June 3rd, 2022

1. Fed Sees Half-Point Rate Hikes at the ‘Next Couple of Meetings. — minutes from the Fed’s May 3-4 meeting, at which the central bank raised interest rates by a half point to a range of 0.75%-1% and unveiled plans to begin reducing the size of its balance sheet, echoed an urgency to tackle inflation that Fed Chairman Jerome Powell said was a priority in his postmeeting press conference. But they also show that the Fed hopes to become more “data dependent” at future meetings amid an uncertain economic outlook. The Fed’s policy-making arm, the Federal Open Market Committee, meets next on June 14-15 and then July 26-27.

2. ECB Signals Delayed Bond Runoff, Diverging From Fed — the European Central Bank is likely to hold on to its mammoth portfolio of sovereign debt as it starts to raise interest rates, ECB officials said, underlining the fine line it is walking as it tightens monetary policy to battle inflation while trying not to weaken the bloc’s most fragile economies. The Fed, the ECB and other major central banks sucked up trillions of dollars of government and private debt during the pandemic to support financial markets and the economy. Now, investors are focusing on whether and how central banks unload those assets, which will have big repercussions for asset prices and bond yields.

3. US Home Sellers Cutting Prices Hits Highest Level Since 2019 — nearly one in five sellers dropped prices during the four week period ended May 22, Redfin Corp. said in a report Thursday. Other measures of how hot the market is, including a house’s time on market and the percentage of homes selling above listing price, have also plateaued. Consumers are contending with some of the highest mortgage rates in years, despite the dip in those figures in the past two weeks. Higher rates, coupled with economic uncertainty, are raising questions about whether the US housing boom has met its limit with signs emerging that the once-intense pace of the market could be decelerating.

4. Inflation Eased Slightly in April — Consumer prices rose 6.3% in April from a year earlier, down from 6.6% in March, as measured by the Commerce Department’s personal-consumption expenditures price index, which it reported Friday. The March rise was the fastest since January 1982. April’s reading was the first time the measure eased since late 2020. The so-called core PCE index—which excludes volatile food and energy prices—increased 4.9% in April from a year ago, down from 5.2% in the year through March. On a monthly basis, core prices rose a seasonally adjusted 0.3%, the same as in February and March. That pace marked a moderate slowdown from the average monthly pace for the previous four months. Minutes from the Fed’s May 3-4 meeting, released Wednesday, show that officials discussed the possibility that they would raise interest rates to levels high enough to slow economic growth deliberately as the central bank races to combat high inflation.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 24th, 2022

“Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” — Warren Buffett

1. Pfizer’s Covid-19 Booster Cleared for 5- to 11-Year-Olds — the Food and Drug Administration reported that children between the ages of 5 and 11 years old can get a booster dose of BioNTech SE and Pfizer Inc.’s PFE, 1.32% COVID-19 vaccine. Children in this age group should wait at least five months after getting the primary series of shots. The regulator authorized a booster of the BioNTech/Pfizer vaccine for teens back in January. The FDA’s advisory committee did not meet to discuss whether the benefits of a third dose of the BioNTech/Pfizer vaccine outweigh the risks for this age group because the companies’ request for authorization in 5 to 11 year olds “did not raise questions that would benefit from additional discussion by committee members,” according to the regulator.

2. U.S. Retail Sales Grew 0.9% in April — Retail sales—a measure of spending at stores, online and in restaurants—rose a seasonally adjusted 0.9% last month compared with March, the Commerce Department said Tuesday. That marked the fourth straight month of higher retail spending. Consumers spent more at restaurants and bars and boosted expenditures on vehicles, furniture, clothing, and electronics. They cut spending sharply on gasoline in April as pump prices pulled back briefly from a run-up related to the war in Ukraine. In another sign of economic momentum, the Federal Reserve said industrial production, a measure of factory, mining and utility output, increased a seasonally adjusted 1.1% in April—also a fourth month of gains.

3. Treasury Likely to Prevent U.S. Investors From Receiving Russian Debt Payments — the U.S. has carved out an exemption, set to expire on May 25, in its sanctions campaign against Russia to allow for sovereign debt payments. Without it in place, banks and investors won’t be able to process and receive bond payments made by the Kremlin, likely prompting Russia’s first default on its foreign debts since 1918. Russia has managed to stay current on over $2.5 billion in foreign debt payments since the onset of the war with Ukraine, largely thanks to the sanctions carve-out, although the U.S. has steadily tightened Russia’s ability to make payments, including new sanctions in April that cut off the Kremlin’s access to U.S. bank accounts for sovereign debt payments.

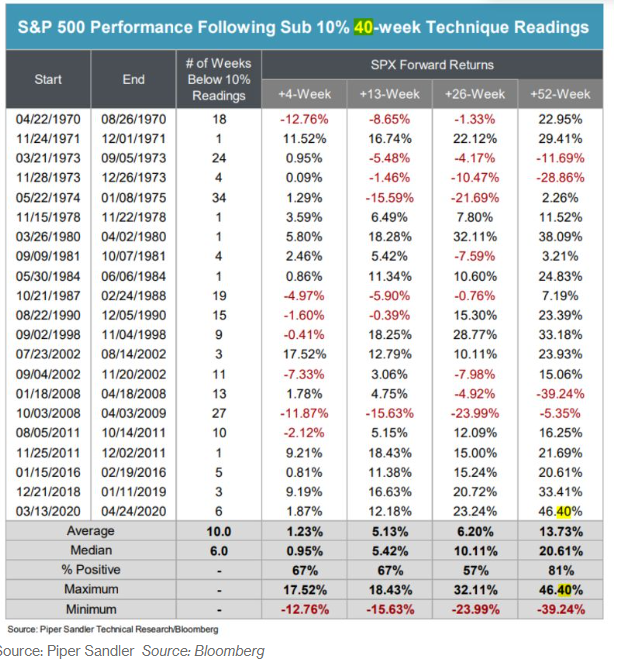

4. S&P 500 Pares Losses After Hitting Bear-Market Territory — the S&P 500 slid so far it was on track to close at least 20% below its January peak—what would have been considered a bear market. A comeback in the final hour of the trading day pushed the index higher. It has been decades since stocks have fallen for such a prolonged period. The Dow industrials notched their eighth straight weekly loss, their longest such streak since 1932, near the height of the Great Depression. The S&P 500 and Nasdaq had their seventh straight weekly loss, their longest such streak since 2001, after the dot-com bubble burst. All three indexes finished the week down at least 2.9%. Below is a chart of SPX performance following Sub 10% corrections.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 16th, 2022

“Only when the tide goes out do you discover who’s been swimming naked.” — Warren Buffett

1. Powell Reiterates Half-Point Hikes Are Likely in June and July — Federal Reserve Chair Jerome Powell reaffirmed that the central bank is likely to raise interest rates by a half percentage point at each of its next two meetings, while leaving open the possibility it could do more. Asked if he was taking a larger 75 basis-point increase off the table, he restated his comment from a May 4 press conference that the Fed wasn’t “actively considering” such a move, according to a transcript of the interview released by Marketplace.

2. US Producer Prices Rise More Than Forecast in Sign of Persistent Inflation — The producer price index for final demand increased 11% from April of last year and 0.5% from the prior month, driven by goods, Labor Department data showed Thursday. That followed sizable upward revisions to the March figures. Excluding the volatile food and energy components, the so-called core PPI increased 0.4% from a month earlier and was up 8.8% from a year ago. While that measure rose at a softer-than-expected monthly pace, March was revised up to a 1.2% advance. The data, while moderating somewhat from March, suggest persistent inflation in the production pipeline will continue to filter through to consumer prices, which also slowed from the prior month. Producers are likely to continue facing higher costs as Russia’s war in Ukraine and Covid-related lockdowns in China further strain supply chains, adding to the probability they’ll pass those expenses onto consumers.

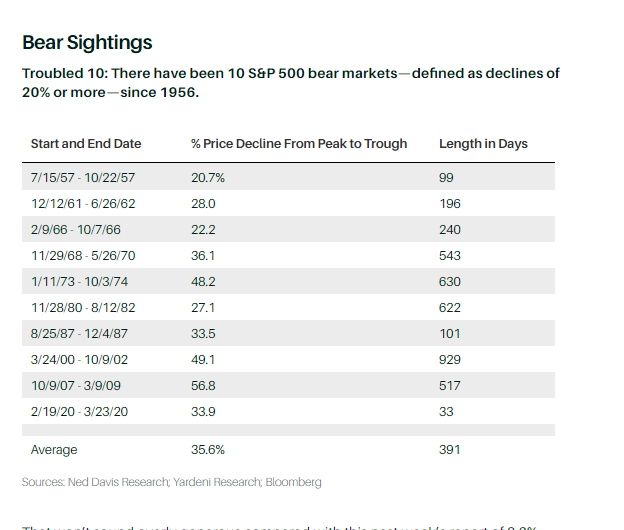

3. Bear Market Stats — according to Ned Davis Research, there have been 10 S&P 500 bear markets—defined as declines of 20% or more—since 1956, the average drop was 36.6% and last an average of 391 days. Below is the chart of the last 10-Bear Market going back to 1957.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 10th, 2022

“Seen through the lens of human perception, cycles are often viewed as less symmetrical than they are. Negative price fluctuations are called “volatility,” while positive price fluctuations are called “profit.” Collapsing markets are called “selling panics,” while surges receive more benign descriptions (but I think they may best be seen as “buying panics”; see tech stocks in 1999, for example). Commentators talk about “investor capitulation” at the bottom of market cycles, while I also see capitulation at the top, when previously prudent investors throw in the towel and buy.” ― Howard Marks

1. 10-Year Treasury Yield Hits 3% for First Time Since 2018 — the yield on the benchmark 10-year Treasury note, which rises when bond prices fall, surged at the start of U.S. trading and reached as high as 3.008% in the afternoon, as traders braced for the outcome of this week’s Federal Reserve meeting. Yields on Treasurys largely reflect investors’ expectations for short-term interest rates over the life of a bond. Rising yields are often associated with a strengthening economy because faster growth and a tighter labor market can lead central banks to crack down on inflation.

2. Fed Lifts Rates by Half Point in Biggest Hike Since 2000 — the Federal Reserve approved a rare half-percentage-point interest rate increase and announced plans to shrink its $9 trillion asset portfolio starting next month in a double-barreled effort to reduce inflation that is running at a four-decade high. The moves, announced after a two-day policy meeting Wednesday, will raise the central bank’s benchmark federal-funds rate to a target range between 0.75% and 1%.

Together, the steps mark the most aggressive Fed tightening of monetary policy at one meeting in decades, aimed at rapidly reducing the economic stimulus that has contributed to rising price pressures. The Fed, which usually lifts interest rates in quarter-percentage-point increments, last raised rates by a half point in 2000.

3. U.S. Mortgage Rates Jump to 5.37%, Highest Since 2009 — The average for a 30-year loan jumped to 5.27% from 5.10% last week, Freddie Mac said in a statement Thursday. The Federal Reserve yesterday raised its benchmark rate by a half point, the biggest bump since 2000, and signaled further hikes to come in its effort to cool inflation and the overheated housing market. Higher mortgage costs — already up more than 2 percentage points this year — may increasingly push out would-be homebuyers and ease competition for a scarce supply of listings. At the current 30-year average, a borrower with a $300,000 mortgage would pay $1,660 a month, $377 more than at the end of last year.

4. Bitcoin Slides Below $37,000 as Investors Unwind Risky Bets — apart from a brief selloff in January, bitcoin’s price hasn’t been this low since last July, when it traded as low as $29,000. The largest cryptocurrency is now down about 47% from its November record high of $68,991. On Wednesday, the central bank announced a half-point rate increase. Fed Chairman Jerome Powell said there may be half-point rate increases in the summer months, but that officials aren’t considering a three-fourths of a percentage point increase. The widespread unwinding of risk assets has hit the cryptocurrency market particularly hard, driving down everything from bitcoin to NFTs. It has also started to have an effect on companies in the industry. Crypto companies were surging early in the year, capped when several paid millions of dollars to run ads during the Super Bowl. But the momentum has faded sharply since then.

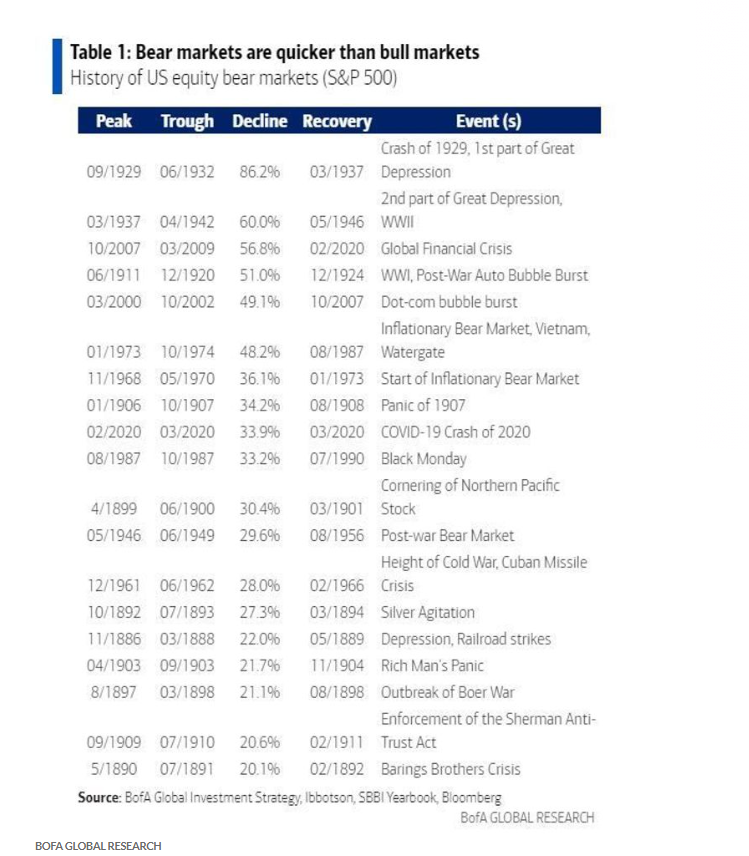

5. Past Bear Market Statistics — based on a BAC ‘s strategist Michael Harnett, Looking at a history of 19 bear markets over the past 140 years, they found the average price decline was 37.3% and the average duration about 289 days. While “past performance is no guide to future performance,” Hartnett and the team say the current bear market would end Oct. 19 of this year, with the S&P 500 at 3,000 and the Nasdaq Composite at 10,000. Check out their chart below:

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 2nd, 2022

“In investing, there is nothing that always works, since the environment is always changing, and investors’ efforts to respond to the environment cause it to change further ― Howard Marks

1. Russia to Cut Gas to Poland and Bulgaria, Making Energy a Weapon — Russia will cut off the gas to Poland and Bulgaria on Wednesday in a major escalation in the standoff between Moscow and Europe over energy supplies and the war in Ukraine. Moscow is making good on a threat to halt gas flows to countries that refuse President Vladimir Putin’s new demand to pay for the fuel in rubles. The European Union has rejected the move in principle but now payment deadlines are starting to fall due, governments across Europe need to decide whether to accept Putin’s terms or lose crucial supplies — and face the prospect of energy rationing.

2. Fidelity to Allow Retirement Savers to Put Bitcoin in 401(k) Accounts — employees won’t be able to start adding cryptocurrencies to their nest eggs right away, but later this year, the 23,000 companies that use Fidelity to administer their retirement plans will have the option to put bitcoin on the menu. The endorsement of the nation’s largest retirement-plan provider suggests crypto investing is moving further into the mainstream, but it remains to be seen whether employers will embrace it for their workers. Under the plan, Fidelity would let savers allocate as much as 20% of their nest eggs to bitcoin, though that threshold could be lowered by plan sponsors. Mr. Gray said it would be limited to bitcoin initially, but he expects other digital assets to be made available in the future.

3. U.S. GDP Drops 1.4% as Economy Shrinks for First Time Since Early in Pandemic — U.S. gross domestic product shrank at a 1.4% annual rate in the first quarter as supply disruptions weighed on the economy, though solid consumer and business spending suggest growth will resume. The decline in U.S. gross domestic product marked a sharp reversal from a 6.9% annual growth rate in the fourth quarter. The drop also marked the weakest quarter since spring 2020, when the Covid-19 pandemic and related shutdowns drove the U.S. economy into a deep—albeit short—recession. The drop in GDP stemmed from a widening trade deficit, with the U.S. importing far more than it exports. A slower pace of inventory investment by businesses in the first quarter—compared with a rapid buildup of inventories at the end of last year—also pushed growth lower. In addition, fading government stimulus spending related to the pandemic weighed on GDP.

4. Russia Makes Bond Payment In Dollars To Avoid Default — Russia said it had made payments on two dollar-denominated bonds, potentially staving off a default on the country’s foreign debt. The nearly $650 million in payments were made in dollars to a London branch of Citigroup Inc. that processes payments on behalf of bondholders, Russia’s finance ministry said Friday.

The money from Russia’s bond payments must land in bondholders’ accounts by Wednesday, the end of a 30-day grace period after Russia missed a payment in early April. Otherwise, the country can officially be called in default by its creditors.

5. Inflation Rises to Four-Decade High — Consumer prices rose 6.6% in March from a year before, up from February’s revised 6.3% increase, as measured by the Commerce Department’s personal-consumption expenditures price index. The March rise was the fastest since January 1982. The so-called core PCE index—which excludes volatile food and energy prices—increased 5.2% in March from a year earlier, down from a revised 5.3% in the year through February. On a monthly basis, core prices rose a seasonally adjusted 0.3% in March from the prior month, the same as the revised 0.3% increase in February. That was down from the 0.5% monthly pace in each of the prior four months—a mild slowdown that hinted broad price pressures might be starting to ease.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 25th, 2022

“Patient opportunism, buttressed by a contrarian attitude and a strong balance sheet, can yield amazing profits during meltdowns.”

― Howard Marks

1. U.S. Home Prices Hit a Record of $375,300 in March — U.S. home prices soared to a new record in March while mortgage rates continued to rise rapidly, slowing home sales in what has been the hottest housing market in more than 15 years. The rise of remote work and the pursuit of more space unleashed a powerful wave of home buying when Covid-19-related lockdowns started to ease in the middle of 2020. The frenzied housing market, supported by ultralow interest rates at the time, lifted home prices throughout the country. Homes for sale often stayed on the market for less than a month, and sometimes only days, while open houses could draw lines around the block.

Now, that frenzy is starting to ease and the volume of home sales is reverting to pre-pandemic levels, said Lawrence Yun, chief economist for the National Association of Realtors. With mortgage rates at 5% and back to their highest level since 2011, Mr. Yun said he expects home sales in 2022 to decline 10% from last year.

2. Florida Bill to End Disney’s Special Tax District Heads to Gov. DeSantis for Signature — Florida lawmakers gave final approval to a bill that would end a special tax district that allows Walt Disney Co. DIS 0.07% ▲ to govern the land housing its theme parks, sending the measure to Republican Gov. Ron DeSantis, who has made clear he would sign it. The move marks a significant setback for Disney’s Florida operations. The special district, created in 1967 and known as the Reedy Creek Improvement District, exempts Disney from numerous regulations and certain taxes and fees. It has permitted the company to manage its theme parks and resorts in the state with little red tape for more than 50 years.

3. Fed’s Jerome Powell Seals Expectations of Half-Point Rate Rise in May — Federal Reserve Chairman Jerome Powell signaled the central bank was likely to raise interest rates by a half percentage point at its meeting next month and indicated similar rate rises could be warranted after that. The Fed has indicated it is also set to begin shrinking its $9 trillion asset portfolio.

4. Mortgage Rates Continue to Rise — the average rate for a 30-year fixed-rate mortgage rose to 5.11%, mortgage-finance giant Freddie Mac said Thursday. The rate hit 5% last week for the first time since 2011, up from 3.22% at the beginning of 2022. The Federal Reserve’s pullback from the mortgage-bond market has helped drive up interest rates on home loans in recent months. So too has its posture on interest rates. The Fed is expected to raise its benchmark rate again at its meeting early next month, and it has signaled that more increases are likely this year. That has driven up yields on the 10-year Treasury note, to which mortgage rates are closely tied.

The combination of rising rates and record home prices has started to weigh on demand. Sales of existing homes dropped 4.5% in March from a year earlier, according to the National Association of Realtors. Purchase mortgage applications last week fell 3% from the prior week and 14% from a year earlier, according to the Mortgage Bankers Association.

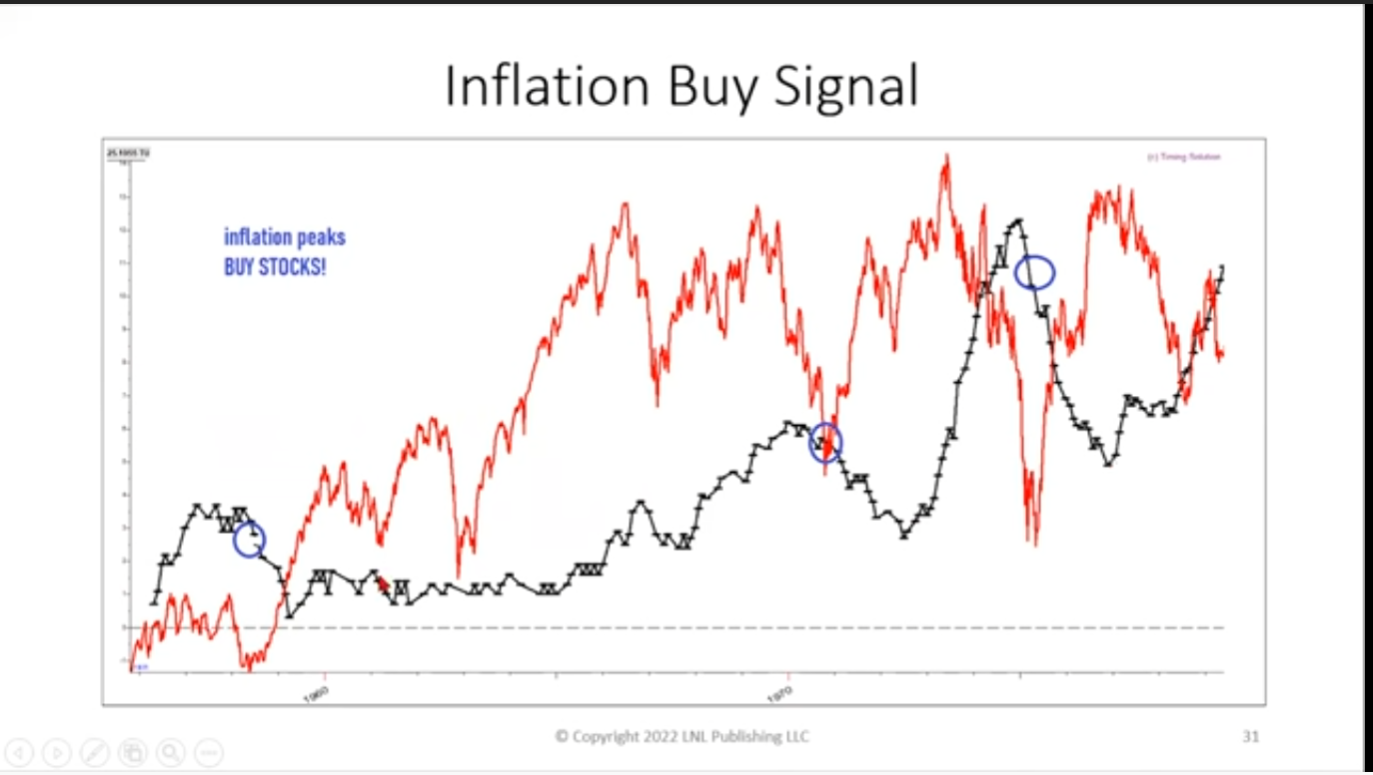

5. Past History of Inflation — based on past history, as inflation tops and starts to rollover, stock market will start to rally as inflation is discounted.

The week ahead — Economic data from Econoday.com:

Tags: Inflation

Posted in Weekly Summary | No Comments »

April 18th, 2022

“Patient opportunism, buttressed by a contrarian attitude and a strong balance sheet, can yield amazing profits during meltdowns.” ― Howard Marks,

1. U.S. Inflation Accelerated to 8.5% in March, Hitting Four-Decade High — U.S. inflation surged to a new four-decade high of 8.5% in March from the same month a year ago, driven by skyrocketing energy and food costs, supply constraints and strong consumer demand. The Labor Department reported the consumer-price index—which measures what consumers pay for goods and services—last month rose at its fastest annual pace since December 1981, up from the 7.9% annual rate in February. Rising prices have been unrelenting, with six straight months of inflation above 6% that is well above the Federal Reserve’s average 2% target.

2. Chinese Stockpile Food as Covid-19 Concerns Ripple Out From Shanghai — As Shanghai battles the country’s worst Covid-19 outbreak in two years, people across the rest of China are stockpiling necessities as they brace for the prospect of similar lockdowns. In Beijing, where some residential districts have been closed in recent weeks as infections have been discovered, supermarket shelves in some parts of the city have been picked clean of toilet paper, canned foods, instant noodles and rice in recent days.

In Suzhou, an industrial hub roughly two hours’ drive west of Shanghai, residents swarmed supermarkets to fill their grocery baskets with instant noodles and other food on Tuesday morning, hours after local officials said they would conduct districtwide testing in one section of the city.

3. Supplier Prices Rose Sharply in March — the Labor Department on Wednesday said the producer-price index, which generally reflects supply conditions in the economy, increased a seasonally adjusted 1.4% in March from the prior month, a pickup from an upwardly revised 0.9% gain in February. Producer prices rose 11.2% on a 12-month basis, compared with an upwardly revised 10.3% increase in February. That marked the fourth consecutive month with a double-digit gain and was the highest since records began in 2010.

4. Mortgage Rates Hit 5% for First Time Since 2011 — the interest rate on America’s most popular mortgage hit 5% for the first time in more than a decade, extending a sharp rise that has yet to significantly slow the red-hot housing market. Rates’ fastest three-month increase since 1987 has made the housing market ground zero for the Federal Reserve’s efforts to tame inflation. Home buyers, already facing surging house prices, are now contending with a substantial increase in financing expenses, further lifting monthly payments. A year ago, buying the median American home at prevailing rates meant a monthly mortgage bill of about $1,223 after a 20% down payment, according to calculations by George Ratiu, an economist at Realtor.com. At recent rates, such a purchase would require a monthly payment of nearly $1,700—a 38% increase, he estimated.

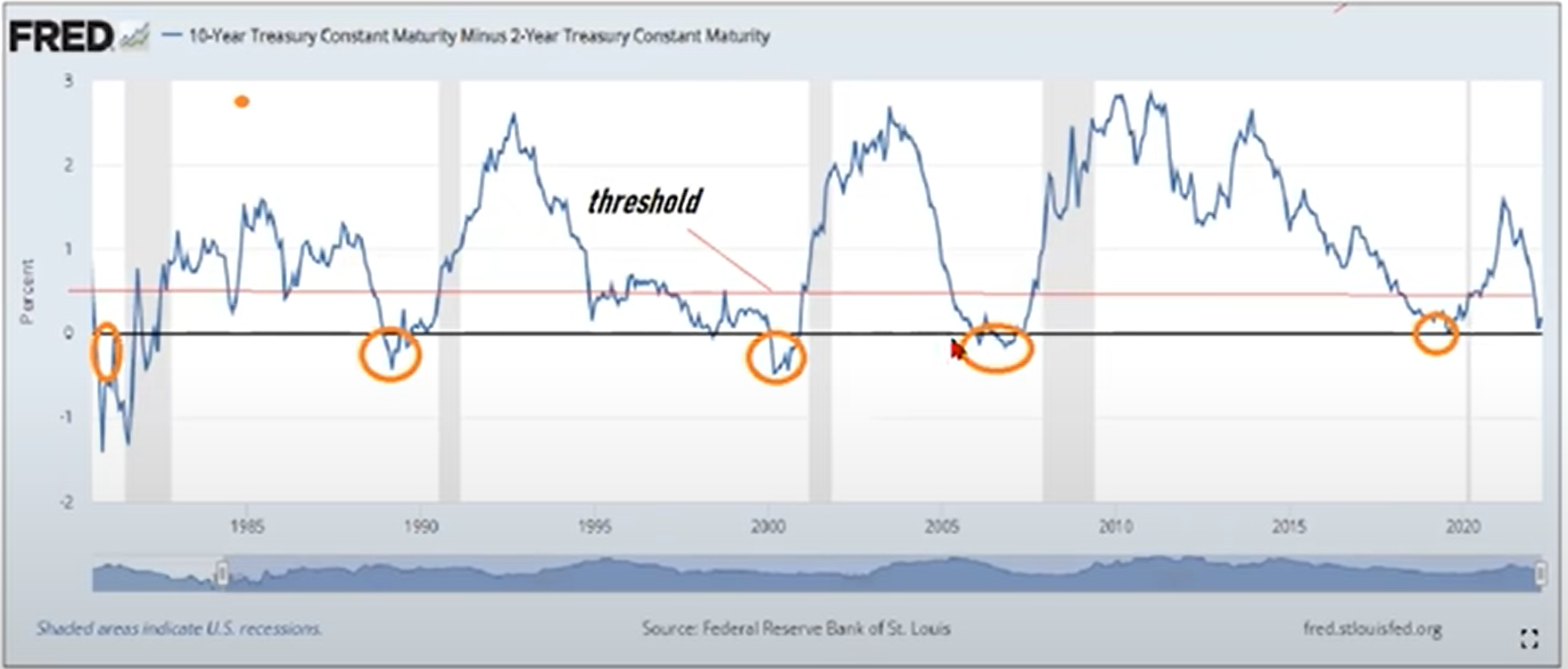

5. Inverted Yield Curve Follows by Recession — chart below from the Fed Reserve Bank of St. Louis shows the yield curve inversion follows by the recession usually precedes the market lead in the range of 10 to 34 months.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 11th, 2022

“Willingness and ability to hold funds uninvested while waiting real opportunities is the key to success in the battle for investment survival” — Gerald Loeb

1. Congressional Negotiators Settle on $10 Billion for Covid-19 Tests, Treatments — the package will allow the U.S. to purchase supplies, including more tests and vaccines, that the Biden administration said would be needed to continue to fight the virus. The $10 billion pulls from unused money in earlier bills passed by Congress, rather than representing new spending. Top U.S. health officials have been closely monitoring the Omicron BA.2 variant, which has triggered a surge in cases in parts of Europe and Asia, and now represents more than half of new Covid-19 cases in the U.S. President Biden said last week that without more federal dollars, another wave of the virus could lead to testing shortages similar to those experienced during the winter’s Omicron surge.

2. Fed Lays Out Plan to Prune Balance Sheet by $1.1 Trillion a Year — Federal Reserve officials laid out a long-awaited plan to shrink their balance sheet by more than $1 trillion a year while raising interest rates “expeditiously” to counter the hottest inflation in four decades. The roadmap for reducing the assets they bought during the pandemic was spelled out on Wednesday in minutes of their March meeting, when officials raised rates by a quarter point. They debated going bigger but chose caution in light of the uncertainty caused by Russia’s invasion of Ukraine, the record of their discussion showed.

3. U.S. Allies to Release Close to 60 Million Barrels of Oil From Reserves — U.S. allies are planning to release close to 60 million additional barrels of oil from their reserves, officials familiar with the matter said, joining the Biden administration in an effort to tame prices after they rose sharply when Russia invaded Ukraine.

The 31-member nations of the International Energy Agency—which include the U.S., most of Europe, Australia, Japan, Mexico and others—are planning to announce a new reserve release totaling 120 million barrels, officials said, the largest release in the IEA’s 47-year history. Around half of that amount will come from U.S. reserves, which were included in Washington’s previously announced decision to release 180 million barrels of oil over six months. That leaves around 60 million barrels of additional oil that will hit the market because of the IEA decision, which is expected to be announced by the end of the week. Those barrels are expected to be released over six months to track the U.S. schedule, an official said. IEA nations on March 1 announced the release of 60 million barrels—including 30 million barrels from the U.S.—in what was then the agency’s biggest-ever release of reserves.

4. Manufacturers Grind to a Halt in China as Covid Lockdowns Expand — manufacturers are struggling to keep some of their China operations going as extended and widening Covid-19 lockdowns choke off supplies and clog up truck routes and ports, heaping more pressure on the stretched global supply chain. Stringent government measures to contain the country’s Covid-19 outbreak, the worst in more than two years, are locking down tens of millions of people, mostly in and around the industrial heartland of Shanghai. The curbs are keeping many workers at home, restricting output at some factories and closing others, including component makers for Apple Inc. and Tesla Inc. Tesla, which suspended work at its factory in Shanghai on March 28, still hasn’t set a date for restarting production, according to people familiar with the matter. The electric-vehicle giant said it is implementing Covid-19 control requirements and setting work arrangements according to government policies.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 4th, 2022

“Accepting losses is the most important investment device to ensure safety of capital” — Gerard Loeb

1. Second Covid-19 Booster Shot Endorsed by FDA, CDC for Adults 50 and Older — the Food and Drug Administration said Tuesday it had cleared extra shots of Pfizer Inc. and its partner BioNTech SE and from Moderna Inc. for adults 50 years and older. The Centers for Disease Control and Prevention followed up by endorsing the second booster shots.

The extra doses are “especially important for those 65 and older and those 50 and older with underlying medical conditions that increase their risk for severe disease from Covid-19 as they are the most likely to benefit from receiving an additional booster dose at this time,” CDC Director Rochelle Walensky said.

2. Shanghai Lockdown Adds to China’s Economic Woes — the lockdown of one of China’s largest and most prosperous cities is the latest blow to the country’s economic fortunes, adding new risks to Beijing’s ambitious growth target in a politically sensitive year for leader Xi Jinping. The economic toll is only starting to come into view. Production at Shanghai-area factories operated by electric-vehicle maker Tesla Inc. and some other companies has been halted while domestic logistics networks have jammed up, slowing global supply chains, according to exporters and business owners. Meanwhile, hundreds of restaurants, retailers and other service-sector businesses have been shut down temporarily. The megacity of more than 25 million people, which accounts for roughly 4% of China’s total economic output and which is home to the country’s largest port and the regional headquarters of hundreds of multinational companies, initially sought to avoid a citywide lockdown. Instead, it systematically tested residents while blocking off some office towers in a bid to minimize disruptions to the economy and people’s daily lives, in line with Mr. Xi’s call this month “to achieve the biggest prevention and control effect with the smallest cost.”

3. Biden Considers Invoking Defense Production Act to Boost Minerals for EV Batteries — President Biden is considering invoking the Defense Production Act as soon as this week to boost domestic production of minerals used in batteries needed for electric vehicles, a person familiar with his plans said. The administration would include minerals like lithium, nickel and graphite, cobalt and manganese under the Korean War-era national security mobilization law, the person said. The designation could help mining companies access government funding for feasibility studies on mining development, productivity and safety improvements, or on how to wring more of these metals out of ore already produced at facilities operating in the U.S. It could also prompt Congress to dedicate more money to such efforts, the person said.

4. Biden to Draw Down Oil Reserves in Bid to Ease Gas Prices — President Biden will tap up to 180 million barrels of government oil reserves to help tamp down near-record high fuel prices, an unprecedented government intervention into oil markets following Russia’s invasion of Ukraine. In remarks from the White House late last week, Mr. Biden framed high energy prices as a wartime issue that requires a robust and wide-ranging response. The oil release—about 1 million barrels a day for six months starting in May—would be the Biden administration’s third, and by far the biggest-ever drawdown from the country’s emergency stockpile of roughly 568 million barrels.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

March 28th, 2022

“Accepting losses is the most single important device to ensure safety of capital” — Gerald Loeb

1. Biden to Sanction Hundreds of Russian Lawmakers — President Biden intends to announce the sanctions on more than 300 members of the Russian State Duma during his trip to Europe, where he will meet with allies from the North Atlantic Treaty Organization to formulate their next steps, according to U.S. officials and internal documents viewed by The Wall Street Journal. The Duma, while far less powerful than the Russian president, has acquired expanded constitutional responsibilities in recent years, particularly regarding the country’s economic affairs. It also serves as a link between various segments of the population and the government, relaying grievances and concerns upward, and distributing state assistance to the public.

2. Russian Stock Market to Partially Reopen — the challenge for Moscow is that the resumption of trading could simply send Russian stocks back into free fall. On Feb. 24, the day when President Vladimir Putin began the assault on Ukraine, the main Russian stock index tumbled 33%. While the index regained a fraction of those losses on Feb. 25—its last day of trading—that was before Western sanctions hammered the ruble and sent the country into an economic crisis.

To limit the fallout, Moscow has turned to some heavy-handed policies. It blocked foreign investors from dumping local stocks—a move that some market participants saw as retaliation for a Western freeze on Russian central bank assets since a big chunk of the Russian market is owned by foreigners. The Russian government ordered its main sovereign-wealth fund to buy billions of dollars worth of shares.

3. Biden Calls for Russia to Be Expelled From G-20 — President Biden said Russia should be expelled from the Group of 20 major economies and pledged the U.S. would take in up to 100,000 refugees fleeing Ukraine as he met Thursday with world leaders to discuss new sanctions and humanitarian aid in response to Moscow’s invasion. With Russian forces facing unexpectedly strong and lethal opposition from Ukrainian forces, Western leaders say they are worried Mr. Putin might resort to using weapons of mass destruction. NATO officials are grappling with the question of what actions by Russia would count as red lines that could prompt more-direct involvement by the alliance. Officials said Russia’s potential use of chemical weapons was part of the discussion among NATO leaders.

4. U.S. to Boost Gas Deliveries to Europe Amid Scramble for New Supplies — The U.S. is ramping up shipments of liquefied natural gas to Europe this year as the continent mounts a world-wide hunt for new supplies to phase out its reliance on Russian energy after the invasion of Ukraine. The globe-spanning effort to wean Europe off Russian energy supplies was at the center of President Biden’s summit with European Union leaders this week in Brussels. The U.S. aims to ship 50 billion cubic meters of LNG to Europe annually through at least 2030, officials said Friday, making up for about a third of the gas the EU receives from Russia. The EU imported a record 22 billion cubic meters of LNG from the U.S. last year. Officials across the continent are racing to sign new contracts with producers in the Middle East and Africa before next winter; EU leaders on Friday also decided to band together when negotiating supply agreements, using the bloc’s collective economic weight to get lower prices.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »