Week of Oct 28, 2022 Weekly Recap & The Week Ahead

Wednesday, November 2nd, 2022THERE WILL NOT BE ANY POSTING FOR THE WEEK OF OCT 28 2022 — WE ARE AWAY FOR THE LONG WEEKEND.

The week ahead — Economic data from Econoday.com:

| Market Outlook |

| Equity Guidance Blog — Financial Market Overview |

THERE WILL NOT BE ANY POSTING FOR THE WEEK OF OCT 28 2022 — WE ARE AWAY FOR THE LONG WEEKEND.

The week ahead — Economic data from Econoday.com:

“It is not the strongest or the most intelligent who will survive but those who can best manage change.” – Charles Darwin

1. Home Construction Fell 8.1% in September — new home construction fell 8.1% in September, a sign that higher mortgage rates continue to cut into buyer demand and depress new building. Housing starts, which measure the beginning of construction on a new home, fell to a seasonally-adjusted annual rate of 1.44 million in September, 8.1% below the revised August estimate of 1.56 million and 7.7% below the September 2021 rate, according to Census Bureau and Department of Housing and Urban Development data released today. Consensus estimates gathered by FactSet had anticipated homes to have been started at a rate of about 1.47 million.

2. Fed’s Beige Book Says Businesses Expect Economy to Weaken — the Fed’s 12 regional reserve-bank districts said business contacts noted “growing concerns about weakening demand,” according to the central bank’s latest compilation of economic anecdotes from around the country, known as the Beige Book. Businesses reported that price pressures remained elevated through early October with some cost increases moderating. “Declines in commodity, fuel, and freight costs were noted,” the report said.

3. U.S. Home Sales Dropped for Eighth Straight Month in September — Sales of previously owned homes declined 1.5% in September from the prior month to a seasonally adjusted annual rate of 4.71 million, the weakest rate since May 2020, the National Association of Realtors said Thursday. September sales fell 23.8% from a year earlier. Existing-home sales have dropped 27% from their recent peak in January as the Federal Reserve’s actions to increase interest rates have pushed many prospective home buyers out of the market.

Some buyers no longer qualify for mortgages at current rates, while others have stepped back from the market due to broader uncertainty about the economy, real-estate agents say. Many current homeowners have mortgage rates below 4%, and some prospective sellers are opting to stay put rather than sell their homes and buy new ones with higher borrowing costs.

4. US Budget Deficit Plunges to $1.38 Trillion as Pandemic Aid Unwinds — The deficit for the fiscal year through September narrowed to $1.38 trillion, from a revised $2.78 trillion the previous year, according to US Treasury Department data released late last week. The deficit reduction came even after the Treasury accounted for President Joe Biden’s move to forgive a swath of student loans. The department said loan modifications had a $430 billion impact on the month of September, a sharp increase from the $137 billion recognition of such costs in September 2021. The Treasury said that it didn’t anticipate further such large-scale hits to the budget from the loan-forgiveness move in subsequent months.

FISCAL 2022 FISCAL 2021

Revenue $4.896 trillion $4.046 trillion

Outlays $6.272 trillion $6.822 trillion

Deficit $1.375 trillion $2.776 trillion

Deficit as % of GDP 5.5% 12.3%

The week ahead — Economic data from Econoday.com:

“If you want to be the best, you have to do things that other people are unwilling to do. —Michael Phelps

1. Bank of England Further Expands Bond-Market Rescue to Restore U.K.’s Financial Stability — the Bank of England extended support targeted at pension funds for the second day in a row, the latest attempt to contain a bond-market selloff that has threatened U.K. financial stability. The turmoil sparked fresh demands for pension funds to come up with cash to shore up LDIs, or liability-driven investments, derivative-based strategies that were meant to help match the money they owe to retirees over the long term.

LDIs were at the root of the bond selloff that prompted the BOE’s original intervention. Pension plans in late September saw a wave of margin calls after Prime Minister Liz Truss’s government announced large, debt-funded tax cuts that fueled an unprecedented bond-market selloff.

2. Fed Minutes Show Policy Pivot Is Not Coming Soon — the minutes noted “broad-based and unacceptably high level of inflation,” and said risks to the inflation outlook are increasing. Many participants emphasized that the cost of taking too little action against inflation outweighed the cost of doing too much, and several underlined the need to maintain a restrictive stance for as long as necessary. A couple of those officials stressed that historical experience demonstrated the danger of prematurely ending periods of tight monetary policy designed to bring down inflation.

3. Core US Inflation Rises to 40-Year High — the core consumer price index, which excludes food and energy, increased 6.6% from a year ago, the highest level since 1982, Labor Department data showed Thursday. From a month earlier, the core CPI climbed 0.6% for a second month. The advance was broad based. Shelter, food and medical care indexes were the largest of “many contributors,” the report said. Prices for gasoline and used cars declined. The CPI report is the last one before next month’s US midterm elections and poses fresh challenges to President Joe Biden and Democrats as they seek to retain thin congressional majorities. Already, the surge in inflation has posed a serious threat to those prospects.

4. U.K. Prime Minister Liz Truss Fires Treasury Chief, U-Turns on Taxes — U.K. Prime Minister Liz Truss fired Treasury chief Kwasi Kwarteng and reversed crucial parts of her government’s tax cuts, after her plans to jolt the economy into growth unraveled in spectacular fashion following a backlash from financial markets and her party. In a scramble to shore up support within her party, the embattled Ms. Truss also ditched her plan to prevent a planned rise in the rate of corporate income tax next April to 25% from 19%—a move taken by predecessor Boris Johnson’s government to help shore up finances. The U-turn was the second major part of her tax-cutting package to be abandoned recently. The turmoil in the U.K. is a sharp reminder of the political and economic challenges facing leaders across the West as they grapple with fast-rising inflation and weak growth. Price increases are forcing central banks to quickly raise interest rates, denting economic growth and making financial markets far more sensitive to deficits and debt.

The week ahead — Economic data from Econoday.com:

“Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria,” — John Templeton

1. Micron to Spend Up to $100 Billion on Chip Factory in New York State — Micron Technology Inc. has agreed to invest as much as $100 billion to build a semiconductor-manufacturing campus in upstate New York, adding to a wave of chip-making plans in the U.S. as Washington tries to boost domestic manufacturing of those critical components. Micron said a year ago that it would spend as much as $150 billion on additional production capacity, though didn’t say where the new money would go. The company had held off on committing to the spending until the U.S. government had approved billions of dollars in subsidies for domestic chip making. “We will need support from the federal government as well as appropriate support from state governments to bridge the 35% to 45% cost gap that exists in overseas production,” Micron Chief Executive Sanjay Mehrotra said earlier this year.

2. U.S. Job Openings Fell in August, Layoffs Up Slightly — employers’ total job openings fell 10% in August to a seasonally adjusted 10.1 million from 11.2 million the month before, the Labor Department said Tuesday. The 1.1-million drop in openings is the largest decline since the early months of the Covid-19 pandemic in 2020, leaving job openings at their lowest level in a year. Openings dropped the most in healthcare, retail and other services industries. The decline in openings coincided with an August easing of job growth. Employers added 315,000 jobs that month, compared with 526,000 jobs in July. The figures reflect a labor market that is still strong overall, but lost some steam in August after recovering rapidly from the effects of the pandemic.

3. OPEC+ Agrees to Biggest Oil Production Cut Since Start of Pandemic — the Organization of the Petroleum Exporting Countries and its Russia-led allies agreed on Wednesday to slash output by 2 million barrels of oil a day, delegates said, a move likely to push up already-high global energy prices and help oil-exporting Russia pay for its war in Ukraine. The move drew an immediate rebuke from the White House, which called the decision shortsighted and suggested the 23-member group collectively known as OPEC+ was actively supporting Russian President Vladimir Putin. It came less than three months after President Biden visited Saudi Arabia, the OPEC’s de facto leader, in a bid to repair relations between the world’s biggest oil consumer and its biggest crude-oil exporter during a period of rising inflation driven in part by high energy prices.

4. September Jobs Report Shows Payrolls Grew by 263,000 — U.S. employers added 263,000 jobs in September, continuing a gradual cooling pattern in the labor market as high inflation and rising interest rates weighed on the economy. The unemployment rate fell to 3.5% from 3.7% in August, the Labor Department said Friday, matching a half-century low that was last reached in July, a reflection of people leaving the job market. Wages rose 5.0% in September from the same month a year earlier, a slower pace than August’s 5.2% annual rate. Job gains were led by the leisure and hospitality industry, which added 83,000 jobs. Healthcare employment rose 60,000.

The number of job openings fell 10% in August to a seasonally adjusted 10.1 million from 11.2 million the month before, the Labor Department said Tuesday. The 1.1 million drop in openings is the largest decline since the early months of the Covid-19 pandemic in 2020. That left job openings at their lowest level in a year but still above their prepandemic level in 2019, when they averaged 7.2 million a month.

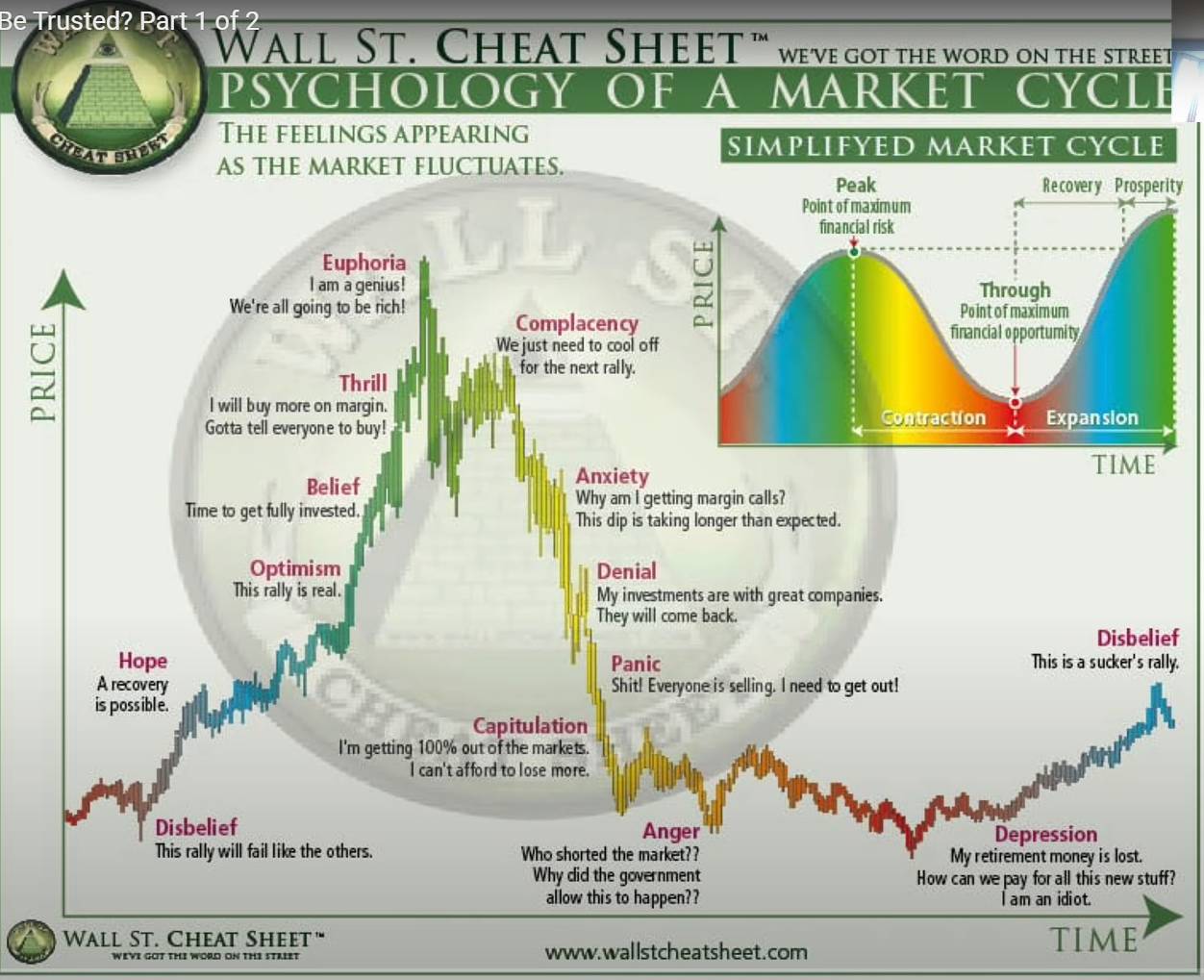

Below is the diagram depicting Stock Market Psychology courtesy of WallStCheatSheet

The week ahead — Economic data from Econoday.com:

“There is nothing new in Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again. – Jesse Lauriston Livermore

1. Bank of England Buys Bonds in Bid to Stop Spread of Crisis — the Bank of England launched an emergency intervention to restore order in bond markets after a government tax-cut plan sent borrowing costs soaring and triggered a meltdown in complex financial instruments held by pension funds. The move aimed to stanch the damage from a furious selloff in U.K. government debt in recent days and stop the losses from running out of control, analysts said. The bank said it offered to buy £5 billion of bonds late last week (equivalent to $5.4 billion) but only took in £1 billion, indicating a limited amount of firepower was required to move markets.

2. Home Prices Suffer First Monthly Decline in Years — U.S. home prices slid in July from June, the first monthly decline in years and the latest sign that higher mortgage rates are starting to weigh on home prices in many of the country’s biggest markets. The S&P CoreLogic Case-Shiller National Home Price Index, which measures the average change in home prices across the nation, fell 0.3% in July from June, the first month-over-month decline since January 2019. On a seasonally adjusted basis, the national index fell 0.2%. That was the first monthly decline in more than a decade by this measure. The average rate on a 30-year fixed-rate mortgage was 6.29% in the week ended Sept. 22, up from 2.88% a year earlier, according to housing-finance agency Freddie Mac.

3. Mortgage Rates Rise to 6.7%, Highest Since 2007 — mortgage rates rose to their highest level in more than 15 years, a new high since the 2008-09 financial crisis that adds pressure to the already cooling U.S. housing market. The average rate on a 30-year fixed mortgage climbed to 6.7%, according to a survey of lenders released Thursday by Freddie Mac. lt was the highest rate since July 2007 and marked the sixth week in a row of rising rates. A year ago, rates were 3.01%.

The surge in mortgage rates follows a series of interest-rate increases from the Federal Reserve. The central bank has moved aggressively to try to cool the highest inflation in decades, raising its benchmark rate five times this year. Officials have indicated more increases are likely in the months ahead.

4. U.S. Jobless Claims Hit Lowest Level in Five Months — initial jobless claims, a proxy for layoffs, decreased to a seasonally adjusted 193,000 last week from a revised 209,000 the previous week, the Labor Department said Thursday. The total was the lowest since late April and below the prepandemic average of 218,000 in 2019, when the labor market was also tight. The Commerce Department separately said inflation in the second quarter was higher than previously estimated, pointing to the difficulties the Federal Reserve faces in tamping down persistent price increases that have spread through the economy. The department didn’t revise its estimate that the U.S. economy, as measured by gross domestic product, contracted 0.6% in the April to June period, however. Consumer spending was stronger than previously estimated, it said, but revised estimates of U.S. exports and inventories offset the improved spending picture.

The week ahead — Economic data from Econoday.com:

“Markets are never wrong – opinions often are.” — Jesse Livermore

1. U.S. Home Sales and Prices Fell in August as Mortgage Rates Rose — sales of previously owned homes dropped 0.4% in August from July to a seasonally adjusted annual rate of 4.8 million, the weakest rate since May 2020, the National Association of Realtors said Wednesday. August sales fell 19.9% from a year earlier.

The housing market has slowed in recent months—with seven months of monthly sales declines through August—as the Federal Reserve aggressively raises interest rates to cool the economy and bring down high inflation. That has led to higher mortgage-interest rates and increased borrowing costs for home buyers by hundreds of dollars a month, pushing many out of the market. The average rate on a 30-year fixed-rate mortgage was 6.02% in the week ended Sept. 15, up from 2.86% a year earlier, according to housing-finance agency Freddie Mac.

2. Fed Raises Interest Rates by 0.75 Percentage Point for Third Straight Meeting — the Federal Reserve approved its third consecutive interest-rate rise of 0.75 percentage point and signaled additional large increases were likely at coming meetings as it combats inflation that remains near a 40-year high.

The decision Wednesday—unanimously supported by the Fed’s 12-member rate-setting committee—will lift its benchmark federal-funds rate to a range between 3% and 3.25%, a level last seen in early 2008. Most of the 19 officials who participated at the Fed’s policy meeting expect to lift the rate at least by another 1.25 percentage point by December, to a range between 4.25% and 4.5%, according to their new projections latest release. The Fed has two more meetings this year.

3. A Day After Fed Raises Rates, Reverse Repos Hit New Record — the Federal Reserve Bank of New York said that a day after the U.S. central bank pushed up its short-term target rate by a large 0.75 percentage point to between 3% and 3.25%, money-market funds and others parked a record $2.359 trillion at the New York Fed’s reverse repo facility. The facility last saw a record inflow on June 30, at $2.329 trillion. That surge came at the end of a quarter, often a time where the reverse repo facility pulls in a significant amount of money due to temporary market factors. The Fed’s reverse repo tool takes in cash, primarily from money-market funds. It is designed to help set a lower end for short-term interest rates. After the Fed’s rate rise Wednesday, the rate now stands at 3.05%, up from 2.30% in place before the Fed lifted rates.

The Fed uses another tool, called the interest on reserves balances rate, now at 3.15%, to set a high end for short-term rates. Together, both rates drive the market-based setting of the federal-funds rate, the central bank’s primary tool to achieve its inflation and job mandates.

4. Oil Falls Below $80 a Barrel — U.S. oil prices fell below $80 a barrel for the first time since January, dragged down by mounting fears of a global recession and a rapidly strengthening U.S. dollar. West Texas Intermediate crude futures dropped 5.7% to close at $78.74. The main U.S. oil price is down about 36% from its June peak and nearly to where it began the year. Brent crude, the global benchmark, shed 4.8% Friday to end at $86.15. Behind the slide: A string of major central banks—including the Federal Reserve, the Bank of England, the Swiss National Bank and Norway’s Norges Bank—raised interest rates this week. Tightening financial conditions on a near-global basis have ratcheted up fears about a widespread economic slowdown, which would also mean lower energy demand. Business surveys Friday indicated that economic activity in Europe declined sharply in September.

The week ahead — Economic data from Econoday.com:

“Every battle is won or lost before it’s ever fought” – Sun Tzu

1. U.S. Inflation Remained High in August — the Labor Department on Tuesday reported its consumer-price index rose 8.3% in August from the same month a year ago, down from 8.5% in July and from 9.1% in June, which was the highest inflation rate in four decades. The CPI measures what consumers pay for goods and services. So-called core CPI, which excludes often volatile energy and food prices, increased 6.3% in August from a year earlier, up markedly from the 5.9% rate in both June and July—a signal that broad price pressures strengthened.

On a monthly basis, the core CPI rose 0.6% in August—double July’s pace. Investors and policy makers follow core inflation closely as a reflection of broad, underlying inflation and as a predictor of future inflation.

2. Mortgage Rates Hit 6.02%, Highest Since the Financial Crisis — per WSJ, the average rate on a 30-year fixed mortgage climbed to 6.02% this week, up from 5.89% last week and 2.86% a year ago, according to a survey of lenders released late last week by mortgage giant Freddie Mac. The last time rates were this high was in the heart of the financial crisis in 2008, when the U.S. was deep in recession. The jump in mortgage rates is one of the most pronounced effects of the Federal Reserve’s campaign to curb inflation by lifting the cost of borrowing for consumers and businesses. Already, it has ushered in a sea change in the housing market by adding hundreds of dollars or more to the monthly cost of a potential buyer’s mortgage payment, slowing what was a red-hot market not so long ago. Higher rates are forcing some would-be buyers to continue renting. Other buyers are skimping elsewhere to make their mortgage payments.

3. U.S. Retail Sales Rose 0.3% in August, Showing Resilience in Face of Inflation — according to WSJ, U.S. consumers spent at a steady pace in August as gasoline prices fell, with purchases of vehicles and back-to-school items like clothing driving the gain. Retail sales, a measure of spending at stores, online and in restaurants, rose 0.3% in August from the prior month, the Commerce Department said Thursday. July spending was revised down to a 0.4% decline from a previous flat reading.

Much of August’s gain was due to higher spending on vehicles, with purchases at motor vehicle and parts dealers up 2.8% on the month. A measure of spending that strips out vehicle sales declined 0.3% from July. Stripping out both vehicle and gasoline spending, retail sales rose 0.3%.

4. FedEx Stock Tumbles After Warning on Economic Trends — The delivery giant’s shares lost 21% Friday—its biggest one-day percentage drop ever—after the company said a macroeconomic slowdown had led to lower volumes of goods moving around the world in recent weeks. FedEx and rival United Parcel Service Inc. have confronted lower volumes of packages this year as a pandemic boom in online shopping cools. Consumers have switched more of their spending to travel and entertainment, plus high inflation has reduced the number of items being purchased. Big retailers that are FedEx customers like Walmart Inc. have also pulled back on orders after they have been stuck with a glut of unsold goods.

The week ahead — Economic data from Econoday.com:

“The stock market is never obvious. It is designed to fool most of the people, most of the time- Jesse Livermore” ― Jesse Livermore

1. Liz Truss to Become Next U.K. Prime Minister, Succeeding Boris Johnson — U.K. Foreign Secretary Liz Truss won the race to lead the ruling Conservative Party and become Britain’s next prime minister, taking the helm of a nation heading into an economic storm. The new prime minister faces a daunting array of challenges. The U.K. economy is spiraling toward recession as inflation ramps up. Ms. Truss has only a narrow base of loyalists within the Conservative Party and polls show limited support for her across the country at-large.

2. U.S. Plans Shift to Annual Covid Shots as New Boosters Roll Out — U.S. health authorities plan to recommend that people get Covid-19 boosters once a year, starting with the new shots now rolling out, a shift from their current practice of issuing new advice every several months.

The annual cadence would be similar to that of flu shots, White House officials said Tuesday, though elderly people and those with weakened immune systems may need more frequent inoculations. To date, health authorities had recommended the extra doses based on the ebbs and flows of the virus’s evolution and new insights into people’s waning immunity. Yet the authorities wound up making recommendations for booster doses to different groups every several months.

3. Fed on Path for Another 0.75-Point Interest-Rate Lift After Powell’s Inflation Pledge — the Federal Reserve appears to be on a path to raise interest rates by another 0.75 percentage point this month in the wake of Chairman Jerome Powell’s public pledge to reduce inflation even if it increases unemployment. St. Louis Fed President James Bullard said in an Aug. 18 interview he was leaning in favor of a 0.75-point rate increase at the coming Fed meeting. “We should continue to move expeditiously to a level of the policy rate that will put significant downward pressure on inflation,” he said. Fed officials have raised rates this year at the fastest clip since the early 1980s, taking their benchmark federal-funds rate from near zero in March to a range between 2.25% and 2.5% in July.

4. ECB Raises Interest Rates by a Historic 0.75 Point as Europe Stares at Recession — the ECB Bank said in a statement that it would increase its key rate to 0.75% from zero—its second hike this year following a 50-basis-point rise in July—and signaled that further rises were likely this year. The increase mirrors recent moves by other major central banks, including the Federal Reserve, which is expected to unveil a third successive 0.75-point rate rise later this month. Canada’s central bank raised its policy rate on Wednesday by 0.75 percentage point to 3.25%, a 14-year high.

Rising borrowing costs will likely increase the risk of a slide into recession for Europe’s currency union, which is wrestling with surging energy costs and sagging confidence among households and businesses, driven by the war in neighboring Ukraine. With governments piling on debt to shield consumers and businesses from the impact of rising prices, a national election in Italy later this month could exacerbate strains in the region’s bond markets.

5. Queen Elizabeth II, Longest-Reigning British Monarch, Dies — Queen Elizabeth II, the longest-reigning monarch in British history and a symbol of stability in an era of sweeping social and political change, has died at age 96. During her seven decades on the throne, the British Empire was dismantled and the U.K.’s role in the world shrank dramatically. Growing pressure for independence in Scotland and arguments for Irish unification threatened to redraw the U.K.’s own borders, and ruptures within her family raised questions about the monarchy’s future role.

But at the end, Queen Elizabeth remained head of state of 14 countries in addition to the U.K., and the leader of a Commonwealth that now includes 54 countries with a combined population of over two billion people. The new monarch is her eldest son, Charles, whose son, William, becomes next in line for the throne.

The week ahead — Economic data from Econoday.com:

THERE WILL NOT BE ANY POSTING FOR THE WEEK OF SEPT 2ND 2022 — WE ARE AWAY FOR THE LONG WEEKEND.

The week ahead — Economic data from Econoday.com:

“You don’t need to trade often. If you can catch one or two moves to the targets during the day with good size, you can make a good living and keep trading costs down” — unknown

1. Covid-19 Booster Campaign Is Expected to Launch Next Month — the Biden administration has completed plans for a fall Covid-19 booster campaign that would launch in September with 175 million updated vaccine doses provided to states, pharmacies and other vaccination sites.

The administration is procuring the doses, which drugmakers are updating to target the newest versions of the virus. The administration has also informed states, pharmacies and other entities they can begin preordering now through the end of August, according to the administration’s fall vaccination planning guide.

2. Biden’s Student Loan Forgiveness Plan to Cancel Up to $20,000 in Debt for Millions — President Biden will forgive up to $20,000 in federal student loan debt for tens of millions of Americans, a move that will provide unprecedented relief for borrowers but is certain to draw legal challenges and political pushback. Following more than a year of internal debate, the president said Wednesday that he will cancel $10,000 in federal student loan debt for borrowers making under $125,000 a year or couples making less than $250,000 a year. In addition, those who receive federal Pell Grants and make less than $125,000 a year would be eligible for total forgiveness of $20,000.

3. Mortgage Rates Rise to Two-Month High at 5.55% — the average rate on a 30-year fixed mortgage climbed to 5.55% this week, according to a Freddie Mac survey of lenders released Thursday. That is nearly double the rate on offer a year ago, though it is down slightly from June levels, which were the highest since 2008.

The higher mortgage rate is causing some prospective buyers to shelve purchase plans, real-estate agents say, because it adds hundreds of dollars or more to the monthly cost of owning a home. Sales of existing U.S. homes fell for a sixth straight month in July, the longest stretch of declines in over eight years. Elevated mortgage rates are also posing a financial threat to mortgage companies that revolve around refinancing homeowners into lower-rate loans. Some lenders are losing money, laying off employees or closing shop.

4. Fed Chair Powell Warns Rates Are Going to Stay High for Some Time — Federal Reserve Chair Jerome Powell signaled the US central bank is likely to keep raising interest rates and leave them elevated for a while to stamp out inflation, and he pushed back against any idea that the Fed would soon reverse course.

“Restoring price stability will likely require maintaining a restrictive policy stance for some time,” Powell said Friday in remarks at the Kansas City Fed’s annual policy forum in Jackson Hole, Wyoming. “The historical record cautions strongly against prematurely loosening policy.” He said restoring inflation to the 2% target is the central bank’s “overarching focus right now” even though consumers and businesses will feel economic pain. He reiterated that another “unusually large” increase in the benchmark lending rate could be appropriate when officials gather next month, though he stopped short of committing to one.

The week ahead — Economic data from Econoday.com:

© Copyright 2026 Market Outlook All Rights Reserved

Design by EGS

Sponsored by Equity Guidance LLC