August 21st, 2018

“The game of speculation is the most uniformly fascinating game in the world. But it is not a game for the stupid, the mentally lazy, the person of inferior emotional balance, or the get-rich-quick adventurer. They will die poor.” – Jesse Livermore

1. Turkey Retaliated With Tariffs on U.S. Cars, Alcohol, Tobacco — a reeling Turkey has responded to U.S. tariffs with retaliatory duties on U.S. passenger cars, alcohol, tobacco, cosmetics and other products. Tariffs on cars are set to rise by 120% and those on made-in-the-U.S. alcoholic drinks by 140%, alongside a 60% increase on tobacco products. The move comes amid increasing fears of contagion from Turkey’s collapse.

2. China, U.S. to Resume Trade Talks This Month — China will send a delegation to the United States later in August to resume trade talks that largely broke down a couple of months ago. Vice Commerce Minister Wang Shouwen will discuss economic and trade issues with U.S. counterpart David Malpass in a new attempt at defusing a trade war that has resulted in billions of dollars in tariffs so far, with threats of more. Formal talks between the U.S. and China broke down last month and led to dueling tariffs.

3. Amazon Eyes Online U.K. Healthcare Market — Major insurance firms in Europe have been invited by Amazon (NASDAQ:AMZN) to participate in a U.K. price comparison website. While there are no firm details on a launch by Amazon into financial services in the region, online insurance comparison players such as AXA (OTCQX:AXAHF), Hastings (OTC:HNGGF), Esure (OTC:ESXRY) and GoCompare are on watch.

4. Federal Probe Focuses On Apartment Mortgage Fraud — WSJ reported the investigation, still in its early stages, has so far resulted in a fraud-conspiracy indictment against four real-estate executives in upstate New York for falsifying information that helped them secure loans multi-family properties. The indictments made fraud-conspiracy charges against Todd Morgan and Kevin Morgan, a son and nephew of Robert Morgan, and charged their mortgage brokers, Frank Giacobbe and Patrick Ogiony of Aurora Capital Advisors. One owner of properties investigators reviewed is Robert C. Morgan, who ran a firm called Morgan Management LLC, but changed its name in June to Grand Atlas Property Management.

5. Q2 Latest Hedge Fund 13F — Hedge funds have finished up reporting on the investments they held at the end of Q2. New portfolio additions such as Keurig Dr Pepper (NYSE:KDP) by Citadel, Groupon (NASDAQ:GRPN) by Engaged Capital and GrubHub (NYSE:GRUB) by Jana Partners. Perhaps not a surprise, Alibaba (NYSE:BABA) was one of the names that cropped up the most times in the portfolio updates. Facebook (NASDAQ:FB) was added by at least six funds in Q2 as a new addition, while ten funds dropped the tech stock or trimmed exposure. In addition, Berkshire boosts stakes in Apple, US Bank, Teva, BNY Mellon, Delta in Q2 — in the latest 13F from Berkshire Hathaway (BRK.A, BRK.B) showed its stake in Apple (AAPL) as boosted to about 252M shares as of June 30 – up roughly 5% from three months earlier. The Oracle and company also added to holdings in U.S. Bancorp (NYSE:USB), Teva Pharmaceuticals (NYSE:TEVA), Bank of New York Mellon (NYSE:BK), General Motors (NYSE:GM), and Goldman Sachs (NYSE:GS). Among those showing trimmed stakes were American Airlines (NASDAQ:AAL), Phillips 66 (NYSE:PSX), Charter Communications (NASDAQ:CHTR), and Wells Fargo (NYSE:WFC).

6. U.S. Seen Near Deal with Mexico On Revised NAFTA But Canada Remains Apart — the U.S. is close to reaching a deal with Mexico on a revamped North American Free Trade Agreement, but thorny issues are yet to be resolved with Canada, according to reports. Both Mexico and the U.S. are seen as having strong incentives to push through a deal quickly: Mexico wants to lock in an agreement before its new leftist president takes office, and the Trump administration wants a win on trade ahead of the midterm elections. U.S. negotiators this week have been meeting with senior Mexican officials in Washington, and the two sides are said to have largely agreed to new rules on auto trade – a top White House priority – that could boost investment in the U.S. President Trump says he is “in no hurry” to complete a NAFTA deal, remarks seen mostly as an attempt to put pressure on Canada.

The week ahead — Economic data from Econoday.com:

Tags: 2Q 13F, NAFTA Deal, Turkey Row

Posted in Weekly Summary | No Comments »

August 13th, 2018

“The markets are always changing, and the successful trader needs to adapt to these changes” — Michael Steinhardt

1. U.S. Reimposes Sanctions on Iran — the first batch of American sanctions on Iran has come into effect, 90 days after the U.S. withdrew from the nuclear deal. The new measures bar the sale of U.S. currency to Iran’s government, sanction trade in precious metals and industrial materials, outlaw the purchase of Iran’s sovereign debt, and restrict the country’s auto and aerospace sector. Unless Iran complies with the U.S. demands, far-tougher steps will take effect on Nov. 5, when the U.S. will cut off Iran’s oil exports and impose sanctions on shipping.

2. China Outspent the U.S. in 5G — since 2015, China has outspent the U.S. by $24B in 5G infrastructure, potentially creating a “tsunami” that will be difficult to catch up with, according to a new study by Deloitte. China has built 350,000 new cell sites, while the U.S. has built fewer than 30,000 in the same time frame. 5G would support connected infrastructure in cities, including driverless cars, and make it possible for people to stream high-bandwidth video.

3. SEC Delayed Decision & Bitcoin Crashes Under $6,500 — the crypto reaching as high as $8,496 in July, but its latest descent has seen the digital currency fall overnight to under $6,500. The move was accelerated after the SEC pushed back an eagerly-awaited decision on the SolidX Bitcoin ETF (XBTC), sponsored by SolidX Management with marketing assistance from Van Eck Securities. A verdict is now expected by the end of September.

4. U.S.-Japan Enters New Trade Talks — Japan and the U.S. are headed for a new round of trade talks today in Washington. Economic Revitalization Minister Toshimitsu Motegi will try to avert steep tariffs on car exports and stress the significance of multilateral free trade, with an eye on persuading the U.S. to return to the TPP. The world’s third-largest economy will also face demands from U.S. Trade Representative Robert Lighthizer, including a trade deficit reduction and the further opening of Japan’s automobile and agriculture markets.

5. Turkish Crisis Rattles Global Markets Amid Escalating Spat With U.S. — the lira dropped as much as 25% against the dollar, extending a tumble that ranks as one of the steepest in world markets this year. Turkey’s problems are spilling over into the greater market following reports that the ECB is concerned over the impact of a weak lira on European banks, especially BBVA, UniCredit (OTCPK:UNCFF), and BNP Paribas (OTCQX:BNPQF). Data from the BIS also showed the currency, which plunged 13.5% overnight to an all-time low against the dollar, will weigh on banking exposure internationally.

The week ahead — Economic data from Econoday.com:

Tags: Turkish Lira Crashes

Posted in Weekly Summary | No Comments »

August 6th, 2018

“Focus, patience, wise discernment, non-attachment —the skills you acquire in meditation and the skills you need to thrive in trading are one and the same.” — unknown

1. Iran’s Rial Hits Record Low — Iran’s currency hit a historic low of 100,000 rials to the dollar over the weekend. The collapse, which has seen the currency lose half its value in just four months, was encouraged by a deepening economic crisis and the imminent return of full U.S. sanctions. The penalties will be reimposed in two stages on Aug. 6 and Nov. 4, forcing many foreign firms to sever business ties with Tehran.

2. Japan, U.S., Australia Plan Infrastructure Push in Asia — forming a trilateral partnership, Australia and Japan have joined the U.S. in a push to invest in infrastructure projects in the Indo-Pacific region as China spends billions of dollars on its Belt and Road initiative across Asia. The investments will include energy, transportation, tourism and technology infrastructure, with the governments aiming to attract private capital to projects.

3. U.S.-China Trade War Back in Focus — the two countries are seeking to resume talks to defuse a tariff battle, according to Bloomberg, although later reports suggested the Trump administration plans to propose tariffs of 25% on $200B of imported Chinese goods after initially setting them at 10%. The Caixin-Markit PMI overnight also showed China’s manufacturing sector growing at its slowest pace in eight months in July, dragged down by declining export orders.

4. Molson Coors Canada and Hydropothecary Announces a Joint Venture — the Canadian unit of Molson Coors (NYSE:TAP) has entered a deal that will allow it to develop cannabis-infused beverages in the Great White North. It’s teaming up with Canadian cannabis producer Hydropothecary (OTCPK:HYYDF) to “participate in this exciting and rapidly expanding consumer segment.” Marijuana use in Canada will become legal later this year.

5. China Dethroned By Japan As World’s No. 2 Stock Market — an intensifying trade spat with the U.S. just led China to cede its four-year title as the world’s second-largest stock market to Japan. After a last week slump, Chinese equities were valued at US$6.09T, losing out to Japan’s $6.17T, while the U.S. remains the world’s largest with a market cap of $31T. The Shanghai Composite Index has lost more than 16% YTD to be among the world’s worst performers, while the yuan has fallen 5.3% against the dollar.

6. Apple Market Cap Over $1T — Apple hit a market cap of $1T last week, becoming the first publicly traded U.S. company to reach the milestone. Many credit the company’s growing software and services sales with driving the valuation. The catch-all category – which includes the App Store (NASDAQ:AAPL), AppleCare, Apple Pay, iTunes and cloud services – posted record revenue of $9.55B for the June quarter.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

July 30th, 2018

“Sometimes the best trade is no trade.” – Anonymous

1. G20 Finance Ministers Release Communique — world financial leaders called for stepped-up dialogue at a G20 meeting last Saturday, but ended the gathering with little consensus on how to resolve multiple disputes over U.S. tariff actions. The communique noted while growth is strong, it’s becoming less synchronized amid downside risks, including financial vulnerabilities, and heightened trade and geopolitical tensions. Ahead of the summit, Treasury Secretary Steven Mnuchin said he “wouldn’t minimize” the possibility that the U.S. will impose tariffs on all $500B worth of goods that the U.S. imports from China. He also discussed trade tensions with the EU. “If Europe believes in free trade, we’re ready to sign a free-trade agreement,” adding that any deal would have to eliminate tariffs, along with other barriers and subsidies.

2. U.S. Economy Grew at 4.1% Rate in Second Quarter — gross domestic product (GDP) — the value of all goods and services produced across the economy—rose at a seasonally and inflation-adjusted annual rate of 4.1% from April through June, the Commerce Department reported last Friday. The Commerce Department said U.S. soybean exports surged in the second quarter, delivering an outsize boon to economic growth even as China shifted much of its sourcing to Brazil in response to its worsening trade relations with the U.S. The export rally likely reflected efforts by buyers to get their soybeans before China’s 25% retaliatory tariffs on U.S. soybeans, which hit in July.

3. Venezuela To Lop Five Zeros Off Currency — Venezuela is delaying its planned currency re-denomination by two weeks to Aug. 20, lopping five zeroes off the refurbished bolivar (instead of three) and linking it to the country’s Petro cryptocurrency. It comes in response to Venezuela’s hyperinflation, which the IMF has said will soar to 1,000,000% this year, throwing the OPEC nation’s already battered economy into a deeper tailspin.

4. Trump Reportedly Wins EU Trade Concessions — President Trump announced at a press conference late last week with the EU’s Jean-Claude Juncker “We agreed today to work together towards zero tariffs, zero non-tariff barriers and zero subsidies for the non-auto industrial goods,”. The U.S. secured further trade concessions, including the import of more soybeans and possibly some liquefied natural gas, while potential auto tariffs will be sidelined as the two sides launch negotiations to cut other trade barriers.

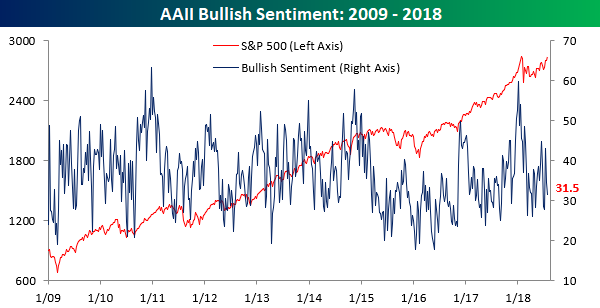

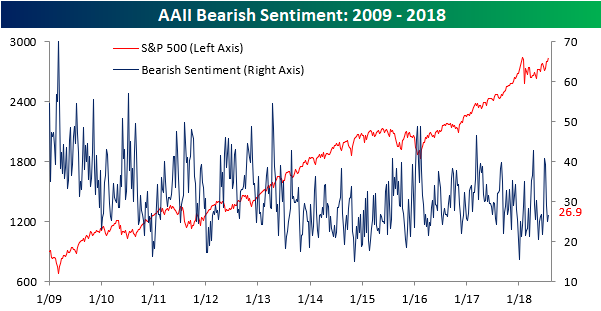

5. AAII Weekly Sentiment — courtesy of BIG, according to this week’s report, bullish sentiment declined for the second week in a row, falling from 34.66% down to 31.52%.

As bullish sentiment declined, bearish sentiment ticked up from just under 25% to just under 27%.

The week ahead — Economic data from Econoday.com:

Tags: AAII Weekly Sentiment, US EU Trade War

Posted in Weekly Summary | No Comments »

July 23rd, 2018

“Where you want to be is always in control, never wishing, always trading, and always first and foremost protecting your butt.” – Paul Tudor Jones

1. Farnborough Airshow — the most important aviation trade show of the year has begun, attracting about 100,000 trade visitors from 100 countries. Alternating every year with the Paris Air Show in France, the Farnborough International Air Show runs until July 22. Boeing (NYSE:BA) kickstarted the exhibition with a $4.7B deal for freight planes with delivery company DHL and the firm purchase of 30 737 MAX 8s with leasing firm Jackson Square. Airbus (OTCPK:EADSY) is already plotting its revenge. It’s working on a blockbuster agreement to sell $23B worth of aircraft to AirAsia, as well as confirming a $9B order from StarLux and Sichuan Airlines.

2. Oil Dips Below $70 on Saudi Offer, SPR Release — Saudi Arabia is said to have offered extra crude to some customers, extending additional cargoes of its Arab Extra Light crude to at least two buyers in Asia, Bloomberg reported. The Trump administration is also actively considering tapping into the U.S.’s 660M-barrel Strategic Petroleum Reserve as political pressure grows to rein in rising gas prices before November elections.

3. U.S. Files Trading Complaints at WTO — the U.S. has filed separate claims with the World Trade Organization against China, the EU, Canada, Mexico and Turkey after the countries lodged complaints over the Trump administration’s steel and aluminum tariffs. President Trump has repeatedly raised the prospects of withdrawing from the WTO, although this month he said that no withdrawal was planned for now. Amid the trade tensions, Chinese mainland stocks are down almost 30% since their peak in January.

4. Japan, EU Sign Trade Agreement — Japan and the EU have signed the world’s largest bilateral trade pact covering about a third of global GDP. The deal, which involved significant concessions on both sides, will eventually reduce heavy Japanese tariffs on European wine, cheese and other foods and lift EU tariffs on Japanese cars and vehicle parts.

5. EU Mulls U.S. Tariffs on Coal, Pharma, Chemicals — the EU will consider introducing tariffs on coal, pharmaceuticals and chemical products from the U.S. if President Trump imposes restrictions on European cars, Germany’s Wirtschaftswoche magazine reported. The potential trade measures will be decided based on the outcome of a meeting next week in Washington between European Commission President Jean-Claude Juncker and President Trump. However, Commerce Secretary Wilbur Ross said it’s “too early” to say whether the Trump administration will move ahead with proposed tariffs of as much as 25% on imported vehicles and auto parts .

The week ahead — Economic data from Econoday.com:

Tags: US EU Trade War

Posted in Weekly Summary | No Comments »

July 16th, 2018

“Accepting losses is the most important single investment device to insure safety of capital.” – Gerald M. Loeb

1. Payments Halted Under Obamacare Program — the Trump administration is suspending a program that pays insurers to stabilize health insurance markets under Obamacare, saying that a recent federal court ruling prevents the money from being disbursed. Based on their 2017 business, the payments amount to $10.4B. With 20M Americans receiving health insurance through the Affordable Care Act, the latest freeze could increase uncertainty and drive up premiums this fall.

2. Brett Kavanaugh Nominated to Supreme Court — Brett Kavanaugh has been nominated for the U.S. Supreme Court, although a tough confirmation fight lies ahead in the Senate. As an ideological conservative he’s expected to push the court to the right on a number of issues, including business regulation. Kavanaugh has been critical of the expanding powers of federal agencies, including on measures like labor rights, credit-card fees and “payday” loans, and has also cast doubt on the constitutionality of the Consumer Financial Protection Bureau. Kavanaugh is widely viewed as being more conservative than Justice Anthony Kennedy, whom Kavanaugh has been nominated to replace.

3. China Ups Tariffs on U.S. Fiber Products — China’s commerce ministry will raise “anti-dumping tariff rates” tomorrow on some optical fiber products originating from the U.S., increasing the levy range to between 33.3% to 78.2%, compared with 4.7% to 18.6% as set in 2011. U.S. companies, including Corning (NYSE:GLW), OFS Fitel (OTCPK:FUWAY) and Draka Communications Americas, are among the firms affected by the change. the Trump administration raised the stakes in its trade war with China, saying it would slap 10% tariffs on an extra $200B worth of Chinese imports. The new list appears to target Beijing’s important manufacturing export industries, going after electronics, textiles, metal components and auto parts.

4. China’s Trade Surplus with U.S. Hits Record — China’s trade surplus with the U.S. swelled to a record in June, a result that could further inflame trade tensions with Washington. Exports to the world’s largest economy rose 5.7%, while imports from the U.S. rose 4%, resulting in a trade surplus of $28.97B. Separately, an explosion at a chemical plant in China overnight killed 19 people and injured 12, marking the latest deadly industrial incident in the country.

5. Index Correlation of 2018 VS Prior Years — courtesy of BIG, in comparing the S&P 500’s performance in 2018 to prior years, correlation of the closing prices – through July 11, of the S&P 500 to every year since 1928. Statistically, just two years correlated strongly with 2018: 1942 and 1980, when the rest of the year was up 11% and 15%, respectively.

The week ahead — Economic data from Econoday.com:

Tags: US-China TradeWars

Posted in Weekly Summary | No Comments »

July 9th, 2018

“If you take emotion – would be, could be, should be – out of it, and look at what is, and quantify it, I think you have a big advantage over most human beings.” — John Henry

1. EU Warns U.S. of $300B in Tariffs — the EU warns that if the U.S. goes ahead with punitive tariffs against EU car imports, the European Commission will likely apply countermeasures worth as much as $294B – about 19% of U.S. goods exports in 2017. The measures risk plunging the global economy into a full-scale trade war, as it will harm employment in the U.S. auto sector, which accounts for more than 4M jobs.

2. Trump Warns the WTO — A statement by President Trump that the administration won’t take any action against the World Trade Organization unless the organization is “unfair” to the U.S. While the latest rhetoric is a downshift in tone, concerns of a standoff still remain. Height Capital Markets warned of the “immense” economic downside from U.S. action against the WTO. The investment firm noted that while Trump cannot roll back the U.S statute agreeing to the WTO, he can signal U.S. withdrawal under the structure of the WTO agreement. “However, this quirk of US law – enabling the President to claim the U.S. is withdrawing even as U.S. law differs – does not guarantee that other nations would still grant the US the protections afforded to a member of the WTO,” .

3. Feds Expand Data Probe into Facebook — Federal agencies are reportedly turning up the heat on Facebook (NASDAQ:FB), with the FBI, SEC and FTC joining the Justice Dept. in probing the company’s response to the Cambridge Analytica data sharing scandal. The focus of the agencies is on squaring Facebook’s statements about the affair with the underlying facts, as well as how forthcoming and prompt the company has been in cooperating.

4. First Half 2018 Asset Class Performance Matrix — courtesy of BIG, below highlights the performance of various asset classes of ETFs during the first half of 2018.

At the halfway point of 2018, small-caps have trumped large-caps, while growth has crushed value. Looking at sectors, Consumer Discretionary (NYSEARCA:XLY), Technology (NYSEARCA:XLK), and Energy (NYSEARCA:XLE) have been the best performers so far this year, while Consumer Staples (NYSEARCA:XLP), Financials (NYSEARCA:XLF), Materials (NYSEARCA:XLB), and Industrials (NYSEARCA:XLI) are solidly in the red.

5. U.S. Offers German Carmakers ‘Zero Tariffs’ Solution — Germany’s big three automakers – BMW (OTCPK:BAMXF), Volkswagen (OTCPK:VLKAF) and Mercedes-parent Daimler (OTCPK:DDAIF) – met with U.S. Ambassador to Germany Richard Grenell, stating they would support the elimination of EU tariffs on imported American cars provided the U.S. did the same. While EU tariffs on passenger cars are 10%, versus 2.5% in the U.S., the latter imposes import duties of 25% on European vans and pick-up trucks.

6. U.S.-China Trade War Started — Accusing the U.S. of “launching the largest trade war in economic history to date,” Beijing has implemented retaliatory tariffs on 545 items worth $34B in response to the comparable U.S. duties that were enacted at midnight. Another $16B in tariffs are expected to go into effect in two weeks, and President Trump has warned of additional levies on $500B in Chinese goods.

The week ahead — Economic data from Econoday.com:

Tags: US-China TradeWars

Posted in Weekly Summary | No Comments »

July 2nd, 2018

“I always define my risk, and I don’t have to worry about it.” – Tony Saliba

1. EU Responds to U.S. Auto Tariff Threat — after President Trump threatened to impose a 20% tariff on all imports of EU-assembled cars, EU Commission Vice President Jyrki Katainen told French newspaper Le Monde “If they decide to raise their import tariffs, we’ll have no choice, again, but to react,”.

2. GE Plans Healthcare Spinoff, Baker Hughes Stake Sale — the once industrial conglomerate is spinning off its healthcare business and unloading ownership in its oil services company Baker Hughes (NYSE:BHGE). The final turnaround plan from CEO John Flannery. GE will focus on its power, aviation and renewable-energy divisions. The company was booted out of the Dow Jones Index and was replaced by Walgreen Boots.

3. Canada Prepares Moves to Block Chinese Steel Diverted from U.S. — Canada is preparing tariffs and quotas on steel from China and other countries to prevent a potential flood of imports from global producers seeking to avoid U.S. tariffs. The Bloomberg report follows warnings from the Canadian steel industry and the EU’s decision to ward off the dumping of steel that would have been sent to the U.S.

4. Amazon’s New Last-Mile Delivery Service — Amazon is building out its own last-mile delivery service, pushing further onto the turf of shipping partners UPS and FedEx (NYSE:FDX). The new program, called Delivery Service Partners, will let entrepreneurs run their own local delivery networks of up to 40 delivery vans emblazoned with Prime logos. “This is all about scaling cost effectively,” said Dave Clark, SVP of Amazon Worldwide Operations (NASDAQ:AMZN).

5. AAII Weekly Bearish Sentiment Surges — according to the latest weekly sentiment survey from AAII, bullish sentiment dropped more than ten percentage points, falling from 38.7% down to 28.4% in what was the largest one week decline since early March.

Meanwhile, bearish sentiment surged, rising from 26.2% up to 40.8% in what is only the second week in the last year where bearish sentiment has been above 40%. More importantly, though, it was the largest one week increase in negative sentiment since January 2016, which also happens to be another time when a plunging Chinese stock market was in the headlines.

The week ahead — Economic data from Econoday.com:

Tags: AAII Weekly Sentiment

Posted in Weekly Summary | No Comments »

June 25th, 2018

“If you personalize losses, you can’t trade.” — Bruce Kovner

1. Trump Directs More Tariffs at China — Trump asked the United States Trade Representative to identify $200 billion worth of Chinese goods for additional tariffs, at a rate of 10 percent. If China “refuses to change its practices” and insists on continuing with the new tariffs it recently declared, then the additional levies would be imposed on Beijing. However, the Chinese Commerce Ministry issued a response, stating that the latest threat of more tariffs violates previous negotiations and consensus reached between both the U.S. and China. Furthermore, President Trump has threatened a further $200B in tariffs on Chinese products should Beijing hit back again, bringing to $450B the potential amount that could be targeted. That sum approaches the roughly $500B in total annual Chinese exports to the U.S. As the trade war unfolds, the Trump administration is also working on measures that protect agriculture and other critical industries from retaliatory tariffs being threatened by China.

2. New York Sues 3M Over Toxic Foam — New York state is going after 3M (NYSE:MMM) and five other manufacturers for the almost $39M the government has spent to protect residents from the toxic firefighting foams made by the companies. Their use at five military and civilian airports in the state caused “extensive contamination” to nearby fish, soil and water, and increased the risk to people of immune system damage and other health problems.

3. China Threatens to Strike Dow-Listed Firms — China’s state-controlled Global Times reported that “If Trump continues to escalate trade tensions with China, we cannot rule out the possibility that China will strike back by adopting a hard-line approach targeting Dow Jones index giants,”. “Beijing will further open up China’s financial markets to the world, a move that may draw funds from U.S. stock markets as global investors increasingly add Chinese stocks to their portfolios.”

4. Dow Jones Removes GE from Index — the Dow Jones Index dropped GE and replaced with Walgreens (NASDAQ:WBA). GE released a statement saying that “Today’s announcement does nothing to change those commitments or our focus in creating a stronger, simpler GE.” The industrial conglomerate has been the worst performing stock in the index – where it was an original member in 1896 and a member continuously since 1907 – falling 55% over the last 12 months, and more than 25% YTD.

5. OPEC Ministers Agree to Raise Oil Production by 1 Million Barrels a Day — OPEC members agreed to start pumping more oil, though the agreement will not end the group’s 18-month-old deal to limit output. Instead the producers are seeking to cut no deeper than 1.2 million bpd, the target they set in November 2016. Expecting a large oil deficit in the second half of this year – due to outages in Venezuela and Libya – as well as calls from top consumers to cool down prices, consensus among the group is to raise production by a combined 1M barrels per day.

The week ahead — Economic data from Econoday.com:

Tags: China Trade War, OPEC Raised Oil Production

Posted in Weekly Summary | No Comments »

June 18th, 2018

…“People somehow think you must buy at the bottom and sell at the top to be successful in the market. That’s nonsense! The idea is to buy when the probability is greatest that the market is going to advance”… Jesse Livermore

1. Trump Drops G7 Communique Endorsement — President Trump refused to endorse a G7 statement pledging to “fight protectionism and reduce tariff barriers,” saying trade among the G7 nations should be free of tariffs and other barriers. “Based on the fact that Canada is charging massive Tariffs to our U.S. farmers, workers and companies, I have instructed our U.S. Reps not to endorse the Communique as we look at Tariffs on automobiles flooding the U.S. Market!”.

2. Trump, Kim Sign ‘Comprehensive’ Document — the meeting between President Trump and Kim Jong-un signed a “comprehensive” and “historic” document that included the following four points: Establishing new US-DPRK relations, building a lasting and stable peace regime, reaffirming commitments to work toward complete denuclearization and recovering POW/MIA remains. U.S. sanctions will remain in effect for the time being and American forces will not be reduced on the Korean peninsula.

3. Lithium Revival Across the U.S. — In North Carolina, Nevada and half a dozen other states, miners are working to revive the U.S. lithium industry, once the world’s largest until it fell off in the 1990s. According to Reuters, Piedmont Lithium (NASDAQ:PLLL), Albemarle (NYSE:ALB) and Lithium Americas (NYSE:LAC) all see opportunity amid a surging EV market and increased battery demand. The U.S. produced only about 2% of the world’s lithium last year, but has around 13% of the world’s identified resources.

4. AT&T prevails in Time Warner merger trial — U.S. District Court Judge Richard Leon has approved AT&T’s (NYSE:T) $85.4B purchase of Time Warner (NYSE:TWX) without conditions, giving the pay-TV provider ownership of cable channels HBO and CNN, as well as film studio Warner Bros. The outcome could spur a wave of deals in the telecom and media industries, as well as clear the way for future vertical mergers.

5. Fed Raises Interest Rates and Signals 2 More Increases Are Coming — the Federal Reserve raised interest rates last Wednesday and signaled that two additional increases were on the way this year. Jerome H. Powell, the Fed chairman, said the economy had strengthened significantly since the 2008 financial crisis and was approaching a “normal” level that could allow the Fed to soon step back and play less of a hands-on role in encouraging economic activity. The Fed’s optimism about the state of the economy is likely to translate into higher borrowing costs for cars, home mortgages and credit cards over the next year as the central bank raises interest rates more quickly than was anticipated

6. Latest AAII Weekly Sentiment — based on the latest Weekly Sentiment, the Bulls are on the offensive this week as AAII Bullish sentiment jumped to 44.78% from 38.93% last week, which is the highest level since mid-February.

While bullish sentiment spiked higher, bearish sentiment did not see as big of a move to the downside. As shown in the chart below, negative sentiment declined from 26.72% down to 21.70%.

7. New High Cumulative A/D Line Versus S&P500 — below displays the chart of the S&P500 ‘s underlying breadth which points to an eventual new high in price for the S&P 500.

The week ahead — Economic data from Econoday.com:

Tags: A/D High, AAII Weekly Sentiment

Posted in Weekly Summary | No Comments »