May 21st, 2019

“The market is a device for transferring money from the impatient to the patient.”– Warren Buffet

1. U.S. Telecoms Prepare for Huawei Ban — paving the way for a ban on doing business with China’s Huawei, President Trump signed an executive order barring American companies from using telecom equipment made by firms posing a national security risk. The order would invoke the International Emergency Economic Powers Act and comes at a delicate time in relations between Beijing and Washington, with the two ratcheting up tariffs over what U.S. officials call China’s unfair trade practices.

2. Trade War Sees U.S. farmers Get $15B in Aid — the Trump administration is planning on providing about $15B in aid to help U.S. farmers whose products may be targeted by the newly unveiled Chinese tariffs. The group has been among the hardest hit in the trade war, with U.S. soybean futures falling to their lowest in a decade on Monday and shipments of the most valuable U.S. farm export to China dropping to a 16-year low in 2018. A new aid program would be the second round of assistance for American farmers, after the Department of Agriculture’s $12B compensation plan last year.

3. Teva, Drugmakers, Accused of Price-Fixing — forty-four U.S. states have filed a lawsuit accusing Teva Pharmaceuticals (NYSE:TEVA) of orchestrating a sweeping scheme with 19 other drugmakers to inflate drug prices – sometimes by more than 1,000% – and stifle competition for generic medicines. “We take these accusations seriously and we are going to defend ourselves,” CFO Mike McClellan declared. Soaring drug prices from both branded and generic manufacturers have sparked outrage across the political spectrum, from Republicans and Democrats alike.

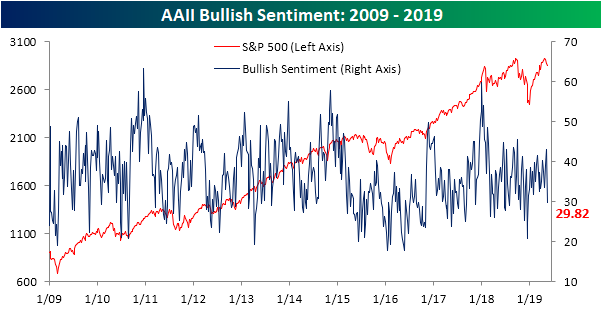

4. AAII Weekly Sentiment — One week after coming in at its highest level since October, bullish sentiment has fallen off of a cliff this week to 29.82% versus 43.12% last week. From a historical perspective, this is not at any kind of extreme, but it did bring optimism to its lowest level of 2019 and by a pretty wide margin at that. Additionally, this was the largest drop in bullish sentiment since December 13th of last year when it fell 17.04% in a week.

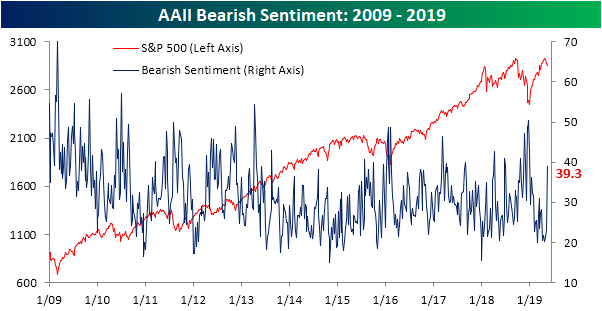

Bearish sentiment spiked up to 39.3% from 23.19% last week. While this was a massive spike higher, it is still well off of any sort of extreme, and we actually saw higher readings late last year. Investors Intelligence is echoing the AAII results, as that survey showed the highest percentage of respondents since February (31.1%) expecting a correction. Granted, bearish sentiment in this survey remains muted, as it actually fell to its lowest level since April of last year.

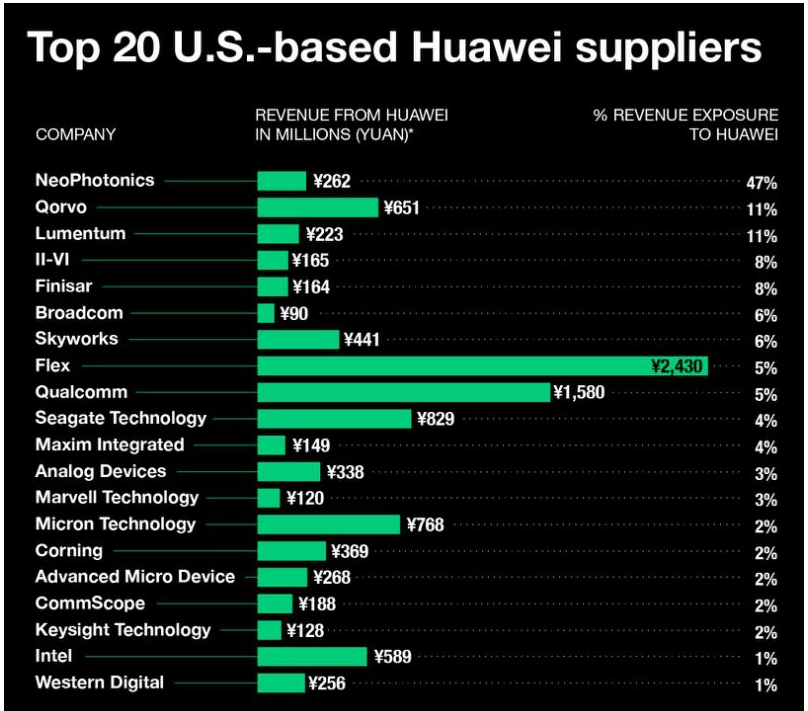

5. Chip Makers Get Caught in Huawei Crossfire — WSJ, following the ban on Huawei, chip companies selling technology to the Chinese communications equipment giant must be granted a special license to do so. Among the hardest-hit chip stocks Thursday were Qualcomm , Broadcom , Qorvo and Skyworks Solutions —key makers of modem and radio-frequency processors used in smartphones. Xilinx is affected as well given its growing business in 5G equipment. Shares of memory suppliers Micron Technology and SanDisk parent Western Digital also slipped in the decision’s aftermath. Below shows a list of US companies effected by the ban.

The week ahead — Economic data from Econoday.com:

Tags: Huawei Ban

Posted in Weekly Summary | No Comments »

May 7th, 2019

“Letting losses run is the most serious mistake made by most investors.” – William O’Neil

1. Tesla to Slash Solar Panel Prices by 38% — losing its status as the nation’s leading rooftop solar company last year, Tesla (NASDAQ:TSLA) announced plans to begin selling solar panels and related equipment for up to 38% below the national average price, NYT reports. This will be achieved by standardizing systems and requiring customers to order them online. Homeowners will also photograph electric meters and send the images to the company, reducing the need for site visits.

2. Boeing CEO to Pitch 737 Max Comeback — Boeing (NYSE:BA) CEO Dennis Muilenburg held his first press conference since the worldwide grounding of the 737 MAX, which led to investigations, lawsuits and a sharp loss in shareholder value. While reports over the weekend suggested that pilots have warned draft 737 MAX training proposals did not go far enough to address their concerns, the FAA may clear the plane to fly in late May or the first part of June.

3. FOMC Meeting Recap— Fed officials agreed to hold their benchmark interest rate steady and signaled comfort that their wait-and-see posture had steadied the economy. the Fed refused to signal anything other than that it was still on pause, while Chair Jerome Powell said the factors dragging on inflation might be “transitory,” not “persistent.”

4. Merck Steps Up Meales Vaccine Production — Merck (NYSE:MRK), the sole U.S. supplier of measles vaccines, has increased output to meet an uptick in U.S. demand amid the country’s biggest outbreak in 25 years. “The demand side of the equation hasn’t been outstripping our underlying capacity,” Chief Marketing Officer Mike Nally said in an interview. The CDC reported 704 cases of measles as of April 26, a 1.3% increase since the 695 reported the week before, with the vast majority of cases occurring in children who have not received the MMR vaccine.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 29th, 2019

“The speculator’s chief enemies are always boring from within. It is inseparable from human nature to hope and to fear. In speculation when the market goes against you hope that every day will be the last day – and you lose more than you should had you not listened to hope – the same ally that is so potent a success-bringer to empire builders and pioneers, big and little. And when the market goes your way you become fearful that the next day will take away your profit, and you get out – too soon. Fear keeps you from making as much money as you ought to. The successful trader has to fight these two deep-seated instincts . . . Instead of hoping he must fear; instead of fearing he must hope.” — Jesse Livermore

1 Occidental Seeks to Buy Anadarko for $38 Billion, Topping Chevron’s Offer — Occidental Petroleum Corp. (OXY) offered to buy Anadarko Petroleum Corp. (APC) for $38 billion, launching a potential bidding war for a company that previously agreed to be purchased by Chevron Corp. (CVX) for about $33 billion.

2. Chip Stocks Volatile After TI, STM — Texas Instruments (NASDAQ:TXN) lost its post-earnings gains after the CFO said the cyclical downturn was likely still in its early stages. European semi peer STMicroelectronics (NYSE:STM) reported Q1 misses and said lower-than-expected FY19 plans would be addressed with inventory adjustments and spending cuts. European chip stocks shook off early losses, but the U.S. sector could still have a volatile day as investors seek clearer sector visibility.

3. Boeing Details Financial Hit From 737 MAX Grounding — The aerospace giant said that it was taking an initial hit of more than $1 billion while the plane is grounded and production of additional aircraft remains scaled back. Mr. Muilenburg, CEO said the Federal Aviation Administration would soon conduct certification flights to test the 737 MAX’s updated software, a key step to restarting commercial flights. Boeing is also working with airlines and pilots to restore trust among fliers. the plane maker reported first-quarter earnings of $2.15 billion. The profit demonstrated the resilience of Boeing’s broader portfolio, with sales of 787s and other jetliners as well as services and military hardware limiting the decline.

However, the company said it would suspend the huge share buybacks that have propelled its share price over the past three years and it dropped full-year profit and sales guidance for 2019.

4. Bank of Japan Leaves Policy Unchanged — the Bank of Japan left policy unchanged, as most economists expected, maintaining its policy balance rate at -0.1% and guiding to keep extremely low interest rates until at least spring 2020. That’s putting a date to policy guidance it had previously just said it would keep for an “extended period.” The BOJ’s target for the 10-year government bond yield is zero, and for the first time the bank projected economic growth for the year ending March 2022 (it expects 1.2% growth then). It sees core CPI rising at 1.6% in fiscal 2021; time’s running out for Gov. Haruhiko Kuroda to hit a 2% inflation rate before his term expires in 2023.

5. Japan Trade Talks Kick Off — U.S. Treasury Secretary Steven Mnuchin is scheduled to meet with Japanese Finance Minister Taro Aso to discuss provisions against currency manipulation and other trade issues. Economy Minister Toshimitsu Motegi is also set to meet with U.S. Trade Representative Robert Lighthizer to negotiate trade issues that could impact automobile manufacturers Honda (NYSE:HMC), Toyota (NYSE:TM), Mazda (OTCPK:MZDAY) and Nissan (OTCPK:NSANY). The meetings precede the planned summit between Prime Minister Shinzo Abe and President Donald Trump later in the week.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 22nd, 2019

“When you talk, you are telling people what you already know. When you listen, however, that’s how you learn something new.” — Dalai Lama

1. Deutsche Bank Subpoenaed Over Trump Business — Congressional investigators have subpoenaed Deutsche Bank (NYSE:DB) as Democrats step up their probes into President Trump and his longtime lender. The subpoenas from the U.S. House of Representatives Intelligence and Financial Services committees mark an escalation of Democratic-led probes into Trump’s business dealings. The committees also subpoenaed multiple other financial institutions, including JPMorgan (JPM), Bank of America (BAC) and Citigroup (C) as part of their investigations.

2. U.S.-China Trade Talks Near Final Round — U.S. Treasury Secretary Steven Mnuchin said a U.S.-China trade agreement would go “way beyond” previous efforts to open China’s markets to American companies and the two sides were “getting close to the final round of concluding issues.” “This is way beyond anything that looked like a bilateral investment treaty,” he added. U.S. negotiators have also reportedly tempered demands that China curb industrial subsidies as a condition for a trade deal after strong resistance from Beijing.

3. U.S., Turkey Deadlock over Russia Missile Dispute Continues — the U.S. and Turkey have failed to break their impasse over Turkey’s plan to deploy a Russian air defense system the Pentagon says could jeopardize U.S. fighter aircraft including Lockheed Martin’s (NYSE:LMT) F-35, which Turkish manufacturers helped build. Turkish officials repeated that the deal with Russia has been signed and is final, while the U.S. has threatened to impose sanctions under legislation that allows the punishment of entities doing business with Russia, and to expel Turkey from the F-35 program. The first batch of Russian S-400 missiles may be delivered as early as June.

4. Qualcomm, Apple Drop All Litigation — Qualcomm (NASDAQ:QCOM) and Apple (NASDAQ:AAPL) agreed to dismiss all litigation worldwide in a settlement that involves Apple paying QCOM. The companies also reached a six-year license agreement, effective April 1, with two one-year option periods plus a multiyear chipset supply agreement. In a regulatory filing Qualcomm says it expects incremental EPS of about $2 as product shipments ramp up.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 15th, 2019

“One of the frustrating things for people who miss the first rally in a bull market is that they wait for the big correction and it never comes. The market just keeps climbing and climbing. It feeds on itself in frenzied fashion and propels prices considerably higher for six months or so, and sometimes longer.” — Martin Zweig

1. China Wants to Eliminate Bitcoin Mining — China’s state planner has labeled Bitcoin (BTC-USD) mining as an “undesirable” industry in a draft proposal, recommending local governments eliminate the sector in the country. The public will have until May 7 to share feedback on proposed amendments, after which the final version will be published and become effective. Last week, the price of Bitcoin soared nearly 20% in its best day since the height of the 2017 bubble, breaking $5,000 for the first time since mid-November.

2. EU Leaders to Grant the U.K. Deadline to Oct. 31 — Theresa May managed to convince EU leaders to grant the U.K. more time before it leaves the bloc, extending the deadline to Oct. 31, but some experts are now saying her days in office are numbered. “A six-month period is clearly enough for the Conservative Party to contemplate a change in leadership while still allowing some time for the incoming PM to seek to negotiate with the EU,” JPMorgan economist Malcolm Barr said in a research note. “One could even cram a general election into that time frame too if PM May were to resign by roughly the end of May.”

3. Tesla Gigafactory Expansion Freeze — Tesla (NASDAQ:TSLA) and Panasonic (OTCPK:PCRFY) are suspending plans to expand the capacity of their $4.5B U.S. plant in the face of uncertain demand for electric vehicles, the Nikkei reports. The two had intended to raise capacity 50% by 2020 to the equivalent of 54 gigawatt-hours, but financial problems forced a re-think. Panasonic also intends to suspend planned investment in Tesla’s battery and EV plant in Shanghai, and instead provide technical support and a small number of batteries from the existing Gigafactory.

4. Chevron to Buy Anadarko in $33B Cash and Stock Deal — Chevron (NYSE:CVX) plans to acquire Anadarko Petroleum (NYSE:APC) in a stock and cash transaction valued at $33B, or $65 per share, enhancing its Upstream portfolio and strengthening its shale, deepwater and natural gas resource basins. Anadarko shareholders will receive 0.3869 shares of Chevron and $16.25 in cash for each APC share. The deal anticipates annual run-rate synergies of approximately $2B, and will be accretive to free cash flow and earnings one year after close. If approved, Chevron said it also plans to boost its annual share buyback program to $5B from $4B.

5. EU Green Lights U.S. Trade Talks — Europe is set to start trade talks with the U.S. after EU ambassadors gave a green light to a proposed mandate for the European Commission to conduct the negotiations on behalf of the 28 EU member countries. The talks commence despite opposition from France, which expressed concerns over the U.S. intention to withdraw from the Paris Agreement on climate change. EU ministers still need to give their rubber stamp, which is due on April 15.

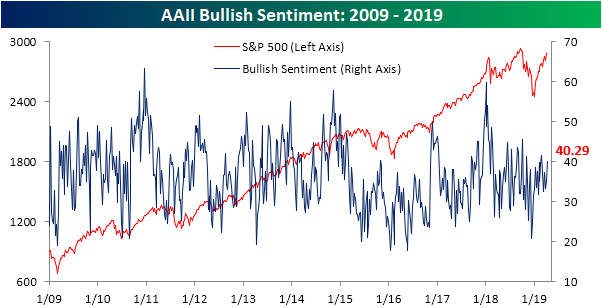

6. AAII Weekly Investor Sentiment Survey — AAII Weekly Sentiments the results are very similar to the final days of February with bullish sentiment around 40%, bearish down near 20%, and neutral once again in the upper 30’s. Up from 35.02% last week, bullish sentiment has crossed back over the 40% threshold; the first time it has done so since the previously mentioned week in February.

While bullish sentiment is sitting a couple of points above the historical average, this is still several percentage points from reaching any sort of extreme level (more than one standard deviation above the aforementioned average).

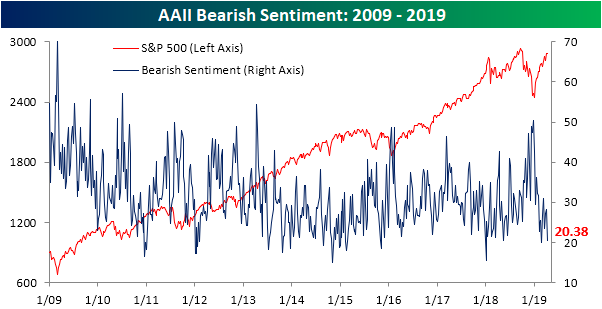

Bearish sentiment, on the other hand, fell all the way back down to 20.38% this week, the lowest since its 20% reading on February 28th. That is around 10% less than the historical average for bearish sentiment. That is also at the lower end of the range bearish sentiment has stayed within in the past decade.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 8th, 2019

1. Boeing Admits MCAS Played Role in 737 Max Crashes — “With the release of the preliminary report of the Ethiopian Airlines flight 302 accident investigation it’s apparent that in both flights the Maneuvering Characteristics Augmentation System, known as MCAS, activated in response to erroneous angle of attack information,” Boeing (NYSE:BA) CEO Dennis Muilenburg said in a statement. However, an update will “add additional layers of protection and will prevent erroneous data from causing MCAS activation. Flight crews will always have the ability to override MCAS and manually control the airplane.”

2. Tesla Deliveries Tumble 31% — the EV maker reported a 31% drop in Q1 deliveries to 63K vehicles (51K Model 3 and 12K Model S and X). While sales were hit by a reduction in U.S. federal tax credits and by difficulties in delivering to Europe and China, Tesla said it finished the quarter with “sufficient” cash. The automaker also reaffirmed its full-year forecast of 360K to 400K deliveries, but investors are asking if that big increase will be possible.

3. 5G Era for Smartphones Has Begun — Verizon (NYSE:VZ) has launched 5G wireless service in parts of Chicago and Minneapolis, while carriers in South Korea – SK Telecom (NYSE:SKM) and KT Corp. (NYSE:KT) – deployed their service in the Seoul metropolitan area. To access the network, Verizon subscribers for now will be limited to the Motorola Z3 (with an accessory clip-on), while Korean early adopters will have to use Samsung’s Galaxy S10. 4G helped reshape the way people hail taxis and order takeout and the mobile industry is hoping the faster speeds provided by 5G will enable self-driving cars, smart cities and will birth immersive digital worlds.

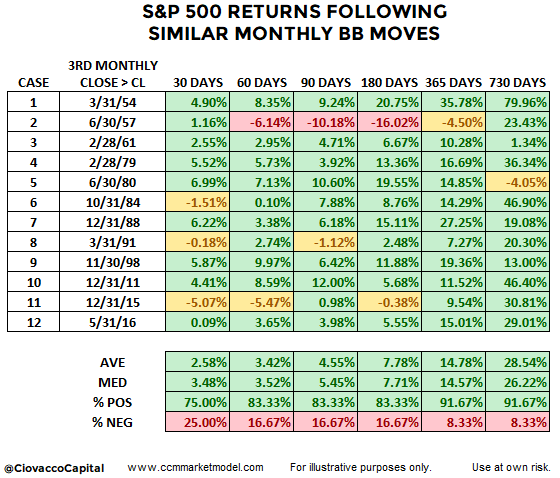

4. Third Consecutive Monthly Close Statistics — the S&P 500 (SPY) closed above the monthly Bollinger Band centerline at the end of January, it aligned the present day with favorable historical probabilities and also provided some distance from setups in the 1974, 2001, and 2008 bear markets. Twelve of the 13 similar historical cases, covered on Feb. 20, also went on to print three consecutive closes above the monthly Bollinger Band centerline. The exception was the 6/30/1960 case, which gave up the centerline in the second month. The table below shows S&P 500 (VOO) performance in the remaining 12 historical cases following the third consecutive close above the monthly Bollinger Band centerline (similar to what occurred at the end of March 2019).

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 3rd, 2019

“When investors hear yield curve inversion, they automatically think ‘recession.’ That’s because every recession since 1962 has been preceded by an inversion. But, not every inversion has been followed by a recession, so keep that in mind.” — BIG

1. DOJ Moves to Strike Down Entire ACA — the U.S. Department of Justice has filed a motion calling for ObamaCare to be struck down in its entirety, siding with a Texas federal district court that had decided the individual mandate was unconstitutional. Hospital and health insurer stocks plunged following that ruling in December. Previously the DOJ was focused on eliminating mandatory coverage for people with pre-existing conditions, but under Attorney General William Barr the federal government’s position has now changed.

2. Aaple Unveils New Products — Apple Inc. (AAPL) unveiled new products for entertainment, financial services, news and videogames last week to extend push into new territory. It plans to make its TV app, which will carry that content, available on competitors’ televisions and other devices as well as its own. Apple also announced Apple Card, a mainly digital credit card launched in partnership with Goldman Sachs Group Inc. that aims to challenge incumbents by offering low interest rates and eliminating both late fees and annual fees. In addition, It unveiled Apple News+, a $9.99 monthly service that provides access to 300-plus magazines as well as newspapers, including The Wall Street Journal through an agreement with parent Dow Jones & Co. And it showed off Apple Arcade, a gaming subscription service offering access to 100-plus exclusive games for an unspecified monthly fee.

3. U.K. Parliament Fails to Get a Majority On Any Brexit Option — U.K. Prime Minister Theresa May pledged to quit in a bid to salvage her deal to leave the EU, but the move appeared to backfire as her political ally, Northern Ireland’s Democratic Unionist Party, said it would continue to reject her agreement. Lawmakers also failed to find a majority for any alternative Brexit arrangement to May’s pact, but overwhelmingly agreed that they opposed leaving the bloc without one. Britain has until April 12 to agree on a strategy./>

4. Lyft Prices IPO at $72/Share — tt’s the first IPO in the ride-hailing market ticker “LYFT,” and the first in a string of tech companies that are planning to go public in 2019. With over $2B raised so far, Lyft priced shares at $72 (at the high end of its range), putting its valuation at over $24B.

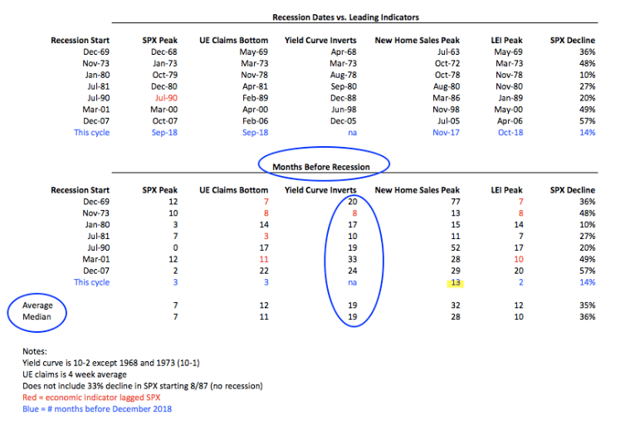

5. Yield Curve Inversion Statistics — based on the recent media chatter about the Yield Curve Inversion, the graph below shows that the standard 10yr/2yr yield curve has inverted on average 19 months before a recession, going back to 1968, whereas a top in the SPX has preceded recession by only an average of 7 months.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

March 25th, 2019

“I always define my risk, and I don’t have to worry about it.” – Tony Saliba

1. France ‘Yellow Vest’ Protests Flare Anew — as a series of national French debates on government policy ended last week, “Yellow Vest” protesters celebrated their 18th weekend with violence on the streets of Paris. More than 80 businesses on the Champs-Elysees were vandalized or torched, with an estimated 10,000 people participating in the demonstrations. The protests have shaved 0.2 percentage points off economic growth since they started, Finance Minister Bruno Le Maire said in late February.

2. Apple is Poised to Unveil its Long-Rumored TV Service — Apple is poised to unveil its long-rumored TV service, and ahead of the event, Netflix (NASDAQ:NFLX) confirmed it won’t be joining the company’s streaming offering. “While Apple (NASDAQ:AAPL) is a great company, we prefer to let our customers watch our content on our service,” CEO Reed Hastings told reporters at the company’s offices in Hollywood.

3. The U.S. Air Force Outlined a Five-Year Plan to Bring back Boeing’s F-15 Fighter — the U.S. Air Force has outlined a five-year plan that showed the extent of the Pentagon’s push to bring back Boeing’s (NYSE:BA) F-15 fighter in an upgraded version. The $7.8B investment would see a jump in eight of the planes next year to 18 each year through 2024. While Lockheed Martin’s (NYSE:LMT) F-35 would get $37.5B over the five years, the more advanced plane would still take a hit (48 F-35s are planned to be purchased each year from fiscal 2021-2023 instead of the 54 previously planned).

4. Britain Says EU Could Offer Brexit extension — the European Union decided to give the United Kingdom an extension on negotiating an exit from the EU – but it won’t be a long reprieve if UK Prime Minister Theresa May can’t get a win in Parliament. European Council President Donald Tusk said Article 50 would be extended to May 22 if Parliament can reach a withdrawal agreement next week; but failing that, the deadline is extended only to April 12.

5. FOMC Meeting Announcement — the Fed decided to hold interest rates steady, as expected, and indicated it would keep rates at current levels for the rest of 2019. The central bank currently holds its benchmark funds rate in a range of 2.25 percent to 2.5 percent. Speaking after the Fed’s decision, Powell said that weakening Chinese and European economies are acting as a deterrent to growth at home even as policymakers see the overall outlook in the U.S. as good. Fed Chairman Jerome Powell also announced that the central bank would end the so-called runoff of bonds from its balance sheet sooner than most expected. That caused the yield on the 10-year Treasury to tumble.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

March 18th, 2019

“The key to trading success is emotional discipline. If intelligence were the key, there would be a lot more people making money trading… I know this will sound like a cliche, but the single most important reason that people lose money in the financial markets is that they don’t cut their losses short.” — Victor Sperandeo

1. Trump’s Budget Proposal Features $8.6B for Wall, Increased Defense Spending — the White House proposed a $4.7T fiscal 2020 budget that called for cutting regular non-defense discretionary spending by 9%, while increasing defense spending and including $8.6B for a border wall. Under the blueprint, the budget doesn’t balance in 10 years and shows a $202B deficit in 2029, assuming economic growth at an average of 3% for the decade. The proposal is likely to be dismissed by Congress and increases the threat of another government shutdown in the fall.

2. Boeing Grounds Global 737 MAX Fleet — Boeing has decided to temporarily suspend its entire fleet of 737 MAX planes “out of an abundance of caution and in order to reassure the flying public of the aircraft’s safety.” The FAA reversed course and grounded the jet after evidence emerged showing a flight that crashed in Ethiopia may have experienced the same problem as a plane that went down five months ago off Indonesia. Analysts say the initial impact of the grounded Boeing (NYSE:BA) jets will be contained, but may escalate if the fleet is not permitted to fly for a longer period.

3. UK Parliament Rejects a Second Brexit Referendum — U.K. lawmakers voted to delay Britain’s departure from the EU, sending Theresa May back to Brussels to request an extension. Her pact with the trading bloc is also expected to be voted on in the House of Commons for a third time next week, after being soundly rejected twice. Parliament further blocked a motion yesterday seeking a second Brexit referendum, though Labour leader Jeremy Corbyn said his team is still working on plans for another public vote.

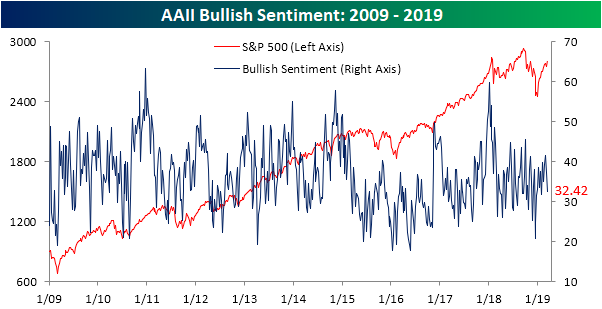

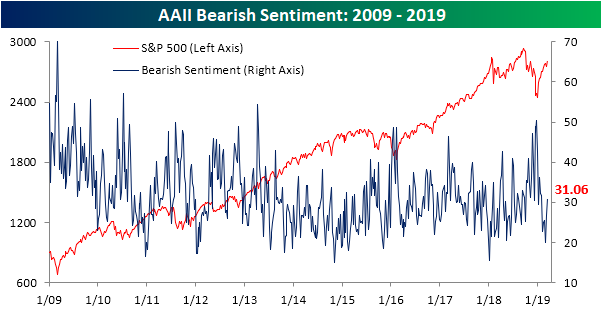

4. AAII’s Weekly Survey of Individual Investors — in the latest Bullish sentiment, it shows another drop in bullish sentiment. This comes following the first weekly decline that equities have seen so far in 2019. The percentage of investors expressing optimism dropped to 32.42% from 37.39% last week. The week prior to that was a recent high, and the highest since early November, at 41.63%.

Conversely, bearish sentiment rose to its highest level since the final days of January coming in at 31.06% versus 26.75% last week. Bearish sentiment has come well off of its lows of 20% only a couple of weeks ago. Where it currently sits is much more in line with its historic average of 30.5%.

5. Tesla Announced Model Y Event — Completing the EV lineup that Elon Musk has dubbed “S3XY,” Tesla (NASDAQ:TSLA) took the wraps off its Model Y, with prices starting at $39,000. The crossover is larger than the entry-level Model 3 but smaller than the Model X, Tesla’s full-size SUV. With a 0-to-60 mph acceleration time of 3.5 seconds and a standard range of 230 miles, the first Model Ys are due for release in fall 2020.

The week ahead — Economic data from Econoday.com:

Tags: BA Grounds 737 Max Fleet

Posted in Weekly Summary | No Comments »

March 12th, 2019

“If it stinks, doesn’t work, is incomprehensible and doesn’t make sense – it’s either economics or philosophy.” — . . . Raymond DeVoe

1. Moody’s Upgrade Greek Debt — Moody’s disclosed a two-notch upgrade (to B1 from B3) on the country’s sovereign debt rating. The nation’s reform program is now “firmly established and is likely to be sustained,” according to the agency, as “most of the fiscal improvement is due to structural measures.” Greek 10-year bond yields fell to their lowest level since early 2006, down 3.3 bps to 3.609%.

2. U.K. Crucial Votes Next Week — crucial votes are scheduled in the U.K. next week that will determine the immediate course of Brexit and the U.K.’s relationship with the EU. If lawmakers vote against Prime Minister Theresa May’s Brexit deal, they will then vote on leaving the 28-member bloc without a deal (hard Brexit). JPMorgan doubts May can achieve victory at this stage, predicting an extension of Article 50 by two or three months with May securing passage of the deal by early April. May and other Brexit officials are in Brussels in a last-ditch effort to score more concessions from European Union leaders before the key votes.

3. Huawei Sues U.S., Calling Equipment Ban Unconstitutional — Huawei has filed suit against the United States, claiming that a ban on government procurement from the world’s largest network equipment maker is unconstitutional. The part of the National Defense Authorization Act with the ban makes it a “bill of attainder,” Huawei says – an unconstitutional singling-out of a group or individual without due process. A court could invalidate just the section involving Huawei, but expect a national security defense to come up.

4. FDA OKs J&J’s Esketamine Nasal Spray for Depression — the FDA has approved the first drug to treat depression in decades, paving the way for Johnson & Johnson (NYSE:JNJ) to sell a nasal spray based on ketamine, which is often used as a party drug with the nickname “Special K”. Esketamine, which will be sold under the brand name Spravato, will be available for adults who have already tried at least two other antidepressant treatments. The fast-acting drug will cost between $590 and $885 (before discounts and rebates) depending on the dosage.

5. German Factory Orders Slump — German factory orders unexpectedly fell in January, adding to the evidence that Europe’s largest economy is continuing to lose momentum. Orders were down 2.6%, the most since June, defying expectations for a 0.5% gain. The Bundesbank’s latest assessment is that Germany is seeing a dent in momentum and that growth this year will be below potential (the economy barely avoided a recession at the end of 2018).

6. Trump Administration Exploring Price Disclosure Requirement for Hospitals and Doctors — the Trump administration is reaching out to the medical industry for feedback on requiring hospitals, doctors and other healthcare providers to publicly disclose the heretofore confidential prices they charge insurers for services. Needless to say, health insurers, hospitals and most doctors will most certainly push back on the proposal. The public comment period will close Friday, May 3.

The week ahead — Economic data from Econoday.com:

Tags: JNJ Depression Nasal Spray

Posted in Weekly Summary | No Comments »