — So-called durable goods orders soared a seasonally adjusted 9.2% on the month, up from a 0.9% gain in February and well ahead of the Dow Jones forecast for a 1.6% increase. Excluding defense, the increase was even higher, at 10.4%, though the ex-transportation number was flat. Transportation equipment orders surged 27%, led by a 139% increase in nondefense aircraft and parts. In addition to aircraft and autos, the durables category also includes items such as appliances, computers and jewelry. On the durables goods side, the advanced report reflects a pull-forward effect as Trump dangled threats against U.S. trading partners through March before announcing his “Liberation Day” duties on April 2. Trump slapped a 10% tariff against all imports as well as a select charges against dozens of countries that he ultimately tabled for 90 days for negotiations.

4. US Consumer Sentiment Slides While Inflation Expectations Jump — The final April sentiment index fell to 52.2 from 57 a month earlier, according to the University of Michigan. While a slight improvement from the preliminary gauge of 50.8, the latest figure is the fourth-lowest in data back to the late 1970s.

Consumers anticipated inflation will rise at an annual rate of 4.4% over the next five to 10 years, the data out Friday showed. They expect prices to rise at a 6.5% pace over the next year. While down from a preliminary reading of 6.7%, year-ahead price expectations are still the highest since 1981.

The week ahead — Economic data from Econoday.com:

“Set your own rules and stick to them; never argue with the market; never make a play you can’t afford; never give way to irrational exuberance. Above all, don’t be a sucker.” — Jesse Livermore

1. China Goes After Boeing, Tells Airlines Not to Order New Aircraft From U.S. Jet Maker — Beijing has told Chinese airlines not to place new orders for Boeing jets and is requiring carriers to seek approval before taking delivery of aircraft they have already ordered, according to people with knowledge of the Chinese regulator’s guidance. Cutting off deliveries to China could dent revenue for the cash-strapped jet maker, which has been working to clear out parked planes and ramp up production and deliveries amid a quality crisis. Longer-term, the Chinese market is crucial; Boeing has forecast it will account for a fifth of the world’s airplane deliveries in the next two decades. Of 130 airplanes Boeing delivered globally this year through March, 18 went to Chinese airlines. Boeing delivered two planes to Chinese airlines earlier this month, according to data from Cirium.

2. March Retail Sales Beat. Consumers Are Stocking Up Ahead of Tariffs — Retail sales gained 1.4% in March from February, better than economists’ forecasts for a 1.3% increase, the Census Bureau reported. “Auto makers, by way of incentives, and savvy consumers are likely attempting to get ahead of future uncertainty surrounding auto pricing levels by taking advantage of March deals,” said Chris Hopson, principal analyst at S&P Global Mobility, in a news release at the end of March. That said, spending among other categories was strong, as well. Stripping out sales of autos and gasoline, retail sales notched a monthly gain of 0.8%, higher than projections for a 0.5% increase.

3. US Mortgage Rates Jump Most Since October, Denting Home Demand — the contract rate on a 30-year mortgage increased 20 basis points in the week ended April 11 to 6.81%, the highest since February, according to Mortgage Bankers Association data released Wednesday. Rates on adjustable and 15-year fixed mortgages also climbed. The jump in financing costs brought an abrupt end to a six-week stretch of increasing home-purchase applications, highlighting home-buyer sensitivity to interest rates as housing prices remain elevated. MBA’s purchase applications index dropped 4.9%. The refinancing gauge slumped more than 12%, the fourth decline in the last five weeks. Mortgage rates track yields on 10-year Treasuries, which soared last week by a half percentage point as the trade war shakes global markets. The weekly surge in yields was the largest in more than two decades, raising fears the US is losing its status as the world’s safe haven. Yields have gradually retreated so far this week.

4. Trump Lashes Out at Powell, Says ‘Termination Cannot Come Fast Enough’ — late last week, in the Oval Office, Trump told reporters he had the power to dismiss Powell as Fed chair—a position that is at odds with Powell’s view of the law. Trump is upset that the Fed isn’t lowering interest rates to cushion the fallout from his trade war. Powell is “too late. He’s always too late, little slow,” Trump said. Inflation in the U.S. could rise more than in other countries in the coming months because Trump has imposed a range of tariffs. Whether the Fed chair can be removed before the end of a four-year term is an open question because it has never been attempted. Trump is trying to dismiss several other Biden appointees who have challenged their removal by citing a 90-year legal precedent that has shielded them from dismissal over a policy dispute.

The week ahead — Economic data from Econoday.com:

“keep your head while others are losing theirs” Rudyard Kipling

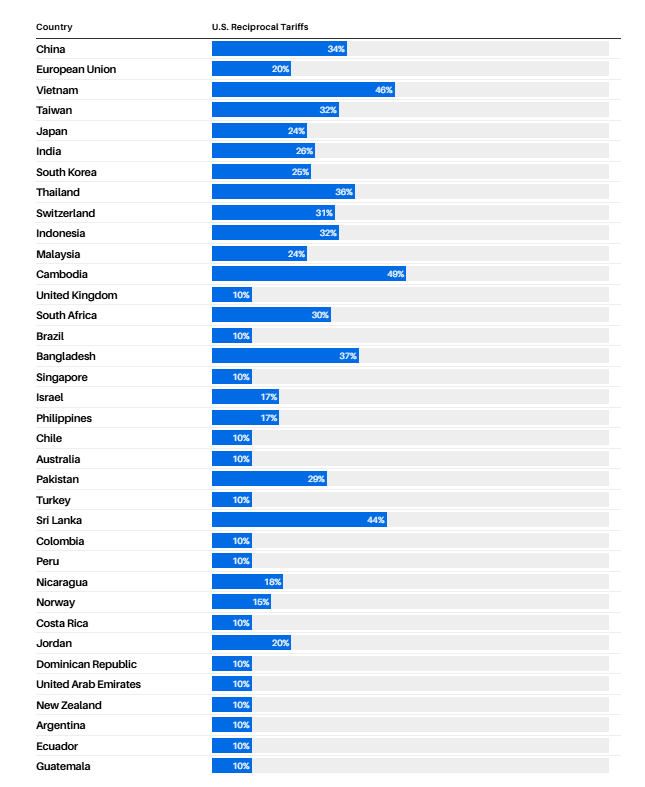

1. Trump: 10% Tariffs Across the Board. ‘Worst’ Trade Partners Will Pay More — Trump presented a large chart listing the specific tariff levels for certain countries, which can be seen below. These include a 34% tariff on goods from China, 46% on those from Vietnam, and 32% on those from Taiwan. Cambodia has the highest tariff rate of any country at 49%. Goods from the European Union will be levied at a 20% rate. “You know, you think of European Union, very friendly. They rip us off. It’s so sad to see. It’s so pathetic,” he said.

2. US Services Index Falters as Employment Shrinks Most Since 2023 — The Institute for Supply Management’s gauge of services dropped to 50.8 from 53.5 a month earlier, according to data released Thursday. The figure was weaker than all but one estimate in a Bloomberg survey of economists. Readings above 50 signal growth. A month earlier, the employment index advanced to the highest level since the end of 2021. A Wednesday report showed private-sector hiring accelerated in March by more than projected in a fairly broad advance.

A sustained trend of weaker employment readings may raise concerns of a broader slowdown in a labor market that has been the economy’s bedrock. Meanwhile, the ISM prices-paid index eased slightly to a still-elevated 60.9 in March.

3. Trump Pauses ‘Reciprocal’ Tariffs, but Hits China Harder — Trump said Wednesday that his 10%, baseline tariff on virtually all imports would stay in effect. But he implemented a 90-day pause for the higher, so-called reciprocal rates he had announced a week earlier on nations the administration views as “bad actors” on trade—except for China. In an early afternoon social-media post, Trump wrote that he had raised the tariff imposed on China to 125%, “effective immediately.” An administration official said that Canada and Mexico would remain exempt, for now, from the 10% baseline global tariff. While America’s neighbors remain subject to plans to impose 25% tariffs on most imports to the U.S. for what Trump says is their role in fueling the fentanyl crisis, an exemption is still in place for these levies on autos and many other goods compliant with the U.S.-Mexico-Canada trade agreement.

4. Consumer Sentiment Sinks, Approaching Three-year Low with Inflation Worries Highest Since 1981 — The University of Michigan’s gauge of consumer sentiment fell to 50.8% in a preliminary April reading from 57.0% in the prior month. It is the lowest level since June 2022. Sentiment has dropped for four straight months and is down 30% from December. Federal Reserve economists believe that if consumers expect high inflation, it will be easier for firms to raise prices, leading to higher price pressure.

The week ahead — Economic data from Econoday.com:

1. Conference Board’s Consumer Survey Drops to 12-Year Low — the Conference Board’s monthly survey showed that forward-looking expectations for income, business and labor-market conditions dropped to the lowest level in 12 years, hitting an index level of 65.2. Levels below 80 often signal a recession, the Conference Board said. Meanwhile, the survey’s index showing consumers’ view of the current situation fell to 92.9, down 7.2 points from a month earlier, marking the fourth straight month of declines. Economists polled by The Wall Street Journal had expected the index to land at 93.5 in March. Analysts have been keeping a close eye on consumer surveys because of mounting evidence of a gloomy mood that could presage a real economic slowdown. In surveys of families and businesses alike in recent weeks, new tariffs are emerging as a central concern. But so far, there has been scant sign of a slowdown in backward-looking data such as the unemployment rate and GDP figures that show what has actually happened in the economy.

2. Trump Plans 25% Tariff on Imported Vehicles — President Trump said he would impose 25% tariffs on global automotive imports to the U.S., making good on a pledge to impose duties on cars and trucks from other nations. The U.S. will start collecting the auto tariffs on April 3, Trump said, the day after he is slated to announce a broader slate of trade actions. Trump’s so-called reciprocal tariffs, slated for that day, were originally planned to equalize U.S. tariffs with those charged by foreign nations, but Trump said Wednesday that the tariffs he plans to implement would likely be lower than that. Trump also said the reciprocal tariffs will target “all countries,” and not just the 15% of nations that Treasury Secretary Scott Bessent had said could be given priority in the April 2 action.

Trump’s team has whipsawed between a maximalist approach to tariffs and offering potential leniency for companies and trading partners. Trump originally said he would impose sector-specific tariffs on industries such as semiconductors, lumber and pharmaceuticals on April 2. But he reiterated on Wednesday that those industry-specific tariffs wouldn’t happen on that date, though they could be announced later.

3. RFK Jr. to Unveil Plans to Cut 10,000 Health Department Workers — Kennedy plans to cut 10,000 employees, according to a statement Thursday. Combined with other departures from buyouts, the reductions mean the agency will employ 62,000 workers, down from 82,000. The secretary also intends to consolidate the department’s 28 divisions into 15 and cut regional offices from 10 to five. HHS said it plans to lay off 3,500 employees at the Food and Drug Administration, but those cuts will not include drug, medical device or food reviewers or inspectors. The CDC workforce will be cut by around 2,400 people. Around 1,200 more employees will be laid off at the National Institutes of Health, mostly focused on purchasing, human resources, and communications.

4. US Consumer Spending Barely Rises, Key Inflation Gauge Picks Up — Consumer spending was weaker than expected again in February while a key inflation metric picked up, in a double whammy for the economy before the brunt of tariffs. Inflation-adjusted consumer spending edged up 0.1%, on the low end of economists’ estimates, after a slump January that analysts mostly blamed on bad weather. Notably in February, Americans reduced spending on services for the first time in three years in the face of higher prices — including on dining out. The Federal Reserve’s preferred inflation rose 0.4% from January, the most in a year, according to Bureau of Economic Analysis data out Friday. The so-called core personal consumption expenditures price index, which excludes food and energy items, was up 2.8% from last year, remaining stubbornly above the Fed’s 2% target.

The week ahead — Economic data from Econoday.com:

“Hope is a bogus emotion that only costs you money.” – Jim Cramer

1. The Fed Keeps Rates Steady but Expects 2 Cuts This Year — Faced with pressing concerns over the impact tariffs will have on a slowing economy, the rate-setting Federal Open Market Committee kept its key borrowing rate targeted in a range between 4.25%-4.5%, where it has been since December. Markets had been pricing in virtually zero chance of a move at this week’s two-day policy meeting.

Along with the decision, officials updated their rate and economic projections for this year and through 2027 and altered the pace at which they are reducing bond holdings. Despite the uncertain impact of President Donald Trump’s tariffs as well as an ambitious fiscal policy of tax breaks and deregulation, officials said they still see another half percentage point of rate cuts through 2025. The Fed prefers to move in quarter percentage point increments, so that would mean two reductions this year.

2. Trump Fires Two Democratic FTC Commissioners — President Trump fired the Federal Trade Commission’s two Democratic commissioners on Tuesday, the latest moves in his campaign to exert more control over independent government agencies. The move runs counter to current Supreme Court precedent that says the FTC’s commissioners can only be removed for cause. The Trump administration has been clear that it is eager to see that precedent revisited. The FTC is one of several commissions that were created to be bipartisan. It isn’t supposed to have more than three members from the same political party. After Tuesday’s dismissals, it will only have two members—Ferguson and fellow Republican Melissa Holyoak—both of whom are Republicans.

3. Trump Signs Order Seeking to Abolish Education Department — Trump’s order directs McMahon, co-founder of World Wrestling Entertainment, to facilitate the closure of the agency to the maximum extent possible and permitted by law. McMahon will face a number of complications in closing the department, a task she has called its “final mission.” Existing law doesn’t allow the president to unilaterally close a department, such as Education, that has been established by Congress. Republicans hold a 53-47 majority in the Senate, giving them control of the chamber, but it is unlikely they would be able to gain support from Democrats to reach a filibuster-proof 60-vote majority to completely unwind the agency.

4. Small Business Administration Planning to Cut More Than 40% of Its Workforce — the extensive workforce reduction and restructuring will take the SBA, an agency with more than 6,500 employees, back to prepandemic staffing levels by eliminating around 2,700 positions. The cuts will affect nonessential roles at the agency, and include voluntary resignations and the expiration of appointments made during the Covid-19 pandemic, the people said. The SBA expanded in size during the Covid-19 pandemic to support programs such as the Paycheck Protection Program, and other small-business initiatives put in place during the Biden administration. The SBA will also expand personnel for disaster loan support and recovery efforts, according to the people.

The week ahead — Economic data from Econoday.com:

“If most traders would learn to sit on their hands 50 percent of the time, they would make a lot more money.” – Bill Lipschutz

1. Trump Doubles Tariffs on Canadian Steel and Aluminum — President Donald Trump said last week that he plans to double the rate of tax on imports of Canadian steel and aluminum after Ontario retaliated against earlier tariffs with higher levies on electricity sent to the U.S. The move comes only days after Trump delayed most of the tariffs on Canada and Mexico until April. Trump also cited Canadian tariffs on dairy products, promised to increase charges on cars, and said Canada relies too much on the U.S. for defense.

2. Ukraine Accepts US-Brokered Ceasefire Plan in Deal for Aid — Ukraine accepted a US proposal for a 30-day truce with Russia as part of a deal with the Trump administration to lift its freeze on military aid and intelligence for Kyiv. The agreement laid out in a joint statement follows eight hours of talks in Saudi Arabia on Tuesday that raised the possibility of a pause of hostilities in Russia’s three-year war that’s ravaged Ukraine. Trump said US officials will speak to their Russian counterparts on Wednesday and that it’s possible he’ll talk to Putin this week.

3. Inflation Cooled to 2.8% in February, Lower Than Expected — Consumer prices were up 2.8% in February from a year earlier, the Labor Department reported last Wednesday, versus a January gain of 3%. Economists polled by The Wall Street Journal had expected a 2.9% gain. Prices excluding food and energy categories—the so-called core measure that economists watch in an effort to better capture inflation’s underlying trend—rose 3.1%. That was the lowest year-over-year reading since 2021. Economists are struggling to keep up with the recent tariff news, but are pushing up their inflation estimates nonetheless. Goldman Sachs economists last week raised their forecast for the Commerce Department’s core inflation gauge to 2.9% in the coming fourth quarter from a year earlier. That compared with a previous estimate of 2.4%.

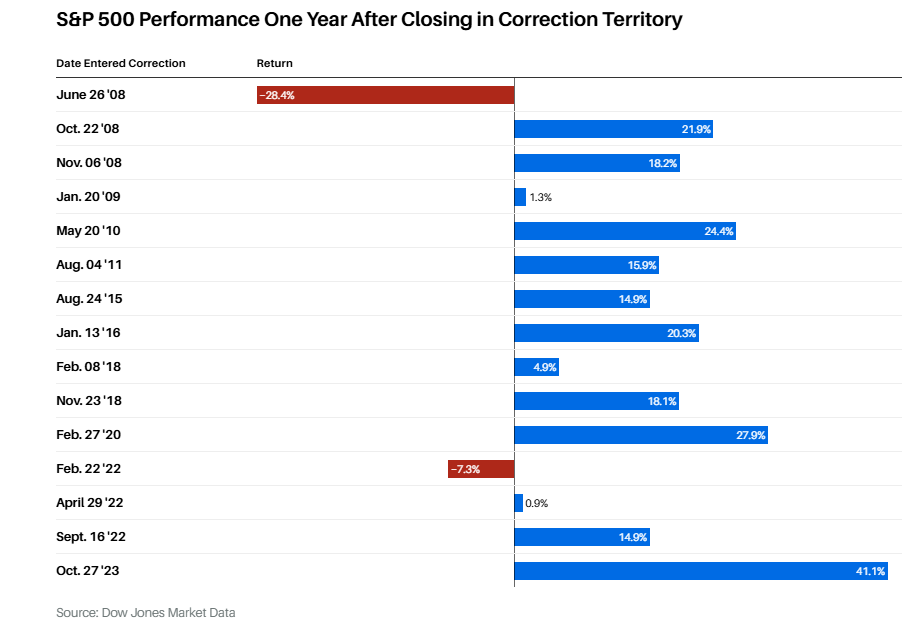

4. Consumer Sentiment Slides in March as Inflation Expectations Jump — The University of Michigan’s consumer sentiment index fell to a reading of 57.9 in the first weeks of March, according to preliminary figures released Friday. Economists were expecting the index would fall to a reading of 64 from February’s 64.7. The declines in sentiment were seen consistently across all groups by age, education, income, wealth, geographic regions, and political affiliations, Hsu said. Republicans, who had thus far remained fairly upbeat about the economy, posted a 10% decline in their expectations for the future. For Independents and Democrats, the expectations index declined 12% and 24%, respectively. On a separate note, below is the stat of the SPY performance 1-year after entering correction.

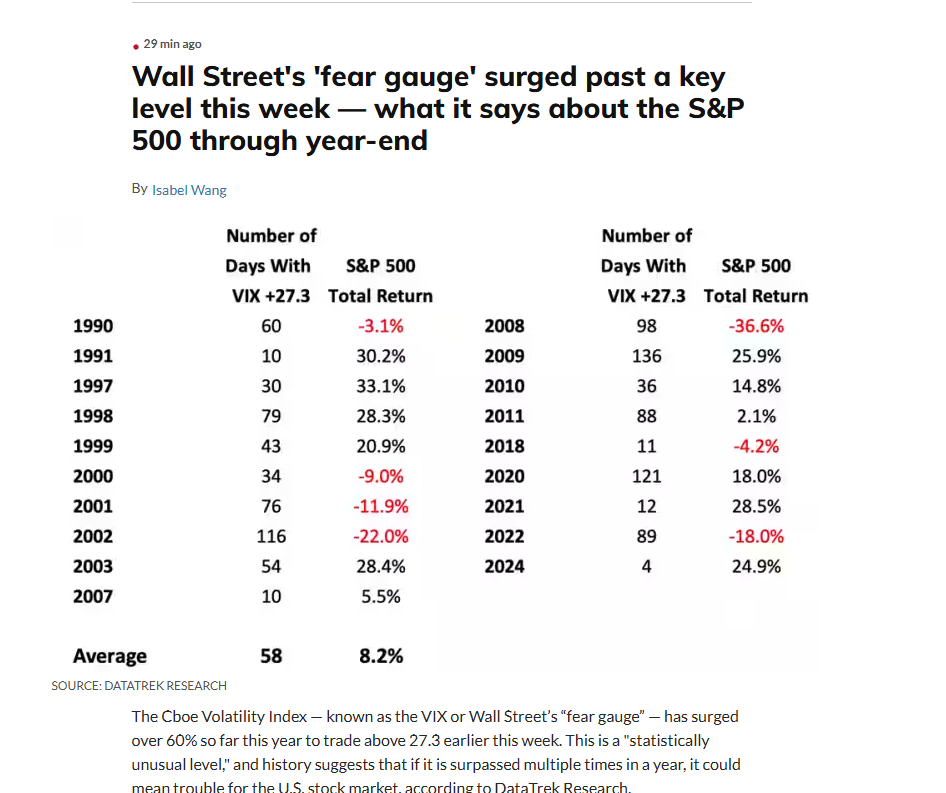

VIX Fear Gauge Statistics

Posted in Weekly Summary | No Comments »

Posted in Weekly Summary | No Comments »

© Copyright 2026 Market Outlook All Rights Reserved

Design by EGS

Sponsored by Equity Guidance LLC

Posted in

Posted in  Posted in

Posted in  Posted in

Posted in