December 30th, 2019

‘Taken together, conditions today are characteristic of those that precede a Minsky Moment, in which excessive speculation and taking on additional credit risk during stable markets leads to a tipping point that leads to a period of instability.’ — Scott Minerd, Guggenheim Partners

HAPPY HOLIDAY & WISHING OUR VIEWERS A HAPPY, HEALTHY AND PROPEROUS NEW YEAR

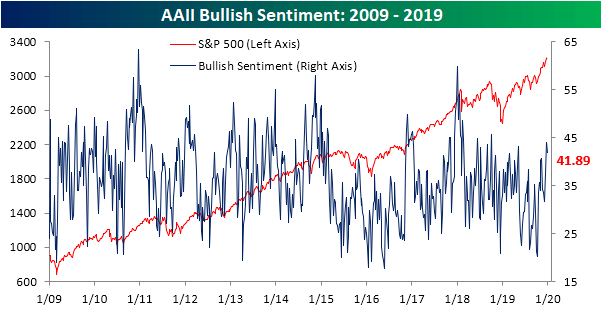

1. AAII Weekly Sentiment — as the major indices continue to establish fresh record highs in the past week with the Nasdaq eyeing an eleventh consecutive up day today, sentiment has actually not shared in moving higher. The reading on bullish sentiment from the AAII fell this week, down to 41.89% from 44.1% last week. Although it is still elevated, currently in the 96th percentile of the past year’s readings, bullish sentiment is less extended than last week and is now back within one standard deviation of its historical average.

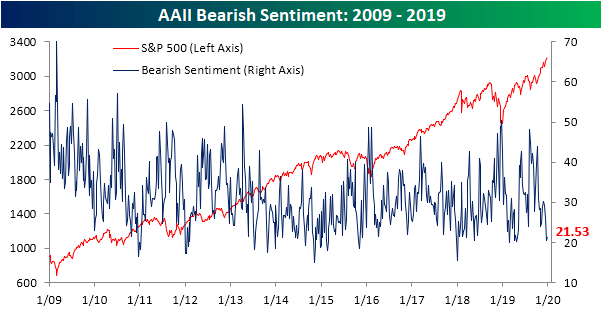

Meanwhile, Bearish sentiment rose just about 1 percentage point this week to 21.53%. As with bullish sentiment, while off of the lowest levels, bearish sentiment is still low relative to where things have stood recently, with this week’s print in the bottom decile of the past year’s readings.

2. Boeing CEO Resigned, Counselor Retires — J. Michael Luttig, who has been managing legal matters associated with the Lion Air and Ethiopian Airlines crashes, will retire from Boeing (NYSE:BA) at year-end. Luttig served as the planemaker’s general counsel since 2006 and assumed his current responsibilities in May 2019. While earlier in the week, CEO Dennis Muilenburg resigned in the wake of the 737 MAX crisis. “The board decided that a change in leadership was necessary to restore confidence in the company moving forward as it works to repair relationships with regulators, customers, and all other stakeholders,” according to a press release. Muilenburg will be replaced by Boeing Chairman David Calhoun, effective January 13, 2020 (CFO Greg Smith will serve as interim CEO during the brief transition period).

3. Super Saturday Sales Top Black Friday by 10% — U.S. consumers are setting more holiday shopping records, as job growth and fatter wallets, along with stronger household finances, have put many in a buying mood this season. Marking the biggest single day in U.S. retail history, Super Saturday (12/21) sales reached $34.4B, topping Black Friday’s $31.2B by 10%, according to Customer Growth Partners. Figures were paced by the ‘Big Four’ mega retailers – Walmart (NYSE:WMT), Amazon (NASDAQ:AMZN), Costco (NASDAQ:COST) and Target (NYSE:TGT) – while online spending this season has so far accounted for 58% of sales growth from a year earlier.

4. China to Cut Tariffs on Range of Goods — China said it will reduce tariffs from Jan. 1 on more than 850 goods, including frozen pork, high-tech components and vital medicines, leading the Shanghai Composite Index to tumble 1.4% overnight. It will also cut import levies for more than 8,000 products for 23 countries and regions that have free-trade agreements with China, known as “most favored nation” rates. While the tariff reduction is not directly linked to the American trade war, it will likely guarantee that the coming Phase One trade deal with the U.S. doesn’t invite complaints from other trading partners.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

December 19th, 2019

“Don’t blindly follow someone, follow market and try to hear what it is telling you.” “You never know what kind of setup market will present to you, your objective should be to find opportunity where risk reward ratio is best.” I do not know what you have received.” — unknown

1. China Makes Move Against Foreign Tech — China’s Communist Party has ordered all state offices to remove foreign hardware and software within three years, FT reported, in a move which could hit Microsoft (NASDAQ:MSFT), Dell (NYSE:DELL) and HP (NYSE:HPQ). Substitutions will take place at a pace of 30% in 2020, 50% in 2021, and 20% the year after, earning the policy the nickname “3-5-2.” Earlier this year, Washington banned U.S. companies from doing business with China’s Huawei, and expanded its blacklist in October to include a number of Chinese surveillance firms like Hikvision.

2. Chevron Gas Assets Take a $10 Billion Hit — in the largest write-down by an energy producer in years, Chevron said that it was cutting the value of a number of properties, notably its U.S. shale holdings in Appalachia, by a combined $10 billion to $11 billion.

3. Aramco Becomes World’s Largest Listed Company — in IPO history, Aramco (ARMCO) shares rose 10% (the daily limit) to 35.2 riyals in Riyadh, raising the company’s valuation to $1.88T and propelling the Saudi Tadawul exchange into the top ten global financial markets. The start of trading of the state-backed oil giant marks the end of a near four-year saga that’s been linked with Crown Prince Mohammed bin Salman’s Vision 2030. The plan hopes to diversify the economy away from energy by pumping funds into mega projects and industries like tourism and entertainment. Aramco valuation hits $2 trillion target. The oil giant’s share price jumped on its second day of trading to reach Saudi Crown Prince Mohammed bin Salman’s coveted valuation target.

4. U.K. Decides the Fate of Brexit — U.K. voters are heading to the polls for a general election that is being seen as a vote on Brexit and will likely shape the country for decades to come. Boris Johnson and his Conservative Party are aiming to win a majority in the 650-seat parliament that will enable them to pass their Brexit deal, formally known as the “Withdrawal Agreement,” and leave the EU by January 31, 2020. Strong short-term impacts are expected on trading floors, but the outcome will also have a long structural influence on U.K. financial asset classes like stocks, sterling and government bonds.

5. FOMC Meeting Recap — the Fed held rates steady and signaled little chance of a near-term move. “Our economic outlook remains a favorable one, despite global developments and ongoing risks,” Jerome Powell said in a statement. President Trump also meets his senior trade team in Washington today about planned Dec. 15 tariffs on nearly $160B in Chinese imports. Many had already expected a Phase One trade deal, but the question now appears to be whether Washington will delay the duties or let them take effect.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

December 10th, 2019

“Stocks take the stairs up and the elevator down.” – unknown

1. Trump Puts Tariffs on Brazil, Argentina, Citing Currencies — A barrage of trade actions was announced by the Trump administration, beginning with tariffs on steel and aluminum from Argentina and Brazil due to a “massive devaluation” of those countries’ currencies. The U.S. Trade Representative also said it would review hiking tariffs on EU products and adding new ones, because of what it called “lack of progress” in resolving a dispute over aircraft subsidies. After the markets closed, the USTR said it planned to slap punitive duties of up to 100% on $2.4B of French products – like Champagne, handbags and cheese – after concluding that a new French digital services tax (DST) would harm U.S. tech companies.

2. Black Friday Online Sales Hit Record $7.4B — online sales rose more than 19.6% to $7.4B on Black Friday, marking the day’s largest revenue grab ever, according to Adobe Analytics, which tracks transactions at 80 of the top 100 U.S. retailers. For Thanksgiving, it estimated web sales grew 14.5% to $4.2B, while Small Business Saturday and Super Sunday sales are projected to surpass $7.6B. Keep an eye today on the usual suspects like Amazon (NASDAQ:AMZN), Walmart (NYSE:WMT), Target (NYSE:TGT) and eBay (NASDAQ:EBAY), as Cyber Monday spending is expected to hit a record $9.4B, an 18.9% jump from a year ago.

3. U.S. Weighing $2.4B of Tariffs in Response to France’s Digital Services Tax — the USTR also threatened that such tariffs could be enacted in the future against Austria, Italy and Turkey, all of which have digital-services taxes. It added that French officials “repeatedly referred to the French DST as the ‘GAFA tax,’ which stands for Google (GOOG, GOOGL), Apple (NASDAQ:AAPL), Facebook (NASDAQ:FB) and Amazon (NASDAQ:AMZN).” Before moving forward with the levies, the agency will hold public hearings on the proposed tariffs on Jan. 7 and will accept public comments through at least Jan. 14,.

4. Aramco Valued at $1.7 Trillion in World’s Biggest IPO — Aramco valued at $1.7 trillion in world’s biggest IPO. Saudi Aramco priced its initial public offering at the high end of the targeted range to give the oil giant a total value of $1.7 trillion. While it ranks as the world’s biggest-ever IPO, the share sale falls well short of the initial $2 trillion valuation targeted by Saudi Crown Prince Mohammed bin Salman.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

December 3rd, 2019

There will not be any re-cap for the week of Nov 29 2019. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 26th, 2019

“When you learn to let go of the need to be right, being wrong gradually lose its power to disturb you.” — unknown

1. Boeing Tried for Deals at Dubai Air Show — Emirates and Boeing are reportedly on the verge of striking a compromise deal for the Middle East’s biggest carrier to order around 30 787 Dreamliners, but fewer 777X jets as part of a delayed order. Boeing (NYSE:BA) has only landed about a third of the orders scored by Airbus (OTCPK:EADSY, OTCPK:EADSF) at the biennial event. Meanwhile, FAA Administrator Steve Dickson stated on the sidelines of the show that the FAA will be tougher on the certification of the Boeing 777X and isn’t following any specific timeline for the return to service of the grounded 737 MAX model. Overall, Airbus (OTCPK:EADSY) scored 220 plane orders during the closely-watched industry event, while Boeing (NYSE:BA) lagged behind with 95 agreements for commercial jets. Boeing still managed to garner sales for its troubled 737 MAX, scoring a total of 50 deals from Air Astana, SunExpress and an unidentified customer. The French planemaker has been ahead for most of 2019. At the end of October, Airbus had posted 542 net orders vs. Boeing’s 45.

2. Disney Sees $100M ‘Frozen 2’ Debut — Disney (NYSE:DIS) is forecasting a hot debut for long-awaited sequel Frozen 2 when it opens on Friday. The company expects the film to draw $100M or so domestically in its first weekend, while some Hollywood estimates are ranging to as high as $105M. The film is set to debut in more than 4,400 theaters in North America. The first Frozen film is the 2nd highest-grossing animated movie of all-time with a global box office haul of $1.29B.

3. FCC Calls for Public C-band Auction — FCC Chairman Ajit Pai announced his support for a public auction to free up C-band spectrum, a key band currently used for delivering video content for next-generation 5G wireless networks. The news sent Intelsat’s (NYSE:I) stock crashing 40%. Major satellite service providers, which hold existing C-band licenses, had proposed selling the spectrum privately to wireless carriers, arguing a private sale would make the spectrum available for 5G faster.

4. China Invited U.S. for More Trade Talks — Beijing’s chief trade negotiator late last week proposed a new round of face-to-face talks, according to people briefed on the matter, as both sides are struggling to strike a limited deal to help de-escalate tensions.

5. FedEx Discontinues Pension for New Hires — Joining the growing ranks of large U.S. companies phasing out guaranteed retirement benefits, FedEx (NYSE:FDX) said it would close its pension plan to new U.S. hires starting in 2020. The shipping giant instead will launch a new 401(k) plan at the start of 2021 with a higher company match (contributing up to 8% of employee salaries, if employees provide 6% of their salary). Just 22% of Fortune 50 companies and 11% of transportation companies offer pensions to new employees.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 18th, 2019

“When you learn to let go of the need to be right, being wrong gradually lose its power to disturb you.” Yvan Byeajee

1. Auto industry Seeks partnerships — Tata Group (NYSE:TTM), the owner of Jaguar Land Rover, has approached carmakers including China’s Geely (OTCPK:GELYY), the owner of Volvo Cars, and BMW (OTCPK:BMWYY) as it seeks partnerships to share the cost of a new generation of vehicles, Bloomberg reports. Scale has become increasingly critical in the auto industry as carmakers pool resources to tackle electrification and self-driving capabilities. Volkswagen (OTCPK:VWAGY) this year decided to team up with Ford (NYSE:F), while PSA Group (OTCPK:PEUGF) last month agreed to merge with Fiat Chrysler (NYSE:FCAU) to create the world’s fourth-largest automaker.

2. Boeing Announces MAX Deliveries Could Resume in December — the planemaker said deliveries of the 737 MAX could begin in December. The company has completed a test of flight control software with the FAA in a simulator, though regulators still must sign off on new pilot training and Boeing needs to conduct a certification flight with officials. Airlines have said they will need at least a month to complete training and install revised software before flights can resume.

3. Disney+ Finally Arrives in Streaming Wars — Disney+ has gone live, challenging the likes of Netflix (NASDAQ:NFLX), Apple TV Plus (NASDAQ:AAPL) and HBO Max (NYSE:T) with a low price of $6.99/month (or $69.99/year). It’ll also offer a triple bundle – including Hulu and ESPN Plus – for $12.99/month. Waves were already made after the Mouse House gave Verizon (NYSE:VZ) customers a free year of the service, as well as broadening device support to nearly every platform: Apple OS, Android, Fire TV, Roku, etc. Disney (NYSE:DIS) has called the service – which will be the exclusive home of Star Wars, Marvel and Pixar – the future of the company, and is building out a slate of original shows and movies based on those brands like The Mandalorian.

4. Goldman Faces ‘Sexist’ Probe Over Apple Card — New York’s Department of Financial Services has initiated a probe into the credit card practices of Goldman Sachs (NYSE:GS) following a series of tweets from David Heinemeier Hansson, the creator of Ruby on Rails. He slammed the Apple Card (NASDAQ:AAPL) for giving him 20x the credit limit than his wife – despite filing joint tax returns and his wife having a better credit score – and alleged that gender discrimination was present in algorithms that determined credit limits. Launched in August, the Apple Card is a joint venture between Apple and Goldman, which is responsible for all credit decisions related to the card.

5. U.S. to extend reprieve for Huawei — as the earlier reprieve expires, the Trump administration will issue another 90-day extension today of a license allowing U.S. companies to continue doing business with Huawei, sources told Reuters. The Chinese firm was added to an economic blacklist back in May on national security grounds. Out of $70B that Huawei spent buying components in 2018, some $11B went to U.S. firms including Qualcomm (NASDAQ:QCOM), Intel (NASDAQ:INTC) and Micron Technology (NASDAQ:MU).

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 12th, 2019

“The intelligent investor is a realist who sells to optimists and buys from pessimists.” – Benjamin Graham

1. Trump Administration is Weighing to Drop Existing Tariffs with China — the Trump administration is weighing whether to drop existing tariffs on $112B of Chinese imports (which were introduced at a 15% rate on Sept. 1). “Phase One” of the pact would include Chinese purchases of American farm goods, rules to deter currency manipulation and some provisions to protect intellectual property and open up Chinese industries to U.S. firms.

2. European Union Aviation Safety Agency Stated Boeing’s MAX Likely to Return to European Service in Q1 2020 –Boeing’s (BA +1.7%) 737 MAX airliner likely will return to service in Europe in Q1 2020, says the head of the European Union Aviation Safety Agency. While the EASE expects to give its approval in January, preparations by national authorities and airlines may delay the resumption of commercial flights by as much as another two months, executive director Patrick Ky says.

3. Walgreens (WBA) Might Goes Private — reports suggested the U.S. drug store chain is exploring private equity interest. If a deal was struck, it would likely be one of the largest leveraged buyouts in history based off Walgreens’ $50B+ market cap. Several private equity firms would likely be involved, though many have long lost their appetite for teaming together on so-called club deals since the financial crisis.

4. U.S. Says Phase-One China Deal Would Include Tariff Rollback — China’s Ministry of Commerce said the world’s two largest economies had agreed to remove duties on each other’s goods in phases. “If China, U.S. reach a phase-one deal, both sides should roll back existing additional tariffs in the same proportion,” declared spokesman Gao Feng. That would potentially provide a road map to end the bruising trade war after reports yesterday suggested a meeting between President Trump and Xi Jinping could be postponed until December.

5. Facebook’s WhatsApp Eplores E-commerce via Catalog Feature — after buying the app for $19B in 2014, Facebook (NASDAQ:FB) is finally building out the service’s e-commerce tools by launching a catalog feature where businesses can display a “mobile storefront” showcasing their wares with images and prices. Facebook similarly added a shopping feature to Instagram in March that lets users click a “checkout” option on items tagged for sale (though transactions there happen directly within the app).

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

November 5th, 2019

The investor of today does not profit from yesterday’s growth. — Warren Buffett

1. Fiat, PSA Confirmed Deal to Merge — Fiat Chrysler and Peugeot owner PSA have officially agreed to join forces through a 50-50 share swap, creating the world’s fourth-largest automaker. “In a rapidly changing environment, with new challenges in connected, electrified, shared and autonomous mobility, the combined entity would leverage its strong global R&D footprint and ecosystem,” the companies said in a statement. The deal calls for paying a special dividend of €5.5B to Fiat (NYSE:FCAU) investors and for PSA (OTCPK:PEUGF) to spin off to its shareholders a €3B stake in parts maker Faurecia (OTCPK:FURCF).

2. China Manufacturing Activity Shrinks Again in October — Factory activity in China contracted for the sixth straight month in October and by more than expected, while service sector growth eased as companies face the weakest economic growth in nearly 30 years. Weighed down by slowing global demand and the Sino-U.S. trade war, the manufacturing PMI fell to 49.3, versus 49.8 in September, according to the country’s statistics bureau. The figures will heap pressure on policymakers to roll out more stimulus to avoid a sharper slowdown and job losses.

3. Fed Cuts Rates for Third Meeting in a Row, Signals Pause — the Federal Reserve cut its benchmark interest rate for the third straight meeting and signaled it may pause before further changes to monetary policy to see whether these easing steps are enough to sustain the economic expansion. At the policy meeting on Wednesday, officials said they would lower the federal-funds target rate by a quarter percentage point, to between 1.5% and 1.75%. Chairman Powell said “Looking ahead, we will be monitoring the effects of our policy actions, along with other information bearing on the outlook, as we assess the appropriate path of the target range for the fed funds rate,” he said. “Of course, if developments emerge that cause a material reassessment of our outlook, we would respond accordingly. Policy is not on a preset course.”

3. LVMH Bids $120 a Share for Tiffany — Tiffany (NYSE:TIF) has received a $120/share offer from LVMH (OTCPK:LVMUY), valuing the company at $14.5B, 22% above Friday’s close. According to informed sources, it will need to sweeten the offer to get the deal done.

4. 5G Goes Online in China — China turned on its 5G networks ahead of schedule on Nov 2nd 2019 – after initially targeting a 2020 launch – amid an ongoing trade war with the U.S. that has turned into a battle over tech supremacy. President Trump said earlier this year that “the race to 5G is on and America must win,” and has been seeking to convince other countries to ban Huawei from their next-generation networks. China Telecom (NYSE:CHA), China Unicom (NYSE:CHU) and China Mobile (NYSE:CHL) all unveiled 5G plans that start at around 128 yuan ($18) per month, though experts have warned of challenges to adoption, including price and a lack of 5G capable handsets.

5. Lagarde Takes Reins of the ECB from Mario Draghi — Christine Lagarde begins her new job atop the European Central Bank today at a time when persistently low inflation and weak growth are showing the limits of monetary policy. Under a 2012 pledge to do “whatever it takes” to save the eurozone from collapse, predecessor Mario Draghi drove interest rates deep into negative territory and pumped trillions of euros into the economy through QE. With an almost exhausted ECB monetary toolkit, unprecedented dissent has broken out between those eurozone members who back this policy and those who are losing faith in further easing.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

October 31st, 2019

There will not be any Weekly Re-Cap for the week of Oct 21 to Oct 25 2019. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

Posted in Weekly Summary | No Comments »

October 22nd, 2019

“Big money is made on the stock market by being on the right side of major moves. The idea is to get in harmony with the market. It’s suicidal to fight trends. They have a higher probability of continuing than not.” – Martin Zweig

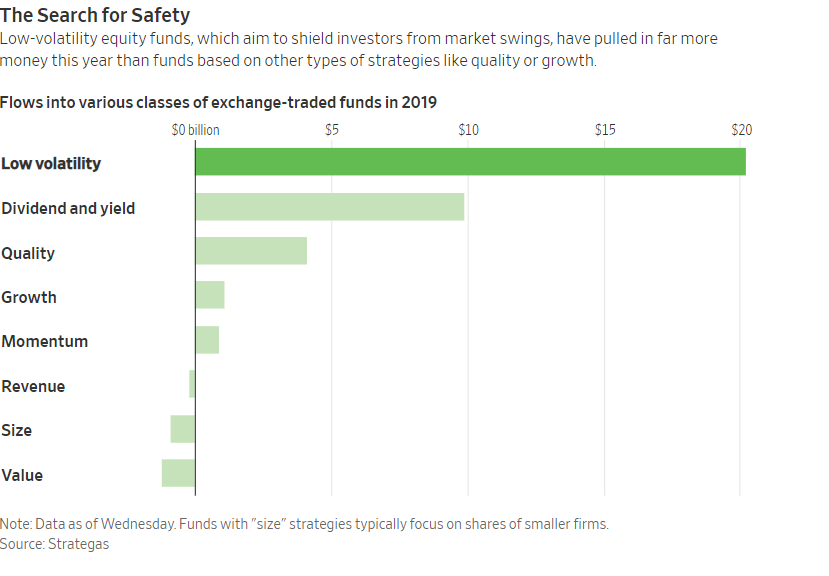

1. Stocks’ Path Toward Records Led by Defensive Plays — much of the gains over the past month have been driven by parts of the market that investors tend to gravitate toward when they are looking for safety, as well as an attractive yield. The S&P 500’s real-estate and utilities sectors, often considered bond-like because of their relatively hefty dividend payouts, have climbed 1.3% and 1.9% respectively over the past month while the broad index has fallen 1%. That makes them by far the best-performing groups in the broad index over that time, followed by technology shares. Exchange-traded funds that aim to minimize investors’ exposure to market swings have also gained popularity, with flows into low-volatility equity ETFs surpassing $20 billion this year—nearly 20 times that of growth stocks, according to Strategas.

2. The U.S. Imposed Sanctions and Raised Steel Tariffs on Turkey — President Trump threatened harsher financial penalties if Turkey continued its offensive in northern Syria, launched after he decided to withdraw U.S. troops from the region. The withdrawal decision was widely criticized on Capitol Hill for leaving Kurdish militias—allies in the U.S.-led fight against Islamic State—open to attack. Mr. Trump also spoke with Turkish President Recep Tayyip Erdogan, calling on him to stop the invasion and negotiate an end to the violence, Vice President Mike Pence said late Monday.

3. U.K., EU Agree on Draft Brexit Deal — Britain and the European Union agreed to new terms for the U.K.’s exit from the bloc late last week, paving the way for a high-stakes vote in the British Parliament.Following days of intense talks more than three years after Britain voted to leave the EU, the two sides struck a compromise intended to ensure a border doesn’t appear on the island of Ireland. It was the main sticking point in negotiations aimed at smoothing Britain’s split with its largest trading partner.

4. UAW Reaches Tentative Labor Deal With GM — the United Auto Workers struck a tentative labor deal with General Motors Co. GM -1.26% on Wednesday, a critical step in ending a monthlong strike that has brought more than 30 GM factories in the U.S. to a standstill. As part of the new deal, GM has committed to invest around $7.7 billion in its U.S. factories over the four-year contract period, which would create or preserve about 9,000 jobs, according to people familiar with the agreement. The company also separately has joined with outside companies to invest another roughly $1.3 billion in facilities near its Lordstown, Ohio, assembly plant, which the company hopes to sell to a startup electric-truck maker, the people said.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »