January 30th, 2023

“Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria,” — Franklin Templeton

1. 4Q GDP up 2.9% in 4Q, Still Risks a Stall in 2023 — Gross domestic product rose at a 2.9% annualized pace, down from 3.2% in the third quarter. A separate report on labor markets published Thursday also pointed to a resilient economy, rather than one on the verge of a slump, with weekly jobless claims unexpectedly falling. For the Fed, which has hiked interest rates at the steepest pace in a generation over the past year, the data suggest that there’s still a path to what’s known as a “soft landing.” That’s a scenario in which tighter monetary policy cools household spending and lowers inflation – but avoids squeezing the economy so hard that it ignites mass layoffs nationwide.

2. Corporate Layoffs Spread Beyond High-Growth Tech Giants — this week, four companies trimmed more than 10,000 jobs, just a fraction of their total workforces. Still, the decisions mark a shift in sentiment inside executive suites, where many leaders have been holding on to workers after struggling to hire and retain them in recent years when the pandemic disrupted workplaces. Unlike Microsoft Corp. and Google parent Alphabet Inc., which announced larger layoffs this month, these companies haven’t expanded their workforces dramatically during the pandemic. Instead, the leaders of these global giants said they were shrinking to adjust to slowing growth, or responding to weaker demand for their products. The U.S. labor market broadly remains strong but has gradually lost steam in recent months. Employers added 223,000 jobs in December, the smallest gain in two years. The Labor Department will release January employment data next week.

3. Consumer Spending Fell 0.2% in December as Inflation Cooled — spending by U.S. households decreased 0.2% in December from the prior month, the Commerce Department said Friday, compared with a downwardly revised 0.1% decrease in November. Households cut spending on goods last month and increased spending slightly on services. The personal-consumption expenditures price index—the Federal Reserve’s preferred gauge of inflation—rose 5% in December from a year earlier, after increasing 5.5% in November.

The core PCE-price index, which captures underlying inflation after removing volatile food and energy prices, rose 4.4% in December from a year earlier—its slowest pace since October 2021. That compared with 4.7% in November. The central bank aims for 2% annual inflation.

4. Tesla Has Become One of the Hottest Stock-Option Trades on Wall Street — Tesla options trading has surged recently: Nearly three million contracts now change hands on an average day, according to Cboe Global Markets data. That is up from 1.5 million a year ago and more than any other stock. Only wagers on the SPDR S&P 500 ETF outpace those on Tesla. Tesla now accounts for roughly 7% of all options trading on an average day, based on Cboe and OCC data. On Jan. 6, the busiest day on record, more than 5.2 million contracts traded, nearly 10% of all options. Activity in Tesla options surpassed volumes tied to the Invesco QQQ exchange-traded fund—which tracks Nasdaq-100 stocks—in December for the first time in nearly two years. And it edged out trading in Apple Inc. options on a sustained basis in July, a notable feat for the S&P 500’s now sixth-largest company by market cap to leapfrog the leader.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 23rd, 2023

“Any idiot can face a crisis – it’s day to day living that wears you out.” – Anton Chekhov

1. US Retail Sales Slide by Most in a Year in Broad-Based Decline — US retail sales fell in December by the most in a year, suggesting consumers are losing some of the resilience that’s kept the economy growing in the face of rapid inflation and steep Federal Reserve interest-rate hikes.

The value of overall retail purchases decreased 1.1% in December after a downwardly revised 1% drop in the prior month, Commerce Department data showed Wednesday. Excluding gasoline and autos, retail sales fell 0.7%. The figures aren’t adjusted for inflation. inflation has shown more consistent signs of slowing in recent months, putting the Fed on track to again slow the pace of interest-rate hikes. The central bank is expected to raise rates by a quarter point when it meets in two weeks.

2. US Producer Price Index Declines by Most Since Start of Pandemic — The producer price index for final demand fell 0.5% last month, the most since April 2020, and was up 6.2% from a year earlier, Labor Department data showed Wednesday. The median estimates in a Bloomberg survey of economists called for the index to fall 0.1% from a month earlier and rise 6.8% from December 2021. The monthly decline was driven by a plunge in goods prices, notably energy and food. Excluding those components, the so-called core PPI rose 0.1% in December and 5.5% from a year earlier.

3. Fed’s Brainard Favors High Rates for Some Time to Cool Inflation — Federal Reserve Vice Chair Lael Brainard said interest rates will need to stay elevated for a period to further cool inflation that’s showing signs of slowing but is still too high. “Even with the recent moderation, inflation remains high, and policy will need to be sufficiently restrictive for some time to make sure inflation returns to 2% on a sustained basis,” Brainard said in prepared remarks for a University of Chicago Booth School of Business event. Brainard said that economic data in the past few months shows cooling consumer demand and wages and tighter financial conditions, all welcome outcomes for policymakers trying to rein in inflation that last year surged to a 40-year high.

4. Treasury Has About $500 Billion of Headroom After Debt Limit Hit — the Treasury Department has about $500 billion of extraordinary measures available that will allow the US to dodge a payments default as Congress works out an agreement on raising the debt limit, which the nation hit late last week.

Treasury Secretary Janet Yellen notified congressional leaders late last week that her department would be deploying two special accounting maneuvers to avoid breaching the debt limit. The Treasury later released a list of the extraordinary measures available, with some figures on how much financial space they offer. The initial two steps taken can free up about $350 billion of extra borrowing authority through early June, according to a Jefferies analysis of data from the department. The initial measures involve changes for two government-run funds for retirees. Later in June, a one-time move would then become available allowing the Treasury to suspend reinvestment in the Civil Service Retirement and Disability Fund, potentially creating an additional $143 billion in headroom, according to the Treasury’s release.

5. U.S. Existing-Home Sales Slid Last Year as Interest Rates Surged — Sales of previously owned homes, which make up most of the housing market, slid 17.8% in 2022 from the prior year to 5.03 million, the National Association of Realtors said Friday. The pandemic-fueled housing boom of 2020 and 2021 carried over to the start of last year. Then the Federal Reserve’s effort to cool the economy and curb inflation by raising interest rates flattened housing-market activity as borrowing rates more than doubled. In October, mortgage interest rates climbed to 7.08%, a two-decade high. More recently, mortgage rates have declined. The average rate on a 30-year fixed mortgage fell to 6.15% this week, the lowest rate since September. Mortgage applications for home purchases rose 25% on a seasonally adjusted basis in the week ended Jan. 13 from the prior week, according to the Mortgage Bankers Association.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 16th, 2023

Most people are driven by greed, fear, envy, and other emotions that render objectivity impossible and open the door for significant mistakes. — Howard Marks

1. World Bank Cuts 2023 Global Growth Projection as Inflation Persists — The bank expects global growth to slow to 1.7% in 2023, down from an estimate of 3% growth in June. That would mark the third-weakest pace of global growth in nearly three decades, overshadowed only by the 2009 and 2020 downturns, according to the World Bank. A separate report showed that global inflation, while starting to cool, remains historically high. The forecast growth rate only narrowly keeps the global economy out of recession territory. The international development organization cited a coalescence of high inflation, rising interest rates, lower investment and Russia’s invasion of Ukraine as threats to growth, along with pandemic-related disruptions in China and stress in its real-estate sector.

2. U.S., Allies Prepare Fresh Sanctions on Russian Oil Industry — In meetings across Europe this week, Treasury officials are discussing the details of the coming sanctions on Russian oil products, which are set to go into effect Feb. 5. The penalties will set two price limits on Russian refined products: one on high-value exports such as diesel and another on low-value ones such as fuel oil, according to people familiar with the plans.

The new limits will follow moves last month by the U.S., European Union and their allies in the Group of Seven advanced democracies to cap the price of Russian crude exports at $60 a barrel. Those sanctions have had a relatively muted impact on global prices, encouraging Western officials who want to pressure Russia’s budget while minimizing volatility in critical global energy markets.

3. U.S. Inflation Slowed for Sixth Straight Month in December — The consumer-price index, a measurement of what consumers pay for goods and services, rose 6.5% last month from a year earlier, down from 7.1% in November and well below a 9.1% peak in June. Core CPI, which excludes volatile energy and food prices, climbed 5.7% in December from a year earlier, easing from a 6% gain in November. Many economists see increases in core CPI as a better signal of future inflation than the overall CPI. Core prices increased at a 3.1% annualized rate in the three months ended in December, the slowest pace in more than a year and down from 7.9% in June.

The figures added to signs that inflation is turning a corner following last year’s surge. They also likely keep the Fed on track to reduce the size of interest-rate increases to a quarter-percentage-point at their meeting that concludes on Feb. 1, down from a half-percentage point increase in December.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 9th, 2023

“Be who you are and say what you feel, because those who mind don’t matter and those who matter don’t mind.” — Bernard Baruch

1. Amazon to Lay Off Over 17,000 Workers, More Than First Planned — the Seattle-based company in November said that it was beginning layoffs among its corporate workforce, with cuts concentrated on its devices business, recruiting and retail operations. At the time, the company expected the cuts would total about 10,000 people, but a person with knowledge of the issue said the number could change, The Wall Street Journal reported. Thousands of those cuts began last year.

2. Fed Minutes Show Officials Feared Markets’ Rallies Could Hinder Inflation Fight –minutes of the Fed’s policy meeting last month, highlighted the tricky communications task that has vexed the central bank over the past six months. The Fed’s rapid rate increases last year have fanned investors’ hopes that inflation will slow quickly over the coming year. In the run-up to the December meeting, longer-term bond yields tumbled, reflecting both optimism about a speedy decline in inflation and fears of a recession this year.

But many Fed officials are anxious they won’t be able to defeat inflation unless they can slow the economy by tightening financial conditions, such as by raising borrowing costs or lowering stock prices.

3. Hiring, Wage Gains Eased in December, Pointing to a Cooling Labor Market in 2023 — after two straight years of record-setting payroll growth following the pandemic-related disruptions, the labor market is starting to show signs of stress. That suggests 2023 could bring slower hiring or outright job declines as the overall economy slows or tips into recession.

Employers added 223,000 jobs in December, the smallest gain in two years, the Labor Department said Friday. Average hourly earnings were up 4.6% in December from the previous year, the narrowest increase since mid-2021, and down from a March peak of 5.6%. All told, employers added 4.5 million jobs in 2022, the second-best year of job creation after 2021, when the labor market rebounded from Covid-19 shutdowns and added 6.7 million jobs. Last year’s gains were concentrated in the first seven months of the year. More recent data and a wave of tech and finance-industry layoffs suggest the labor market, while still vibrant, is cooling.

4. New Alzheimer’s Drug Approved by FDA, Promises to Slow Disease — U.S. health regulators gave early approval to a new Alzheimer’s drug from Eisai Co. and Biogen Inc., the most promising to date in a new class of medicines that may help slow cognitive decline caused by the disease.

The Food and Drug Administration granted conditional approval to the drug, called lecanemab, based on an early study finding it reduced levels of a sticky protein called amyloid from the brains of people with early-stage Alzheimer’s. The companies will sell it under the brand name Leqembi.

Eisai said it would sell the drug at a price of $26,500 a year for the average patient, and that it would be available commercially by Jan. 23. A preliminary report by the Institute for Clinical and Economic Review, a nonprofit that works with drugmakers and insurers to evaluate drug prices, said a fair price would be in the range of $8,500 to $20,600 a year.

2022 Market Recap — below is the highlight of events happened in 2022

2022_Recap_1

2022_Recap_2

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 3rd, 2023

“Happy New Year — wishing our readers a Prosperous, Healthy and Happy New Year — due to a shorten holiday week, no Weekly Recap will be posted”

The staffs at EGS.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

December 27th, 2022

Happy Holidays — below is the quote from 2017 Berkshire Hathaway shareholder letter about market volatility:

“If you can keep your head when all about you are losing theirs …

If you can wait and not be tired by waiting …

If you can think – and not make thoughts your aim …

If you can trust yourself when all men doubt you …

Yours is the Earth and everything that’s in it.”

1. 3Q GDP Revised to 3.2% rate — the U.S. expanded at an annual 3.2% annual rate in the third quarter, a more robust pace of growth than previously reported, new government figures show. The increase in gross domestic product, the official scorecard for the economy, initially was reported at 2.6% and updated to 2.9% last month. A bigger increase in consumer spending, mostly on services such as travel and recreation, accounted for the stronger GDP print in the third quarter.

2. US Home Sales Dropped by a Record 35% in November — Purchases dropped 35% year-over-year, according to a recent report from Redfin, marking the largest decline since the real estate brokerage started collecting data in 2012. A separate report found sales that of previously owned homes fell for a 10th-straight month in November — the longest string of declines dating back to 1999.

The Federal Reserve’s attempts to tamp down inflation this year have brought the housing market to a screeching halt, with high borrowing costs sidelining potential buyers. It’s a drastic shift from the buying frenzy early in the pandemic that prompted bidding wars and drove home values though the roof.

3. Key Inflation Gauge Cools, US Consumer Spending Misses Forecasts — the personal consumption expenditures price index excluding food and energy, which Fed Chair Jerome Powell has stressed is a more accurate measure of where inflation is heading, rose 0.2% in November from a month earlier, Commerce Department data showed. That matched estimates, but data for the prior month were revised higher. From a year earlier, the gauge was up 4.7%, a step down from a 5% gain in October. The overall PCE price index increased 0.1% and was up 5.5% from a year ago, the lowest since October 2021 but still well above the central bank’s 2% goal. Looking ahead, the central bank is expected to continue raising interest rates into next year — to a higher level than many investors had expected — and remain restrictive for some time. As for the size of any February rate hike, Powell said the decision will be based on incoming data, and others for December to be released throughout next month.

Posted in Weekly Summary | No Comments »

December 19th, 2022

“The worst trades are generally when people freeze and start to pray and hope rather than take some action” — Robert Mnuchin

1. CPI Report Shows U.S. Inflation Eased in November — the Labor Department on Tuesday said that its consumer-price index climbed 7.1% in November from a year ago, down sharply from 7.7% in October—building on a trend of moderating price increases since June’s 9.1% peak. Core CPI, which excludes volatile energy and food prices, rose 6% in November from a year ago, easing from a 6.3% gain in October. September’s 6.6% increase was the biggest jump since August 1982. Prices softened significantly on a month-to-month basis. The CPI increased 0.1% in November from the prior month, compared with 0.4% in October. Core CPI rose 0.2% in November, down from 0.3% in October and 0.6% in August and September. The CPI measures what consumers pay for goods and services.

The Fed has raised its benchmark interest rate this year at the fastest pace since the early 1980s to combat inflation. It is expected to announce on Wednesday a 0.5-percentage-point increase, bringing rates to a range between 4.25% and 4.5%, the highest level since December 2007.

2. Bankman-Fried Is Charged With Fraud — U.S. prosecutors on Tuesday charged FTX founder Sam Bankman-Fried with eight counts of fraud and conspiracy, in what they called a scheme to defraud his crypto exchange’s customers and his hedge fund’s lenders. The indictment, brought by the U.S. attorney’s office for the Southern District of New York, accuses him of misappropriating FTX.com customers’ deposits and using those to pay expenses and debts of Alameda Research, his crypto hedge fund. Mr. Bankman-Fried is charged as well with defrauding the U.S. and violating campaign finance rules for conspiring with others to make illegal political contributions. The SEC alleged in its lawsuit that Mr. Bankman-Fried diverted customer funds from the start of his cryptocurrency exchange to support his hedge fund, Alameda Research, and to make venture investments, real-estate purchases and political donations. The arrest charges are the latest bombshells in a case that has transfixed Wall Street and Washington. FTX, one of the largest crypto exchanges in the world, filed for bankruptcy last month after it ran out of cash and rival Binance walked away from a shotgun merger.

3. Fed Raises Rate by 0.5 Percentage Point, Signals More Increases Likely — the Federal Reserve approved an interest-rate increase of 0.5 percentage point and signaled plans to keep raising rates at its next few meetings to combat high inflation. At a news conference, Fed Chair Jerome Powell suggested the central bank would strongly consider dialing down the size of rate rises to a more traditional quarter-percentage-point increment at its next meeting on Jan. 31-Feb. 1. Given how high the Fed raised rates this year, “it’s now not so important how fast we go,” Mr. Powell said. Most officials penciled in plans to raise the rate to between 5% and 5.5% next year, with the median projection implying a further 0.75 percentage point in rate rises. In September, they anticipated lifting it to around 4.6% by the end of next year.

4. Retail Sales Fall Sharply as Shoppers Feel Inflation’s Pinch — Retail sales fell more than expected in November, suggesting that while inflation has started to cool off consumers are still feeling the burden of higher prices, pointing to an inauspicious start to the holiday season.

Retail sales last month fell 0.6% to $689.4 billion, a starker decline than the 0.2% decrease economists had been expecting, according to new data from the Census Bureau. This was the biggest drop in nearly a year, which bodes poorly for retailers as they gear up for the last leg of the holiday season. Excluding autos, sales were down 0.2%, and excluding both auto and fuel sales fell 0.2%. In October, retail sales rose 1.3%.

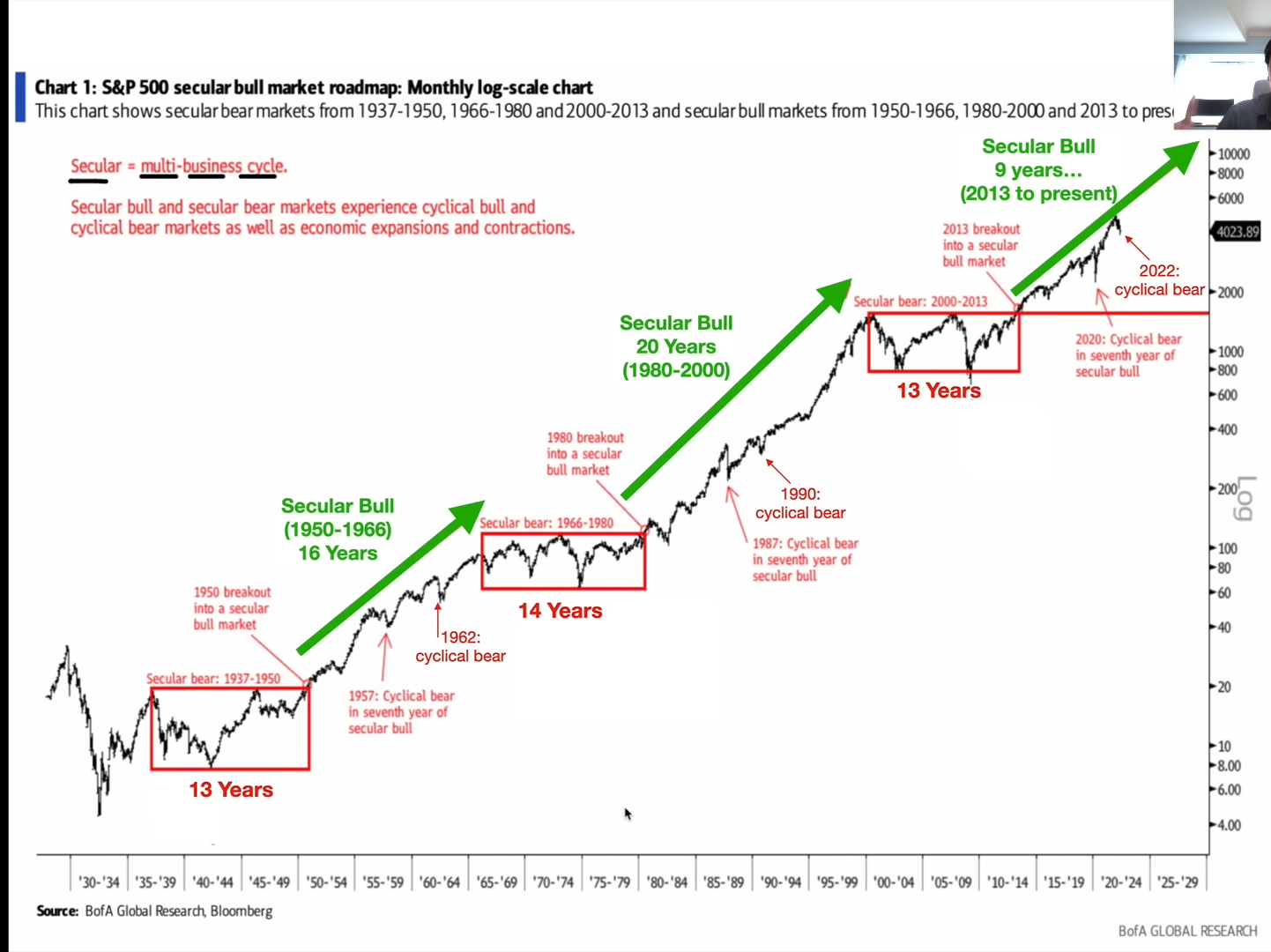

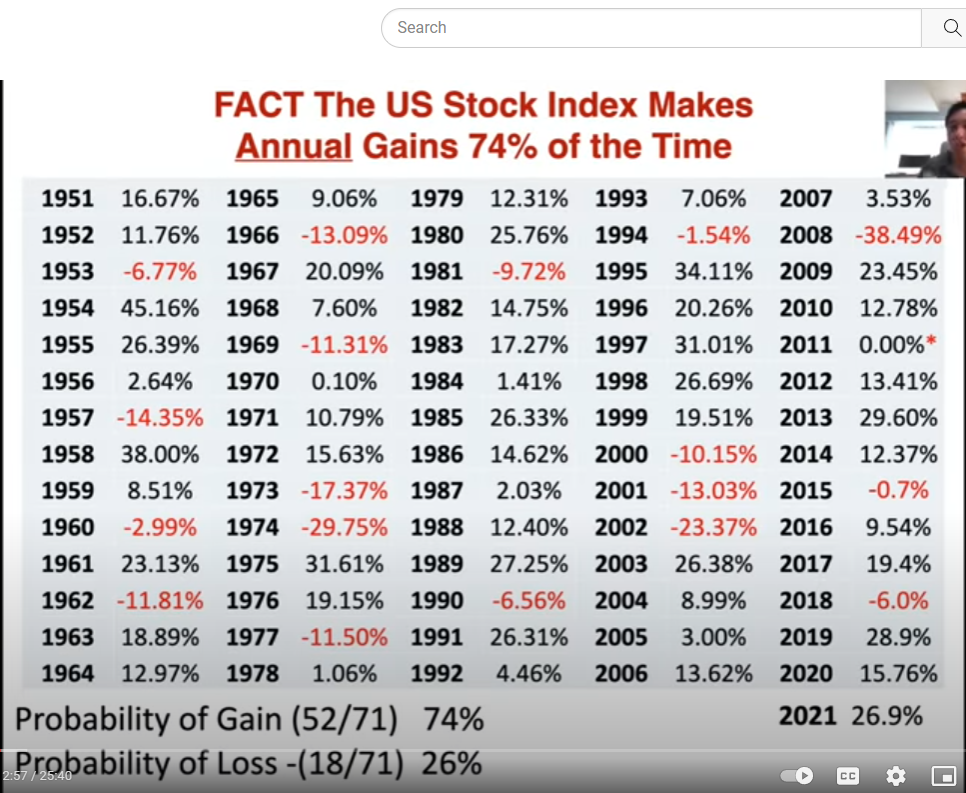

5. S&P 50O Index Secular Bull Market Roadmap Stat from 1929 to Present — table below shows the S&P500 Index returns from 1929 to present courtesy of BofA Research. Note that currently, the S&p500 is in a Bear Market within a Secular Bull.

In addition, from 1951 to present, probability of market gain from a down year is approximately 74%. See the figures posted below.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

December 12th, 2022

“I made my money by selling too soon & never lost money by turning a profit” Bernard Baruch

1. Fed to Weigh Higher Interest Rates Next Year While Slowing Rises This Month — Federal Reserve officials have signaled plans to raise their benchmark interest rate by 0.5 percentage point at their meeting next week, but elevated wage pressures could lead them to continue lifting it to higher levels than investors currently expect.

They have raised rates this year at the fastest pace since the early 1980s, including by 0.75 point at each of their past four meetings to combat inflation. Fed Chair Jerome Powell indicated last week that the central bank was prepared to downshift the size of rate increases at its coming meeting on Dec. 13-14. A smaller 0.5-point increase would mark a new phase of policy tightening as they calibrate how much higher to lift rates. Policy makers expect price pressures to ease meaningfully next year, but brisk wage growth or higher inflation in labor-intensive service sectors of the economy could lead more of them to support raising their benchmark rate next year above the 5% currently anticipated by investors.

2. Continuing US Jobless Claims Rise to Highest Since February — recurring applications for US unemployment benefits rose to the highest since early February, suggesting that Americans who are losing their job are having more trouble finding a new one as the labor market shows tentative signs of cooling.

Continuing claims, which include people who have already received unemployment benefits for a week or more, climbed by 62,000 to 1.7 million in the week ended Nov. 26, Labor Department data showed this week.

3. US Producer Prices Top Estimates, Supporting Fed Hikes Into 2023— the producer price index, a measure of what companies get for their products in the pipeline, increased 0.3% for the month and 7.4% from a year ago, which was the slowest 12-month pace since May 2021. Economists surveyed by Dow Jones had been looking for a 0.2% gain.

Excluding food and energy, core PPI was up 0.4%, also against a 0.2% estimate. Core PPI was up 6.2% from a year ago, compared with 6.6% in October. The hot inflation data keeps the Fed on track for another rate increase, likely a 0.5% hike that would push benchmark borrowing rates to a target range of 4.25%-4.5%. Policymakers have been pushing rates higher in an effort to quell stubborn inflation that has emerged over the past 18 months after being mostly dormant for more than a decade.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

December 5th, 2022

“I skate to where the puck is going to be, not where it has been.” … Wayne Gretzky

1. Home Prices Drop for Third Straight Month as US Market Cools — the US housing market pulled back even more in September, with prices slipping 1.2% from a month earlier.

It was the third straight decline for the seasonally adjusted measure of prices in 20 large US cities, according to the S&P CoreLogic Case-Shiller index. The housing market suddenly started to cool this year, driven in part by higher borrowing costs as the Federal Reserve hiked its benchmark rate to tamp down inflation. The more-than-doubling of mortgage rates this year has sidelined potential buyers and slowed demand, leading sellers to list fewer properties.

2. U.S. GDP grew 2.9% in third quarter — Gross domestic product, the official scorecard for the economy, was revised up from a 2.6% rate of growth in the preliminary reading issued last month. GDP had shrunk in the first two quarters of the year. The economy is forecast to expand again in the fourth quarter running from October to December, but estimates vary from as much as 4% to less than 1%. All figures are adjusted for inflation. The main engine of the economy, consumer spending, increased at a solid 1.7% annual clip in the third quarter, the government said. Previously the increase was put at a softer 1.4%.

— Business spending was weak, however. Investment fell sharply in large structures such as office buildings and oil rigs. The housing market also slumped due to soaring interest rates.

— Corporate profits also fell 1.1% in the third quarter. Adjusted pretax earnings declined to an annualized $2.97 trillion.

3. Powell Says the Fed Is Prepared to Slow the Pace of Rate Hikes in December — Fed Chair Powell emphasized that the Fed would be focused on slower but steadier interest rate increases in the coming months, likely reaching a higher terminal, or peak, rate than had previously been expected and keeping rates elevated for some time.

“It makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down,” Powell said in a speech at the Brookings Institution. “The time for moderating the pace of rate increases may come as soon as the December meeting.” Powell’s remarks come after the Fed has already raised interest rates by 3.75 percentage points this year over the course of six meetings. In each of the last four meetings, the Fed raised rates by 75 basis points, or three-quarters of a percentage point. The goal for the central bank in slowing its pace is to get a feel for what will be an appropriate level after seeing the impact on the broader economy of this year’s rate hikes, Powell said.

4. US Inflation Indicator Rises by Less Than Forecast as Spending Increases — the personal consumption expenditures price index excluding food and energy, which Fed Chair Jerome Powell stressed this week is a more accurate measure of where inflation is heading, rose a below-forecast 0.2% in October from a month earlier, Commerce Department data showed Thursday. The overall PCE price index increased 0.3% for a third month and was up 6% from a year ago, still well above the central bank’s 2% goal.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 28th, 2022

“Throughout my financial career, I have continually witnessed examples of other people that I have known being ruined by a failure to respect risk. If you don’t take a hard look at risk, it will take you.” — Larry Hite

1. Fed Minutes Show Most Officials Favored Slowing Rate Rises Soon — their discussion at the meeting, described in minutes of the gathering released Wednesday, suggests they could downshift to a rate rise of 0.5 percentage point, or 50 basis points at their meeting next month. “A substantial majority of participants judged that a slowing in the pace of increase would soon be appropriate,” the minutes said. Officials approved the fourth consecutive supersize rate increase at their Nov. 1-2 meeting, bringing their benchmark rate to a range between 3.75% and 4%. They are boosting rates at the fastest pace since the early 1980s to reduce inflation that is running near a 40-year high.

All 19 officials at the meeting supported the decision to raise rates this month and broadly agreed they needed to keep lifting them, the minutes showed. Still, the discussion revealed some were more anxious about the possibility of overdoing the increases, while others worried they might not be making enough progress to warrant a downshift.

2. Violent Protests Erupt at Apple’s Main iPhone Plant in China — hundreds of workers at Apple Inc.’s main iPhone-making plant in China clashed with security personnel, as tensions boiled over after almost a month under tough restrictions intended to quash a Covid outbreak. The protest started overnight over unpaid wages and fears of spreading infection, according to the witness, asking to remain anonymous for fear of repercussions. Several workers were injured and anti-riot police arrived on the scene Wednesday to restore order, the person added.

3. China’s Daily Covid Tally Tops 30,000 for First Time as Curbs Spread — China’s daily Covid infections broke through 30,000 for the first time ever as officials struggle to contain outbreaks that have triggered a growing number of restrictions across the country’s most important cities. Rising infections across the country are challenging Chinese authorities who want to shift away from city-wide lockdowns to more targeted measures that are less disruptive to residents and businesses. But after initially easing off on testing and movement restrictions — in line with a new 20-point virus playbook issued by Beijing — officials in some places are again imposing mass testing orders and lockdowns as they strive to meet the overriding objective of suppressing Covid.

That’s meant instead of issuing explicit orders, major cities are locking down apartment block by apartment block and imposing other under-the-radar curbs. In Beijing supermarket delivery apps are being overwhelmed after residents across Chaoyang, its biggest district, were told not to leave their homes unless necessary. Grocery outlets in the district are also no longer taking orders.

4. EU Unveils Proposal to Cap Natural-Gas Prices — the European Union set out the details of a long-debated proposal to cap natural-gas prices on the bloc’s main trading hub, part of an effort to shield consumers from the effects of higher energy costs linked to Russia’s invasion of Ukraine.

The European Commission, the bloc’s executive arm, said that its proposal was designed to deal with exceptional circumstances where the benchmark price for natural gas in Europe exceeds 275 euros, equivalent to about $282, per megawatt hour for two weeks. Prices would also need to be above reference levels by a set margin for 10 consecutive days within those two weeks. The proposal for a price cap, which the commission refers to as a market-correction mechanism, would apply to month-ahead prices on the Title Transfer Facility, a virtual trading hub based in the Netherlands. The commission said over-the-counter trading wouldn’t be affected because it is difficult to monitor and those trades can help in balancing markets.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »