November 21st, 2022

“Every battle is won or lost before it’s ever fought” — unknown

1. FTX Says Number of Creditors in Bankruptcy Could Top 1 Million — FTX’s bankruptcy could involve “more than one million creditors,” its lawyers said in court filings late Monday, showing the vast reach the second-largest cryptocurrency exchange had before its downfall. Its sudden collapse this month has jolted the financial world. Digital currencies including bitcoin have fallen significantly in the past week, while lawmakers have stepped up their pushback against crypto-friendly legislative proposals.

2. U.S. Retail Sales Rose 1.3% in October Ahead of Holiday Season — U.S. retail sales rose sharply in October as consumers spent more on everyday staples and big-ticket items such as autos and furniture.

Retail sales—which includes spending on clothing, wine and ottomans but also meals at restaurants—increased a seasonally adjusted 1.3% in October compared with September, when spending was unchanged from the prior month, the Commerce Department reported. Consumers spent more at auto dealers, furniture stores, grocery stores and gasoline stations. Retail sales—which includes spending on clothing, wine and ottomans but also meals at restaurants—have generally risen in recent months amid higher prices and rising interest rates that can make purchases, particularly big ones, more expensive.

3. Crypto Lender BlockFi Plans Bankruptcy Filing Within Days in FTX Fallout — cryptocurrency lender BlockFi Inc. is preparing to file for bankruptcy within days, according to people with knowledge of the matter who asked not to be named because discussions are private. The crypto lender paused client withdrawals, citing uncertainties with FTX, while saying it had adequate liquidity and was exploring options with outside advisers. FTX US and BlockFi are closely tied. In July, FTX US provided the lender with a $400 million revolving credit line, which came with an option to purchase the company. And BlockFi has given loans to now-bankrupt Alameda Research, Bloomberg reported.

The sudden unraveling and subsequent bankruptcy of FTX — once seen as a savior to struggling crypto firms — is reverberating across the digital asset landscape. Bankrupt Voyager Digital Ltd., which Sam Bankman-Fried was going to rescue in a $1.4 billion deal, is now scrambling to find a replacement buyer for its assets. And Genesis is exploring options after suspending redemptions and new loan originations amid a liquidity shortfall.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 14th, 2022

‘Only when the tide goes out that do you discover who’s been swimming naked. ‘ – Warren Buffett.

1. Consumer Prices Rose 7.7% in October From Year Earlier — the Labor Department on Thursday said that its consumer-price index increased 7.7% in October from the same month a year ago, the smallest 12-month increase since January 2022. The reading was down from 8.2% in September. June’s 9.1% inflation rate was the highest in four decades.

On a monthly basis, the CPI rose 0.4% in October from September, the same pace as the previous month. The CPI measures what consumers pay for goods and services.

The so-called core CPI—which excludes volatile energy and food prices—climbed 6.3% in October from a year earlier, down from 6.6% in September, which was the biggest increase since August 1982. The October inflation report could keep Federal Reserve officials on track to approve a half-percentage-point interest-rate increase next month and to pencil in slightly higher rates next year than they had anticipated previously.

2. FTX Hurtles Toward Bankruptcy With $8 Billion Hole, US Probe — the crisis engulfing Sam Bankman-Fried’s FTX.com is rapidly worsening, with the onetime crypto wunderkind warning of bankruptcy if his firm can’t secure funds to cover a shortfall of as much as $8 billion. The acknowledgment of his firm’s deepening troubles and limited options is a stunning turn for Bankman-Fried, who was once worth $26 billion and likened to John Pierpont Morgan. It also underscores the uncertainty hanging over FTX, its clients and cryptocurrency markets.

3. FTX Files for Bankruptcy — beleaguered cryptocurrency platform FTX filed for bankruptcy protection Friday—a swift demise for a company hailed as a trusted platform just a week ago. In a statement, the company said Chief Executive Sam Bankman-Fried resigned from his position but would remain at the company to assist with an orderly transition. FTX said that it would begin a process to review and monetize assets for stakeholders. FTX is the latest in a string of crypto companies seeking bankruptcy protection this year. Months ago, Mr. Bankman-Fried served as a lender of last resort to his industry, following the failure of other crypto companies. Its fortunes reversed in the past 10 days, after a CoinDesk report showed the depth of the relationship between FTX and Alameda, triggering a loss of faith in the platform by amateur and professional investors.

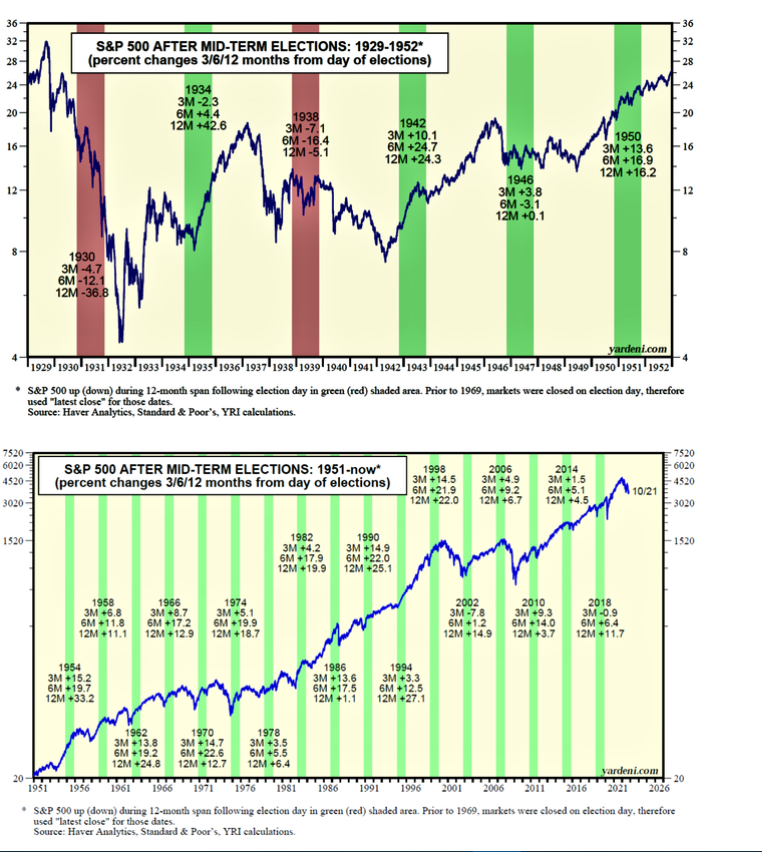

4. The midterm-election effect on the S&P500 Index — historically, midterm elections set up nice rallies with phenomenal consistency. Since 1942, after midterm elections the S&P 500 went up 7.6%, 14.1%, and 14.9% over the next three, six and 12 months, notes Ed Yardeni of Yardeni Research. That’s irrespective of the election outcome. The two charts below show the history. The green- and red-shaded areas represent the 12 months following an election. The percentage market move during the three-, six- and 12-month time frames are written below the election year.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 7th, 2022

“Markets are never wrong – opinions often are.” — Jesse Livermore

1. Fed Approves Fourth 0.75-Point Rate Rise, Hints at Smaller Hikes — the Federal Reserve lifted interest rates by 0.75 percentage point to combat inflation and signaled plans to keep raising them, though possibly in smaller increments. Fed officials in the latest policy statement acknowledged it could take time for rapid increases this year to be reflected in the economy. “The committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments,” they said at the conclusion of a two-day meeting. Officials are boosting interest rates at the fastest pace since the early 1980s to reduce inflation that is running near a 40-year high. They have raised rates by 0.75 point at four consecutive meetings, with the latest one taking the central bank’s benchmark federal-funds rate to a range between 3.75% and 4%.

2. Bank of England Raises Key Interest Rate by 0.75 Point — the Bank of England raised its key interest rate by 0.75 percentage point on Thursday, the largest increase since 1989, in an effort to tame surging inflation but which, by the bank’s own estimates, will help drive the U.K. economy into a recession lasting over a year.

The central bank lifted its benchmark lending rate for the eighth consecutive meeting to 3% from 2.25%, taking it to the highest level since November 2008. Higher borrowing costs will hurt an already weak economy as consumers brace for a difficult winter of falling real incomes and rising prices.

3. Surge in Pediatric Respiratory Viruses, Including RSV, Strains Children’s Hospitals — physicians are reporting unseasonably high numbers of respiratory illnesses in children, straining many children’s hospitals before the typically busier winter months. RSV is an easily transmissible virus that infects the respiratory tract. The virus spreads through droplets from coughing and sneezing and on surfaces. Positive tests for RSV have been on the rise across the U.S., according to the Centers for Disease Control and Prevention. The increase in cases has come ahead of the typical winter peak for such illnesses, hospital officials said. For most people, RSV amounts to a cold, and nearly all children come in contact with the virus by the age of two, health authorities said. But it can be severe for some infants and older adults, especially for those who have pre-existing health conditions.

4. Jobs Report Shows Payrolls Grew 261,000 in October — Employers added a seasonally adjusted 261,000 jobs in October, a robust number but the fewest since December 2020, and the unemployment rate rose to 3.7%, the Labor Department said Friday. Wage gains in October ticked up from the previous month. On an annual basis, however, wage increases have eased, a possible sign of loosening in the labor market. The report points to an economy that is gradually losing momentum following a torrid stretch of growth last year and earlier this year. Over the past three months, employers added an average 289,000 jobs a month, down from 539,000 during the same period a year ago. But that is still far more than before the pandemic. In 2019, job gains averaged 164,000 a month.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 2nd, 2022

THERE WILL NOT BE ANY POSTING FOR THE WEEK OF OCT 28 2022 — WE ARE AWAY FOR THE LONG WEEKEND.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 24th, 2022

“It is not the strongest or the most intelligent who will survive but those who can best manage change.” – Charles Darwin

1. Home Construction Fell 8.1% in September — new home construction fell 8.1% in September, a sign that higher mortgage rates continue to cut into buyer demand and depress new building. Housing starts, which measure the beginning of construction on a new home, fell to a seasonally-adjusted annual rate of 1.44 million in September, 8.1% below the revised August estimate of 1.56 million and 7.7% below the September 2021 rate, according to Census Bureau and Department of Housing and Urban Development data released today. Consensus estimates gathered by FactSet had anticipated homes to have been started at a rate of about 1.47 million.

2. Fed’s Beige Book Says Businesses Expect Economy to Weaken — the Fed’s 12 regional reserve-bank districts said business contacts noted “growing concerns about weakening demand,” according to the central bank’s latest compilation of economic anecdotes from around the country, known as the Beige Book. Businesses reported that price pressures remained elevated through early October with some cost increases moderating. “Declines in commodity, fuel, and freight costs were noted,” the report said.

3. U.S. Home Sales Dropped for Eighth Straight Month in September — Sales of previously owned homes declined 1.5% in September from the prior month to a seasonally adjusted annual rate of 4.71 million, the weakest rate since May 2020, the National Association of Realtors said Thursday. September sales fell 23.8% from a year earlier. Existing-home sales have dropped 27% from their recent peak in January as the Federal Reserve’s actions to increase interest rates have pushed many prospective home buyers out of the market.

Some buyers no longer qualify for mortgages at current rates, while others have stepped back from the market due to broader uncertainty about the economy, real-estate agents say. Many current homeowners have mortgage rates below 4%, and some prospective sellers are opting to stay put rather than sell their homes and buy new ones with higher borrowing costs.

4. US Budget Deficit Plunges to $1.38 Trillion as Pandemic Aid Unwinds — The deficit for the fiscal year through September narrowed to $1.38 trillion, from a revised $2.78 trillion the previous year, according to US Treasury Department data released late last week. The deficit reduction came even after the Treasury accounted for President Joe Biden’s move to forgive a swath of student loans. The department said loan modifications had a $430 billion impact on the month of September, a sharp increase from the $137 billion recognition of such costs in September 2021. The Treasury said that it didn’t anticipate further such large-scale hits to the budget from the loan-forgiveness move in subsequent months.

FISCAL 2022 FISCAL 2021

Revenue $4.896 trillion $4.046 trillion

Outlays $6.272 trillion $6.822 trillion

Deficit $1.375 trillion $2.776 trillion

Deficit as % of GDP 5.5% 12.3%

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 17th, 2022

“If you want to be the best, you have to do things that other people are unwilling to do. —Michael Phelps

1. Bank of England Further Expands Bond-Market Rescue to Restore U.K.’s Financial Stability — the Bank of England extended support targeted at pension funds for the second day in a row, the latest attempt to contain a bond-market selloff that has threatened U.K. financial stability. The turmoil sparked fresh demands for pension funds to come up with cash to shore up LDIs, or liability-driven investments, derivative-based strategies that were meant to help match the money they owe to retirees over the long term.

LDIs were at the root of the bond selloff that prompted the BOE’s original intervention. Pension plans in late September saw a wave of margin calls after Prime Minister Liz Truss’s government announced large, debt-funded tax cuts that fueled an unprecedented bond-market selloff.

2. Fed Minutes Show Policy Pivot Is Not Coming Soon — the minutes noted “broad-based and unacceptably high level of inflation,” and said risks to the inflation outlook are increasing. Many participants emphasized that the cost of taking too little action against inflation outweighed the cost of doing too much, and several underlined the need to maintain a restrictive stance for as long as necessary. A couple of those officials stressed that historical experience demonstrated the danger of prematurely ending periods of tight monetary policy designed to bring down inflation.

3. Core US Inflation Rises to 40-Year High — the core consumer price index, which excludes food and energy, increased 6.6% from a year ago, the highest level since 1982, Labor Department data showed Thursday. From a month earlier, the core CPI climbed 0.6% for a second month. The advance was broad based. Shelter, food and medical care indexes were the largest of “many contributors,” the report said. Prices for gasoline and used cars declined. The CPI report is the last one before next month’s US midterm elections and poses fresh challenges to President Joe Biden and Democrats as they seek to retain thin congressional majorities. Already, the surge in inflation has posed a serious threat to those prospects.

4. U.K. Prime Minister Liz Truss Fires Treasury Chief, U-Turns on Taxes — U.K. Prime Minister Liz Truss fired Treasury chief Kwasi Kwarteng and reversed crucial parts of her government’s tax cuts, after her plans to jolt the economy into growth unraveled in spectacular fashion following a backlash from financial markets and her party. In a scramble to shore up support within her party, the embattled Ms. Truss also ditched her plan to prevent a planned rise in the rate of corporate income tax next April to 25% from 19%—a move taken by predecessor Boris Johnson’s government to help shore up finances. The U-turn was the second major part of her tax-cutting package to be abandoned recently. The turmoil in the U.K. is a sharp reminder of the political and economic challenges facing leaders across the West as they grapple with fast-rising inflation and weak growth. Price increases are forcing central banks to quickly raise interest rates, denting economic growth and making financial markets far more sensitive to deficits and debt.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 10th, 2022

“Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria,” — John Templeton

1. Micron to Spend Up to $100 Billion on Chip Factory in New York State — Micron Technology Inc. has agreed to invest as much as $100 billion to build a semiconductor-manufacturing campus in upstate New York, adding to a wave of chip-making plans in the U.S. as Washington tries to boost domestic manufacturing of those critical components. Micron said a year ago that it would spend as much as $150 billion on additional production capacity, though didn’t say where the new money would go. The company had held off on committing to the spending until the U.S. government had approved billions of dollars in subsidies for domestic chip making. “We will need support from the federal government as well as appropriate support from state governments to bridge the 35% to 45% cost gap that exists in overseas production,” Micron Chief Executive Sanjay Mehrotra said earlier this year.

2. U.S. Job Openings Fell in August, Layoffs Up Slightly — employers’ total job openings fell 10% in August to a seasonally adjusted 10.1 million from 11.2 million the month before, the Labor Department said Tuesday. The 1.1-million drop in openings is the largest decline since the early months of the Covid-19 pandemic in 2020, leaving job openings at their lowest level in a year. Openings dropped the most in healthcare, retail and other services industries. The decline in openings coincided with an August easing of job growth. Employers added 315,000 jobs that month, compared with 526,000 jobs in July. The figures reflect a labor market that is still strong overall, but lost some steam in August after recovering rapidly from the effects of the pandemic.

3. OPEC+ Agrees to Biggest Oil Production Cut Since Start of Pandemic — the Organization of the Petroleum Exporting Countries and its Russia-led allies agreed on Wednesday to slash output by 2 million barrels of oil a day, delegates said, a move likely to push up already-high global energy prices and help oil-exporting Russia pay for its war in Ukraine. The move drew an immediate rebuke from the White House, which called the decision shortsighted and suggested the 23-member group collectively known as OPEC+ was actively supporting Russian President Vladimir Putin. It came less than three months after President Biden visited Saudi Arabia, the OPEC’s de facto leader, in a bid to repair relations between the world’s biggest oil consumer and its biggest crude-oil exporter during a period of rising inflation driven in part by high energy prices.

4. September Jobs Report Shows Payrolls Grew by 263,000 — U.S. employers added 263,000 jobs in September, continuing a gradual cooling pattern in the labor market as high inflation and rising interest rates weighed on the economy. The unemployment rate fell to 3.5% from 3.7% in August, the Labor Department said Friday, matching a half-century low that was last reached in July, a reflection of people leaving the job market. Wages rose 5.0% in September from the same month a year earlier, a slower pace than August’s 5.2% annual rate. Job gains were led by the leisure and hospitality industry, which added 83,000 jobs. Healthcare employment rose 60,000.

The number of job openings fell 10% in August to a seasonally adjusted 10.1 million from 11.2 million the month before, the Labor Department said Tuesday. The 1.1 million drop in openings is the largest decline since the early months of the Covid-19 pandemic in 2020. That left job openings at their lowest level in a year but still above their prepandemic level in 2019, when they averaged 7.2 million a month.

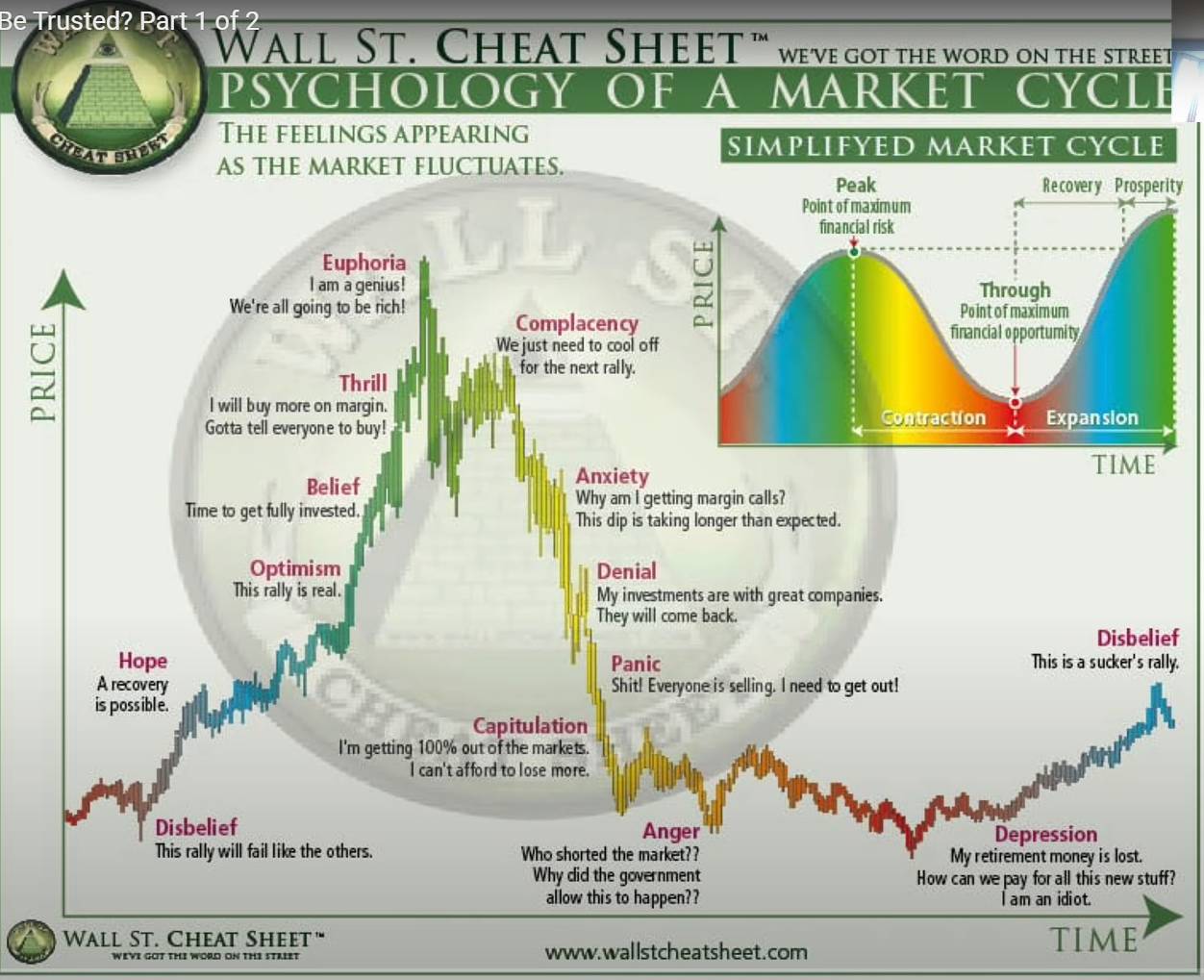

Below is the diagram depicting Stock Market Psychology courtesy of WallStCheatSheet

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 3rd, 2022

“There is nothing new in Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again. – Jesse Lauriston Livermore

1. Bank of England Buys Bonds in Bid to Stop Spread of Crisis — the Bank of England launched an emergency intervention to restore order in bond markets after a government tax-cut plan sent borrowing costs soaring and triggered a meltdown in complex financial instruments held by pension funds. The move aimed to stanch the damage from a furious selloff in U.K. government debt in recent days and stop the losses from running out of control, analysts said. The bank said it offered to buy £5 billion of bonds late last week (equivalent to $5.4 billion) but only took in £1 billion, indicating a limited amount of firepower was required to move markets.

2. Home Prices Suffer First Monthly Decline in Years — U.S. home prices slid in July from June, the first monthly decline in years and the latest sign that higher mortgage rates are starting to weigh on home prices in many of the country’s biggest markets. The S&P CoreLogic Case-Shiller National Home Price Index, which measures the average change in home prices across the nation, fell 0.3% in July from June, the first month-over-month decline since January 2019. On a seasonally adjusted basis, the national index fell 0.2%. That was the first monthly decline in more than a decade by this measure. The average rate on a 30-year fixed-rate mortgage was 6.29% in the week ended Sept. 22, up from 2.88% a year earlier, according to housing-finance agency Freddie Mac.

3. Mortgage Rates Rise to 6.7%, Highest Since 2007 — mortgage rates rose to their highest level in more than 15 years, a new high since the 2008-09 financial crisis that adds pressure to the already cooling U.S. housing market. The average rate on a 30-year fixed mortgage climbed to 6.7%, according to a survey of lenders released Thursday by Freddie Mac. lt was the highest rate since July 2007 and marked the sixth week in a row of rising rates. A year ago, rates were 3.01%.

The surge in mortgage rates follows a series of interest-rate increases from the Federal Reserve. The central bank has moved aggressively to try to cool the highest inflation in decades, raising its benchmark rate five times this year. Officials have indicated more increases are likely in the months ahead.

4. U.S. Jobless Claims Hit Lowest Level in Five Months — initial jobless claims, a proxy for layoffs, decreased to a seasonally adjusted 193,000 last week from a revised 209,000 the previous week, the Labor Department said Thursday. The total was the lowest since late April and below the prepandemic average of 218,000 in 2019, when the labor market was also tight. The Commerce Department separately said inflation in the second quarter was higher than previously estimated, pointing to the difficulties the Federal Reserve faces in tamping down persistent price increases that have spread through the economy. The department didn’t revise its estimate that the U.S. economy, as measured by gross domestic product, contracted 0.6% in the April to June period, however. Consumer spending was stronger than previously estimated, it said, but revised estimates of U.S. exports and inventories offset the improved spending picture.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

September 26th, 2022

“Markets are never wrong – opinions often are.” — Jesse Livermore

1. U.S. Home Sales and Prices Fell in August as Mortgage Rates Rose — sales of previously owned homes dropped 0.4% in August from July to a seasonally adjusted annual rate of 4.8 million, the weakest rate since May 2020, the National Association of Realtors said Wednesday. August sales fell 19.9% from a year earlier.

The housing market has slowed in recent months—with seven months of monthly sales declines through August—as the Federal Reserve aggressively raises interest rates to cool the economy and bring down high inflation. That has led to higher mortgage-interest rates and increased borrowing costs for home buyers by hundreds of dollars a month, pushing many out of the market. The average rate on a 30-year fixed-rate mortgage was 6.02% in the week ended Sept. 15, up from 2.86% a year earlier, according to housing-finance agency Freddie Mac.

2. Fed Raises Interest Rates by 0.75 Percentage Point for Third Straight Meeting — the Federal Reserve approved its third consecutive interest-rate rise of 0.75 percentage point and signaled additional large increases were likely at coming meetings as it combats inflation that remains near a 40-year high.

The decision Wednesday—unanimously supported by the Fed’s 12-member rate-setting committee—will lift its benchmark federal-funds rate to a range between 3% and 3.25%, a level last seen in early 2008. Most of the 19 officials who participated at the Fed’s policy meeting expect to lift the rate at least by another 1.25 percentage point by December, to a range between 4.25% and 4.5%, according to their new projections latest release. The Fed has two more meetings this year.

3. A Day After Fed Raises Rates, Reverse Repos Hit New Record — the Federal Reserve Bank of New York said that a day after the U.S. central bank pushed up its short-term target rate by a large 0.75 percentage point to between 3% and 3.25%, money-market funds and others parked a record $2.359 trillion at the New York Fed’s reverse repo facility. The facility last saw a record inflow on June 30, at $2.329 trillion. That surge came at the end of a quarter, often a time where the reverse repo facility pulls in a significant amount of money due to temporary market factors. The Fed’s reverse repo tool takes in cash, primarily from money-market funds. It is designed to help set a lower end for short-term interest rates. After the Fed’s rate rise Wednesday, the rate now stands at 3.05%, up from 2.30% in place before the Fed lifted rates.

The Fed uses another tool, called the interest on reserves balances rate, now at 3.15%, to set a high end for short-term rates. Together, both rates drive the market-based setting of the federal-funds rate, the central bank’s primary tool to achieve its inflation and job mandates.

4. Oil Falls Below $80 a Barrel — U.S. oil prices fell below $80 a barrel for the first time since January, dragged down by mounting fears of a global recession and a rapidly strengthening U.S. dollar. West Texas Intermediate crude futures dropped 5.7% to close at $78.74. The main U.S. oil price is down about 36% from its June peak and nearly to where it began the year. Brent crude, the global benchmark, shed 4.8% Friday to end at $86.15. Behind the slide: A string of major central banks—including the Federal Reserve, the Bank of England, the Swiss National Bank and Norway’s Norges Bank—raised interest rates this week. Tightening financial conditions on a near-global basis have ratcheted up fears about a widespread economic slowdown, which would also mean lower energy demand. Business surveys Friday indicated that economic activity in Europe declined sharply in September.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

September 19th, 2022

“Every battle is won or lost before it’s ever fought” – Sun Tzu

1. U.S. Inflation Remained High in August — the Labor Department on Tuesday reported its consumer-price index rose 8.3% in August from the same month a year ago, down from 8.5% in July and from 9.1% in June, which was the highest inflation rate in four decades. The CPI measures what consumers pay for goods and services. So-called core CPI, which excludes often volatile energy and food prices, increased 6.3% in August from a year earlier, up markedly from the 5.9% rate in both June and July—a signal that broad price pressures strengthened.

On a monthly basis, the core CPI rose 0.6% in August—double July’s pace. Investors and policy makers follow core inflation closely as a reflection of broad, underlying inflation and as a predictor of future inflation.

2. Mortgage Rates Hit 6.02%, Highest Since the Financial Crisis — per WSJ, the average rate on a 30-year fixed mortgage climbed to 6.02% this week, up from 5.89% last week and 2.86% a year ago, according to a survey of lenders released late last week by mortgage giant Freddie Mac. The last time rates were this high was in the heart of the financial crisis in 2008, when the U.S. was deep in recession. The jump in mortgage rates is one of the most pronounced effects of the Federal Reserve’s campaign to curb inflation by lifting the cost of borrowing for consumers and businesses. Already, it has ushered in a sea change in the housing market by adding hundreds of dollars or more to the monthly cost of a potential buyer’s mortgage payment, slowing what was a red-hot market not so long ago. Higher rates are forcing some would-be buyers to continue renting. Other buyers are skimping elsewhere to make their mortgage payments.

3. U.S. Retail Sales Rose 0.3% in August, Showing Resilience in Face of Inflation — according to WSJ, U.S. consumers spent at a steady pace in August as gasoline prices fell, with purchases of vehicles and back-to-school items like clothing driving the gain. Retail sales, a measure of spending at stores, online and in restaurants, rose 0.3% in August from the prior month, the Commerce Department said Thursday. July spending was revised down to a 0.4% decline from a previous flat reading.

Much of August’s gain was due to higher spending on vehicles, with purchases at motor vehicle and parts dealers up 2.8% on the month. A measure of spending that strips out vehicle sales declined 0.3% from July. Stripping out both vehicle and gasoline spending, retail sales rose 0.3%.

4. FedEx Stock Tumbles After Warning on Economic Trends — The delivery giant’s shares lost 21% Friday—its biggest one-day percentage drop ever—after the company said a macroeconomic slowdown had led to lower volumes of goods moving around the world in recent weeks. FedEx and rival United Parcel Service Inc. have confronted lower volumes of packages this year as a pandemic boom in online shopping cools. Consumers have switched more of their spending to travel and entertainment, plus high inflation has reduced the number of items being purchased. Big retailers that are FedEx customers like Walmart Inc. have also pulled back on orders after they have been stuck with a glut of unsold goods.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »