Week of Oct 7, 2022 Weekly Recap & The Week Ahead

“Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria,” — John Templeton

1. Micron to Spend Up to $100 Billion on Chip Factory in New York State — Micron Technology Inc. has agreed to invest as much as $100 billion to build a semiconductor-manufacturing campus in upstate New York, adding to a wave of chip-making plans in the U.S. as Washington tries to boost domestic manufacturing of those critical components. Micron said a year ago that it would spend as much as $150 billion on additional production capacity, though didn’t say where the new money would go. The company had held off on committing to the spending until the U.S. government had approved billions of dollars in subsidies for domestic chip making. “We will need support from the federal government as well as appropriate support from state governments to bridge the 35% to 45% cost gap that exists in overseas production,” Micron Chief Executive Sanjay Mehrotra said earlier this year.

2. U.S. Job Openings Fell in August, Layoffs Up Slightly — employers’ total job openings fell 10% in August to a seasonally adjusted 10.1 million from 11.2 million the month before, the Labor Department said Tuesday. The 1.1-million drop in openings is the largest decline since the early months of the Covid-19 pandemic in 2020, leaving job openings at their lowest level in a year. Openings dropped the most in healthcare, retail and other services industries. The decline in openings coincided with an August easing of job growth. Employers added 315,000 jobs that month, compared with 526,000 jobs in July. The figures reflect a labor market that is still strong overall, but lost some steam in August after recovering rapidly from the effects of the pandemic.

3. OPEC+ Agrees to Biggest Oil Production Cut Since Start of Pandemic — the Organization of the Petroleum Exporting Countries and its Russia-led allies agreed on Wednesday to slash output by 2 million barrels of oil a day, delegates said, a move likely to push up already-high global energy prices and help oil-exporting Russia pay for its war in Ukraine. The move drew an immediate rebuke from the White House, which called the decision shortsighted and suggested the 23-member group collectively known as OPEC+ was actively supporting Russian President Vladimir Putin. It came less than three months after President Biden visited Saudi Arabia, the OPEC’s de facto leader, in a bid to repair relations between the world’s biggest oil consumer and its biggest crude-oil exporter during a period of rising inflation driven in part by high energy prices.

4. September Jobs Report Shows Payrolls Grew by 263,000 — U.S. employers added 263,000 jobs in September, continuing a gradual cooling pattern in the labor market as high inflation and rising interest rates weighed on the economy. The unemployment rate fell to 3.5% from 3.7% in August, the Labor Department said Friday, matching a half-century low that was last reached in July, a reflection of people leaving the job market. Wages rose 5.0% in September from the same month a year earlier, a slower pace than August’s 5.2% annual rate. Job gains were led by the leisure and hospitality industry, which added 83,000 jobs. Healthcare employment rose 60,000.

The number of job openings fell 10% in August to a seasonally adjusted 10.1 million from 11.2 million the month before, the Labor Department said Tuesday. The 1.1 million drop in openings is the largest decline since the early months of the Covid-19 pandemic in 2020. That left job openings at their lowest level in a year but still above their prepandemic level in 2019, when they averaged 7.2 million a month.

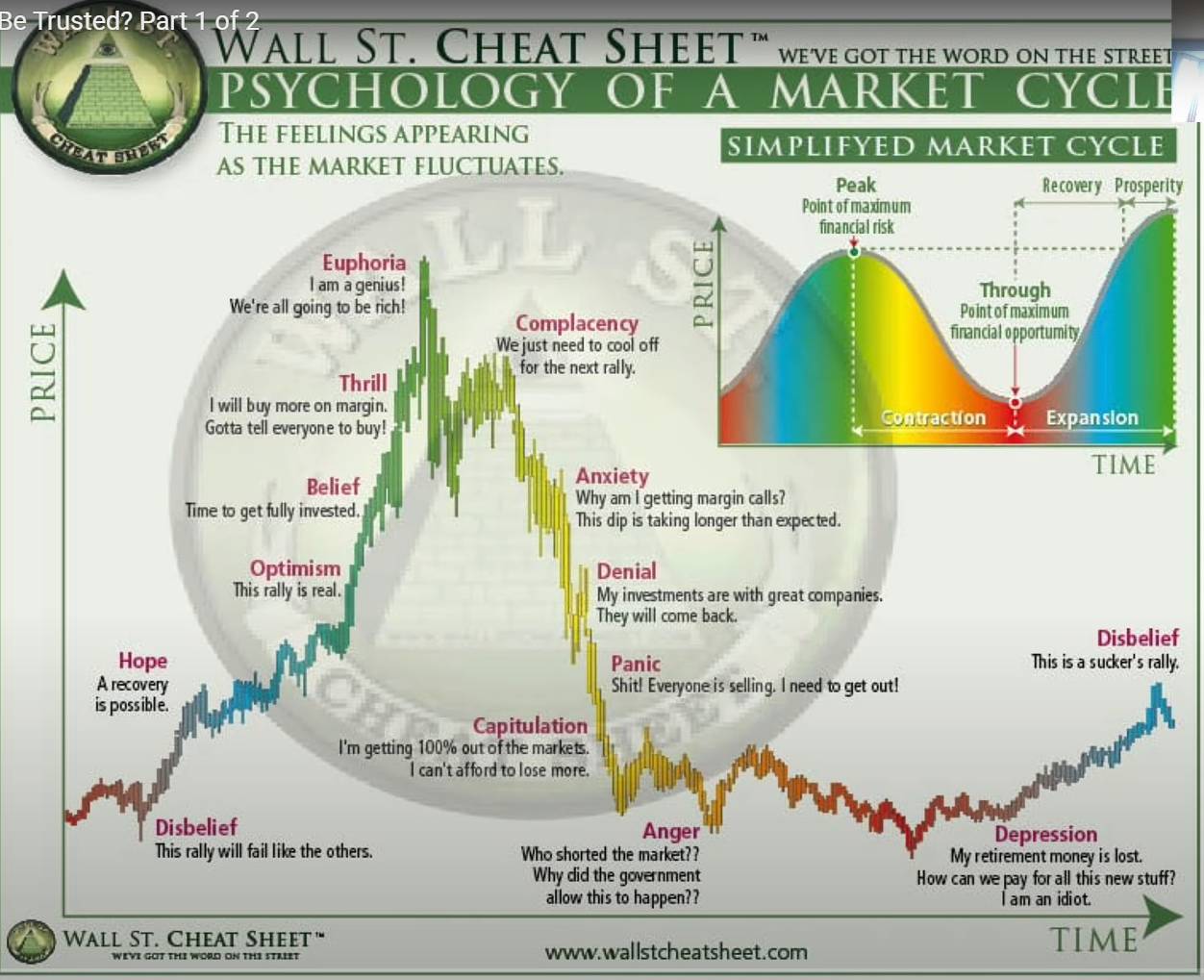

Below is the diagram depicting Stock Market Psychology courtesy of WallStCheatSheet

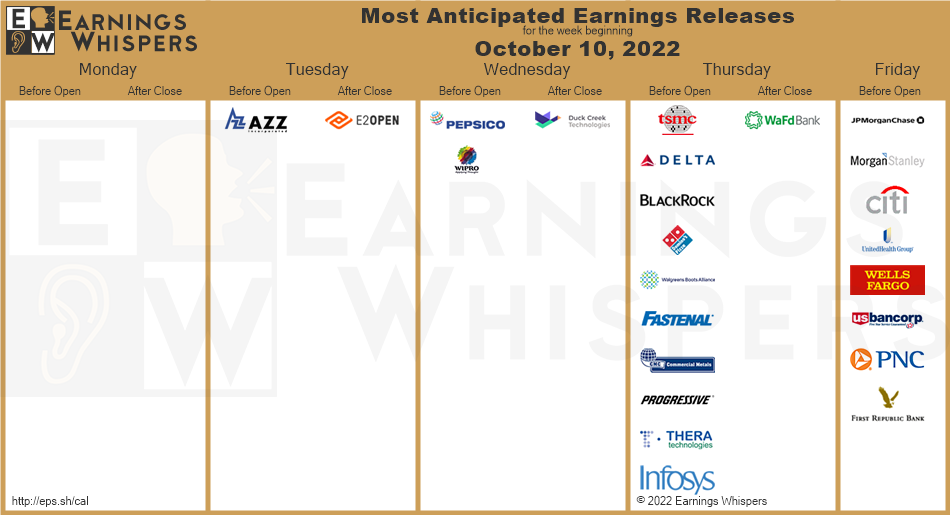

The week ahead — Economic data from Econoday.com: