Week of April 22, 2022 Weekly Recap & The Week Ahead

April 25th, 2022“Patient opportunism, buttressed by a contrarian attitude and a strong balance sheet, can yield amazing profits during meltdowns.”

― Howard Marks

1. U.S. Home Prices Hit a Record of $375,300 in March — U.S. home prices soared to a new record in March while mortgage rates continued to rise rapidly, slowing home sales in what has been the hottest housing market in more than 15 years. The rise of remote work and the pursuit of more space unleashed a powerful wave of home buying when Covid-19-related lockdowns started to ease in the middle of 2020. The frenzied housing market, supported by ultralow interest rates at the time, lifted home prices throughout the country. Homes for sale often stayed on the market for less than a month, and sometimes only days, while open houses could draw lines around the block.

Now, that frenzy is starting to ease and the volume of home sales is reverting to pre-pandemic levels, said Lawrence Yun, chief economist for the National Association of Realtors. With mortgage rates at 5% and back to their highest level since 2011, Mr. Yun said he expects home sales in 2022 to decline 10% from last year.

2. Florida Bill to End Disney’s Special Tax District Heads to Gov. DeSantis for Signature — Florida lawmakers gave final approval to a bill that would end a special tax district that allows Walt Disney Co. DIS 0.07% ▲ to govern the land housing its theme parks, sending the measure to Republican Gov. Ron DeSantis, who has made clear he would sign it. The move marks a significant setback for Disney’s Florida operations. The special district, created in 1967 and known as the Reedy Creek Improvement District, exempts Disney from numerous regulations and certain taxes and fees. It has permitted the company to manage its theme parks and resorts in the state with little red tape for more than 50 years.

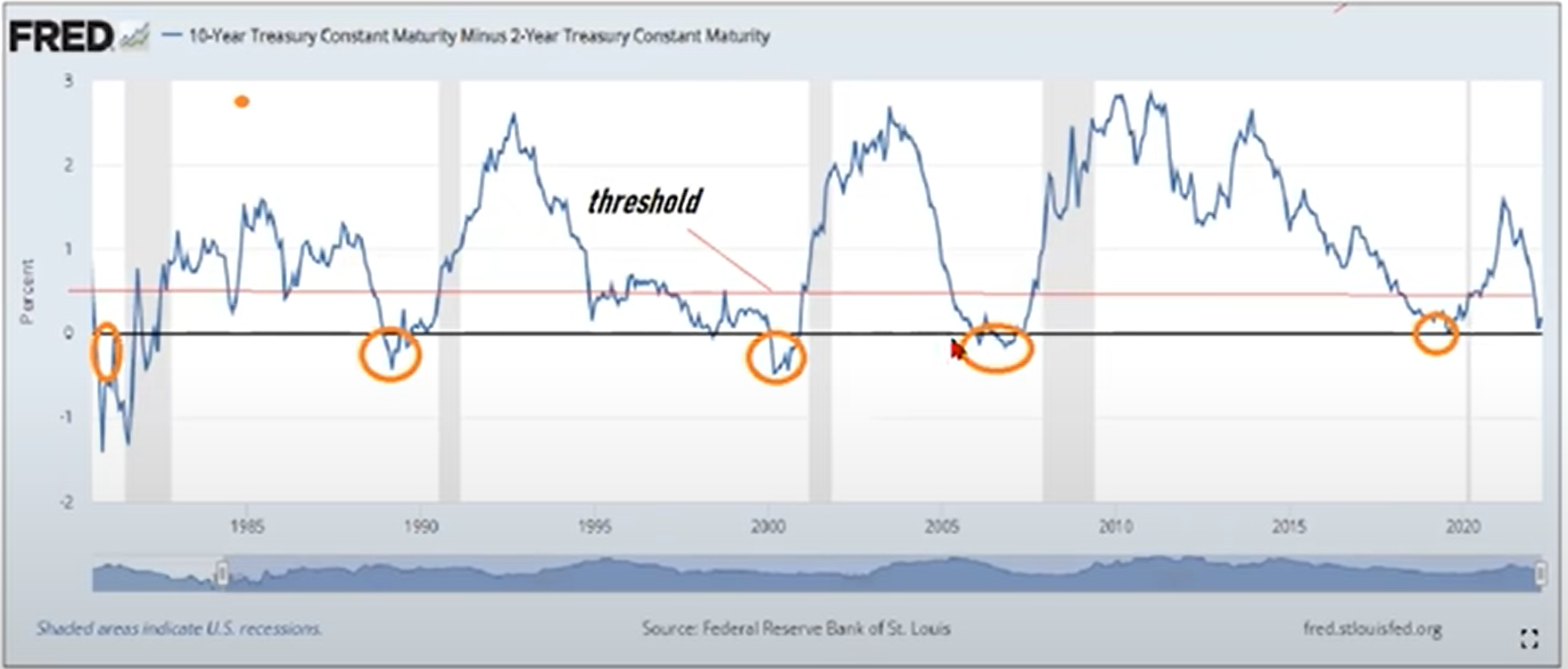

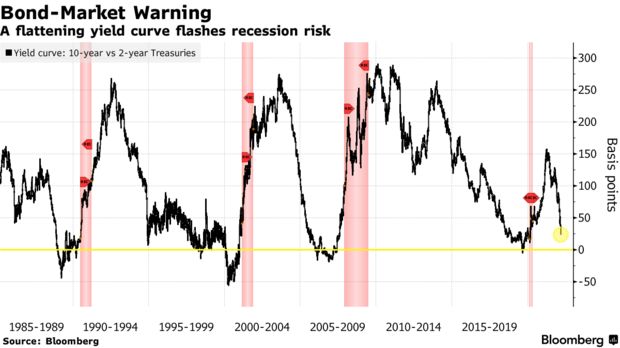

3. Fed’s Jerome Powell Seals Expectations of Half-Point Rate Rise in May — Federal Reserve Chairman Jerome Powell signaled the central bank was likely to raise interest rates by a half percentage point at its meeting next month and indicated similar rate rises could be warranted after that. The Fed has indicated it is also set to begin shrinking its $9 trillion asset portfolio.

4. Mortgage Rates Continue to Rise — the average rate for a 30-year fixed-rate mortgage rose to 5.11%, mortgage-finance giant Freddie Mac said Thursday. The rate hit 5% last week for the first time since 2011, up from 3.22% at the beginning of 2022. The Federal Reserve’s pullback from the mortgage-bond market has helped drive up interest rates on home loans in recent months. So too has its posture on interest rates. The Fed is expected to raise its benchmark rate again at its meeting early next month, and it has signaled that more increases are likely this year. That has driven up yields on the 10-year Treasury note, to which mortgage rates are closely tied.

The combination of rising rates and record home prices has started to weigh on demand. Sales of existing homes dropped 4.5% in March from a year earlier, according to the National Association of Realtors. Purchase mortgage applications last week fell 3% from the prior week and 14% from a year earlier, according to the Mortgage Bankers Association.

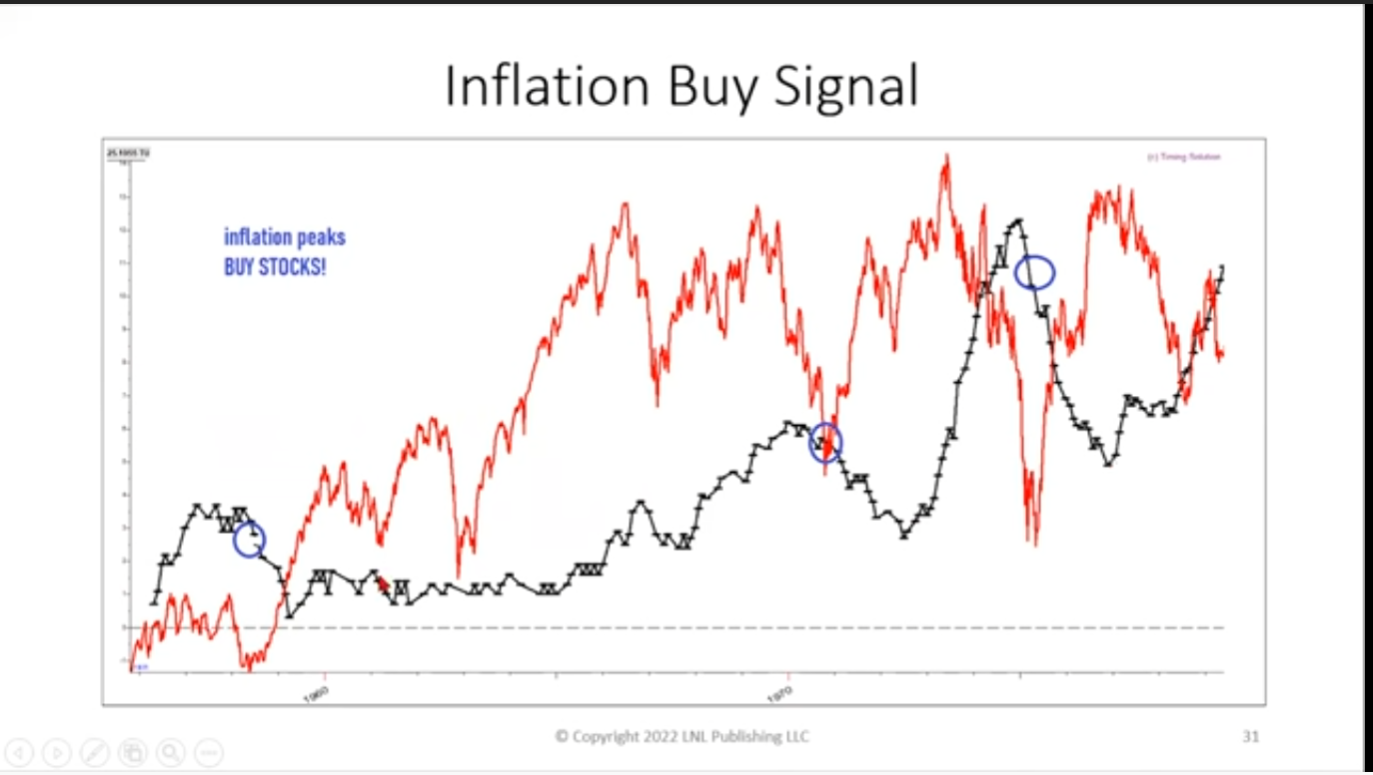

5. Past History of Inflation — based on past history, as inflation tops and starts to rollover, stock market will start to rally as inflation is discounted.

The week ahead — Economic data from Econoday.com: