Week of Jan 5, 2024 Weekly Recap & The Week Ahead

There isn’t a single formula. You need to know a lot about business and human nature and the numbers… It is unreasonable to expect that there is a magic system that will do it for you. — C Munger

1. Fed Minutes Suggest Rate Hikes Are Over, but Offer No Timetable on Cuts — At the meeting, the rate-setting Federal Open Market Committee agreed to hold its benchmark rate steady in a range between 5.25% and 5.5%. Members indicated they expect three quarter-percentage point cuts by the end of 2024. Officials noted the progress that has been made in the battle to bring down inflation. They said supply chain factors that contributed substantially to a surge that peaked in mid-2022 appear to have eased. In addition, they cited progress in bringing the labor market better into balance, though that also is a work in progress.

The “dot plot” of individual members’ expectations released following the meeting showed that participants expect cuts over the coming three years to bring the overnight borrowing rate back down near the long-run range of 2%.

2. U.S. Auto Sales Bounced Back in 2023 — The U.S. auto industry rebounded in 2023 with many car companies reporting double-digit sales gains, marking a return to normalcy for a sector that has been on a roller coaster since the start of the pandemic. Automakers’ results were boosted by pent-up demand and better availability on dealership lots. A six-week United Auto Workers strike this fall did little to dampen the industry’s momentum and electric-vehicle sales continued to rise, albeit at a slower rate than in the previous year. Analysts project industrywide sales of new cars in the U.S. could reach nearly 15.5 million in 2023, about a 13% increase from the prior year, once all car companies have released their figures.

3. Money-Market Fund Assets Rise to New All-Time High — Money-market fund assets rose to an all-time high, led by inflows into the government sector as investors sought to protect their cash at the end of the year. About $78.6 billion flowed into US money-market funds in the week through Jan. 3, according to Investment Company Institute data. Total assets rose to $5.965 trillion from $5.89 trillion the week prior. Retail investors have been piling into money funds since the Federal Reserve began one of the most-aggressive tightening cycles in decades in 2022. But last month, the Fed signaled that campaign is over and projected deeper interest-rate cuts this year.

4. Job Gains Picked Up in December, Capping Year of Healthy Hiring — The U.S. economy added 216,000 jobs last month, the Labor Department reported Friday. That was larger than November’s gain of 173,000, and better than forecasters were expecting. Hiring was revised down in both October and November. For all of 2023, employers added 2.7 million jobs, a slowdown from 2022, but a better gain than in the years preceding the pandemic. Hiring was broad-based last month, with healthcare and government leading job gains. Transportation and warehousing employers shed jobs. The unemployment rate in December held at 3.7%. The jobless rate began 2023 at 3.4%, matching lows not seen since the late 1960s, and remains low despite inching higher late last year.

Wages rose a healthy 4.1% last month from a year earlier. More broadly, there are signs the tight labor market conditions that prompted employers to offer robust pay raises in early 2023 continue to wane.

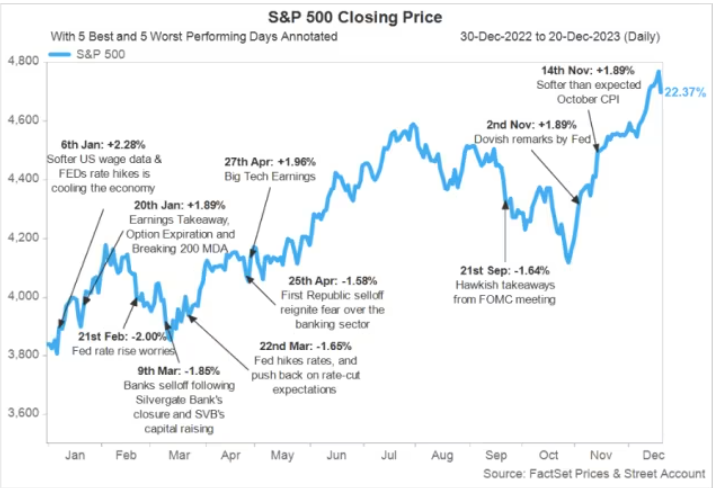

In a look back at 2023, data provider FactSet took a look at the biggest daily market moves in both directions.

The week ahead — Economic data from Econoday.com: