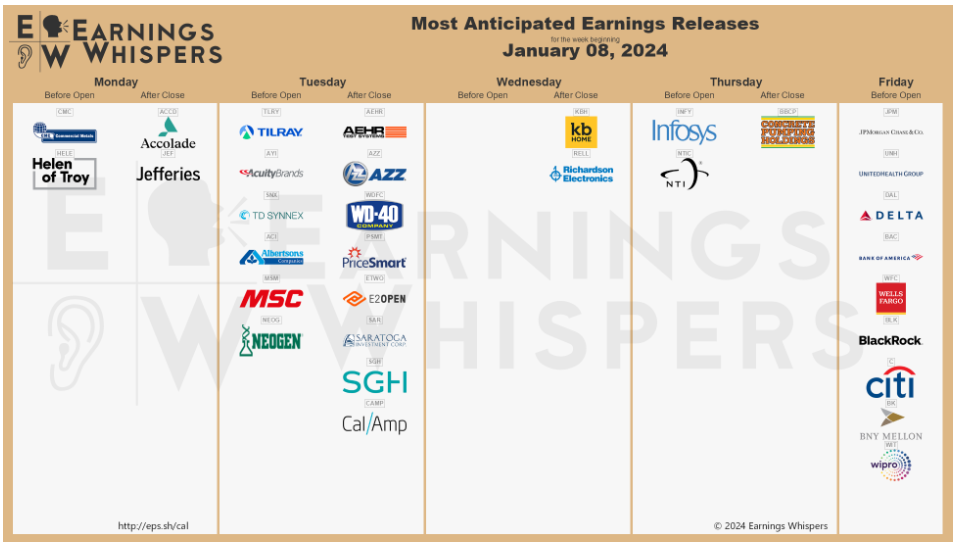

Week of Jan 12, 2024 Weekly Recap & The Week Ahead

Tuesday, January 16th, 2024“It takes character to sit there with all that cash and do nothing. I didn’t get to where I am by going after mediocre opportunities.” — Charles Munger

1. SEC Authorizes Bitcoin-Spot ETFs in Crypto’s Big Breakthrough — US regulators for the first time approved exchange-traded funds that invest directly in Bitcoin, a move heralded as a landmark event for the roughly $1.7 trillion digital-asset sector that will broaden access to the largest cryptocurrency on Wall Street and beyond. The Securities and Exchange Commission, whose three-part mandate includes investor protection, authorized funds from industry heavyweights BlackRock, Invesco and Fidelity to smaller competitors including Valkyrie to begin trading late last week.

The approvals also mark a rare capitulation by the SEC following opposition that lasted for more than a decade, ever since Tyler and Cameron Winklevoss first proposed a Bitcoin ETF in 2013. BlackRock Inc.’s surprise application last June, followed by an appeals court ruling that called the denial of a different application “arbitrary and capricious,” triggered a blistering rally in the cryptocurrency as speculation that US regulators would finally give their blessing to the structure.

2. Inflation Edged Up in December After Rapid Cooling Most of 2023 — The consumer-price index climbed 0.3% in December from the prior month and increased 3.4% from a year earlier, the Labor Department said Thursday. That compares with November’s 0.1% monthly gain and marks an acceleration from that month’s 3.1% annual increase. Core prices, which strip out volatile food and energy items, rose 0.3% in December from the prior month—the same monthly increase as November and slightly faster than would be consistent with the Federal Reserve’s long-term inflation target of 2%. Core prices increased 3.9% from a year earlier, a modest slowing from November’s 4% annual increase. Thursday’s report isn’t likely to change the Fed’s near-term policy outlook.

3. PPI report shows U.S. wholesale prices declining for a third straight month — the decline in wholesale inflation last month offers a bit of relief after a hotter-than-expected increase in the consumer price index. The CPI posted the biggest gain in December in three months. A separate measure of “core” wholesale prices that strips out volatile food, energy and trade margins rose a mild 0.2%% last month, the government said. That matched the Wall Street forecast. The cost of goods fell 0.4% in December because of another decline in energy prices. Food prices also fell. The cost of wholesale services, where inflation is running the hottest, was flat in December.

4. SEC Approves Bitcoin ETFs for Everyday Investors — The SEC decision clears the way for the first U.S. exchange-traded funds that hold bitcoin to be sold to the public. Expectations of U.S. regulatory approval for such funds drove the price of bitcoin to the highest level in about two years. The digital currency traded just below $46,000 late Wednesday, up from $17,000 in January 2023. Until now, everyday investors who wanted to buy and sell digital currencies have had to either trade on crypto exchanges and incur hefty transaction fees or purchase products that track bitcoin in less direct ways. At least half a dozen bitcoin-futures ETFs are already on the market. Those funds use futures contracts to provide exposure to bitcoin price moves, though they have been criticized for often straying from bitcoin’s price.

All 11 applications filed by asset managers including BlackRock, Fidelity Investments, ARK Investment Management, Invesco, WisdomTree Bitwise Asset Management, Valkyrie and Grayscale Investments have been greenlighted to list. The new funds, known as spot-bitcoin ETFs because they buy and sell the digital currency itself, are expected to begin trading on Thursday.

The week ahead — Economic data from Econoday.com: