November 27th, 2018

“There is only one side of the market and it is not the bull side or the bear side, but the right side.” – Jesse Livermore

1. New U.S. Report Complaint China Continuing ‘Unfair, Unreasonable’ Trade Practices — the U.S. Trade Representative said in an update to its “Section 301”, investigation into China’s intellectual property and technology transfer policies, Beijing has failed to take any substantive actions against its “unfair” trade practices. It’s not a good sign after last weekend’s tensious APEC summit. President Trump is also due to meet Xi Jinping in ten days at the G20 summit in Buenos Aires.

2. FedEx Adds EV Fleet — FedEx (NYSE:FDX) is adding 1,000 electric delivery vans to its fleet, which will come from Chanje Energy and Ryder System (NYSE:R). The vans can travel more than 150 miles and haul 6,000 pounds when fully charged, while having the potential to help FedEx save 2K gallons of fuel and avoid 20 tons of annual emissions per vehicle. All of the EVs will be operated in California.

3. Crypto Selloff Intensifies; Bitcoin Plunges 20% — Bitcoin (BTC-USD) hit the $4,000 level, continuing a week of major losses in the cryptocurrency world. The plunge comes amid a broad selloff in the equity markets, persistent concerns about regulatory scrutiny and disagreements within the coin developer community – known as a “hard fork.” Other cryptos down sharply include Ripple (XRP-USD), Bitcoin Cash (BCH-USD), Ether (ETH-USD) and Litecoin (LTC-USD).

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 19th, 2018

“We have to practice defensive investing, since many of the outcomes are likely to go against us. It’s more important to ensure survival under negative outcomes than it is to guarantee maximum returns under favorable ones.” ― Howard Marks

1. Gas to Top Coal as Energy Source by 2030 — natural gas is expected to overtake coal as the world’s second largest energy source after oil by 2030 due to a drive to cut air pollution and the rise of LNG. The estimates are based on the IEA’s “New Policies Scenario” that takes into account legislation and policies to reduce emissions and fight climate change. They also assume more energy efficiencies in fuel use and other factors.

2. California Wildfire Deadliest in State History — the death toll has reached 42 in California’s wildfire, making it the deadliest in state history, while an additional 228 people remain missing. Despite sharp criticism on Twitter, President Trump approved California’s request for federal disaster aid. Edison International (NYSE:EIX) and PG&E (NYSE:PCG), whose shares have plunged over the last two sessions, will likely face lawsuits blaming their faulty power lines for sparking the blazes.

3. OPEC and Its Partners Plan of Larger Output Cut — looking to avert an oversupply that has weakened prices, OPEC and its partners are reportedly discussing a proposal to cut crude output by up to 1.4M bpd for 2019, a larger figure than officials have previously mentioned. Oil prices are now experiencing the “normal volatility that comes in the run up to our conference [on Dec. 6]… it’s a period of anxiety for all stakeholders,” OPEC Secretary General Mohammed Barkindo told CNBC.

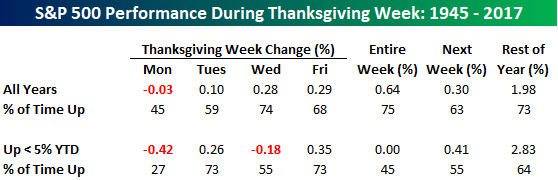

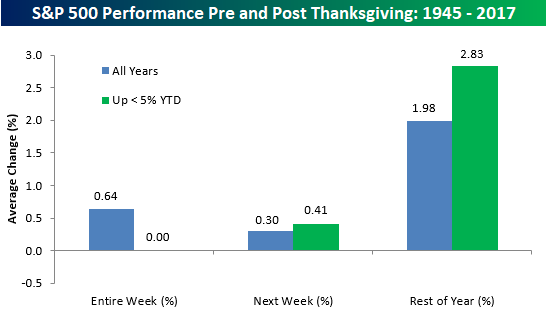

4. Thanksgiving Market Returns — courtesy of BIG, As shown in the table below, during years where the S&P 500 was positive but up less than 5% YTD heading into Thanksgiving week, the index’s average change during the week has been 0.00% with gains less than half of the time.

As we move past Thanksgiving, though, seasonal trends for the market based on this year’s performance so far improve. In those years where the S&P 500 was up less than 5% YTD heading into Thanksgiving week, the average gains the week after Thanksgiving was 0.41% with positive returns 55% of the time. For the remainder of the year, average returns were even stronger at +2.83%. Not bad for a period of just over five weeks!

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 13th, 2018

“Successful Investing takes time, discipline and patience. No matter how great the talent or effort, some things just take time: You can’t produce a baby in one month by getting nine women pregnant.” — Warren Buffett

1. U.S. Issues Eight Waivers From Iran Oil Sanctions — Eight countries including Turkey, Italy, India, Japan and South Korea – will receive temporary six-month waivers allowing them to continue to import Iranian petroleum products as they move to end such imports entirely, but the Islamic Republic can only spend the money on a narrow range of humanitarian items. Iran exported the equivalent of 2.5M barrels a day in April, before the announcement of sanctions turned away buyers.

2. China Ready for U.S. Trade Talks — Vice President Wang Qishan told the Bloomberg New that “The Chinese side is ready to have discussions with the U.S. on issues of mutual concern and work for a solution on trade acceptable to both sides,”. Ahead of his expected meeting with President Xi later this month, President Trump has threatened to impose further tariffs on $267B of Chinese imports if the two countries cannot reach a trade deal.

3. Canabis Pot Stocks Rally on AG Sessions Exit — the marijuana sector exploded to the upside after Attorney General Jeff Sessions resigned following months of public criticism from President Trump. A longtime opponent of attempts to legalize weed, Sessions lifted an Obama-era policy (known as the Cole Memo) earlier this year that kept federal authorities from cracking down on the pot trade in states where the drug is legal. Cannabis stocks added to their gains as Michigan approved recreational marijuana.

4. Google Plots Significant Expansion in NYC — Google is gearing up for an expansion of its NYC real estate that could add space for more than 12,000 new workers, an amount nearly double the search giant’s current staffing in the city, WSJ reports. Google (GOOG, GOOGL) plans on buying/leasing a 1.3M-square-foot office building at St. John’s Terminal and expanding its existing property at Chelsea Market by about 300K square feet. Amazon (NASDAQ:AMZN) is also considering the area for its second headquarters.

5. Midterm Results, Democrats take House and Republican Controls Senate — gridlock in Washington could also stall the White House’s bid to deregulate banking and financial services. Representative Maxine Waters, a fierce Trump critic and Wall Street foe, appears poised to take control of the House’s powerful financial services committee. The halt of deregulation legislation could also affect other sectors like energy, industrials and small business.

6. U.S. Oil Benchmark Drops Below $61/bbl in Bear Market Territory — U.S. crude is now down by around 20% since early October as rising supply and concerns of an economic slowdown pressure prices. Fresh U.S. sanctions are unlikely to cut as much oil out of the market as initially expected with Washington granting temporary exemptions to Iran’s biggest buyers. American production has also reached a new record high of 11.6M bbl/day.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 5th, 2018

“Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be a more productive than energy devoted to patching leaks.” — Warren Buffett

1. U.S. Treasury See 2018 Borrowing Rising to $1.34T — the U.S. Treasury Department expects to issue $425B in debt this quarter, bringing government borrowing this year to $1.34T, more than double from 2017. The borrowing estimate is still $15B lower than its estimate in July. Separately, the Fed is expected this week to vote on standards that would change the way big banks are regulated, dividing institutions into categories based on risk factors.

2. Ford, Baidu Testing Self-Driving Cars in China — following an initial announcement made in June that the two companies would explore areas of cooperation in the fields of AI and connectivity, Ford (NYSE:F) and Chinese internet giant Baidu (NASDAQ:BIDU) said they are now teaming on self-driving cars. The two-year initiative will see the firms collaborate to meet the Level 4 standard set by U.S. industry organization SAE International – meaning autonomous vehicles developed by the two will not require intervention from a human driver.

3. U.S.-China Trade Developments — President Trump has asked officials in his administration to start drafting terms of a trade deal with Beijing, sources told Bloomberg, which reported that multiple agencies are involved in the effort. Hopes are for reaching an agreement with Chinese President Xi Jinping later this month at the G20 summit in Argentina.

4. Moody’s Cuts GE Credit Rating Again — General Electric fell for a sixth straight session after Moody’s lowered the company’s credit rating by two notches to Baa1 from A2, three notches above “junk” territory. The downgrade, which came a month after S&P cut GE’s credit rating, reflected “the adverse impact on GE’s cash flows from the deteriorating performance of the Power business… and misjudgment of financial prospects and operational missteps.”

The week ahead — Economic data from Econoday.com:

Tags: GE Downgraded

Posted in Weekly Summary | No Comments »

October 30th, 2018

“I will tell you how to become rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.” — Warren Buffett

1. Foreign Buying of U.S. Treasurys Softens, Unsettling Financial Markets — foreign investors, traders and central bankers are buying fewer Treasurys. The foreign pullback has helped fuel a bond selloff this fall, which has driven the 10-year yield to 3.17% and has shaken the nine-year-long rally in U.S. stocks, and that continuing reductions in foreign appetite could further unsettle financial markets. China and Japan still both own more than $1 trillion of U.S. debt, according to the U.S. data.

2. Amazon, Qualcomm partner on Alexa headphones — Qualcomm is teaming up with Amazon (NASDAQ:AMZN) to spread the use of its voice assistant, releasing a set of chips that any maker of Bluetooth headphones can use to embed Alexa directly into the device. The functionality would be similar to Apple’s (NASDAQ:AAPL) AirPods, which let users tap the devices to talk to Siri.

3. Moody’s Decided Against Cutting Italian Debt Ratings to Junk — the euro is under pressure amid a bout of disappointing data on the eurozone’s two largest economies. German business activity was shown to have grown by its slowest rate for nearly three and a half years, while French manufacturing also struggled as its PMI index hit a 25-month low.

4. Target Ramps Up Same-Day Delivery Program and Offering Free Two-Day Shipping — In a bid to win shoppers over rivals like Walmart (NYSE:WMT) and Amazon (NASDAQ:AMZN), Target (NYSE:TGT) for the first time ever is offering free two-day shipping – with no minimum purchase required – this holiday season. Target said its “Drive Up” service – where shoppers can place their orders online and have them brought directly to their cars – will also be available at nearly 1,000 stores.

5. U.S. to China: No Trade Talks Without Firm Proposal — the U.S. is refusing to resume trade negotiations with China until Beijing comes up with a concrete proposal to address Washington’s complaints about forced technology transfers and other economic issues, officials told WSJ. The impasse threatens to undermine a meeting between President Trump and Xi Jinping at the G20 summit in November. Businesses have been counting on sufficient progress for the suspension of the next round of U.S. tariffs.

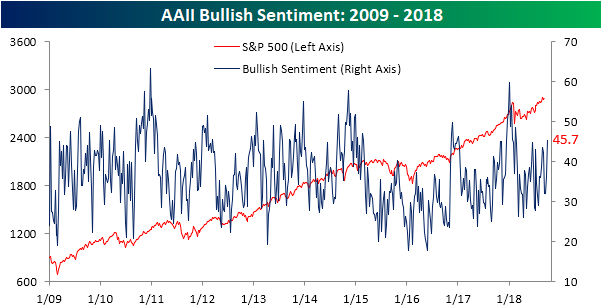

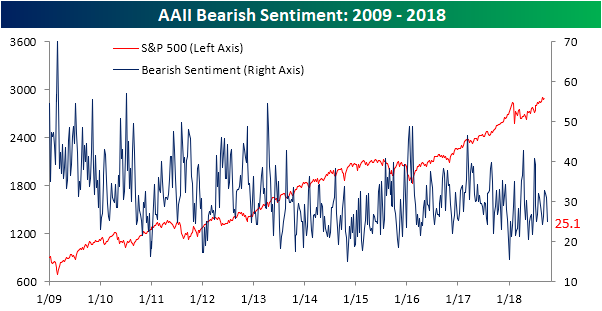

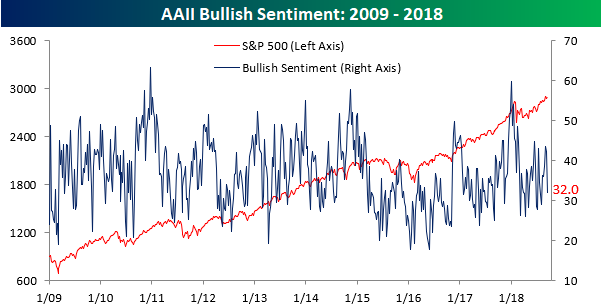

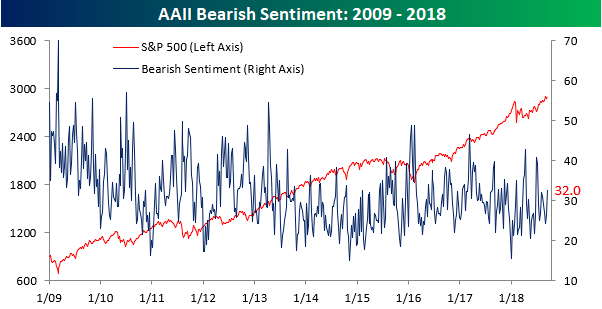

6. AAII Weekly Sentiment Survey — according to the latest weekly sentiment survey from AAII, bullish sentiment saw another decline this week falling from just under 34% to 27.97%. That’s low enough to rank as the fourth weakest reading in bullish sentiment this year.

On the bearish side, negative sentiment rose by a similar amount that bullish sentiment declined, jumping from 35.0% up to 41.0%. That’s the highest reading since the last week of June, right before the July 4th rally, and the third highest reading in bearish sentiment of the year.

Posted in Weekly Summary | No Comments »

October 22nd, 2018

“I believe in analysis and not forecasting.” — Nicolas Darvas

1. Sears Files for Chapter 11 Bankruptcy — Sears has filed for bankruptcy after years of staying afloat through financial maneuvering, a merger with Kmart and relying on billions of CEO Eddie Lampert’s own money. It’s set to shutter 142 stores towards the end of the year and begin liquidation sales shortly. While Lampert will step down as CEO, he’ll remain Sears (NASDAQ:SHLD) chairman, as his ESL Investments negotiates a debtor in possession loan and other funding to support what was once the country’s biggest retailer through the bankruptcy process.

2. Italy Endorses Deficit-Hiking Budget — Italy’s government signed off on an expansionary 2019 budget late Monday – with planned measures that would boost welfare spending, lower the retirement age and cut taxes – in defiance of EU rules that require a shrinking deficit. The draft budget law has rattled financial markets in the past month, with investors demanding significantly higher interest rates to buy Italian bonds.

3. Fidelity Starts Crypto Unit — Fidelity Investments is getting into the crypto scene with a new unit called Fidelity Digital Assets Services. “Our goal is to make digitally-native assets, such as bitcoin, more accessible to investors,” announced CEO Abigail P. Johnson. “We expect to continue investing and experimenting, over the long-term, with ways to make this emerging asset class easier for our clients to understand and use.”

4. U.S. to Open Trade Talks with EU, UK, Japan — Just weeks after the retooling of NAFTA, the U.S. Trade Representative’s office has informed Congress it intends to open trade talks with the EU, U.K. and Japan, aiming to “address both tariff and non-tariff barriers and to achieve fairer, more balanced trade.” Under fast-track rules, the U.S. cannot start trade talks until 90 days after notifying Congress.

5. Canada Legalizes Marijuana Nationwide — Canada begins legalization of recreational marijuana sales in Canada, with provinces handling their own regulations for sale, growth and taxation. Adults will be allowed to carry and share up to 30 grams of legal marijuana in public, cultivate up to four plants in their households and make products such as edibles for personal use. Canadians can also order weed through the mail. Companies related are — TLRY, CRON, CGC, MJ

6. Fed Minutes Point to Continued, Gradual Interest-Rate Increases — the latest Fed minutes shows officials voted unanimously at the September meeting to raise their benchmark rate to a range between 2% and 2.25%. Projections released after the meeting show most officials expected they would need to raise rates one more time this year and around three times in 2019 if the economy performs in line with current forecasts.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 15th, 2018

There will not be any Weekly Re-Cap for the week of Oct 8 to Oct 12 2018. We are away for some needed R&R.

The staffs at EGS.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 9th, 2018

“I have learned through the years that after a good run of profits in the markets, it`s very important to take a few days off as a reward. The natural tendency is to keep pushing until the streak ends. But experience has taught me that a rest in the middle of the streak can often extend it.”– Martin Schwartz

1. Sharp Joins the OLED Revolution — Japan’s Sharp (OTCPK:SHCAY) has finally jumped into the organic light-emitting diode market as it looks to catch up to rivals. The long-awaited decision comes as the major iPhone supplier continues its recovery after being bought two years ago by Taiwan’s Foxconn (OTC:FXCOF). Sharp will offer the OLED panels in its new smartphones later this year and plans to sell the screens to other manufacturers.

2. Exxon Eyes Major Investment at Singapore Refinery — Exxon Mobil is considering a multi-billion dollar investment at its Singapore refinery, the company’s largest, as the shipping and oil refining industries scramble to prepare for new marine fuel regulations starting in 2020. New rules from the International Maritime Organization limit sulfur content to 0.5%, from 3.5% currently, to curb pollution produced by the world’s ships. Singapore is also home to Exxon’s (NYSE:XOM) biggest integrated petrochemical complex.

3. Shell Green Lights Canadian LNG Project — Royal Dutch Shell (RDS.A, RDS.B) is pressing ahead with Canada’s largest-ever infrastructure project, designed to send gas from Canada, where prices are relatively low, to demand centers in Asia. Construction of the 14M tons/year venture – which is expected to generate an internal rate of return of around 13% – will start immediately, with LNG production expected to begin before the mid-2020s. Minority partners include PetroChina (NYSE:PTR), Mitsubishi (OTCPK:MSBHY), Korea Gas and Malaysia’s Petroliam Nasional Bhd.

4. U.S. and Canada Reach Last-Minute Pact to Revise Nafta — the U.S. and Canada struck a deal at the last minute to revise the North American Free Trade Agreement just before a U.S-imposed deadline of October 1. The pact allows Canada to join the accord reached between the U.S. and Mexico in August. The new agreement, to be officially called the U.S.-Mexico-Canada Agreement, now includes rules for financial services and digital business that have emerged since Nafta was originally signed in 1994. Canada agreed to curb protection for its dairy industry, while the U.S. dropped demands to get rid of special Nafta courts that allow member states to challenge trade restrictions imposed by others.

5. AAII Weekly Sentiment Survey — According to the weekly sentiment survey from AAII, bullish sentiment surged 9.4 percentage points to 45.66% from last week’s reading of 36.22%.

That move represents the largest one-week increase since early July and the highest weekly reading since mid-February. While we’re not quite at the 50% reading yet, we would note that the last time optimism in this survey neared the 50% level was in late December. That wasn’t the exact top of the market right before the correction, but it was close to it.

bearish sentiment is back down in the mid-20 percent range, which is a level it has seen repeatedly throughout the year.

6. Chinese Spy Chip Report Weighs on Apple Suppliers — shares in Apple’s suppliers saw a broad decline on the back of a bombshell report that alleged Chinese spy chips were discovered in data center equipment used by Amazon (NASDAQ:AMZN) and Apple (NASDAQ:AAPL). The tech giants have denied the allegations by Bloomberg Businessweek, which said the hack reached almost 30 U.S. companies and compromised America’s technology supply chain. Companies effected are: AMS,Largan, LG Display, Murata, Wistron, Hon Hai, AAC Tech, Merry, TDK, TSMC .

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 3rd, 2018

“Prices are too high” is far from synonymous with “the next move will be downward.” Things can be overpriced and stay that way for a long time . . . or become far more so.” ― Howard Marks

1. Brent Crude Spikes to Fresh Four-Year High Near $81/bbl — brent crude jumped to its highest in four years overnight after the world’s biggest oil producers, led by Saudi Arabia and Russia, decided against further increases in production, despite calls from Pres. Trump for OPEC to lower prices. At its last meeting in Algiers, OPEC said it was satisfied “regarding the current oil market outlook, with an overall healthy balance between supply and demand.” Brent spiked as much as 2.6% higher to $80.94 per barrel to its loftiest levels since 2014, while U.S. WTI climbed 1.8% to $72.06 per barrel, its highest since this June.

2. EU Plans Route To Do Business with Iran Without U.S. Sanctions — the EU will establish a special payment channel allowing companies to legally continue financial transactions with Iran without exposure to U.S. sanctions. The mechanism would facilitate payments related to Iranian oil trade, exports, and imports. The details of the mechanism will come after future meetings with technical experts. The special purpose vehicle was jointly announced by EU foreign policy chief Federica Mogherini and Iranian Foreign Minister Javad Zarif.

3. Ontario Expected to Unveil Cannabis Law — expectations on Ontario that a new legalization law will be unveiled on Sept 28 ’18. Ontario is the only province that hasn’t created guidelines for how cannabis will be sold in brick-and-mortar retail shops, despite the province accounting for more than 40% of all cannabis usage in the nation last year. An announcement isn’t anticipated until after the market closes today, which could lead to more speculative trading on Aurora Cannabis (OTCQX:ACBFF), Canopy Growth (NYSE:CGC), Cronos Group (NASDAQ:CRON) and Tilray (NASDAQ:TLRY).

4. SEC Sues Elon Musk For Fraud, Seeks Removal from Tesla — the SEC sued Elon Musk for fraud and sought to remove him from Tesla Inc(TSLA). It sued Mr. Musk in Manhattan federal court, alleging he “had not even discussed, much less confirmed, key deal terms, including price, with any potential funding source,” according to the lawsuit. U.S. law forbids public-company executives from making false statements or misleading investors about information that is material to an investment decision.

5. U.S., Japan Agree to Trade Talks; Japan Avoids U.S. Auto Tariffs For Now — President Trump and Japanese Prime Minister Abe have agreed to start trade talks in an arrangement that for now protects Japanese automakers from further tariffs. As part of the agreement, Abe said the U.S. would not impose additional tariffs on the auto sector, while also protecting the politically important farm sector from access that goes beyond the terms in the Trans-Pacific Partnership agreement that Trump abandoned last year. U.S. Trade Representative Lighthizer said the talks would occur in two “tranches” with hopes for an “early harvest” from the initial talks on lowering trade barriers.

The week ahead — Economic data from Econoday.com:

Tags: Canabis

Posted in Weekly Summary | No Comments »

September 24th, 2018

“Always something new, always something I didn’t expect, and sometimes it isn’t horrible.” – Robert Jordan

1. U.S. LNG Deliveries to Germany by 2022 — U.S. companies expect to begin delivering LNG to Germany in four years at the latest, according to deputy U.S. energy secretary Dan Brouillette, and will challenge Russia which now accounts for 60% of German gas imports. In July, President Trump accused Germany of being a “captive” of Russia due to its energy reliance and urged it to halt work on the $11B, Russian-led Nord Stream 2 gas pipeline.

2. Aurora Cannabis(OTCQX:ACBFF) on talks with Coca-Cola on CBD drinks — Coca-Cola (NYSE:KO) said it was closely watching the fast-growing marijuana drinks market for a possible entry. Molson Coors (NYSE:TAP) has already announced a joint venture with Hydropothecary to develop cannabis drinks, while Diageo (NYSE:DEO) is in talks with at least three Canadian cannabis producers about a possible deal.

3. SEC subpoenas Goldman, Silver Lake in Tesla probe — the tension continues to build at Tesla (NASDAQ:TSLA) as a DOJ probe runs alongside a wide-ranging SEC investigation. Subpoenas have already been received by Goldman Sachs and Silver Lake, the two firms hired by Tesla to help the company explore Elon Musk’s go-private plan.

4. US/China Tarriff Escalate — President Trump ordered another $200 billion in 10% tariffs on Chinese goods, which could rise to 25% by year end. China retaliated with $60 billion in tariffs at 5% to 10% and Trump threatened $267 billion more.

5. AAII Weekly Investor Sentiment — in the latest survey of individual investor sentiment from AAII, bullish sentiment declined (ever so slightly) for the third straight week, dropping from 32.09% down to 32.04%.

Meanwhile, bearish sentiment came in at the exact same level as bullish sentiment this week, dropping from 32.84% down to 32.04%. The last time both gauges of sentiment were at the exact same level was in June 2016.

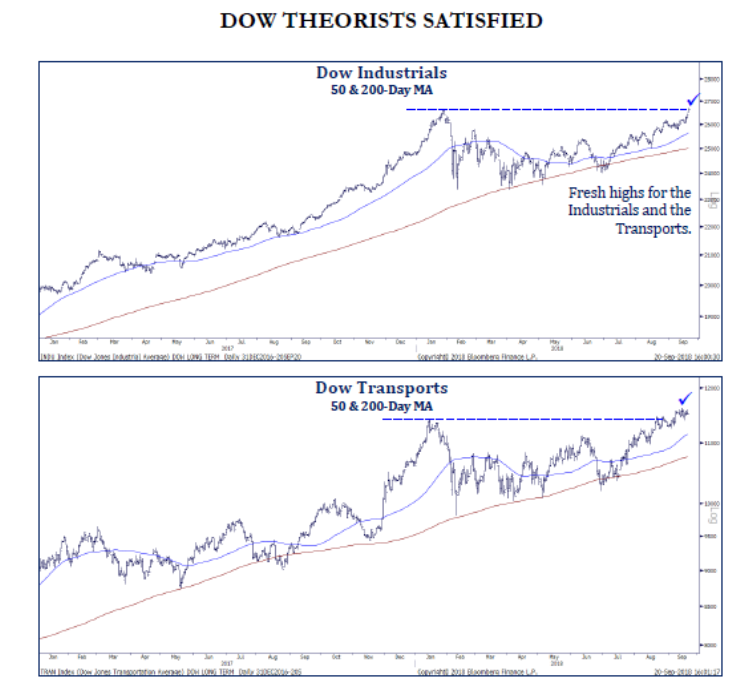

6. Dow Theory Generates Buy Signal for the Dow Theorist Followers — this occurs when the Dow Industrials sets a new high following a new high for Dow Transports. This happened over the last two weeks as industrials set their high on September 21 following transports on September 14. This signal did not work in 2008 as Dow Transports was the last average to peak when it topped out in May 2008 while Dow Industrials peaked in October 2007.

The week ahead — Economic data from Econoday.com:

Tags: AAII Weekly Sentiment, US/China Trade War

Posted in Weekly Summary | No Comments »