July 29th, 2019

”Money cannot consistently be made trading every day or every week during the year” — Jesse Livermore

1. Brexit Leader Boris Johnson Wins Race for UK Prime Minister — Boris Johnson, the former foreign secretary and mayor of London who has pledged to take Britain out of the European Union on Oct. 31, is set to become British prime minister after winning the leadership of the ruling Conservative Party. His anointment will herald a period of intense political and economic uncertainty for the U.K., with the prospect of a sudden break from the EU and questions about how long his minority government will last.

2. Congress Moves Toward Ban on Buying Chinese Buses, Railcars Over Spy Fears — China’s push to gain a bigger foothold in U.S. public transit systems could derail in Congress, which is moving to bar use of federal funds to buy Chinese buses and railcars. The effort threatens to further fray trade talks with China, which wants to become a global player in transport and is already fuming over the U.S. decision to blacklist telecommunications giant Huawei Technologies Co. The U.S. House of Representatives passed its version of an annual defense-policy bill July 12 with language blocking transit agencies from using federal money to buy railcars made by Chinese state-owned, -controlled or -subsidized companies.

3. UPS to Join FedEx in Starting Seven-Day Delivery; Launches Drone Business — United Parcel Service (NYSE:UPS) will start delivering packages on Sundays starting in January, following FedEx’s (NYSE:FDX) announced move to seven-day delivery as the two work to meet the demands of online shopping. UPS also announced a new drone delivery subsidiary called UPS Flight Forward and said it has applied for FAA certifications needed to expand the business. Those would allow drone flights beyond an operator’s visual line of sight, at night and without limit to the number of drones or operators in command.

4. SK Hynix Cutting DRAM Production, NAND Input — SK Hynix (OTC:HXSCF,OTC:HXSCL) plans to cut its DRAM production capacity from Q4 due to the demand environment and tech migration. The company will also reduce its NAND wafer input by more than 15%, up from its previous plans to cut input 10% compared to last year. Competitors in these spaces include Micron (NASDAQ:MU), Intel (NASDAQ:INTC), and Western Digital (NASDAQ:WDC).

5. ECB Signals Rate Cut, Possible Stimulus Relaunch — the European Central Bank signaled it is preparing to cut short-term interest rates for the first time since early 2016 and possibly restart its giant bond-buying program. The ECB said in a statement Thursday that it expects to keep its key interest rate at its current level of minus 0.4% or lower through the first half of 2020, a clear signal that it is planning a rate cut.

The economic outlook “is getting worse and worse,” especially in manufacturing, ECB President Mario Draghi said at a press conference. “Basically we don’t like what we see on the inflation front.”

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

July 23rd, 2019

“Skate To Where The Puck Is Going To Be” — Wayne Gretzky

1. 737 MAX Woes Hobble Budget Carrier Ryanair — Ryanair (NASDAQ:RYAAY) is taking the knife to its operations in Europe, blaming possible further delivery delays of Boeing’s (NYSE:BA) 737 MAX planes. It’s planning to cut back service at some airports and abandon others entirely because regulators may not return the grounded MAX to service until as late as December. Ryanair had planned its flight schedule based on the delivery of 58 of the aircraft by summer 2020, but Europe’s biggest budget carrier, which can only take delivery of up to eight aircraft per month, now expects to receive only 30. In addition, American Airlines (NASDAQ:AAL) has extended Boeing (NYSE:BA) 737 MAX cancellations for the fourth time, but “remains confident that impending software updates, along with the new training elements, will lead to recertification of the aircraft this year.” That’s despite being the next MAX operator to extend cancellations into early November.

2. China Posts Weakest Growth in 27 Years — China’s economic growth decelerated in the second quarter to its slowest pace since 1992, growing by 6.2% and prompting expectations of more stimulus. The data was weighed down by an impasse in negotiations that shattered hopes for a trade deal in late May, though President Trump and Xi Jinping got discussions back on track by the end of June. Separate economic figures handily topped forecasts as the country’s industrial output grew 6.3% in June from a year earlier, while retail sales surged 9.8%. The Shanghai Composite closed up 0.4% following the news.

3. Huawei May Soon Restart U.S. Sales — the U.S. may approve licenses for companies to re-start new sales to Huawei in as little as two weeks, according to Commerce Secretary Wilbur Ross. It’s a sign President Trump’s recent effort to ease restrictions on the Chinese telecom equipment supplier could move forward quickly amid chip industry lobbying, coupled with Chinese political pressure. Out of $70B that Huawei spent buying components in 2018, some $11B went to U.S. firms including Qualcomm (NASDAQ:QCOM), Intel (NASDAQ:INTC) and Micron Technology (NASDAQ:MU).

4. DoJ Seeks Pause of Antitrust Ruling Against Qualcomm — the U.S. Department of Justice asks a federal appeals court to pause enforcement of the May antitrust ruling that would force the company to change how it licenses its patents, citing support from the Energy Department and Defense Department. The Justice Department says QCOM likely will win its appeal of the May ruling because Judge Koh, who found the company’s license practices were anti-competitive, ignored established antitrust principles and imposed an overly broad remedy. Defense Under Secretary Ellen Lord wrote in a filing made in the 9th Circuit Court of Appeals “For DoD, Qualcomm is a key player both in terms of its trusted supply chain and as a leader in innovation, and it would be impossible to replace Qualcomm’s critical role in 5G technology in the short term,”. In a related note, Vodafone launches 5G in Germany.

5. WHO Declared Ebola Outbreak Global Health Emergency — the World Health Organization has declared the Ebola outbreak in Democratic Republic of Congo to be a “public health emergency of international concern” after the spread of the virus to the city of Goma and into Uganda. The designation signals risk that a disease could spread globally and is meant to corral political and financial support to stop it. Responders have been using an experimental vaccine made by Merck (NYSE:MRK) in an attempt to halt the spread of the virus, with more than 140,000 people in the DRC immunized so far.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

July 15th, 2019

” I learned early that there is nothing new in Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again. I’ve never forgotten that.” –Jesse Livermore

1. Trump’s Rule Requiring ‘Drug Prices in TV Dds Blocked — U.S. District Judge Amit Mehta has blocked a Trump administration rule requiring drugmakers to put prices in TV ads, a central part of the president’s push to lower the cost of prescription medications. The rule of the Health and Human Services Department would violate free speech and exceeded the agency’s statutory authority, Mehta wrote, adding that “the responsibility rests with Congress to act in the first instance.” The lawsuit was brought by Merck (NYSE:MRK), Eli Lilly (NYSE:LLY) and Amgen (NASDAQ:AMGN), which have long argued that list prices do not reflect the actual cost of drugs as they do not take into account discounts and rebates negotiated with health insurers and PBMs.

2. Deutsche Bank Launches Makeover, Plans 18,000 Job Cuts — Deutsche Bank (NYSE:DB) is confirming a radical transformation, through a restructuring that will see it exit the global equities business and shed 18,000 jobs. The latest overhaul looks to charges of €7.4B through 2022, while it won’t pay a dividend this year or next. The German bank also expects to report a net loss of €2.8B for the second quarter, before it narrows its focus on serving European companies and retail-banking customers.

2. Fed Chairman Jerome Powell Sent a Strong Signal the Central Bank Could Cut Interest Rates Later This Month — In testimony before a House committee, Mr. Powell highlighted how the economic outlook hasn’t improved in recent weeks. He also warned of risks that weaker inflation readings could prove more persistent than previously anticipated. Mr. Powell will testify again today, this time in front of a Senate committee.

Stocks in the U.S. leapt after Mr. Powell’s testimony. The Nasdaq Composite closed at a record 8202.52. Energy and technology stocks led the S&P 500 higher as it briefly breached the 3000 level for the first time before ending the day at 2993.07.

3. Deutsche Bank is Being Investigated by the U.S. Justice Department — The U.S. Justice Department is investigating whether Deutsche Bank violated foreign corruption or anti-money-laundering laws in its work for 1Malaysia Development Bhd., which included helping it raise $1.2 billion in 2014 as concerns about the fund’s management and financials had begun to circulate.

“Deutsche Bank has cooperated fully with all regulatory and law-enforcement agencies that have made inquiries relating to 1MDB,” a spokesman for the bank said. He cited Justice Department documents saying 1MDB made “material misrepresentations and omissions to Deutsche Bank officials” in connection with 1MDB’s transactions with the bank. “This is consistent with the bank’s own findings in this matter,” he added.

4. President Voiced No Support for Bitcoin — “I am not a fan of Bitcoin (BTC-USD) and other cryptocurrencies, which are not money, and whose value is highly volatile and based on thin air,” President Trump tweeted last night. He also took a slap at Facebook (NASDAQ:FB) and its Libra crypto offering, which he said “will have little standing or dependability.” If Facebook and others want to become banks, he adds, they can stand in line and get banking charters like all the rest. “We have only one real currency in the USA, and it is stronger than ever, both dependable and reliable.”

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

July 9th, 2019

“Obviously the thing to do was to be bullish in a bull market and bearish in a bear market… I came to learn that even when one is properly bearish at the very beginning of a bear market it is not well to begin selling in bulk until there is no danger of the engine back-firing.” – Jesse Livermore

1. U.S. Proposes More tariffs on EU Goods — Washington has turned its attention back to the EU. The U.S. Trade Representative has released a $4B list of additional goods that may be targeted with retaliatory tariffs as part of a long-running battle at the WTO over subsidies given to Airbus (OTCPK:EADSY) and Boeing (NYSE:BA). The list, which includes Italian cheese, Scotch whisky, chemicals and metals, adds to products valued at $21B that the USTR had identified in April as facing possible tariffs.

2. EU Open to Talks on Subsidies Dispute — the EU is open to talks with Washington in a dispute over aircraft subsidies, but it is also preparing retaliation after the U.S. added Italian cheese, Scotch whisky and other products to a list of goods in line for hefty tariffs. The WTO has found that Airbus (OTCPK:EADSY) and Boeing (NYSE:BA) received billions of dollars of harmful subsidies in a pair of cases marking the world’s largest-ever corporate trade dispute. Billions of dollars of tit-for-tat tariffs are on the line, with Washington first to seek the duties under the WTO timetable.

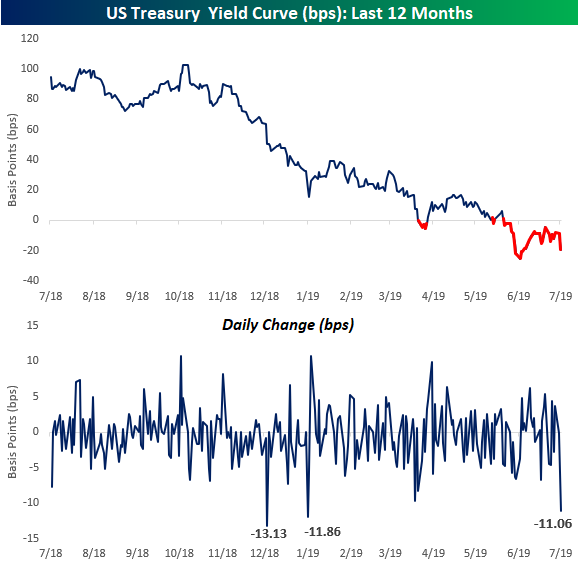

3. 10-year Yield Plummeting Below 2% — with the 10-year plummeting below 2% again and the 3-month yield spiking up by over 7 basis points, which is its biggest one day gain since December 2017. The 11-bps move further into inverted territory is the biggest one-day move since January 2nd (see second chart). While not back at new lows, today marks the 29th day that the curve has now been inverted. In Fedspeak news, Cleveland Fed President Loretta Mester (who leans hawkish but isn’t a voter) just noted in a speech that she’s in no hurry to cut. She argues that “Cutting rates at this juncture could reinforce negative sentiment about a deterioration in the outlook even if this is not the baseline view, and could encourage financial imbalances given the current level of interest rates, which would be counterproductive.”

Tuesday’s 11-bps move further into inverted territory is the biggest one-day move since January 2nd.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

July 1st, 2019

“Don’t look for the needle in the haystack. Just buy the haystack.” — John Bogle, founder of Vanguard

1. U.S. Weighs Ban on China-Made 5G Equipment — the Trump administration is examining whether to require that next-generation 5G cellular equipment used in the U.S. be designed and manufactured outside China, WSJ reports. The proposals could force telecom equipment giants Ericsson (NASDAQ:ERIC) and Nokia (NYSE:NOK) to reshuffle their production locations, with Citi analysts estimating that China represented 45% and 10% of their manufacturing-facility area in 2018. Washington has already essentially banned telecom equipment from Chinese companies, especially industry leader Huawei, over cybersecurity concerns.

2. China to Insist U.S. Lift Huawei Ban as Part of Trade Truce — ahead of their G20 meeting in Osaka, President Xi plans to present President Trump with a set of terms the U.S. should meet before China is ready to settle their market-rattling trade confrontation, WSJ reports. Among the preconditions, Beijing is insisting that Washington remove its ban on the sale of American technology to Huawei and also wants the U.S. to lift all punitive tariffs. The nation additionally wants the Trump administration to drop efforts to get China to buy even more U.S. exports than Beijing said it would when the two leaders last met in December.

3. FAA Identifies New Potential Risk on Boeing 737 MAX — following a Reuters report stating the FAA had found a new “potential risk” the company must fix before the 737 MAX can return to service. The risk was discovered during a simulator test last week, which likely will prevent BA from running a certification test flight until at least July 8. In an SEC filing, Boeing said the FAA has asked it to address a specific condition of flight not covered by planned software changes.

4. AbbVie Looks to Acquire Allergan for more than $60B –– bbVie’s (NYSE:ABBV) announced $63B deal for Allergan (NYSE:AGN), with the two drugmakers betting a combination will deliver new sources of growth. Buying Allergan would result in a major position in the $8B+ market for Botox and other beauty drugs, as well as a number of popular eye treatments, as AbbVie braces for the end of patent protection for the world’s top-selling drug, Humira.

5. U.S. Unveils “hard-hitting” Iran Sanctions — crude prices are on watch as the Trump administration ordered new sanctions against the assets of Ayatollah Ali Khamenei and several Iranian military commanders, as well as plans to target Foreign Minister Javad Zarif later this week. The penalties effectively freeze the business operations of the Supreme Leader’s office, which controls a global network of private companies that some experts estimate is worth between $100B-$200B. Tensions already worsened in May, when Washington ordered all countries to halt imports of Iranian oil, and then escalated following a series of apparent Iranian-backed skirmishes in the Middle East. “Imposing useless sanctions is the permanent closure of the path of diplomacy,” Foreign Ministry spokesman Abbas Mousavi wrote on Twitter.

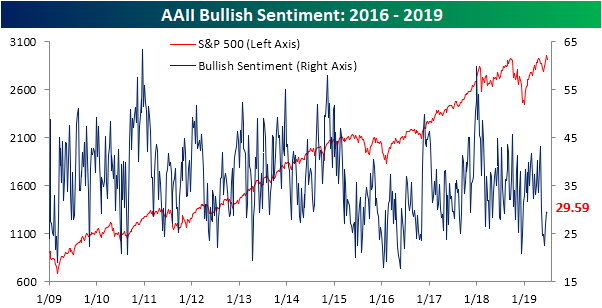

6. AAII Weekly Sentiment Survey — while S&P 500 moved up towards an all-time closing high, bullish sentiment levels were relatively muted in spite of this price action. The percentage of investors reporting as bullish rose only 0.08% to 29.59%. Bullish sentiment saw a similar sized move only one month ago when it had risen from 24.71% to 24.79% in the final week of May. Given these readings, bullish sentiment remains at the lower end of its normal range sitting over 8.5 percentage points from the historical mean.

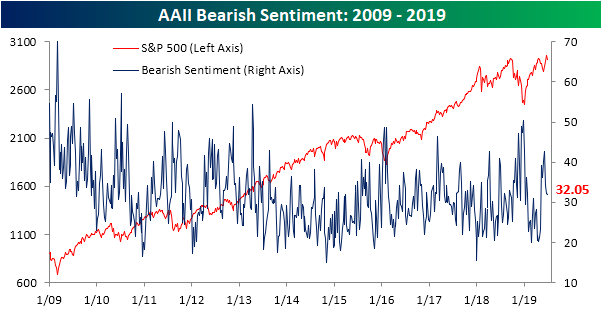

Bearish sentiment perfectly mirrored bullish sentiment this week as the percentage of pessimistic investors fell by just 0.08% to 32.05% and still above the historical average of 30.32%.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 24th, 2019

“Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.” — John Templeton

1. Facebook Releases Plan for Libra Crypto — it could amount to the biggest catalyst for digital assets in their decade-long existence. Facebook (NASDAQ:FB) has unveiled a consortium to create an open-source digital currency called Libra, set to launch in the first half of next year, which would allow consumers to send money around the world easily and for free. While Libra won’t be run by Facebook – but rather by a nonprofit association and backed by relatively stable government money – the company does have a plan to profit from it with a new subsidiary, Calibra, which is building a digital wallet for storing and exchanging the currency. Furthermore, U.S. lawmakers from both sides of the aisle are forming a growing group calling for hearings on Facebook’s (NASDAQ:FB) Libra cryptocurrency. Democrat Maxine Waters, chairwoman of the House Financial Services Committee, said she wants Facebook to testify about the plans and the company should put them on hold for a review, while she’s also received a letter from the committee’s top Republican, Patrick McHenry, calling for a hearing. Many have additionally cited concerns about the social network’s checkered past when it comes to trust and privacy.

2. Boeing Gets Zero New Orders at Paris Air Show Day One — Boeing (NYSE:BA) didn’t announce a single new order on the first day of the expo, while rival Airbus (OTCPK:EADSF) recorded orders and options for 123 planes, according to CNBC. The report reinforces Boeing CEO Dennis Muilenburg’s view that this year’s Paris Air Show would be less about orders and more about reassuring customers and suppliers that the company is making progress on getting the grounded 737 MAX back in the air.

3. Rocket Explodes Near Exxon Site in Iraq — a rocket struck the site of the residential and operational headquarters of several global major oil companies in southern Iraq early Wednesday, including ExxonMobil (NYSE:XOM), but had no effect on oil fields or exports, sources told Bloomberg. The incident in the Basra province injured three Iraqi workers, however, prompting Exxon to evacuate 20 foreign employees. While attacks on energy facilities, including a Saudi Arabian pipeline and several oil tankers, as well as a U.S. military buildup, are stoking concerns, a considerable ratcheting of tensions will likely be required to drive prices higher.

4. FOMC Monetary Policy Meeting — as the Fed latest FOMC meeting, the yield on the benchmark 10-year Treasury dropped below 2% overnight for the first time since November 2016. The FOMC left interest rates unchanged at its monetary policy meeting last Wednesday, dropped the word “patient” from its statement and said it would “act as appropriate” to sustain the economy. The Fed Funds Futures pointing to a 100% chance of monetary policy easing in July.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 24th, 2019

“One learns the most from mistakes, not successes.” — Paul Tudor Jones

1. Raytheon and United Technologies Agree to Merge — United Technologies and Raytheon have agreed to an all-stock merger, creating the second-largest defense-and-aerospace company in the U.S. after Boeing (NYSE:BA) with combined annual sales of around $74B. The deal won’t include United Tech’s (NYSE:UTX) elevator (Otis) and air conditioning units (Carrier), which it plans to spin off in 2020. Raytheon’s (NYSE:RTN) Tom Kennedy will become executive chairman of the combined company, to be called Raytheon Technologies, while UTX’s Greg Hayes will be named CEO. Two years after the deal closes, Hayes will assume the role of chairman and CEO.

2. Beijing Offers Support to Local Government — Beijing encouraged local governments to use special bonds for infrastructure projects in a bid to shore up economic growth. That helped offset President Trump’s threat to raise tariffs again if President Xi Jinping doesn’t meet with him at the G-20 summit at the end of June. The onshore yuan also bounced off its closing low of the year as the PBOC set its reference rate higher than forecast and announced plans to sell bills this month after the currency was hit in May.

3. Hong Kong Protests Intensify — Protests against Hong Kong’s controversial extradition law shut down key parts of the city, with police firing tear gas and rubber bullets to drive away thousands of demonstrators. Financial institutions also scrambled for liquid assets, triggering interbank interest rates in the territory to shoot up across the curve, with the one-month and two-month HIBOR reaching their highest level since late 2008. Hong Kong Chief Executive Carrie Lam argues the legislation is necessary to close a legal loophole that makes the city a refuge to criminals, but opponents say its approval would tear down the legal wall intended to keep Hong Kong’s justice system separate from China’s.

4. FTC Opposes Qualcomm Antitrust Request — the FTC has asked District Judge Lucy Koh to deny Qualcomm’s (NASDAQ:QCOM) request to delay enforcement of an antitrust ruling handed down in May, announcing that it was in the public interest because an appeal could take years. LG Electronics (OTC:LGEAF) reiterated the view of the FTC, saying it could be forced into signing another unfair deal unless Koh’s protections remain in place. On May 28, Qualcomm asked to put the sweeping antitrust decision on hold as it would “radically restructure its business relationships” in ways that would be impossible to reverse if it wins an appeal.

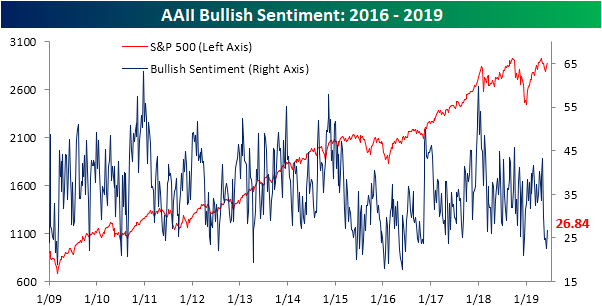

5. AAII Weekly Sentiment Survey — last week’s rally has reversed this build-up of bearish sentiment to a small degree, as the percentage of investors reporting as bulls in this week’s AAII survey grew to 26.84% from 22.53% last week. While this is an improvement, investors have been hesitant to rush back, as bullish sentiment remains low relative to history. This week’s reading is still over one standard deviation below the historical average of 38.19%.

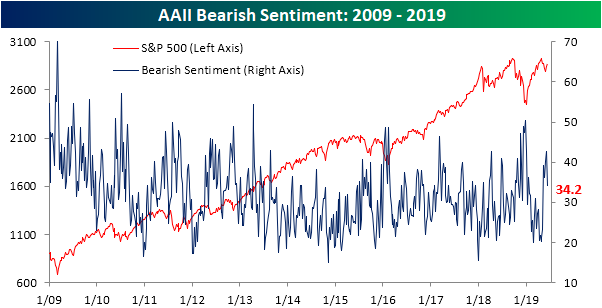

Bearish sentiment, on the other hand, saw a sharper move, falling to 34.2% versus 42.58% last week. That is the largest decline in bearish sentiment since February 7th of this year, when it had fallen just under 9%, from 31.76% to 22.78%. Similar to bulls, while this is an improvement, bearish sentiment remains elevated above its historical average.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 10th, 2019

“If it is abvious, it is obviously wrong” — Joe Granville

1. FTC Takes on Amazon, DOJ to Oversee Google — Amazon (NASDAQ:AMZN) could face heightened antitrust scrutiny under a new agreement between the government’s twin antitrust agencies that puts it under closer watch by the Federal Trade Commission, The Washington Post reported. The move would divvy up competition oversight of two of the country’s top tech companies, with the U.S. Justice Department having more jurisdiction over Google (GOOG, GOOGL) and paving the way for a potential investigation of the search-and-advertising giant.

2. Big Tech Faces Congressional Probe — the House Judiciary Committee unveiled a sweeping “top-to-bottom” review of unnamed tech companies early last week as reports surfaced of a dual effort from the DOJ and the FTC to tackle the perceived dominance and potential abuses of Big Tech. “The growth of monopoly power across our economy is one of the most pressing economic and political challenges we face today,” said David Cicilline, who chairs the Antitrust Subcommittee, adding that “market power in digital markets presents a whole new set of dangers.”

3. Trump Touted Progress in Mexico Talks — “Progress is being made” in talks with Mexico, according to President Trump, but “not nearly enough!” Discussions will continue , but “unless an agreement is reached a 5% tariff on Mexican goods would begin on Monday.” The peso slid as much as 1.3% as credit ratings agency Fitch downgraded the nation’s sovereign debt near junk status – citing risks posed by heavily indebted oil company Pemex and trade tensions – while Moody’s lowered its outlook to negative. Where would the levies hit hardest? Mexico is the world’s biggest exporter of beer (BUD, STZ), selling $3.6B worth to the U.S. last year, along with $2B in avocados (CVGW, FDP) and $2B in tomatoes. Corporations are also speaking out. Chipotle (NYSE:CMG) estimated a $15M hit, but said it could cover that by raising burrito prices by around 5 cents, while auto parts maker Aptiv (NYSE:APTV) said a 5% tariff would cost the company $17M per month.

4. US/China Trade War – China has lots of policy room according to PBOC — PBOC Governor Yi Gang declared if the trade war with the U.S. deepens, “we have plenty of room in interest rates, we have plenty of room in required reserve ratio rate, and also for the fiscal, monetary policy toolkit, I think the room for adjustment is tremendous,”. The yuan has stabilized in recent weeks as authorities voiced support for the currency, following a rapid selloff that pushed it near 7 per dollar – a level not breached since the global financial crisis.

5. Theresa May to step down as Tory leader — after 1,059 days in charge, U.K. Prime Minister Theresa May has officially stepped down as leader of the ruling Conservative Party. The race has already started to replace her, with 11 contenders and Boris Johnson the current favorite. Starting next week, the party’s 300 or so MPs will whittle down the field of candidates to two through successive rounds of voting. After that, the party’s rank-and-file members, an estimated 124K people, will decide which of those two finalists gets to be leader.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 31st, 2019

There will not be any re-cap for the week of May 24 to May 31 2019. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 21st, 2019

“Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected.” — George Soros

1. Walmart Pushes Veterinary Clinic — with spending on pets in the U.S. estimated to exceed $75.3B this year, Walmart (NYSE:WMT) aims to have 100 veterinary clinics open in its stores within the next 12 months, growing from the 21 it has today. The retailer is also for the first time launching an online pet pharmacy, WalmartPetRX.com, rivaling Chewy.com. Walmart has seen a roughly 60% increase in the number of dog- and cat-related health-care items sold on its website over the past year, according to a company spokeswoman.

2. China Hardens Trade Stance as Talks Enter New Phase — the new hard line taken by China in trade talks—surprising the White House and threatening to derail negotiations—came after Beijing interpreted recent statements and actions by President Trump as a sign the U.S. was ready to make concessions, said people familiar with the thinking of the Chinese side. Adding to the pressure, the U.S. formally filed paperwork Wednesday to raise tariffs on $200 billion of Chinese goods to 25% from the current 10% at 12:01 a.m. Friday. Beijing’s Commerce Ministry responded by threatening to take unspecified countermeasures. At a campaign rally in Florida Wednesday night, Mr. Trump said Chinese leaders “broke the deal” in trade talks with the U.S.

3. BlackRock Pulls Out of Italian Bank Banca Carige Rescue — BlackRock’s (NYSE:BLK) withdrawal from the proposed deal increases the possibility that the Italian government may have to bail out Banca Carige (OTC:BCIGY). BlackRock, which was to have bought about half a 720M euro ($806M) share issue, rejected the proposed deal for reasons including excessive risk. The deal would have given BlackRock control of Italy’s 10th-largest bank.

4. Iran Begins Withdrawal from Nuclear Deal — a year after the U.S. pulled out of the Iran nuclear accord, Tehran declared it’s no longer committed to parts of the deal. President Hassan Rouhani said the remaining signatories – the U.K., France, Germany, China and Russia – had 60 days to implement their promises to protect Iran’s oil and banking sectors, giving them a choice of following President Trump or engaging with the Islamic Republic in violation of American sanctions. Iran will also begin to build up its stockpiles of low enriched uranium and heavy water, and threatened to resume construction of the Arak nuclear reactor.

5. U.S. Hits China with Tariff Increase — President Trump’s tariff increase on $200B worth of Chinese goods took effect last Friday after midnight. China’s Commerce Ministry immediately announced it would take countermeasures against the American move, but did not reveal what its response would entail. President Trump is already taking steps to impose a fresh round of tariffs on $325B in Chinese goods that aren’t currently taxed. If that happens, virtually all Chinese exports to the U.S. would face 25% tariffs, further ratcheting up tensions between the world’s two largest economies.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »