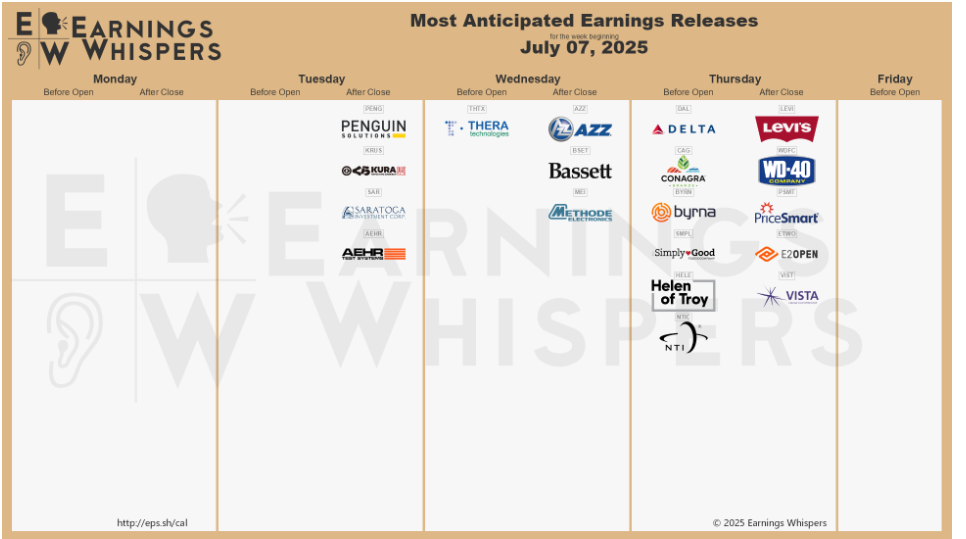

July 9th, 2025

“I AM A CONSISTENT WINNER BECAUSE: 1. I objectively identify my edges. 2. I predefine the risk of every trade. 3. I completely accept the risk or I am willing to let go of the trade. 4. I act on my edges without reservation or hesitation. 5. I pay myself as the market makes money available to me. 6. I continually monitor my susceptibility for making errors. 7. I understand the absolute necessity of these principles of consistent success and, therefore, I never violate them.”

― Mark Douglas

1. US Job Openings Unexpectedly Rise to Highest Since November — available positions increased by 374,000 to 7.77 million, according to Bureau of Labor Statistics data published Tuesday. That exceeded all estimates in a Bloomberg survey of economists. Vacancies in the hospitality sector accounted for three quarters of May openings. The finance, transportation and warehousing industries as well health care also saw more moderate gains. The May gain brought openings roughly in line with last year’s average. However, the increase was concentrated in one industry and openings in other sectors were more mixed. That suggests employers are growing cautious about expanding their staff while at the same time mostly holding onto their existing workers.

2. The private sector lost 33,000 jobs in June, badly missing expectations for a 100,000 increase — Private payrolls lost 33,000 jobs in June, the ADP report showed, the first decrease since March 2023. Economists polled by Dow Jones forecast an increase of 100,000 for the month. The May job growth figure was revised even lower to just 29,000 jobs added from 37,000. This week, the government’s nonfarm payrolls report will be out on Thursday with economists expecting a healthy 110,000 increase for June, per Dow Jones estimates. Economists are expecting the unemployment rate to tick higher to 4.3% from 4.2%. Some economists could revise down their jobs reports estimates following ADP’s data.

Weekly jobless claims data is also due Thursday, with economists penciling in 240,000. This string of labor stats comes during a shortened trading week, with the market closing early on Thursday and remaining dark on Friday in honor of the July Fourth holiday.

3. Trump Wins Broad Economic Policy Shift as House Passes Tax Bill — President Donald Trump secured a sweeping shift in US domestic policy as the House passed a $3.4 trillion fiscal package that cuts taxes, curtails spending on safety-net programs and reverses much of Joe Biden’s efforts to move the country toward a clean-energy economy. The 218-214 vote in the House Thursday sends the legislation to Trump, in time for a July 4 deadline he set. House leaders had to keep earlier procedural votes open for hours to convince a small band of holdouts to support the legislation.

The Senate also imposed deeper cuts in Medicaid health insurance for the poor and disabled, reducing spending on the program by nearly $1 trillion over the next decade, according to the CBO. Most clean-energy tax breaks passed under Biden are phased out and a popular $7,500 consumer tax credit for electric vehicles is eliminated for purchases made after Sept. 30.

The core of the bill is an extension of 2017 Trump tax cuts for individuals and pass-through businesses that were set to expire at the end of 2025. It also provides new resources for Trump’s crackdown on illegal immigration and for military spending including the president’s “Golden Dome” missile defense plan. A group of House Republicans from high-tax states such as New York, New Jersey and California won a temporary increase in the limit on the state and local tax deduction to $40,000. After five years, the cap will snap back to the current $10,000 limit originally imposed under Trump’s 2017 tax law.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

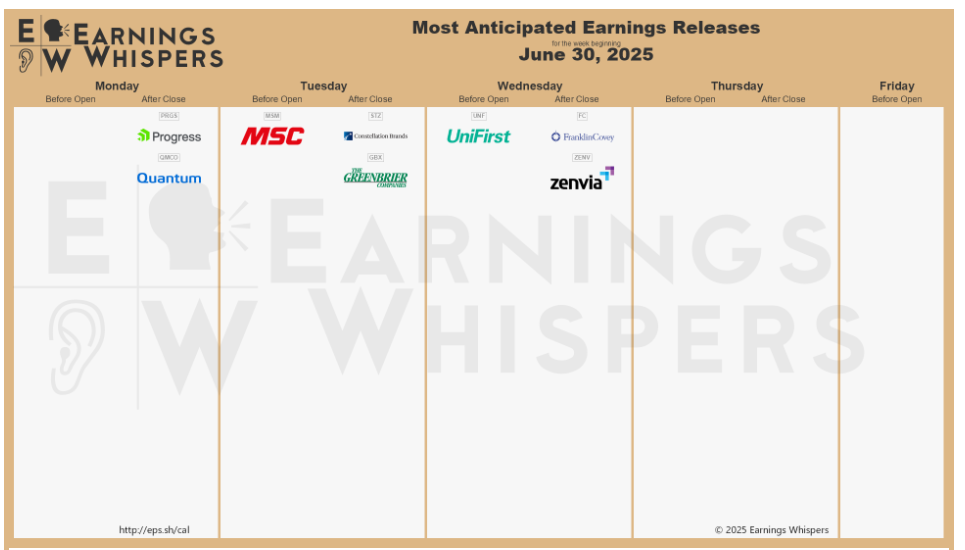

July 2nd, 2025

“The worse a situation becomes the less it takes to turn it around, the bigger the upside,” and “Once we realize that imperfect understanding is the human condition there is no shame in being wrong, only in failing to correct our mistakes” — George Soros

1. U.S. Home Price Growth Cools to Near-Two-Year Low — the S&P CoreLogic Case-Shiller National Home Price Index, which measures home prices across the country, rose 2.7% in the 12 months to April, the slowest on-year appreciation since mid-2023 and cooling from 3.4% in March, data released showed. Mortgage rates continued at a mid-6% range throughout April, keeping monthly payment burdens near generational highs and pricing out significant segments of potential buyers, said Nicholas Godec, head of fixed income tradables and commodities at S&P Dow Jones Indices. The data suggests affordability constraints have hit previously overheated markets hardest, while traditionally stable markets with more reasonable price levels are attracting renewed interest, Godec continued.

2. US GDP Revised Lower as Consumers Slash Services Spending — US consumer spending grew in the first quarter at the weakest pace since the onset of the pandemic on a sharp deceleration in outlays for a variety of services. Spending on services contributed 0.3 percentage point to gross domestic product in the first three months of the year, the least since the second quarter of 2020, according to Bureau of Economic Analysis figures published Thursday. That was down sharply from a previously reported 0.79 point boost. Overall consumer spending increased at a 0.5% pace, instead of the previously reported 1.2%. GDP declined at a downwardly revised 0.5% annualized rate in the first quarter as a result.

The numbers indicate the economy’s woes early in the year weren’t entirely related to the deterioration in the trade balance related to the Trump administration’s tariffs.

3. Economy Core Inflation Rate Rose to 2.7% in May, more than expected — The personal consumption expenditures price index, the Fed’s primary inflation reading, rose a seasonally adjusted 0.1% for the month, putting the annual inflation rate at 2.3%. Economists surveyed by Dow Jones had been looking for respective levels of 0.1% and 2.3%. Excluding food and energy, core PCE posted respective readings of 0.2% and 2.7%, compared with estimates for 0.1% and 2.6%. Fed policymakers consider core to be a better measure of long-term trends because of historic volatility in the two categories. The annual rate was 0.1 percentage point ahead of the April reading. The Fed targets inflation at 2%, a level where it has not been since early 2021. Along with the inflation numbers, consumer spending and income showed further signs of weakening. Spending fell 0.1% for the month, compared with the estimate for an increase of 0.1%. Personal income declined 0.4%, against the forecast for a gain of 0.3%.

4. China’s Industrial Profit Declined in May — Industrial profit fell 9.1% year over year in May, tumbling from April’s 3.0% rise, data released by the National Bureau of Statistics showed Friday. The decline was due to multiple factors, including insufficient demand, falling prices of industrial products and short-term fluctuations, said Yu Weining, a statistician with the bureau. Hefty tariffs imposed by the U.S. on Chinese goods since April led to production at many factories being suspended till late May, when Beijing and Washington reached a truce in a trade war. China’s industrial profit fell 1.1% in the January-May period, reversing from a 1.4% increase recorded in the first four months, the statistics bureau said.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

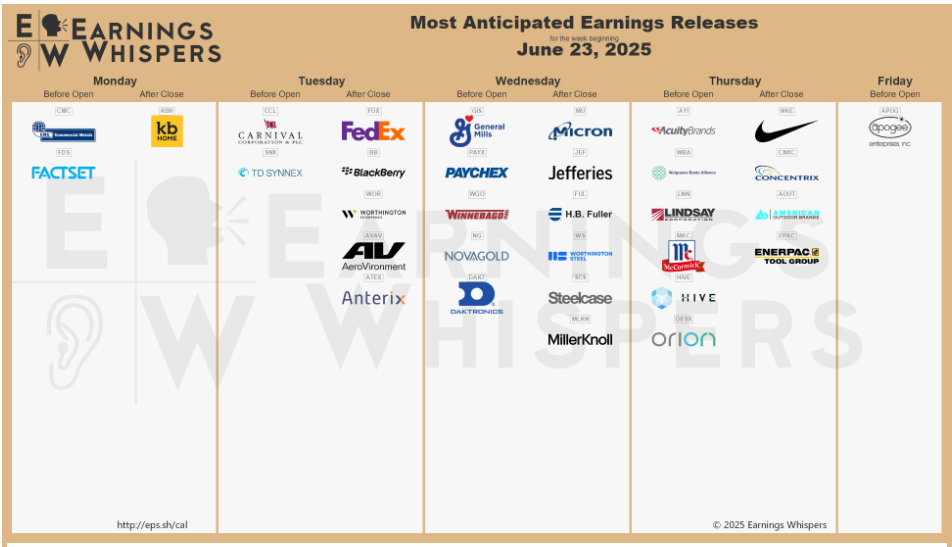

June 25th, 2025

“buy on the sound of cannons, sell on the sound of trumpets” — Nathan Rothschild

1. US Retail Sales Drop for Second Month as Tariff Anxiety Sets In — The value of retail purchases, not adjusted for inflation, decreased 0.9%, the most since the start of the year and restrained by autos, Commerce Department data showed Tuesday. That followed a downwardly revised 0.1% drop in April, marking the first back-to-back decline since the end of 2023. In the retail sales report, seven of the 13 categories posted drops, dragged down by building materials, gasoline and motor vehicles — which came after a buying spree in anticipation of tariffs. Spending at restaurants and bars, the only service-sector category in the retail report, fell by the most since early 2023.

2. Fed’s Forecast Sees Fewer Rate Cuts in 2026 and 2027 — The Federal Reserve kept a steady hand on interest rates, maintaining them at their target range of 4.25% to 4.5%. The central bank is calling for two rate cuts this year, but policymakers see higher inflation. They have also cut their outlook for gross domestic product. The Federal Reserve’s meeting had a dovish tone, with expectations for two rate cuts still in place for this year despite upward revisions to near-term inflation forecasts, said Simon Dangoor, head of fixed income macro strategies at Goldman Sachs Asset Management. “Implicitly FOMC members continue to expect stronger near-term inflation to prove largely transitory and their tolerance to upward moves in unemployment remains low,” he said. “We expect the Fed to remain on hold at next month’s meeting but think a path could open up to a resumption of its easing cycle later this year should the labor market weaken.”

3. Trump Delays TikTok Ban for a Third Time — The TikTok ban was set to take effect on Jan. 19, but Trump has issued a series of extensions that have allowed the app to continue operating. The most recent extension expired Thursday. The 2024 statute authorizes the president to issue a one-time enforcement extension of up to 90 days if he certifies to Congress that “binding legal agreements” are in place that will lead to TikTok’s sale. It is unclear whether that certification has been made or if other laws permit additional enforcement delays. At Thursday’s press briefing, White House press secretary Karoline Leavitt said that “the White House Counsel’s Office and the Department of Justice strongly believe in the legal rationale” for the third extension, but didn’t provide further details. Trump came to TikTok’s defense last year after recognizing the addictive social-media platform was an effective way to reach young voters. In his first term, however, Trump had unsuccessfully sought to close down the app or transfer control of certain features after national-security officials concluded TikTok harvests sensitive data from tens of millions of Americans and can use its algorithm to manipulate content to further Chinese political objectives.

4. U.S. Prepares Action Targeting Allies’ Chip Plants in China — Currently, South Korea’s Samsung Electronics 005930 0.51%increase; green up pointing triangle and SK Hynix 000660 4.47%increase; green up pointing triangle as well as Taiwan Semiconductor Manufacturing 2330 1.93%increase; green up pointing triangle enjoy blanket waivers that allow them to ship American chip-making equipment to their factories in China without applying for a separate license each time. Jeffrey Kessler, head of the Commerce Department unit in charge of export controls, told the three companies this week he wanted to cancel those waivers, according to people familiar with the meetings. They said Kessler described the action as part of the Trump administration’s crackdown on critical U.S. technology going to China.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

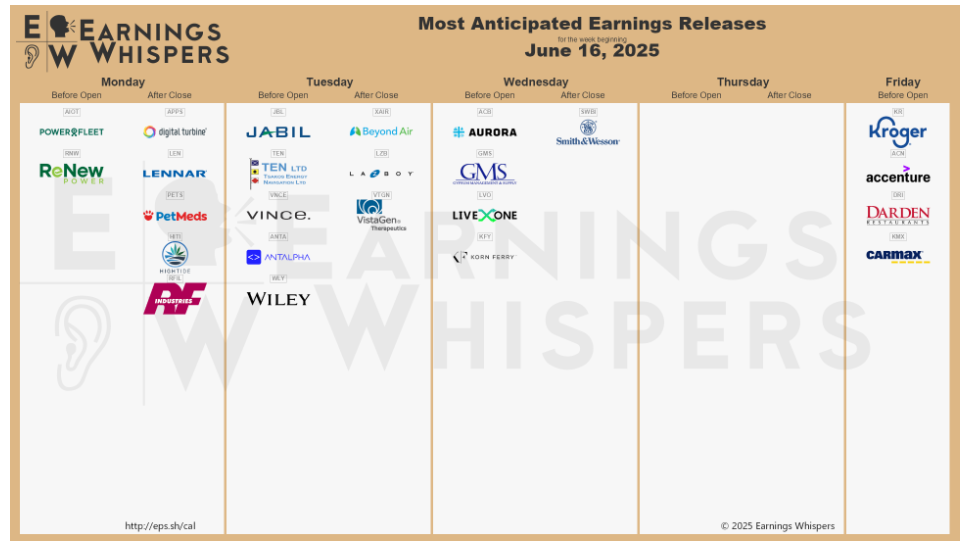

June 17th, 2025

“If most traders would learn to sit on their hands 50 percent of the time, they would make a lot more money.” – Bill Lipschutz

1. India, US to Expedite Trade Talks Ahead of Trump’s Tariff Deadline — Trade officials from India and the US met in New Delhi for about a week to discuss issues including greater market access, digital trade, customs rules and technical barriers to trade, the official told reporters in New Delhi, asking not to be identified as the information isn’t public. The US trade team arrived in New Delhi last week to advance trade negotiations. India and the US are working on a phased trade deal with an early agreement targeted for July, the deadline for implementation of the Trump administration’s so-called reciprocal tariffs. Those tariffs — which target Indian exports with 26% levies — are facing legal challenges in Washington.

2. US Core Inflation Rises Less Than Forecast for Fourth Month — The consumer price index, excluding the often volatile food and energy categories, increased 0.1% from April, according to Bureau of Labor Statistics data out Wednesday. From a year ago, it rose 2.8%. Goods prices, excluding food and energy commodities, were unchanged. New and used-car prices both declined, as did apparel. Meanwhile, services prices minus energy rose 0.2%, a deceleration from the prior month and reflecting a decline in airfares and hotel stays.

The string of below-forecast inflation readings adds to evidence that consumers have yet to feel the pinch of President Donald Trump’s tariffs — perhaps because the most punitive levies have temporarily been on pause, or thanks to companies so far absorbing the extra costs or boosting inventory ahead of tariffs.

3. Muted US Producer Prices Add to String of Tame Inflation Reports — The producer price index rose 0.1% from a month earlier, according to a Bureau of Labor Statistics report released Thursday. The median forecast in a Bloomberg survey of economists called for a 0.2% increase. Excluding food and energy, the PPI also increased 0.1%. The PPI report follows May consumer price data that showed a fourth month of tame inflation. While the impact of higher tariffs has so far been modest for Americans, economists see price pressures building in the second half of the year as companies look to pass costs on to their customers.

4. Israel Attacks Iran’s Nuclear Sites and Kills Senior Commanders — Israel launched strikes across Iran on Friday morning, targeting nuclear facilities and killing top military commanders in a major escalation against its chief adversary that risks sparking a broad war in the Middle East. The strikes were far more extensive than those Israel carried out against Iran last year and underscored the country’s growing assertiveness, as well as its military and intelligence capabilities. Israel said it struck around 100 targets across Iranian cities on Friday morning, using 200 planes. The attacks caused oil to surge as much as 13%, though it later pared its gains, and investors to buy havens such as gold and US Treasuries.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 10th, 2025

“I’m not better than the next trader, just quicker at admitting my mistakes and moving on to the next opportunity”. — George Soros

1. OECD Warns That World Growth to Slow Amid Trade Turmoil — The world economy will lose pace this year, hamstrung by uncertainty stemming from a whipsawing U.S. trade policy, according to new forecasts from the Organization for Economic Cooperation and Development. Collectively, the global economy is now set to grow by 2.9% this year and next, the OECD said in its quarterly report released Tuesday. That marks a downgrade to the group’s previous forecasts, which saw growth at 3.1% in 2025 and 3% in 2026, and suggests the world economy is set to slow from the 3.3% expansion it booked last year.

2. U.S. Hiring Slows Again, ADP Report Shows — Just 37,000 jobs were created last month, down from 62,000 in April, according to the ADP National Employment report released Wednesday. Economists polled by The Wall Street Journal had expected hiring to pick up pace to 110,000 new jobs on the month. The downturn means jobs growth was its weakest in more than two years. Signs of weakness in hiring in the private sector contrast to other indications of a robust jobs market. There has been little sign elsewhere that gloomier economic sentiment is leading to an uptick in unemployment.

3. US Trade Deficit Narrows by Most on Record as Imports Plunge — The gap in goods and services trade shrank 55.5% from the prior month, to $61.6 billion, the smallest since 2023 and more than completely reversing the sharp widening that occurred in the first quarter, Commerce Department data showed Thursday. The median estimate in a Bloomberg survey of economists was for a $66 billion deficit. Imports of goods and services declined a record 16.3% in April, while exports increased 3%. The sharp narrowing in April puts trade on track for a large contribution to gross domestic product in the second quarter after being largely responsible for a 0.2% annualized decline in first-quarter GDP. Higher US reciprocal duties on most imported goods that went into effect early in the month helps explain the huge slowdown in inbound shipments from overseas producers.

4. US Jobs Report Points to Gradual Moderation in Labor Market — Nonfarm payrolls increased 139,000 last month after a combined 95,000 in downward revisions to the prior two months, according to Bureau of Labor Statistics data out Friday. The unemployment rate held at 4.2%, while wage growth accelerated. The payrolls figure, which was slightly better than expectations, helps alleviate concerns of a rapid deterioration in labor demand as companies contend with higher costs related to tariffs and prospects of slower economic activity. President Donald Trump’s decision to pause some of the more punitive import duties, including those on China, has helped lift sentiment among businesses as well as consumers. The labor market report wraps up a week of disappointing economic data that included a further increase in applications for jobless benefits and weaker services activity.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 3rd, 2025

“There will not be any posting for the week of May 30th, 2025. We are away for some needed R&R.” — Have a good week.

Posted in Weekly Summary | No Comments »

May 22nd, 2025

“Do more of What Work and Do Less of What Doesn’t” — unknown

1. U.S. and China agree to slash tariffs for 90 days in major trade breakthrough — The trade agreement means that “reciprocal” tariffs between both countries will be cut from 125% to 10%. The U.S.′ 20% duties on Chinese imports relating to fentanyl will remain in place, meaning total tariffs on China stand at 30%. The breakthrough comes after U.S. and China trade representatives held high-stakes talks in Switzerland over the weekend. The pause will begin Wednesday. Both China and the U.S. said they will continue discussions on economic and trade policy.

2. Monthly Inflation Ticked Up in Early Hints of Tariff Effects — The consumer-price index rose a seasonally adjusted 0.2% in April, the Labor Department said Tuesday. That matched the forecasts of economists polled by The Wall Street Journal. However, it was a turnaround from March, when month-over-month prices fell 0.1%. Year-over-year inflation cooled to a 2.3% increase in April, below the 2.4% that economists had expected and below March’s annual rate. A big decline in gasoline prices versus a year earlier helped pull that rate lower. Prices excluding food and energy categories—the so-called core measure that economists watch in an effort to better capture inflation’s underlying trend—rose 2.8%. That matched forecasts by economists.

3. US Producer Prices Fell Unexpectedly in April as Margins Shrank — The 0.5% decrease in the producer price index followed no change in March, Bureau of Labor Statistics data showed Thursday. The median forecast in a Bloomberg survey of economists called for a 0.2% gain. Excluding food and energy, the PPI declined 0.4% — the most since 2015. Stripping out food, energy and trade, a less-volatile measure favored by many economists, prices fell 0.1%, the first decline in five years. Compared with a year ago, the gauge rose 2.9%. The figures suggest American manufacturers and service providers are so far refraining from passing along higher US duties on imports. The impact on consumers has also been modest even as producers are feeling the pinch from aggressive levies on imported materials and other inputs.

4. US Retail Sales Barely Rise, Suggesting Some Spending Pullback — Growth in US retail sales decelerated notably in April, reflecting consumers pulled back spending on cars, sporting goods and other categories of imported goods amid concerns about rising prices from tariffs.

The value of retail purchases, not adjusted for inflation, increased 0.1%, Commerce Department data showed Thursday. That followed a a revised 1.7% gain in March, which was the largest in two years. Seven of the report’s 13 categories posted decreases, also restrained by apparel — another good which is largely imported — as well as gasoline. Car sales declined slightly after a buying spree in the previous month. Spending at restaurants and bars, the only service-sector category in the retail report, rose firmly for a second month.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 14th, 2025

“Do More of What Works and Less of What Doesn’t” — unknown

1. U.S. Trade Deficit Hits Record as Companies Front-Load Pharmaceuticals — The U.S. trade deficit ballooned 14% to a record $140.5 billion in March, as businesses stockpiled goods to get ahead of sweeping tariffs that President Trump imposed the following month. The value of imported goods totaled $346.8 billion, according to Census Bureau data, continuing a sharp increase that began in January. Nearly all of the $22.5 billion surge in imported consumer goods for March were pharmaceutical products, which the Trump administration is currently considering to hit with tariffs. Imports of computer accessories, automobiles, and car parts and engines also increased.

2. Fed Warns of Rising Economic Risks as It Leaves Rates Steady — The Federal Reserve warned that the economy faced growing risks of higher unemployment and higher inflation due to tariff increases when officials agreed to hold interest rates steady on Wednesday. Tariffs represent a shock that can decrease an economy’s ability to supply goods or services while sending up prices. The unpredictable rollout of increased duties on imported goods threatens to sap profits and chill new investment until businesses have more clarity on their underlying cost structure. Expectations of a rate cut at the Fed’s next meeting in mid-June declined when Powell said officials felt like the costs of waiting to learn more about the economy were “fairly low.”

3. US Productivity Drops for First Time Since 2022 as Output Falls — Productivity, or nonfarm employee output per hour, decreased at a 0.8% annualized rate after a revised 1.7% increase in the fourth quarter, data from the Bureau of Labor Statistics showed Thursday. Because of the decline in productivity, unit labor costs — what businesses pay employees to produce one unit of output — jumped 5.7% in the January-March period, the most in a year. The retreat in productivity was largely due to a 0.3% decline in business output, foreshadowed by data last week showing a trade-related slide in gross domestic product, even as worker hours climbed. Over the near term, productivity gains may suffer somewhat as companies reconsider investment plans until there’s more clarity about US trade and tax policy.

4. Trump Hails UK Trade Framework as First of Many Tariff Deals — Under the agreement, Trump said Thursday the UK would fast-track US items through their customs process and reduce barriers on “billions of dollars” of agricultural, chemical, energy and industrial exports, including beef and ethanol. The British government said auto tariffs would be reduced to 10% and metals duties to zero. Trump and UK Prime Minister Keir Starmer said final details of the pact would still be negotiated over the coming weeks and statements from both governments made clear that many specifics were left to be resolved later.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 7th, 2025

“It takes 20 years to build a reputation and five minutes to ruin it.” — Buffetts

1. U.S. Economy Contracts at 0.3% Rate in First Quarter — the Commerce Department said U.S. gross domestic product—the value of all goods and services produced across the economy—fell at a seasonally and inflation adjusted 0.3% annual rate in the first quarter. That was the steepest decline since the first quarter of 2022. Net exports, the difference between imports and exports, were a large drag on growth in the first quarter, stripping 4.83 percentage points from headline GDP. Imports increased at a 41.3% pace in the first quarter as businesses tried to get ahead of tariffs that began to come into effect during the first three months of the year and were dramatically increased in the current, second quarter. The GDP report is the first major economic scorecard for the January-to-March quarter, a period in which the White House changed hands from President Joe Biden to President Trump. January—most of which was before Trump took office—was hit by wildfires in Los Angeles and disruptive winter storms in many parts of the country.

2. US Manufacturing Activity Shrinks by the Most Since November — The Institute for Supply Management’s factory gauge eased 0.3 point to 48.7, data out Thursday showed. The group’s production index stumbled more than 4 points to 44. Readings below 50 indicate contraction. Prices paid for inputs, however, accelerated slightly. The figures illustrate an industrial sector struggling for traction as US tariffs and general uncertainty surrounding trade policy interrupt expansion plans. Orders shrank for a third month and backlogs retreated at a faster pace, consistent with subdued demand.

3. US Consumer Spending Jumps While Key Inflation Gauge Slows Down — Inflation-adjusted consumer spending climbed 0.7% last month, according to Bureau of Economic Analysis data out Wednesday. That was the most since the start of 2023 and suggested households spent aggressively to get ahead of new tariffs.

Meantime, the Federal Reserve’s preferred inflation gauge — the personal consumption expenditures price index — stagnated from a month earlier for the first time in nearly a year. Excluding food and energy, the so-called core PCE was also unchanged, the tamest in almost five years. The data round out a quarter in which the US economy contracted for the first time since 2022 on a monumental pre-tariffs import surge and more moderate consumer spending. The report earlier Wednesday also showed core PCE inflation accelerated to a 3.5% pace in the first quarter — the most in a year.

4. U.S. payroll growth totals 177,000 in April, defying expectations — Nonfarm payrolls increased a seasonally adjusted 177,000 for the month, slightly below the downwardly revised 185,000 in March but above the Dow Jones estimate for 133,000, the Bureau of Labor Statistics reported Friday. The unemployment rate held at 4.2%, as expected, indicating that the labor market is holding relatively stable. The survey of households, which is used to calculate the jobless rate, showed an even stronger gain, with an increase of 436,000 in those who reported holding jobs on the month.

A broader unemployment gauge that includes discouraged workers and those holding part-time jobs for economic reasons, or the underemployed, edged lower to 7.8%. The labor force participation rate ticked higher to 62.6%. The strong report led traders to push out expectations for an interest rate cut until July, according to the CME Group’s FedWatch gauge of futures pricing.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 30th, 2025

“Do more of what works and less of what doesn’t” — Unknown

1. Trump U-Turns on Powell, China Follow Dire Economic Warnings — Trump entered office with a steadfast desire to reshape the global economy. But his resolve has appeared to waver in the face of turmoil in equities and bonds and pleas from powerful executives who fear his sweeping tariffs and interference with the Federal Reserve could set off an economic calamity. Trump on Tuesday said he had no intention to fire Powell — despite days of criticism over the central bank’s policies — and said he believed a deal with Beijing would significantly reduce the sweeping tariffs he’s posted on Chinese goods. After a report that the US would be willing to phase in lighter tariffs on Beijing over five years on Wednesday, Trump told reporters that China was “going to do fine” once talks had settled.

2. March home sales drop to their slowest pace since 2009 — Sales of previously owned homes in March fell 5.9% from February to 4.02 million units on a seasonally adjusted annualized basis, according to the National Association of Realtors. That’s the slowest March sales pace since 2009. Sales were 2.4% lower than March 2024 and slumped across all regions month-to-month. They fell hardest in the West, the priciest region of the country, down more than 9%. The West, however, was the only region to see a year-over-year gain, due to strong activity in the Rocky Mountain states where job growth is strong.

3. Economy Orders for big-ticket items like autos and appliances surged 9.2% in March in rush to beat tariffs — So-called durable goods orders soared a seasonally adjusted 9.2% on the month, up from a 0.9% gain in February and well ahead of the Dow Jones forecast for a 1.6% increase. Excluding defense, the increase was even higher, at 10.4%, though the ex-transportation number was flat. Transportation equipment orders surged 27%, led by a 139% increase in nondefense aircraft and parts. In addition to aircraft and autos, the durables category also includes items such as appliances, computers and jewelry. On the durables goods side, the advanced report reflects a pull-forward effect as Trump dangled threats against U.S. trading partners through March before announcing his “Liberation Day” duties on April 2. Trump slapped a 10% tariff against all imports as well as a select charges against dozens of countries that he ultimately tabled for 90 days for negotiations.

4. US Consumer Sentiment Slides While Inflation Expectations Jump — The final April sentiment index fell to 52.2 from 57 a month earlier, according to the University of Michigan. While a slight improvement from the preliminary gauge of 50.8, the latest figure is the fourth-lowest in data back to the late 1970s.

Consumers anticipated inflation will rise at an annual rate of 4.4% over the next five to 10 years, the data out Friday showed. They expect prices to rise at a 6.5% pace over the next year. While down from a preliminary reading of 6.7%, year-ahead price expectations are still the highest since 1981.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »