Week of Oct 11 ’25 Weekly Recap & The Week Ahead

October 14th, 2025“A good trader watches his capital as carefully as a professional scuba diver watches his air supply.” – Anonymous

1. Fed Minutes Reveal Divide Over Outlook for Interest-Rate Cuts — Officials largely agreed that a recent slowdown in job growth outweighed lingering concerns over sticky inflation when they cut their benchmark rate by a quarter-point last month, to a range between 4% and 4.25%. Most of them thought “it would likely be appropriate to ease policy further over the remainder of the year,” according to minutes of the Sept. 16-17 meeting. But the written account said a few of them thought a rate cut wasn’t necessary last month or could have also supported holding rates steady. The minutes indicated that support for a larger half-point cut was limited to one official, Fed governor Stephen Miran, who dissented from the decision. Miran was appointed by President Trump and sworn in on the morning of the first day of the meeting.

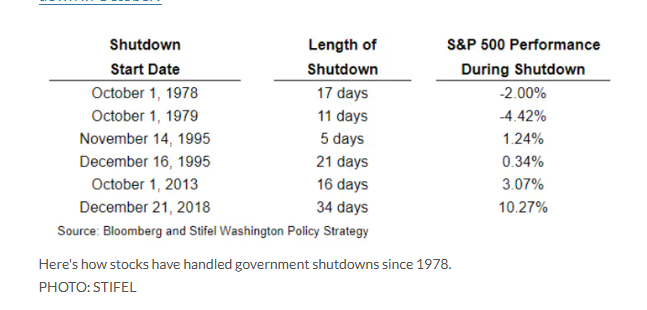

2. Trump Renews Threats With Congress Mired in a Shutdown Brawl — There was no sign of progress as government workers and military personnel prepare for missed paychecks and the general public begins to feel the effects of the closure on everything from taxpayer services to air travel. Trump has repeatedly threatened to fire federal workers, withhold back pay for some government employees and cut funding for programs favored by Democrats, but so far none have materialized. Some Republicans have questioned that strategy, saying it distracts from their messaging to blame Democrats for the shutdown effects. The Senate has canceled plans for a recess next week to stay in Washington if the shutdown persists, a person familiar with the decision said. Speaker Mike Johnson, however, has declined to call House lawmakers back since before the shutdown started, insisting that the House did its job by passing a stopgap funding bill that would reopen the government through Nov. 21.

3. Americans Are Falling Behind on Their Car Payments — Since the pandemic, buyers on auto-dealer lots have encountered surging sticker prices and smaller incentives from automakers to lessen the blow. To afford an automobile, more consumers, especially lower-income families, have resorted to buying used cars and taking out longer loans. The percentage of new-car buyers with credit scores below 650 was nearly 14% in September, roughly one in seven people, J.D. Power said last month. That is the highest for the comparable period since 2016. And the portion of subprime auto loans that are 60 days or more overdue on their payments hit a record of more than 6% this year, according to Fitch Ratings, while delinquency rates for other borrowers have remained relatively steady.

4. China Widens Rare Earth Curbs Ahead of Key Xi-Trump Meeting — China has unveiled broad new curbs on its exports of rare earths and other critical materials, as Beijing moves to shore up its trade war leverage ahead of a high-stakes meeting this month between Donald Trump and Xi Jinping. Overseas exporters of items that use even traces of certain rare earths sourced from China will now need an export license, the Ministry of Commerce said in a statement Thursday, citing national security grounds. Certain equipment and technology for processing rare earths and making magnets will also be subject to controls, according to a separate release.Separately, the ministry later announced plans to expand export controls to a range of new products in measures that will be enforced from November 8. The newly-affected products include five more rare earths — holmium, europium, ytterbium, thulium, erbium — plus certain lithium-ion batteries, graphite anodes and synthetic diamonds, as well as some equipment for making those materials.

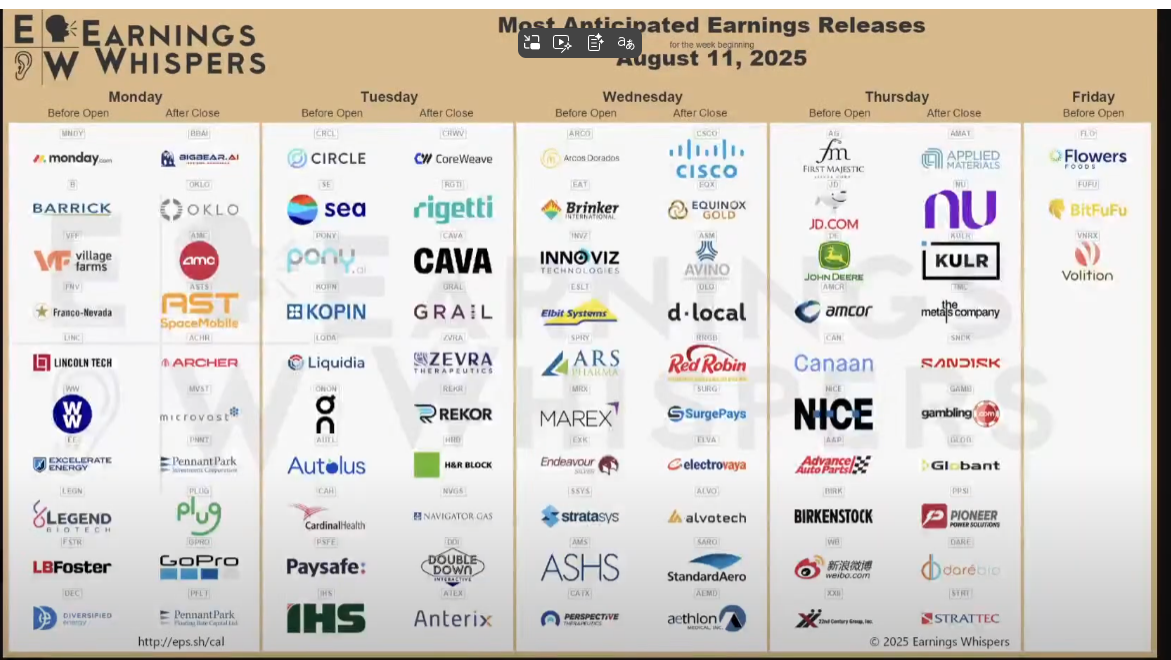

The week ahead — Economic data from Econoday.com: