September 18th, 2018

“A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when others are fearful,” Warren Buffett

1. Trump Says Apple Should Shift Production to U.S. to Avoid China Tariffs — President Trump tweeted that Apple (NASDAQ:AAPL) should make more of its products in the U.S. if it wants to avoid tariffs on Chinese imports. In the filing, Apple said the new proposed tariffs would affect prices for a “wide range” of products, including the Watch, AirPods headphones and Beats headphones. China has warned it will match any U.S. tariffs.

2. Trump Readies New Tariffs on Chinese Imports — the Trump administration reportedly set to announce a new round of tariffs on as much as $200B in Chinese goods, while Beijing considers scrapping upcoming trade talks in response. The duties will be set at 10%, below the 25% level announced in early August, to diminish the impact on U.S. consumers ahead of the holiday shopping season and before midterm elections. Global shares are edging down on the news, while the Shanghai Composite closed at its lowest level since 2014. former finance minister Lou Jiwei told a forum, besides retaliating with tariffs, China could also restrict export of goods, raw materials and components core to U.S. manufacturing supply chains.

3. EPA Set to Ease Rules On Methane Leaks for Oil and Gas Companies — the Environmental Protection Agency will reportedly announce a rollback of Obama-era methane emission rules. The EPA proposal wants to give oil and gas companies more time to assess and safely repair infrastructure that’s often found in remote areas. The changes would give drillers a year to perform leak inspections and 60 days to make repairs, double the current time frames.

4. Apple’s iPhone Launch — AAPL unveiled its biggest and most expensive iPhone at its fall launch event, with most of the buzz swirling around a rumored phablet (iPhone Xs Max?) that’s supposed to boast a 6.5-inch OLED screen. Two other models will likely be called the iPhone Xs (5.8-inch OLED) and Xr (6.1-inch LCD). the iPhone XR starting at $749, iPhone Xs starting at $999 and iPhone Xs Max starting at $1,099. More products anticipated include the Watch Series 4, third-gen iPad Pro, budget MacBook, and updated AirPods with a long-delayed charging mat.

5. More Strikes Entertainment Deals — Twitter has struck a host of new media partnerships, bringing “hundreds of hours” of entertainment to audiences in the Asia Pacific region. The deal includes game highlights from the UEFA Champions League, live-streaming from Formula One and live Red Carpet events. Twitter (TWTR) has seen double-digit audience growth in Asia Pacific and is “projecting by about 2020, we’ll be at about a billion views here in (Asia Pacific) alone.”

6. Gas explosions near Boston — NiSource’s (NYSE:NI) Columbia Gas explosions killed at least one person, injured 12 more and forced thousands to evacuate from three communities north of Boston. Some 70 fires, explosions or investigations of gas odor were reported, according to Massachusetts State Police. NiSource’s (NYSE:NI) Columbia Gas unit had said earlier that it would be upgrading gas lines in neighborhoods across the state.

The week ahead — Economic data from Econoday.com:

Tags: US/China Trade War

Posted in Weekly Summary | No Comments »

September 10th, 2018

“The secret to being successful from a trading perspective is to have an indefatigable and an undying and unquenchable thirst for information and knowledge.” — Paul Tudor Jones

1. EU Open to More U.S. Beef Imports — the EU is willing to start talks with Washington on increasing U.S. beef imports, a move aimed at cementing a trade truce agreed upon in July. The bloc already upped its U.S. soybean imports, which rose 283% Y/Y in July, bringing the EU’s total American soybean share to 37%, up from 9% a year ago. Both agricultural products have been hit by retaliatory tariffs from China and Mexico, with U.S. beef producers forced to stockpile meat in cold storage facilities.

2. China Warns of Retaliation Over New U.S. Tariffs — according to the country’s commerce ministry “If the U.S., regardless of opposition, adopts any new tariff measures, China will be forced to roll out necessary retaliatory measures,” . Due to China’s massive trade surplus over the U.S., many expect the nation could further devalue its currency or crack down on U.S. firms inside the country. The Trump administration is reportedly ready to move ahead with a next round of tariffs .

3. Emerging-Market Stocks Hover Near Bear Territory — Emerging markets were teetering on the verge of bear territory last week as a rising dollar and higher U.S. interest rates are siphoning money from the developing world and making their debts more expensive. The gauge of 24 emerging-market countries has now dropped by a fifth since its January high after steep falls in the Turkish and Argentine currencies sparked a wider selloff. The Shanghai Composite Index has fallen 24% from its peak in January, while the yuan is down around 6% since June. The recent bout of selling was partly triggered last month by sharp declines in the Turkish lira, which is down by more than 40% this year, and later the Argentine peso, which has fallen 51%. Elsewhere, the Indian rupee reached its weakest-ever levels this week, and the Indonesian rupiah is trading around two-decade lows.

4. Goldman Sachs Is Said to Cool to Crypto-Trading as Bitcoin Runs Cold — Crypto prices continue to tumble following a Business Insider report that stated Goldman Sachs was dropping plans to open a trading desk for cryptocurrencies. Bitcoin (BTC-USD) is down about 12% over the last 24 hours to a low of $6,279. The alts posted far worse during that time, with the price of Ethereum (ETH-USD) tumbling by 20%, Ripple (XRP-USD) dropping by 14% and Bitcoin Cash (BCH-USD) falling 19%.

5. Ebola Outbreak Spreading in Congo — Congo has confirmed its first Ebola death in the eastern city of Butembo, the first urban outbreak of the virus. The current wave has already killed 89 people and it’s close to becoming the eighth largest Ebola outbreak in history. A vaccination campaign has already been underway for weeks, with experimental treatments from companies like Merck (NYSE:MRK) and Gilead Sciences (NASDAQ:GILD).

The week ahead — Economic data from Econoday.com:

Tags: China/US Trade War

Posted in Weekly Summary | No Comments »

September 4th, 2018

“The core problem, however, is the need to fit markets into a style of trading rather than finding ways to trade that fit with market behavior.” – Brett Steenbarger

1. U.S., Canada Set for High-Stakes Trade Talks Under Cloud of White House Threat — Canadian Foreign Minister Chrystia Freeland traveled to Washington to continue trade negotiations. “We’ll give them a chance to have a separate deal, or we could put it into this,” President Trump declared, adding that the “simplest deal is more or less already made. White House Economic Adviser Larry Kudlow told CNBC “We may have to resort to auto tariffs if the U.S. and Canada can’t reach a fair deal,”.

2. Apple to Take iPhone X Design to New Phones — Apple plans to unveil three new phones using the edge-to-edge screen design of the iPhone X, sources told Bloomberg. The new “S year” devices, expected to be unveiled at Apple’s product event in September, will include updated features and cover a broader range of prices, colors and sizes. One will even include a 6.5-inch display, the largest Apple (NASDAQ:AAPL) has ever included on an iPhone.

3. U.S. to Pay Farmers $4.7 Billion to Offset Trade-Conflict Losses — the Trump administration pledged to pay farmers $4.7 billion to offset losses from trade disputes with foreign buyers of U.S. agricultural products. The payments would help protect farmers from “unjustified tariffs” some nations have applied in response to President Trump’s trade policies. China, Mexico, the European Union and other trade partners have levied tariffs on U.S. farm goods from soybeans to pork to apples, leaving growers vulnerable during a downturn in the agricultural economy. Soybean farmers are in line to get roughly three-fourths of the direct payments, or $3.6 billion, followed by producers of pork, cotton, sorghum, dairy and wheat.

4. India Set for Record Oil Demand Growth — India is set to overtake China as the biggest source of growth for oil demand by 2024, according to a forecast by Wood Mackenzie. The country’s expanding middle class will be a key factor, as well as its growing need for mobility. On the other hand, China – which overtook the U.S. as the biggest importer of crude oil in 2017 – is set to see a decline due to two trends: Alternative energy sources and a more efficient freight system.

5. Fresh Stress for Emerging Market Currencies — Argentina’s peso tanked 7.5% against the dollar late last week, bringing losses to nearly 50% over the past year, after President Macri asked the IMF to speed up delivery of a $50B bailout package. In response to the suffering peso, other fragile emerging market currencies sold off sharply overnight, with Turkey’s lira and the South African rand feeling heat, and India’s rupee slumping to a new record low. The tumult highlights a heavy international dependence on the dollar. Some 48% of the world’s $30T in cross-border loans are priced in the U.S. currency, up from 40% a decade ago.

6. Moody’s Lowers Rating on Ford — Moody’s has lowered Ford’s (NYSE:F) credit rating to one notch above junk bond status, and warned of further downgrades if it doesn’t make “clear progress” on its $11B turnaround plan. The second-largest U.S. auto manufacturer is faces weakening profit margins in North America, a retrenching business in China, and losses in South America and Europe.

The week ahead — Economic data from Econoday.com:

Tags: US/Canada Trade Talk

Posted in Weekly Summary | No Comments »

August 27th, 2018

“Amateurs think about how much money they can make. Professionals think about how much money they could lose.” – Jack Schwager

1. U.S. Proposed Sale from Strategic Oil Reserve to Reduce Global Oil Supplies — the U.S. Department of Energy is offering 11M barrels of crude for sale from the nation’s Strategic Petroleum Reserve ahead of sanctions on Iran that are expected to reduce global oil supplies and increase prices. The SPR was established in the 1970s after the U.S. economy was paralyzed by an oil embargo. As recently as 2011 it contained 727M barrels in caverns along the Texas and Louisiana coasts.

2. JPMorgan to Unveil New Investing App — JPMorgan (NYSE:JPM) is rolling out a digital investing service next week that comes bundled with free or discounted trades, a sophisticated portfolio-building tool and no-fee access to the bank’s stock research. “You Invest,” more than two years in the making, has a distinct advantage over many competitors: JPMorgan already has financial ties with half of American households.

3. Hospitals Shut At a Rate of 30 Annually — U.S. hospitals have been closing at a rate of about 30 a year, according to the American Hospital Association, and patients living far from major cities may be left with even fewer hospital choices as insurers push them toward online providers like Teladoc (NYSE:TDOC) and clinics such as CVS’s MinuteClinic (NYSE:CVS). The next year to 18 months could see a further increase in shutdowns, with the risks coming following years of mergers and acquisitions.

4. China Retaliates Against New U.S. Tariffs — a fresh round of U.S. tariffs on $16B worth of Chinese imports kicked in at last week, prompting Beijing to retaliate with its own levies on American goods worth the same amount. The world’s two largest economies, which are in the midst of trade talks, have now slapped tit-for-tat duties on a combined $100B of products since early July, with more in the pipeline. Economists reckon that every $100B of imports hit by tariffs would reduce global trade by around 0.5%.

5. SEC Dismisses More Bitcoin ETFs — the SEC has once again thwarted an attempt to build a bitcoin ETF, rejecting applications for nine separate bitcoin-based exchange-traded funds. Cboe Global Markets (NASDAQ:CBOE) and NYSE Arca (NYSE:ICE) would have listed the products. The commission leaned on the same reasoning as for the earlier rejections, mainly that there aren’t enough protections against fraud and market manipulations.

6. U.S.-China Trade Talks End with No Major Progress — Mid-level trade talks between the U.S. and China ended without any formal signs of progress, although Chinese officials said they plan to keep the lines of communication open. Sources indicated the two sides mainly swapped talking points without getting any detailed negotiations. Representatives from the U.S., European Union, and Japan plan to meet in Washington to extend talks on how to leverage the World Trade Organization and other ways pressure can be exerted on China.

The week ahead — Economic data from Econoday.com:

Tags: Bitcoin, US/China Trade Talk

Posted in Weekly Summary | No Comments »

August 21st, 2018

“The game of speculation is the most uniformly fascinating game in the world. But it is not a game for the stupid, the mentally lazy, the person of inferior emotional balance, or the get-rich-quick adventurer. They will die poor.” – Jesse Livermore

1. Turkey Retaliated With Tariffs on U.S. Cars, Alcohol, Tobacco — a reeling Turkey has responded to U.S. tariffs with retaliatory duties on U.S. passenger cars, alcohol, tobacco, cosmetics and other products. Tariffs on cars are set to rise by 120% and those on made-in-the-U.S. alcoholic drinks by 140%, alongside a 60% increase on tobacco products. The move comes amid increasing fears of contagion from Turkey’s collapse.

2. China, U.S. to Resume Trade Talks This Month — China will send a delegation to the United States later in August to resume trade talks that largely broke down a couple of months ago. Vice Commerce Minister Wang Shouwen will discuss economic and trade issues with U.S. counterpart David Malpass in a new attempt at defusing a trade war that has resulted in billions of dollars in tariffs so far, with threats of more. Formal talks between the U.S. and China broke down last month and led to dueling tariffs.

3. Amazon Eyes Online U.K. Healthcare Market — Major insurance firms in Europe have been invited by Amazon (NASDAQ:AMZN) to participate in a U.K. price comparison website. While there are no firm details on a launch by Amazon into financial services in the region, online insurance comparison players such as AXA (OTCQX:AXAHF), Hastings (OTC:HNGGF), Esure (OTC:ESXRY) and GoCompare are on watch.

4. Federal Probe Focuses On Apartment Mortgage Fraud — WSJ reported the investigation, still in its early stages, has so far resulted in a fraud-conspiracy indictment against four real-estate executives in upstate New York for falsifying information that helped them secure loans multi-family properties. The indictments made fraud-conspiracy charges against Todd Morgan and Kevin Morgan, a son and nephew of Robert Morgan, and charged their mortgage brokers, Frank Giacobbe and Patrick Ogiony of Aurora Capital Advisors. One owner of properties investigators reviewed is Robert C. Morgan, who ran a firm called Morgan Management LLC, but changed its name in June to Grand Atlas Property Management.

5. Q2 Latest Hedge Fund 13F — Hedge funds have finished up reporting on the investments they held at the end of Q2. New portfolio additions such as Keurig Dr Pepper (NYSE:KDP) by Citadel, Groupon (NASDAQ:GRPN) by Engaged Capital and GrubHub (NYSE:GRUB) by Jana Partners. Perhaps not a surprise, Alibaba (NYSE:BABA) was one of the names that cropped up the most times in the portfolio updates. Facebook (NASDAQ:FB) was added by at least six funds in Q2 as a new addition, while ten funds dropped the tech stock or trimmed exposure. In addition, Berkshire boosts stakes in Apple, US Bank, Teva, BNY Mellon, Delta in Q2 — in the latest 13F from Berkshire Hathaway (BRK.A, BRK.B) showed its stake in Apple (AAPL) as boosted to about 252M shares as of June 30 – up roughly 5% from three months earlier. The Oracle and company also added to holdings in U.S. Bancorp (NYSE:USB), Teva Pharmaceuticals (NYSE:TEVA), Bank of New York Mellon (NYSE:BK), General Motors (NYSE:GM), and Goldman Sachs (NYSE:GS). Among those showing trimmed stakes were American Airlines (NASDAQ:AAL), Phillips 66 (NYSE:PSX), Charter Communications (NASDAQ:CHTR), and Wells Fargo (NYSE:WFC).

6. U.S. Seen Near Deal with Mexico On Revised NAFTA But Canada Remains Apart — the U.S. is close to reaching a deal with Mexico on a revamped North American Free Trade Agreement, but thorny issues are yet to be resolved with Canada, according to reports. Both Mexico and the U.S. are seen as having strong incentives to push through a deal quickly: Mexico wants to lock in an agreement before its new leftist president takes office, and the Trump administration wants a win on trade ahead of the midterm elections. U.S. negotiators this week have been meeting with senior Mexican officials in Washington, and the two sides are said to have largely agreed to new rules on auto trade – a top White House priority – that could boost investment in the U.S. President Trump says he is “in no hurry” to complete a NAFTA deal, remarks seen mostly as an attempt to put pressure on Canada.

The week ahead — Economic data from Econoday.com:

Tags: 2Q 13F, NAFTA Deal, Turkey Row

Posted in Weekly Summary | No Comments »

August 13th, 2018

“The markets are always changing, and the successful trader needs to adapt to these changes” — Michael Steinhardt

1. U.S. Reimposes Sanctions on Iran — the first batch of American sanctions on Iran has come into effect, 90 days after the U.S. withdrew from the nuclear deal. The new measures bar the sale of U.S. currency to Iran’s government, sanction trade in precious metals and industrial materials, outlaw the purchase of Iran’s sovereign debt, and restrict the country’s auto and aerospace sector. Unless Iran complies with the U.S. demands, far-tougher steps will take effect on Nov. 5, when the U.S. will cut off Iran’s oil exports and impose sanctions on shipping.

2. China Outspent the U.S. in 5G — since 2015, China has outspent the U.S. by $24B in 5G infrastructure, potentially creating a “tsunami” that will be difficult to catch up with, according to a new study by Deloitte. China has built 350,000 new cell sites, while the U.S. has built fewer than 30,000 in the same time frame. 5G would support connected infrastructure in cities, including driverless cars, and make it possible for people to stream high-bandwidth video.

3. SEC Delayed Decision & Bitcoin Crashes Under $6,500 — the crypto reaching as high as $8,496 in July, but its latest descent has seen the digital currency fall overnight to under $6,500. The move was accelerated after the SEC pushed back an eagerly-awaited decision on the SolidX Bitcoin ETF (XBTC), sponsored by SolidX Management with marketing assistance from Van Eck Securities. A verdict is now expected by the end of September.

4. U.S.-Japan Enters New Trade Talks — Japan and the U.S. are headed for a new round of trade talks today in Washington. Economic Revitalization Minister Toshimitsu Motegi will try to avert steep tariffs on car exports and stress the significance of multilateral free trade, with an eye on persuading the U.S. to return to the TPP. The world’s third-largest economy will also face demands from U.S. Trade Representative Robert Lighthizer, including a trade deficit reduction and the further opening of Japan’s automobile and agriculture markets.

5. Turkish Crisis Rattles Global Markets Amid Escalating Spat With U.S. — the lira dropped as much as 25% against the dollar, extending a tumble that ranks as one of the steepest in world markets this year. Turkey’s problems are spilling over into the greater market following reports that the ECB is concerned over the impact of a weak lira on European banks, especially BBVA, UniCredit (OTCPK:UNCFF), and BNP Paribas (OTCQX:BNPQF). Data from the BIS also showed the currency, which plunged 13.5% overnight to an all-time low against the dollar, will weigh on banking exposure internationally.

The week ahead — Economic data from Econoday.com:

Tags: Turkish Lira Crashes

Posted in Weekly Summary | No Comments »

August 6th, 2018

“Focus, patience, wise discernment, non-attachment —the skills you acquire in meditation and the skills you need to thrive in trading are one and the same.” — unknown

1. Iran’s Rial Hits Record Low — Iran’s currency hit a historic low of 100,000 rials to the dollar over the weekend. The collapse, which has seen the currency lose half its value in just four months, was encouraged by a deepening economic crisis and the imminent return of full U.S. sanctions. The penalties will be reimposed in two stages on Aug. 6 and Nov. 4, forcing many foreign firms to sever business ties with Tehran.

2. Japan, U.S., Australia Plan Infrastructure Push in Asia — forming a trilateral partnership, Australia and Japan have joined the U.S. in a push to invest in infrastructure projects in the Indo-Pacific region as China spends billions of dollars on its Belt and Road initiative across Asia. The investments will include energy, transportation, tourism and technology infrastructure, with the governments aiming to attract private capital to projects.

3. U.S.-China Trade War Back in Focus — the two countries are seeking to resume talks to defuse a tariff battle, according to Bloomberg, although later reports suggested the Trump administration plans to propose tariffs of 25% on $200B of imported Chinese goods after initially setting them at 10%. The Caixin-Markit PMI overnight also showed China’s manufacturing sector growing at its slowest pace in eight months in July, dragged down by declining export orders.

4. Molson Coors Canada and Hydropothecary Announces a Joint Venture — the Canadian unit of Molson Coors (NYSE:TAP) has entered a deal that will allow it to develop cannabis-infused beverages in the Great White North. It’s teaming up with Canadian cannabis producer Hydropothecary (OTCPK:HYYDF) to “participate in this exciting and rapidly expanding consumer segment.” Marijuana use in Canada will become legal later this year.

5. China Dethroned By Japan As World’s No. 2 Stock Market — an intensifying trade spat with the U.S. just led China to cede its four-year title as the world’s second-largest stock market to Japan. After a last week slump, Chinese equities were valued at US$6.09T, losing out to Japan’s $6.17T, while the U.S. remains the world’s largest with a market cap of $31T. The Shanghai Composite Index has lost more than 16% YTD to be among the world’s worst performers, while the yuan has fallen 5.3% against the dollar.

6. Apple Market Cap Over $1T — Apple hit a market cap of $1T last week, becoming the first publicly traded U.S. company to reach the milestone. Many credit the company’s growing software and services sales with driving the valuation. The catch-all category – which includes the App Store (NASDAQ:AAPL), AppleCare, Apple Pay, iTunes and cloud services – posted record revenue of $9.55B for the June quarter.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

July 30th, 2018

“Sometimes the best trade is no trade.” – Anonymous

1. G20 Finance Ministers Release Communique — world financial leaders called for stepped-up dialogue at a G20 meeting last Saturday, but ended the gathering with little consensus on how to resolve multiple disputes over U.S. tariff actions. The communique noted while growth is strong, it’s becoming less synchronized amid downside risks, including financial vulnerabilities, and heightened trade and geopolitical tensions. Ahead of the summit, Treasury Secretary Steven Mnuchin said he “wouldn’t minimize” the possibility that the U.S. will impose tariffs on all $500B worth of goods that the U.S. imports from China. He also discussed trade tensions with the EU. “If Europe believes in free trade, we’re ready to sign a free-trade agreement,” adding that any deal would have to eliminate tariffs, along with other barriers and subsidies.

2. U.S. Economy Grew at 4.1% Rate in Second Quarter — gross domestic product (GDP) — the value of all goods and services produced across the economy—rose at a seasonally and inflation-adjusted annual rate of 4.1% from April through June, the Commerce Department reported last Friday. The Commerce Department said U.S. soybean exports surged in the second quarter, delivering an outsize boon to economic growth even as China shifted much of its sourcing to Brazil in response to its worsening trade relations with the U.S. The export rally likely reflected efforts by buyers to get their soybeans before China’s 25% retaliatory tariffs on U.S. soybeans, which hit in July.

3. Venezuela To Lop Five Zeros Off Currency — Venezuela is delaying its planned currency re-denomination by two weeks to Aug. 20, lopping five zeroes off the refurbished bolivar (instead of three) and linking it to the country’s Petro cryptocurrency. It comes in response to Venezuela’s hyperinflation, which the IMF has said will soar to 1,000,000% this year, throwing the OPEC nation’s already battered economy into a deeper tailspin.

4. Trump Reportedly Wins EU Trade Concessions — President Trump announced at a press conference late last week with the EU’s Jean-Claude Juncker “We agreed today to work together towards zero tariffs, zero non-tariff barriers and zero subsidies for the non-auto industrial goods,”. The U.S. secured further trade concessions, including the import of more soybeans and possibly some liquefied natural gas, while potential auto tariffs will be sidelined as the two sides launch negotiations to cut other trade barriers.

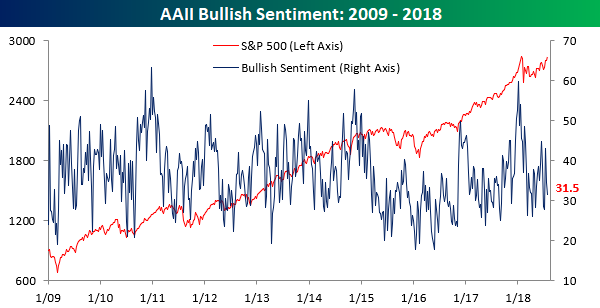

5. AAII Weekly Sentiment — courtesy of BIG, according to this week’s report, bullish sentiment declined for the second week in a row, falling from 34.66% down to 31.52%.

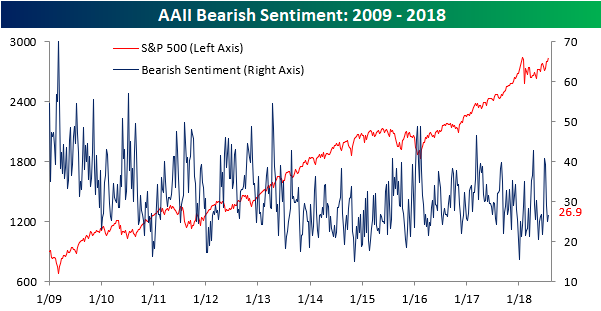

As bullish sentiment declined, bearish sentiment ticked up from just under 25% to just under 27%.

The week ahead — Economic data from Econoday.com:

Tags: AAII Weekly Sentiment, US EU Trade War

Posted in Weekly Summary | No Comments »

July 23rd, 2018

“Where you want to be is always in control, never wishing, always trading, and always first and foremost protecting your butt.” – Paul Tudor Jones

1. Farnborough Airshow — the most important aviation trade show of the year has begun, attracting about 100,000 trade visitors from 100 countries. Alternating every year with the Paris Air Show in France, the Farnborough International Air Show runs until July 22. Boeing (NYSE:BA) kickstarted the exhibition with a $4.7B deal for freight planes with delivery company DHL and the firm purchase of 30 737 MAX 8s with leasing firm Jackson Square. Airbus (OTCPK:EADSY) is already plotting its revenge. It’s working on a blockbuster agreement to sell $23B worth of aircraft to AirAsia, as well as confirming a $9B order from StarLux and Sichuan Airlines.

2. Oil Dips Below $70 on Saudi Offer, SPR Release — Saudi Arabia is said to have offered extra crude to some customers, extending additional cargoes of its Arab Extra Light crude to at least two buyers in Asia, Bloomberg reported. The Trump administration is also actively considering tapping into the U.S.’s 660M-barrel Strategic Petroleum Reserve as political pressure grows to rein in rising gas prices before November elections.

3. U.S. Files Trading Complaints at WTO — the U.S. has filed separate claims with the World Trade Organization against China, the EU, Canada, Mexico and Turkey after the countries lodged complaints over the Trump administration’s steel and aluminum tariffs. President Trump has repeatedly raised the prospects of withdrawing from the WTO, although this month he said that no withdrawal was planned for now. Amid the trade tensions, Chinese mainland stocks are down almost 30% since their peak in January.

4. Japan, EU Sign Trade Agreement — Japan and the EU have signed the world’s largest bilateral trade pact covering about a third of global GDP. The deal, which involved significant concessions on both sides, will eventually reduce heavy Japanese tariffs on European wine, cheese and other foods and lift EU tariffs on Japanese cars and vehicle parts.

5. EU Mulls U.S. Tariffs on Coal, Pharma, Chemicals — the EU will consider introducing tariffs on coal, pharmaceuticals and chemical products from the U.S. if President Trump imposes restrictions on European cars, Germany’s Wirtschaftswoche magazine reported. The potential trade measures will be decided based on the outcome of a meeting next week in Washington between European Commission President Jean-Claude Juncker and President Trump. However, Commerce Secretary Wilbur Ross said it’s “too early” to say whether the Trump administration will move ahead with proposed tariffs of as much as 25% on imported vehicles and auto parts .

The week ahead — Economic data from Econoday.com:

Tags: US EU Trade War

Posted in Weekly Summary | No Comments »

July 16th, 2018

“Accepting losses is the most important single investment device to insure safety of capital.” – Gerald M. Loeb

1. Payments Halted Under Obamacare Program — the Trump administration is suspending a program that pays insurers to stabilize health insurance markets under Obamacare, saying that a recent federal court ruling prevents the money from being disbursed. Based on their 2017 business, the payments amount to $10.4B. With 20M Americans receiving health insurance through the Affordable Care Act, the latest freeze could increase uncertainty and drive up premiums this fall.

2. Brett Kavanaugh Nominated to Supreme Court — Brett Kavanaugh has been nominated for the U.S. Supreme Court, although a tough confirmation fight lies ahead in the Senate. As an ideological conservative he’s expected to push the court to the right on a number of issues, including business regulation. Kavanaugh has been critical of the expanding powers of federal agencies, including on measures like labor rights, credit-card fees and “payday” loans, and has also cast doubt on the constitutionality of the Consumer Financial Protection Bureau. Kavanaugh is widely viewed as being more conservative than Justice Anthony Kennedy, whom Kavanaugh has been nominated to replace.

3. China Ups Tariffs on U.S. Fiber Products — China’s commerce ministry will raise “anti-dumping tariff rates” tomorrow on some optical fiber products originating from the U.S., increasing the levy range to between 33.3% to 78.2%, compared with 4.7% to 18.6% as set in 2011. U.S. companies, including Corning (NYSE:GLW), OFS Fitel (OTCPK:FUWAY) and Draka Communications Americas, are among the firms affected by the change. the Trump administration raised the stakes in its trade war with China, saying it would slap 10% tariffs on an extra $200B worth of Chinese imports. The new list appears to target Beijing’s important manufacturing export industries, going after electronics, textiles, metal components and auto parts.

4. China’s Trade Surplus with U.S. Hits Record — China’s trade surplus with the U.S. swelled to a record in June, a result that could further inflame trade tensions with Washington. Exports to the world’s largest economy rose 5.7%, while imports from the U.S. rose 4%, resulting in a trade surplus of $28.97B. Separately, an explosion at a chemical plant in China overnight killed 19 people and injured 12, marking the latest deadly industrial incident in the country.

5. Index Correlation of 2018 VS Prior Years — courtesy of BIG, in comparing the S&P 500’s performance in 2018 to prior years, correlation of the closing prices – through July 11, of the S&P 500 to every year since 1928. Statistically, just two years correlated strongly with 2018: 1942 and 1980, when the rest of the year was up 11% and 15%, respectively.

The week ahead — Economic data from Econoday.com:

Tags: US-China TradeWars

Posted in Weekly Summary | No Comments »