October 14th, 2019

“I think investment psychology is by far the more important element, followed by risk control, with the least important consideration being the question of where you buy and sell.” — Tom Basso

1. US/China Up the Ante with Trade Dispute / Adds Chinese Firms to Blacklist — the U.S. added 28 Chinese entities to an export blacklist, citing their role in Beijing’s repression of Muslim minorities in northwest China. The decision came days before high-level trade talks are set to resume in Washington. The U.S. said the action isn’t related to trade talks, but it is likely to disturb Chinese officials already incensed over what Beijing sees as U.S. support for the pro-democracy movement in Hong Kong. Trade negotiations have made little progress since hitting an impasse in May. The one recent bright spot has been Chinese agricultural purchases, including more than 1.5 million metric tons of U.S. soybeans in the last week of September alone.

2. Boeing Suffers Setbacks — the effort to return 737 MAX jets to service has hit a new snag because of heightened European safety concerns about portions of proposed fixes to flight-control systems. Separately, the pilots’ union at Southwest Airlines sued Boeing, alleging that the plane maker rushed the 737 MAX to market and misrepresented the plane as safe. Boeing called the suit “meritless.”

3. US/China Trade Talks Resume — Senior U.S. and Chinese officials will square off for trade talks Thursday at a pivotal moment in the countries’ relationship, with higher tariffs looming if negotiators fail to break a five-month stalemate. China is looking to narrow the scope of its negotiations with the U.S. to trade matters only and put thornier issues—such as U.S. national security concerns over Chinese telecom giant Huawei Technologies Co.—on a separate track in a bid to break the deadlock. Business groups want Mr. Trump abandon plans to raise tariffs to 30%, which is set to happen Oct. 15. They also want him to drop plans to impose new tariffs of 15% on $156 billion in smartphones, apparel and other consumer goods starting Dec. 15.

4. Fed to Increase Supply of Bank Reserves — the Federal Reserve will soon increase its purchases of short-term Treasury securities to avoid a recurrence of the unexpected strains experienced in money markets last month, Fed Chairman Jerome Powell said in a speech in Denver. Fed officials stopped shrinking the assets on their balance sheet in August but never said when they would allow the balance sheet to grow again. As a result, bank deposits held at the Fed—a crucial liability on the balance sheet—have continued declining. Stresses in very-short-term funding markets recently suggested banks have grown reluctant to lend those reserves.

5. US/China Agreed to a Trade Truce — the US/China agreed to a initial tentative agreement on Friday. Mr. Trump said China will make some $40 billion to $50 billion more in agricultural purchases over two years and has promised to better protect intellectual property and welcome more foreign financial services. In return the U.S. won’t increase tariffs to 30% from 25% on $250 billion of Chinese goods next week as Mr. Trump had planned. The two countries also agreed to keep talking toward what Mr. Trump called a “phase two” agreement that would include the tougher issues such as Chinese technology theft and predatory regulation against American companies. There will also be a new consultation process to address disputes and monitor enforcement. The implication is that if progress continues, Mr. Trump will cancel the tariffs planned for December on more Chinese goods.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 8th, 2019

“Reaching any goal in trading requires specific domain knowledge and technical skills. But then, after that, it’s all mindset management. Yet most people ignore that —they automatically think they have that last part all figured out, and it’s a mistake.” ― Yvan Byeajee,

1. U.S. Factory Activity Contracted Again in September — the Institute for Supply Management reported earlier last week its U.S. manufacturing index fell to 47.8 in September from 49.1 in August. The reading is the lowest since June 2009 and represents a continuation of the slowdown seen in August, when the index contracted for the first time since August 2016. The deeper contraction in the manufacturing sector is the latest sign that the escalated trade war between the U.S. and China is taking a big bite from the economy. Manufacturing was once considered a big winner under the Trump administration with improvement in employment and activity over the past few years.

2. Charles Schwab Ending Online Trading Commissions on U.S.-Listed Products — Charles Schwab Corp. said it would eliminate commissions on trades made on its mobile and web channels, rattling the online brokerage industry. Charles Schwab said the move, which is effective Oct. 7, is aimed at making online investing more affordable. It noted that new firms entering the market often use zero or low commissions as a lever. Companies effected are: SCHW, AMTD, ETFC, IBKR.

3. U.S. Factory Activity Contracted — U.S. factory activity contracted for the second straight month in September, hitting a 10-year low and triggering concerns about the economy. Surveys of purchasing managers in Europe and Asia, also released Tuesday, pointed to deepening declines in factory activity last month, as a slowdown in exports hit factories.

4. Online Gaming Flutter Entertainment agreed to buy PokerStars owner Stars Group for about $6 billion — FanDuel owner Flutter Entertainment agreed to buy PokerStars owner Stars Group for about $6 billion. The deal creates an online-gambling giant as internet and app-based betting is taking hold in the U.S. It also connects FanDuel with Fox Corp., which owns a minority stake in Stars and recently launched its own betting app, Fox Bet. Fox Corp. and WSJ parent News Corp share common ownership.

Flutter, based in Dublin and listed in London, owns bookie brands in the U.K. including Paddy Power and Betfair. Flutter’s FanDuel, in addition to its fantasy-sports site, offers online and retail betting in New Jersey and Pennsylvania. Nasdaq-listed Stars Group, based in Toronto, owns popular online poker brands such as PokerStars and Sky Betting & Gaming.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 1st, 2019

If a speculator is correct half of the time, he is hitting a good average. Even being right 3 or 4 times out of 10 should yield a person a fortune if he has the sense to cut his losses quickly on the ventures where he is wrong. -Bernard Baruch

1. UK Court Decided Suspension of Parliament Unlawful — Prime Minister Boris Johnson acted unlawfully when he suspended Parliament this month for five weeks, according to the British Supreme court, opening the door to new challenges to his Brexit strategy. Sterling rose nearly 0.4% on the back of the decision to trade at $1.2478. The President of the Supreme Court, Brenda Hale, said there was no justification for the government taking such extreme action, but that it was for parliament to decide what to do next.

2. FAA Announces 737 Max Return Up to Individual Countries — each country will make “its own decision” on when the Boeing (NYSE:BA) 737 MAX returns to service, according to FAA Administrator Steve Dickson, who has not yet set a timeline on when to allow the jets back in U.S. skies. The planes have been grounded worldwide since mid-March after two crashes within five months of each other killed 346 people. On Monday, Boeing also announced that it will pay $144,500 to each of the victims’ families from a $50M financial assistance fund.

3. Juul Under Criminal Investigation — Federal prosecutors in California are conducting a criminal probe into e-cigarette maker Juul (JUUL), in which tobacco giant Altria (NYSE:MO) owns a 35% stake, WSJ reports. Regulators have criticized Juul for fueling a teen vaping “epidemic,” while lawmakers have urged the FDA to pull most e-cigarettes off the market. It follows an outbreak of a deadly lung disease linked to vaping that has sickened at least 530 people and killed eight. Massachusett is imposing a four-month ban on sales of all vaping products amid a national health emergency that so far has been linked to nine deaths and has sickened at least 530 people. T

4. Pelosi Announces Impeachment Inquiry into Trump Amid Alleged Abuses of Power — the House started an impeachment inquiry into President Donald Trump as a swell of Democrats denounce the president over alleged abuses of power, House Speaker Nancy Pelosi. Based on past history of Clinton impeachment, the S&P 500 fell as much as 4.9% on October 8, 1998, the day the House voted to begin impeachment proceedings against President Clinton, before trimming losses to end the day down 1.2%. By the time Clinton was acquitted by the Senate in February 1999, the index was up 28%. Markets shrugged off an impeachment inquiry against President Nixon on February 6, 1974, but the S&P 500 fell around 30% until his resignation. There were other forces at play, however, including Nixon’s decision to suspend the gold standard and a recession following the oil shock of late 1973.

5. Amazon Pilots Care Clinics — building on previous healthcare efforts, a new pilot is being launched for Amazon (NASDAQ:AMZN) workers in the Seattle area, offering a virtual primary care clinic with an option to send nurses to employees’ homes. Amazon has already partnered with JPMorgan (NYSE:JPM) and Berkshire Hathaway (BRK.A, BRK.B) – on an effort called Haven – which explores how to move the needle on healthcare expenses for their combined 1.2M employees. In addition, the company has a pharmacy division under PillPack and an R&D group sometimes referred to as Grand Challenge or 1492.

6. IPO Market Weakens — the IPO market took another hit as Endeavor Group Holdings yanked its planned offering and Peloton Interactive’s shares skidded on their first day of trading. The entertainment company became the second big casualty of the IPO market’s recent chill after WeWork’s parent company pulled its offering earlier this month. It is the second time Endeavor has hit the brakes on its IPO this year. Part of the reason Endeavor pulled its deal, according to people familiar with the matter, was the poor performance of Peloton in its debut. Investors soured on shares of Peloton, the startup known for its exercise bikes that allow users to join along in virtual spin classes from home, pushing them 11% below their IPO price of $29.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

September 23rd, 2019

“In this business if you’re good, you’re right six times out of ten. You’re never going to be right nine times out of ten.” -Peter Lynch

1. Index Funds Had More Assets by Value Than Stock-Picking Rivals — Funds that track broad U.S. equity indexes hit $4.27 trillion in assets as of Aug. 31, giving them more money than stock-picking rivals for the first-ever monthly reporting period. Funds that try to beat the market had $4.25 trillion as of that date. In the past decade, $1.32 trillion fled actively managed U.S. equity mutual funds and exchange-traded funds as nearly $1.36 trillion was added to low-cost funds that mimic market indexes. That shift lowered the price of investing for individuals, reduced the influence of stock pickers and turned a handful of Wall Street outsiders into the biggest power brokers in the industry.

2. General Motors Factory Workers Headed to Picket Lines in 10 States — the United Auto Workers union called on thousands of workers to walk off the job in an effort to secure better pay, more job security and other benefits. The walkout is one of the largest private-sector work stoppages in decades. The UAW further announced it will pay striking workers $250 a week, but that does not go very far, especially when they need to cover their own health insurance. GM’s credit rating could also topple into junk bond status if the strike lasts more than a week or two, according to Moody’s.

3. S.Korea Downgrades Japan Trade Status — South Korea is following through with plans to drop Japan from a list of countries receiving fast-track approvals in trade, a reaction to a similar move by Tokyo to downgrade Seoul’s trade status. The dispute between the nations began in July when Japan imposed tighter export controls on three chemicals South Korean companies use to produce semiconductors and displays for smartphones and TVs, which are major import items for South Korea. The escalating row is rooted in wartime history and could cast uncertainty into the global supply chain and economy.

4. The Federal Reserve Cut Its Benchmark Interest Rate — the Federal Reserve cut its benchmark interest rate by a quarter-percentage point for the second time in two months, as Chairman Jerome Powell left the door open to more cuts. Three officials voted against the decision, with two saying rates should have been left unchanged, and one supporting a bigger cut. Mr. Powell repeatedly cited the costs of rising trade-policy uncertainty.

5. NY Fed to Conduct Third Repo Operation — the New York Fed is offering an overnight repurchase agreement operation for the third day in a row, injecting $75B into a vital corner of finance to restore order in the banking system. The temporary liquidity follows the Fed’s reduction in the interest rate on excess reserves, or IOER, another attempt to quell money-market stresses. The prior operations have soothed markets, with repo rates declining Wednesday to more normal levels after jumping to 10% on Tuesday, four times where they were last week.

6. Pentagon Weighs Sending More Military Assets to Mideast — President Trump is weighing responses to the attacks on Saudi oil facilities, and U.S. military officials are considering sending more antimissile batteries, a squadron of jet fighters and added surveillance capabilities, as well as possibly committing an aircraft carrier and other warships to the region.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

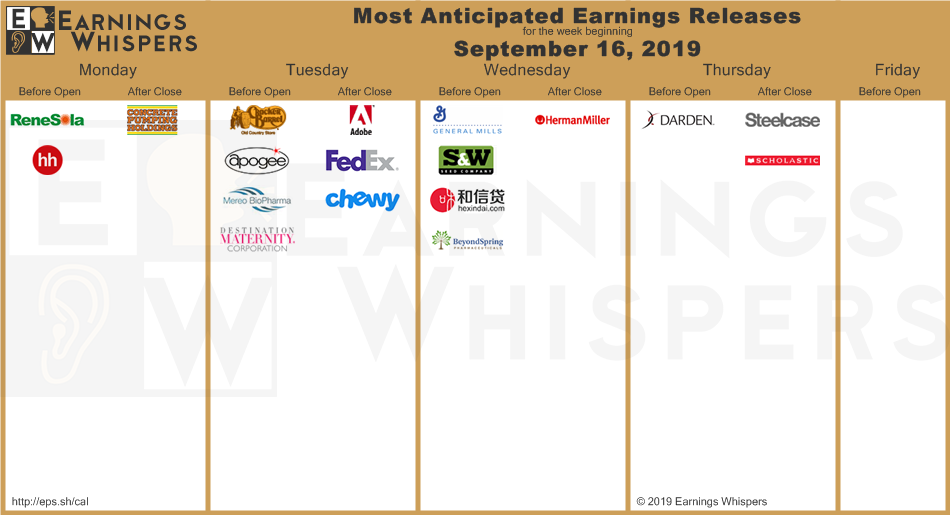

September 16th, 2019

“Trading doesn’t just reveal your character, it also builds it if you stay in the game long enough.” — Unknown

1. Apple’s Unveiled New Products at Fall Event — the tech giant stucks with its three-device approach to its new iPhone lineup, rolling out a trio of devices in the iPhone 11 family featuring Apple’s A13 chip, which Apple says is the fastest ever to be in a smartphone. The cheapest of these three devices, the iPhone 11, has a dual-camera design that supports ultrawide shots and night-mode capabilities for low-light situations. The front-facing camera allows users to take slow-motion selfies, which Apple calls “slofies.” . The big surprise came when Apple (AAPL) revealed that it would charge $4.99 a month for its previously announced streaming video service, Apple TV+, which is now set to launch on Nov. 1. That price was lower than the $9.99 monthly fee that some analysts and reports had expected before the event, and it makes Apple’s offering cheaper than streaming services from Netflix Inc.

2. More Deaths Linked to Vaping, CDC Warns — three more deaths linked to vaping have been reported in Indiana, California and Minnesota, bringing the total number of such U.S. deaths to five. Some type of chemical irritation is likely associated with the illnesses, but more information is needed to determine the exact cause. U.S. health officials are now investigating more than 450 cases of possible vaping-related illnesses in 33 states, while last week, the governor of Michigan announced the state will become the first to ban flavored e-cigarettes. President Trump said the U.S. plans to pull most vaping products from the market. citing growing concerns about health hazards and rising use by teenagers of the alternative to cigarettes. The Food and Drug Administration intends to ban popular fruity flavors, as well as menthol and mint e-cigarettes, from stores and online sellers, leaving just tobacco-flavored products. The move poses a major threat to a fast-growing industry estimated to reach $9 billion in sales this year and dominated by startup Juul Labs.

3. Trump to Delay Tariffs on China by Two Weeks — President Trump said the U.S. will delay by two weeks a planned increase in tariffs on some Chinese imports, a move that could ease chilled relations between the two nations ahead of planned trade talks in Washington next month. The planned tariff increases were to cover largely nonconsumer items—materials businesses use to produce goods—with the levy going from 25% to 30%. In response, China’s Commerce Ministry said that it welcomed the postponement and that Chinese companies had started making price inquiries for U.S. agricultural goods including soybeans and pork. Beijing suspended purchases of the U.S. products in August. Ministry spokesman Gao Feng said that the possible resumption of agricultural products isn’t a bargaining chip in trade talks.

4. ECB Cuts Rates and Launches Sweeping Stimulus Package — the European Central Bank cut its key interest rate and launched a sweeping package of bond purchases Thursday that lays the ground work for what is likely to be a long period of ultraloose monetary policy, jolting European financial markets. Mr. Trump said the ECB was “trying, and succeeding, in depreciating the Euro against the VERY strong Dollar, hurting U.S. exports.” The ECB joins central banks around the world, including the Federal Reserve, that have been cutting interest rates in recent weeks amid a bitter trade dispute between the U.S. and China, a fall in trade volumes and a slowdown in global growth. Second-quarter figures released Thursday by the Organization for Economic Cooperation and Development showed year-to-year economic growth in the Group of 20 leading economies was at its weakest since the start of 2013.

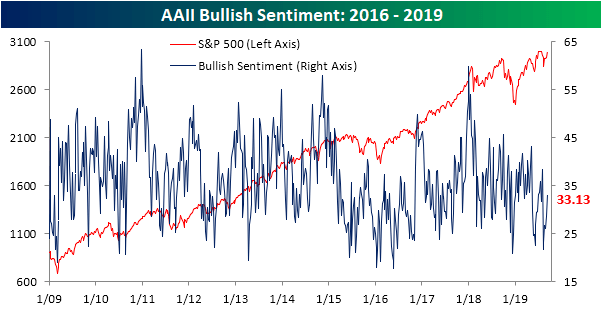

5. AAII’s weekly Sentiment — The percentage of investors reporting as bullish in AAII’s weekly survey rose from 28.64% last week up to 33.13%. That is the highest since August 1st when 38.44% reported bullish sentiment. With two consecutive weeks of improvements, bullish sentiment is now well off of its lows from the second week of August (21.66%) and is back within a normal range relative to its historical average of 38%.

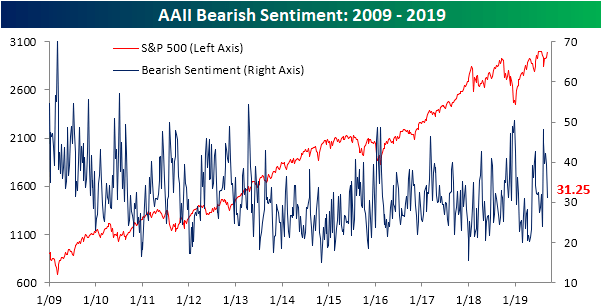

Meanwhile, bearish sentiment is now the lowest that it has been since the first week of August. With bearish sentiment falling 8.26 percentage points this week to 31.25%, it was the largest drop since June 13th’s 8.38-percentage point decline.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

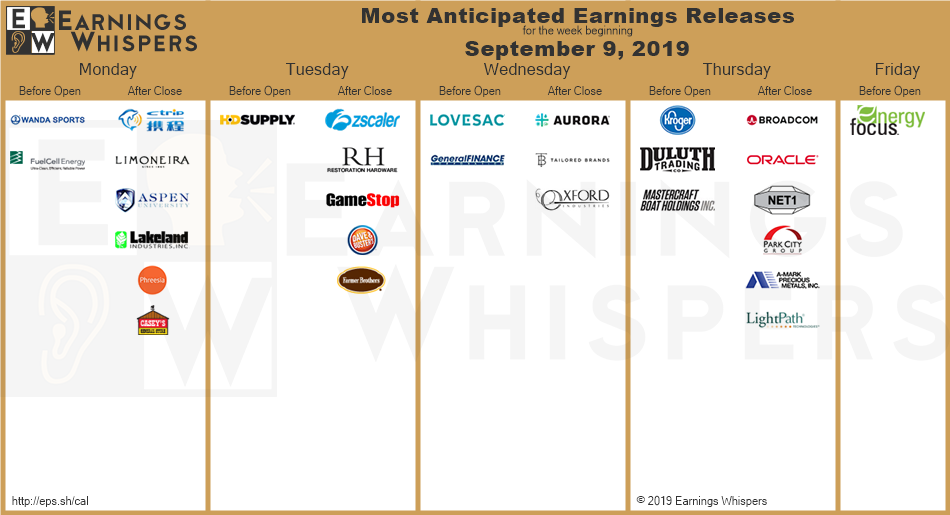

September 9th, 2019

“One of the funny things about the stock market is that every time one person buys, another sells, and both think they are astute” – William Feather

1. Trade War Between the U.S. and China Rippling Effect — new U.S. tariffs on clothing and other imports from China that went into effect Sunday are expected to hit consumers. President Trump has since told U.S. companies to look for alternatives to China. A round of retaliatory Chinese tariffs has now also taken effect, targeting imports of U.S. soybeans, crude oil and pharmaceuticals. It is crimping growth in Asian industrial giants such as Japan and South Korea and hitting factories as far from the front line as Germany. Global industrial production fell in the three months through June, as did trade flows, and a series of surveys of manufacturing companies in Asia and Europe suggests a rebound is unlikely over the coming months.

2. U.S., China Agree to Renew Trade Talks — China’s Ministry of Commerce says leaders of the U.S. and Chinese trade talks held a phone call and agreed to meet early next month in Washington, D.C., for another round of negotiations. Deputy-level officials will work together in mid-September to lay the groundwork for the meeting. On a related note, the markets already expect the Fed to cut interest rates modestly at the Sept. 17-18 policy meeting. Investors place a 90% probability on a quarter-percentage-point rate cut and a 10% probability on a larger, half-point cut, according to CME Group.

3. Apple Returns to Bond Market— taking advantage of the steep decline in benchmark interest rates, Apple (NASDAQ:AAPL) is joining U.S. companies including Deere (NYSE:DE) and Disney (NYSE:DIS) by launching its first bond deal since 2017 and selling $7B of debt. All three companies issued 30-year bonds with yields below 3%, a first for the corporate debt market. Bonds issued by big-name corporations give investors a relatively safe alternative that still pays more than government bonds.

4. Argentina Imposes Currency Controls — The spiraling economic crisis in Argentina has prompted the central bank to slap capital controls on businesses as the peso lost more than a quarter of its value since primary elections last month. Exporters will face limits of five days to repatriate foreign currency, while institutions will need authorization of the bank to buy dollars in the forex market, except in the case of foreign trade. The decision reverses one of the first big achievements of President Macri who removed strict capital controls after taking power in December 2015 (the restrictions had prompted the MSCI index to strip Argentina of its status as an emerging market, demoting it to a frontier market).

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

September 2nd, 2019

“Michael Marcus taught me one other thing that is absolutely critical: You have to be willing to make mistakes regularly; there is nothing wrong with it. Michael taught me about making your best judgment, being wrong, making your next best judgment, being wrong, making your third best judgment, and then doubling your money.” – Bruce Kovner

1. Cigarette makers Philip Morris International and Altria Group Are in Advanced Talks to Merge — the potential blockbuster deal would reunite two tobacco giants struggling with shrinking demand. The two companies split in 2008 but hold the same portfolio of cigarettes, including Marlboro. The products are sold by Altria in the U.S. and Philip Morris elsewhere. A combination would create a company with a market value of roughly $200 billion.

2. Judge Ordered Johnson & Johnson Must Pay $572 Million for the Opioid-Addiction Crisis in Oklahoma — Judge Thad Balkman said the state proved the company launched a misleading marketing campaign to convince the public that opioids posed little addiction risk and were appropriate to treat a range of chronic pain. The verdict caps the first opioid case to go to trial among thousands brought by state and local municipalities and could signal further findings of liability for drug companies facing similar cases. The three major drug wholesalers – McKesson (NYSE:MCK), AmerisourceBergen (NYSE:ABC) and Cardinal Health (NYSE:CAH) – should see some action now that J&J’s exposure is clarified.

3. Impossible Whopper Goes on Sale Nationwide — Burger King (NYSE:QSR) will bring the Impossible Whopper to all of its 7,200 U.S. locations today after a successful test run in seven markets. The nation’s second-largest burger chain began testing the plant-based burger from Impossible Foods at locations in St. Louis in April. Those outlets saw traffic outperform national averages by 18.5% that month, according to a report from inMarket.

4. Retailer Forever 21 Weighs Bankruptcy Filing — things are getting harder in the retail landscape as Forever 21 reportedly considers filing for bankruptcy, in a move that could put pressure on mall owners Simon Property Group (NYSE:SPG) and Brookfield Property Partners (NASDAQ:BPY). Struggles also saw Hudson’s Bay (OTCPK:HBAYF) offload Lord & Taylor on Wednesday to clothing rental startup Le Tote for $100M. Not everything is so bleak, however, as sneaker retailer Puma (OTCPK:PUMSY) opened its first U.S. flagship store today on the corner of Fifth Avenue and 49th Street in Manhattan.

5. Florida Braces for Hurricane Dorian — Hurricane Dorian is strengthening and is forecast to hit Florida as a Category 4 storm during the busy Labor Day weekend, becoming the first major hurricane to hit the area in 15 years. American Airlines (NASDAQ:AAL) and Southwest (NYSE:LUV) are allowing travelers to change their Florida flights without fees ahead of the storm, potentially weighing on the carriers which have weathered a difficult summer. Some of the nation’s largest investor-owned hospitals are also gathering supplies in preparation, including Tenet Healthcare (NYSE:THC), HCA Healthcare (NYSE:HCA) and Universal Health Services (NYSE:UHS). There’s additional concern for insurers and orange juice farmers, while the oil industry watches if the storm will pass into the Gulf of Mexico.

6. S&P calls ‘default’ in Argentina — Argentina’s decision to “unilaterally” extend maturities on its short-term debt constitutes a “default,” according to Standard & Poor’s, which slashed the country’s long-term foreign and local currency issue ratings to CCC – “vulnerable to nonpayment.” The downgrade came after Argentine bond prices fell and country risk soared to levels not seen since 2005 on Thursday amid fears of a full-blown financial crisis.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

August 22nd, 2019

“It wasn’t raining when Noah built the ark.” — Howard Ruff

There will not be any Weekly Re-Cap for the week of Aug 12 to Aug 23 2019. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

Posted in Weekly Summary | No Comments »

August 13th, 2019

“Reaching any goal in trading requires specific domain knowledge and technical skills. But then, after that, it’s all mindset management. Yet most people ignore that —they automatically think they have that last part all figured out, and it’s a mistake.”

1. FedEx Said It Would End its Contract to Deliver Amazon Packages — FedEx is gambling that it is better off filling its trucks with other customers’ goods. The company’s contract with Amazon expires at the end of this month. In June, FedEx said it was ending its air-shipping contract with Amazon in the U.S. The company would still handle international shipments. The decisions are evidence of escalating tensions between the longtime partners as Amazon builds its own delivery network.

2. White House to Move Forward With Ban on U.S. Government Business With Huawei — the White House is expected to start implementing provisions of a law that bars the U.S. government from doing business with Huawei. The planned move comes despite the Chinese tech giant’s efforts to block the rule in court. The Office of Management and Budget issued an interim rule this week laying out steps to ensure government agencies aren’t doing business with Huawei and several other Chinese companies. The rule is set to go into effect Aug. 13. Additionally, the White House is reportedly delaying a decision on whether to allow U.S. companies to do business with Huawei, while China released weaker economic data and pegged the yuan north of the $7 mark for the second consecutive session.

3. China Keeps Official Yuan Rate Just Stronger Than 7 Per Dollar — earlier in the week, Beijing let traded prices for its currency weaken past 7 per dollar, prompting the U.S. Treasury to designate it a currency manipulator. China currency at the weakest level since 2008, but again avoided moving this rate beyond the critical 7-yuan-to-the-dollar level. Asian stocks declined, while European stocks edged up against a backdrop of continuing worries about the U.S.-China trade war. The tensions are rising at a time when Chinese President Xi Jinping can ill afford to make concessions as he struggles with domestic issues. That raises the likelihood of a protracted trade conflict.

4. Britain, U.S. to Protect Shipping Through Strait of Hormuz From Iranian Threats — Britain joined the U.S. in forming an international mission to protect shipping through the Strait of Hormuz from Iranian threats, a decision that came after London struggled to build a European maritime coalition to safeguard ships in the region. The U.K. was dragged into the center of the simmering crisis between Iran and the West after Iran seized a tanker flying the British flag in July. The capture came after Britain seized an Iranian tanker the U.K. claimed was carrying oil to a sanctioned entity in Syria.

5. Facebook Introduces Facebook News Tab This Fall — set to launch this fall, Facebook (NASDAQ:FB) has confirmed that it’s working on a news tab to deliver “trustworthy news” to users. The announcement follows a WSJ report that said the social network had approached numerous news outlets like ABC News, Dow Jones, The Washington Post and Bloomberg about paying them as much as $3M annually to license their news articles. The tab would give news high prominence on Facebook, alongside core features like the News Feed (which includes updates from friends), Messenger and Watch (for videos).

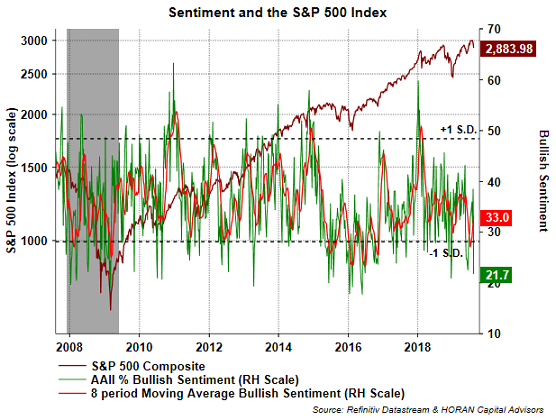

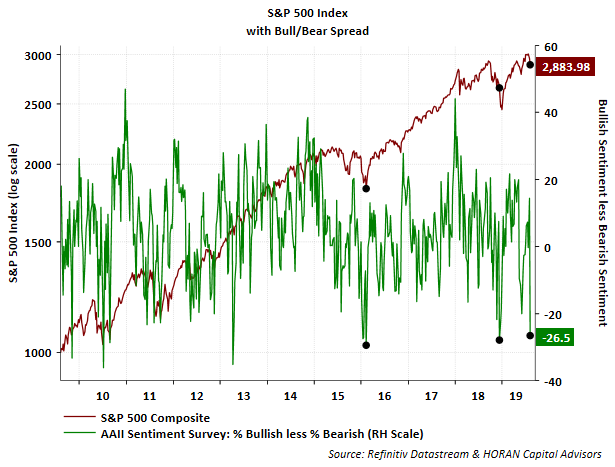

6. AAII Investor Sentiment — AAII is reporting individual investor bullish sentiment declined a sizable 16.8 percentage points to 21.7% in the week ending 8/7/2019. This is the lowest level since bullish sentiment reached 20.9% on December 13, 2018, a market bottom in the fourth quarter 2018 pullback. The low level of bullish sentiment certainly classifies this as an extreme level.

Neutral sentiment fell 7.4 percentage points, resulting in bearish sentiment spiking higher to 48.2%. This results in the bull/bear spread coming in at an extreme -26.5 as seen in the below chart. At this level of spread, historically, market lows have occurred at or near these levels.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

August 6th, 2019

“We want to perceive ourselves as winners, but successful traders are always focusing on their losses” – Peter Borish”

1. U.S. and China Are Set to Resume Trade Talks in Shanghai — negotiators will make another attempt to piece together a trade agreement amid considerably lowered expectations for a sweeping deal. People close to the talks say a major breakthrough is unlikely on points such as the U.S. insistence that China commit to legal changes to protect intellectual property and abandon state subsidies to business, or Beijing’s demands that the U.S. drop all tariffs as a condition for a deal. But more modest achievements may be possible, such as a commitment by China to purchase more agricultural products and action by the U.S. to relax its ban on U.S. companies selling to telecommunications giant Huawei Technologies.

2. Massive Data Breach at Capital One (COF) — CapitalOne disclosed a data breach exposed 140K Social Security numbers of its credit card customers, around 80K bank account records and 1M Canadian Social Insurance numbers. Additional information including names, addresses, phone numbers, credit scores and credit limits were also exposed, although credit card account numbers and log-in credentials were not taken. The suspect? Paige A. Thompson, a former employee of Amazon Web Services (NASDAQ:AMZN), where the bank had stored its customer data. Capital One (NYSE:COF) estimates the hack will cost the company approximately $100M-$150M in 2019.

3. Federal Borrowing Soars as Deficit Fear Fades — the U.S. government expects to borrow more than $1 trillion in 2019. Political support for taming deficits has faded in recent years, with Republicans supporting higher deficits in exchange for tax cuts and Democrats pushing for domestic-spending increases. Low borrowing costs suggest markets remain unfazed by all the red ink. Government debt has soared, but 10-year Treasury yields have fallen. Mainstream economists are increasingly questioning whether larger federal debt and deficits might be tolerable if put toward programs that would bolster long-term growth.

4. Hospitals May Be Forced to Disclose Discount Rates Negotiated With Insurer — The Trump administration proposed a rule requiring hospitals to disclose the discounted prices they negotiate with insurance companies, or face fines. The proposal could upend the $1 trillion hospital industry by revealing rates that have long been secret. The price-disclosure requirements would cover all of the more than 6,000 hospitals that accept Medicare, as well as some others. Hospitals that fail to share the discounted prices in an online form could be fined up to $300 a day, according to the proposal. The price-disclosure requirements would cover all the more than 6,000 hospitals that accept Medicare, as well as some others, and is likely to face fierce industry opposition. Comments on the proposal would be due in September and, if completed, the rule would take effect in January.

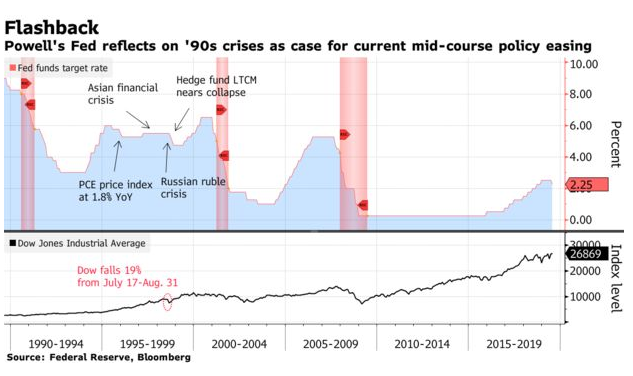

5. Fed Cuts Rates by a Quarter Point in Precautionary Move — the Federal Reserve cut interest rates by a quarter-percentage point—the first reduction since 2008—in a pre-emptive strike to cushion the economy from a global slowdown and escalating trade tensions. Officials also announced they would end the runoff of their $3.8 trillion asset portfolio on Thursday, two months earlier than previously planned. Fed Chairman Jerome Powell, at a news conference after the decision was released, called the rate cut a “mid-cycle adjustment” and didn’t rule out more reductions. But he also said it was “not the beginning of a long series of rate cuts” because that path is only followed at times of more severe economic distress. Powell’s remark raised comparisons to 1995-96 and 1998, when Alan Greenspan headed the Fed. In each instance, the central bank ended up cutting rates three times in a successful effort to prolong an economic upswing that until this year was the longest.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »