Week of March 4, 2022 Weekly Recap & The Week Ahead

“There ‘s an old saying in poker that there’s a “fish” in every game, and if you’ve played for an hour without having figured out who the fish is, then it’s you.” — unknown

1. IEA Will Deploy Emergency Oil Stocks to Ease Soaring Prices — the U.S. and other major economies have agreed on a coordinated release of oil stockpiles after Russia’s invasion of Ukraine pushed crude above $100 a barrel. The International Energy Agency, which represents key industrialized consumers, will deploy 60 million barrels from stockpiles around the world. Half of that amount will come from the U.S. Strategic Petroleum Reserve, with the rest from IEA members in Europe and Asia, said a person familiar with the matter, who asked not to be named because the information isn’t public.

That will be the second release from American crude reserves within a few months as soaring fuel costs become a growing political problem for President Joe Biden.

2. As Russia Sanctions Intensify, Several Oligarchs Speak Out Against Ukraine War — in recent days a parade of Russian businessmen burnished their antiwar stances as governments tightened a noose around Kremlin-connected businesses and property. Oligarch Roman Abramovich, who hasn’t been sanctioned, said that he was helping Ukraine negotiate peace with Russia. Oleg Tinkov, the billionaire founder of Russia’s Tinkoff Bank, a unit of TCS Group Holding PLC, highlighted the work his foundation does to help children and his desire for no war. Mr. Tinkov also hasn’t been sanctioned. Oleg Deripaska, a raw-materials magnate who was previously sanctioned in the U.S., wrote on social media Sunday that peace “is very important.” The European Union said Monday night that it added 26 prominent Russians officials and businessmen to its sanctions list, freezing their assets and imposing travel bans. The U.K. is expected to sanction more oligarchs in the coming days. Even Monaco, famed for its generous tax rules and status as a playground for the well-heeled, said it was clamping down on sanctioned Russians.

3. Russia Keeps Stock Market Closed in Longest Pause Since 1998 — Russia will keep local stock trading closed for a third day as its wealth fund prepares to deploy billions of dollars to buy the country’s battered stocks following the invasion of Ukraine. The three-day shuttering of stock trading on the Moscow bourse is its longest closure for extraordinary circumstances since October 1998, according to the exchange. The halt came after the U.S. and Europe imposed harsher sanctions on Russia over the war in Ukraine, sending the country’s assets plunging. As much as half of Russia’s international reserves may have been frozen abroad as punishment for Putin’s invasion of Ukraine. In response, the central bank has introduced capital controls and banned foreigners from selling securities locally, effectively shutting the exits for investors. European Union ambassadors have also agreed to exclude seven Russian banks from the SWIFT financial-messaging system.

4. Fed’s Powell Says Ukraine War Creates Risks of Higher Inflation — Federal Reserve Chairman Jerome Powell said that Russia’s invasion of Ukraine was likely to push up inflation, a setback to central bank expectations that price pressures would diminish in the coming months. Because of Russia’s role in global energy and other commodity markets, “we’re going to see upward pressure on inflation at least for a while,” Mr. Powell told the Senate Banking Committee on Thursday. Consumer prices in January rose 6.1% from a year earlier, according to the Fed’s preferred gauge. Excluding volatile food and energy categories, so-called core inflation rose 5.2%, close to a 40-year high.

5. Strong Hiring, Low Unemployment Point to Economy Making Post-Pandemic Pivot — employers added 678,000 workers to their payrolls in February, the biggest gain in seven months, the Labor Department said Friday. The jobless rate fell to 3.8% from 4.0% a month earlier, edging closer to the 50-year low of 3.5% hit just before the pandemic. Hotels, restaurants, amusement parks and other hospitality industries led the way in hiring as firms sought to accommodate a growing number of vacationers, convention attendees and business travelers. Big states and cities in recent days have lifted some of the remaining Covid restrictions, which could further boost business and hiring. However, big threats loom, including a sharp run-up in oil prices that could crimp household spending and ultimately nick the economic and labor market recovery, economists said.

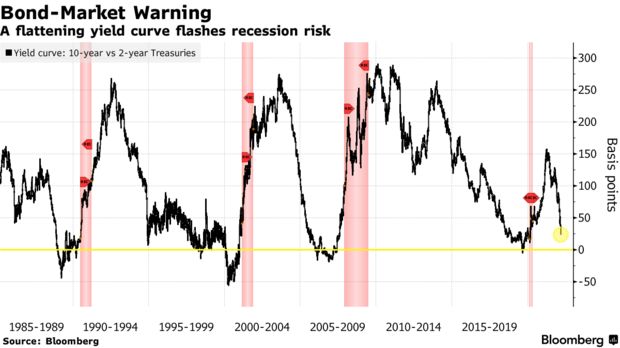

6. Bond Market Warning — from Bloomberg, the specter of stagflation, a rare combination of surging prices in a constricting economy, is showing in the bond market. Ten-year inflation breakevens just increased to the highest level since 2005, while the yield curve — the spread of 10- over two-year Treasury yields — narrowed to levels not seen since the pandemic recession. History shows an outright inversion, as happened in 2019, would signal an imminent contraction.

The week ahead — Economic data from Econoday.com: