Week of March 28, 2022 Weekly Recap & The Week Ahead

Monday, April 4th, 2022“Accepting losses is the most important investment device to ensure safety of capital” — Gerard Loeb

1. Second Covid-19 Booster Shot Endorsed by FDA, CDC for Adults 50 and Older — the Food and Drug Administration said Tuesday it had cleared extra shots of Pfizer Inc. and its partner BioNTech SE and from Moderna Inc. for adults 50 years and older. The Centers for Disease Control and Prevention followed up by endorsing the second booster shots.

The extra doses are “especially important for those 65 and older and those 50 and older with underlying medical conditions that increase their risk for severe disease from Covid-19 as they are the most likely to benefit from receiving an additional booster dose at this time,” CDC Director Rochelle Walensky said.

2. Shanghai Lockdown Adds to China’s Economic Woes — the lockdown of one of China’s largest and most prosperous cities is the latest blow to the country’s economic fortunes, adding new risks to Beijing’s ambitious growth target in a politically sensitive year for leader Xi Jinping. The economic toll is only starting to come into view. Production at Shanghai-area factories operated by electric-vehicle maker Tesla Inc. and some other companies has been halted while domestic logistics networks have jammed up, slowing global supply chains, according to exporters and business owners. Meanwhile, hundreds of restaurants, retailers and other service-sector businesses have been shut down temporarily. The megacity of more than 25 million people, which accounts for roughly 4% of China’s total economic output and which is home to the country’s largest port and the regional headquarters of hundreds of multinational companies, initially sought to avoid a citywide lockdown. Instead, it systematically tested residents while blocking off some office towers in a bid to minimize disruptions to the economy and people’s daily lives, in line with Mr. Xi’s call this month “to achieve the biggest prevention and control effect with the smallest cost.”

3. Biden Considers Invoking Defense Production Act to Boost Minerals for EV Batteries — President Biden is considering invoking the Defense Production Act as soon as this week to boost domestic production of minerals used in batteries needed for electric vehicles, a person familiar with his plans said. The administration would include minerals like lithium, nickel and graphite, cobalt and manganese under the Korean War-era national security mobilization law, the person said. The designation could help mining companies access government funding for feasibility studies on mining development, productivity and safety improvements, or on how to wring more of these metals out of ore already produced at facilities operating in the U.S. It could also prompt Congress to dedicate more money to such efforts, the person said.

4. Biden to Draw Down Oil Reserves in Bid to Ease Gas Prices — President Biden will tap up to 180 million barrels of government oil reserves to help tamp down near-record high fuel prices, an unprecedented government intervention into oil markets following Russia’s invasion of Ukraine. In remarks from the White House late last week, Mr. Biden framed high energy prices as a wartime issue that requires a robust and wide-ranging response. The oil release—about 1 million barrels a day for six months starting in May—would be the Biden administration’s third, and by far the biggest-ever drawdown from the country’s emergency stockpile of roughly 568 million barrels.

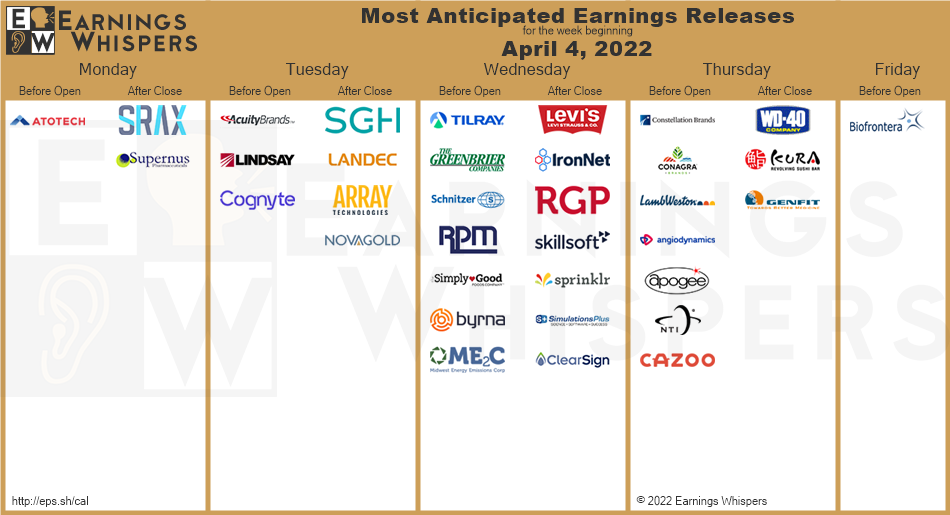

The week ahead — Economic data from Econoday.com: