March 10th, 2020

“An expert in any field will have an advantage over a rookie. But neither the veteran nor the rookie can be sure what the next flip will look like. The veteran will just have a better guess” — Howard Marks

1. Former Vice President Joe Biden Won the South Carolina Democratic Presidential Primary — Pete Buttigieg dropped out of the race, a day after Tom Steyer ended his bid. The rapid ascent of Mr. Sanders in the primaries confronts American business with the once unthinkable: The most powerful policy maker in the world could soon be a strident, lifelong critic of capitalism and big business. Also, SuperTuesday results in Biden sweeps the South, wins Texas; Sanders takes California. Joe Biden notched an impressive string of Super Tuesday victories, while Bernie Sanders won delegate-rich California, as the pair broke away from the field in the race for the Democratic presidential nomination. The Democratic nomination contest has narrowed to essentially a two-person race

2. Washington State Emerged as the U.S. Center of a Spreading Coronavirus — state health officials reported four additional deaths there and 18 confirmed cases, and a number of schools closed for disinfection. The OECD said global economic growth will slow sharply this year as governments attempt to contain the epidemic, although the scale of the setback is highly uncertain. Industries from airlines to oil and energy face weakened business.

3. Federal Reserve Cuts Rates by Half Percentage Point to Combat Virus Fear — the Fed made an emergency half-percentage-point rate cut, the first rate change between scheduled policy meetings since the 2008 financial crisis. But U.S. stock markets fell anyway, and the yield on the benchmark 10-year Treasury note slipped below 1% for the first time, reflecting fears of a coronavirus recession.

4. General Motors is Renewing Its Push to Convince Wall Street on Electric Cars — in a presentation at the company’s engineering center near Detroit, GM executives detailed their strategy, including plans for new battery technology that will allow its vehicles to travel up to 400 miles on a single charge. The company said it would spend $20 billion to develop electric and autonomous vehicles. Investors have so far been putting their money on Tesla as the company best positioned to capitalize on a big swing toward electric vehicles. Tesla’s valuation has soared to more than $130 billion, roughly three times GM’s.

5. The number of U.S. coronavirus cases has risen Rapidly — the number of U.S. coronavirus cases has risen to 206, with 11 deaths. Ten of those deaths are in Washington state. While many of the overall cases are linked to travel, a growing number in certain parts of the country is linked to what is known as community transmission. Community transmission is a milestone for any disease, given that the virus could be circulating among the general public. But U.S. health officials said the mortality rate for the virus was likely lower than what other health organizations have estimated, citing the probability of many unreported cases. Seattle-area companies and schools reacted swiftly. The Northshore School District shut its 33 campuses for up to 14 days, affecting over 23,500 students. Facebook, Amazon and Microsoft all asked many employees to work from home. In California, Gov. Gavin Newsom declared a state of emergency as the number of cases there rose to more than 50. Officials said two New York City residents and nine people in surrounding counties tested positive, bringing the total number of cases in the state to 22.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

March 3rd, 2020

There will not be any re-cap for the week of Feb 28 2020. We are away for some needed R&R.

Have a good week.

The week ahead — Economic data from Econoday.com:

The staffs at EGS.

Tags: Corona Virus

Posted in Weekly Summary | No Comments »

February 27th, 2020

There will not be any re-cap for the week of Feb 21 2020. We are away for some needed R&R.

Have a good week.

The week ahead — Economic data from Econoday.com:

The staffs at EGS.

Posted in Weekly Summary | No Comments »

February 18th, 2020

“The desire for constant action irrespective of underlying conditions is responsible for many losses in Wall Street even among the professionals, who feel that they must take home some money every day, as though they were working for regular wages.” – Jesse Livermore

1. T-Mobile, Sprint Deal Wins Approval, Reshaping Industry — a federal judge’s approval of T-Mobile’s takeover of Sprint will test whether three giants will compete as aggressively for cellphone users as four unequal players once did. The opinion will leave most of the country’s wireless customers with three major network operators: Verizon Communications Inc., AT&T Inc. and the new T-Mobile. New entrant Dish plans to use the deal as a springboard for its mobile ambitions, while U.S. cable companies are stuck with existing providers’ networks for their fledgling cellular services.

2. President Trump Unveilled $4.8 trillion budget — President Trump budget will propose steep reductions in social-safety-net programs and foreign aid and higher outlays for defense and veterans. The plan would increase military spending 0.3%, to $740.5 billion for fiscal year 2021, which begins Oct. 1. It will request $2 billion in new funding for border-wall construction, significantly less than the amount it sought last year. The proposal is unlikely to become law, however, as Democrats control the House and spending bills in the GOP-led Senate need bipartisan support.

3. FTC Expands Antitrust Investigation Into Big Tech — the Federal Trade Commission ordered five big tech companies to provide detailed information about their previous acquisitions of small companies, expanding the agency’s investigation into possible antitrust concerns in digital markets. The FTC ordered the companies— Amazon. com Inc., Apple Inc., Facebook Inc., Microsoft Corp. and Google owner Alphabet Inc. —to turn over information and documents relating to the scope, structure and purpose of their takeovers of smaller companies between 2010 and 2019.

4. Bernie Sanders Wins New Hampshire Primary — Sen. Bernie Sanders won the New Hampshire Democratic presidential primary Tuesday night in a narrow victory that ensures the race to challenge President Trump this November will remain heated.

With more than 85% of precincts reporting, Mr. Sanders, who is from neighboring Vermont, had 25.7% of the vote, followed by Pete Buttigieg with 24.4% and Sen. Amy Klobuchar of Minnesota with 19.7%. Sen. Elizabeth Warren of Massachusetts and former Vice President Joe Biden, who each have previously led the Democratic field in national polling, lagged well behind with less than 10% of the vote.

4. Mobile World Congress Called Off Amid Virus Worries — with swaths of individual companies pulling out of the exhibition over the past week, the GSMA telecoms association that hosts the get-together has called off the Feb. 24-27 event. Fears over the coronavirus outbreak were to blame despite assurances from local and national health officials that it would have been safe to hold it. The Mobile World Congress draws more than 100,000 visitors to Barcelona and is known as the year’s biggest event for the telecom industry.

5. Huawei Charged With Racketeering, Stealing Trade Secrets — Huawei Technologies Co. and two of its U.S. subsidiaries were charged with racketeering conspiracy and conspiracy to steal trade secrets in a federal indictment. Federal prosecutors in Brooklyn said the new charges related to a decadeslong effort by Huawei and its subsidiaries, in the U.S. and China, to steal intellectual property, including from six U.S. technology companies. Prosecutors said Huawei’s efforts were successful and resulted in the company obtaining nonpublic intellectual property about robotics, cellular-antenna technology and internet-router source code. The alleged thefts allowed the company to cut costs and research-and-development delays, giving it an unfair competitive advantage

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

February 10th, 2020

‘Look, everybody has a pain threshold, and you know when a stock becomes unmoored from valuations, [because] it has certain dynamic growth aspects to it and has cultlike aspects to it — you just have to walk away.’ — Steve Eisman about Tesla short

1. Chinese Leader Xi Jinping Called the Coronavirus a Major Test of China’s System of Governance — Mr. Xi told a special meeting of the Communist Party’s ruling Politburo Standing Committee there would be consequences for officials who shirk responsibility in tackling the crisis. the number of confirmed coronavirus cases in mainland China rose above 42,000. The death toll from the outbreak climbed above 1,000, while Hong Kong reported its first death from the pathogen. Macau moved to shut its casinos—whose revenues are more than six times that of the Las Vegas Strip—for two weeks. American health authorities reported a second case of passage from one person to another in the U.S., and raised the number of confirmed cases to 11. Companies, governments and schools are developing policies on the fly to try to halt the spread, creating a live global public-health experiment in containment.

2. State of the Union Address — President Trump touted his record in a lengthy and triumphal State of the Union. Ahead of today’s anticipated acquittal in his impeachment trial, the president used his annual address Tuesday to paint an optimistic picture of America’s future and present himself as the lead architect of the country’s economic boom. He avoided commenting on impeachment.The speech was punctuated by enthusiastic applause from Trump backers and mostly silence from Democrats; House Speaker Nancy Pelosi notably ripped her copy of the speech in half as Mr. Trump finished.

3. Disney Emerges as a Formidable Streaming Contender — the number of subscribers to the company’s new streaming service, Disney+, more than doubled in its first three months. CEO Robert Iger said older programming, ranging from classic Disney movies to seasons of “The Simpsons,” has been as popular with Disney+ subscribers as its new, original content such as “The Mandalorian.” Disney+ is already competing with Netflix, Amazon and Apple in the market. Netflix, the largest streaming platform, started offering streaming in 2007 and created a stand-alone streaming plan in 2010. It didn’t cross 28 million subscribers until late 2012, according to its financial statements.

4. Senate Acquits Trump on Both Impeachment Articles — the Republican-led Senate acquitted the president of charges stemming from his efforts to press Ukraine to announce investigations that would benefit him politically. The vote to acquit marked a clear victory for the president. GOP senators strongly supported his acquittal, but several said Democrats had proved that he acted improperly—though not in a manner deserving of impeachment—regarding Ukraine. Utah Sen. Mitt Romney was the lone Republican to vote to convict and remove Mr. Trump from office.

5. China to Cut in Half Tariffs on $75 Billion of U.S. Goods — China said it would cut tariffs on $75 billion of U.S. imports in half as part of efforts to implement a recently signed trade agreement with Washington. The tariff cuts set to take effect on Feb. 14 come amid growing doubts about Beijing’s ability to follow through on the phase-one trade deal, in which China has pledged to boost its purchases of American goods and services by $200 billion over two years.

The U.S. trade deficit narrowed in 2019 for the first time in six years, as disputes with China and other countries reduced the U.S.’s exports and imports while reshaping relationships with economic partners. Exports declined for the first time since 2016, dropping 0.1%, the Commerce Department said. But imports fell more sharply, decreasing 0.4%. That combination shrank the overall trade deficit 1.7%, to $616.8 billion. U.S. tariffs on roughly $370 billion in annual Chinese imports remain in place.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

February 4th, 2020

“The markets are always changing, and the successful trader needs to adapt to these changes” — Michael Stainhardt

1. Yield Curve Inverted — the U.S. Treasury yield curve, measured by the gap between yields on three-month and 10-year bonds, briefly inverted overnight for the first time since October as Treasuries rallied for a sixth day. The two-year/five-year curve already inverted on Monday, while the gap between two-year and 10-year yields – considered a recession signal – was at the flattest since Nov. 29. “If the signs were to multiply, there could be a more severe impact not just in China but globally,” said Philip Shaw, chief economist at Investec. “Markets are starting to speculate the Fed could bring rates down by summer.”

2. Flights To/From China Suspended as Coronavirus Spreads — British Airways became the first global airline to cancel all flights to and from the mainland as the virus spreads beyond Asia. The U.S. expanded passenger screenings for the virus to 20 airports and is considering suspending flights to China.

3. Corona Virus Updates — the coronavirus has killed at least 165 people while infecting more than 7,000. The vast majority of those infected are in China. Corona virus has a relatively high death rate compared with something like influenza (though less than the related SARS outbreak nearly two decades ago). And it is centered in a densely populated part of the world where international travel is increasingly common. It’s also new. Public health experts cannot say yet how long it will last, how far it will spread, and how deadly it could get. Public-health officials say the virus and the respiratory ailments it causes pose little risk in the U.S., where only 5 cases have been identified. And while there’s evidence it’s contagious even in the early stages before symptoms show, it appears to be far less contagious than SARS, whooping cough or measles. In addition, the outbreak is disrupting businesses around the world, from banks to retailers to airlines. Global firms are working to protect employees in or planning travel to China, while also dealing with dropping demand and its potential economic impact. Investors who began the year feeling largely sanguine about the stock market are struggling to make sense of whether the growing outbreak could upend their bets on a global economic recovery.

4. UPS Aims for Driverless, Electric Future — following in the footsteps of Amazon (AMZN), which recently inked a deal for 100,000 electric vehicles from Rivian, UPS (NYSE:UPS) has placed an order for 10,000 electric vans (with an option for 10,000 more) from U.K.-based Arrival. The contract, worth “hundreds of millions of euros,” will also see UPS take a minority stake in the startup. Besides joining the EV revolution, UPS has driverless dreams. A six-month test will begin with Alphabet’s (GOOG, GOOGL) Waymo next month, using the latter’s autonomous Chrysler Pacifica minivans to shuttle packages from Phoenix UPS stores to a nearby sorting center.

5. FOMC Meeting — the Federal Reserve left its benchmark interest rate unchanged and reaffirmed its make-no-moves posture. Officials repeated nearly verbatim the policy outlook expressed in December, and offered a mixed assessment of the economic outlook. They described consumer spending as moderate, a downgrade from “strong” last month, and said business investment had stayed weak. Fed officials have, however, signaled that they see greater risks of surprises that could force them to lower rates.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 28th, 2020

“The secret to being successful from a trading perspective is to have an indefatigable and an undying and unquenchable thirst for information and knowledge.” — Paul Tudor Jones

1. A Newly Identified Virus Originating in Central China has Spread Between Humans — with a diagnostic test available, the number of confirmed cases more than tripled to 218—including in Beijing, Shanghai and Shenzhen—with three deaths from the pneumonia the virus causes. The prospect of human-to-human transmission, rather than just animal-to-human, comes as tens of millions of Chinese crisscross the country for the Lunar New Year holiday—commonly called the world’s largest annual human migration—though more are staying put this year. The virus has already spread outside China, and appeared in South Korea for the first time.

2. France, U.S. Declare Digital Tax Truce — averting another trade war – for now – the U.S. and France have agreed to put aside their digital tax dispute until the end of 2020. Negotiations at the OECD will continue during that period as France postpones the levy and the U.S. delays retaliatory tariffs. The measure had imposed a 3% tax on digital revenues of companies like Google (GOOG, GOOGL), Apple (NASDAQ:AAPL), Facebook (NASDAQ:FB) and Amazon (NASDAQ:AMZN) – which have more than €750M in global revenue, including at least €25M in France – while the U.S. had threatened to place duties of up to 100% on $2.4B of French imports.

3. The Chinese Government Locked Down Cities in an Effort to Stop the Spread of a New Coronavirus — the government locked down Wuhan, the city of 11 million people where the new virus originated. Authorities announced later that nearby Huanggang, with 7.5 million people, was slated for lockdown at midnight. Ezhou, another neighboring city with just over a million residents, said it would enact similar restrictions. Under the lockdowns, all outbound flights, trains, long-distance buses and ferries are halted, and public transportation is shut. Markets, movie theaters and other public places have been closed or had access restricted. The lockdowns constitute a dramatic escalation in the battle to contain a pneumonia outbreak that has killed at least 17 people.

4. Boeing CEO Updates — the new Boeing (NYSE:BA) CEO said the planemaker will not cut its dividend despite the extended grounding of the 737 MAX and expects to resume MAX production “months” before the mid-year return to service. The latest delay was triggered by the company’s recommendation that pilots should undergo simulator training. He’ll also “start with a clean sheet of paper” on a decision whether to launch a new midsize airplane seating 220-270 passengers, effectively halting current plans worth $15B-20B.

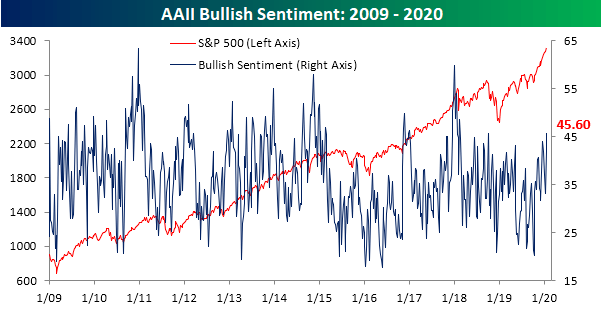

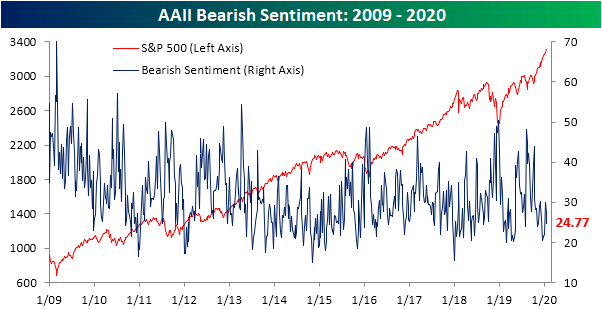

5. AAII’s Investor Sentiment Survey — In the span of just two weeks, the percentage of respondents in AAII’s investor sentiment survey reporting as bullish has risen from the middle of the past few years’ range of 33.07% to 45.6% (and from 41.83% last week), the highest reading since early October 2018. Back then, bullish sentiment peaked out just slightly higher at 45.66%, before turning lower as stocks sharply sold off.

In spite of the strong bullish reading, bearish sentiment was actually lower in the final weeks of 2019 and the first week of this year. Now at 24.77%, bearish sentiment is low but still within a normal range of one standard deviation of the past year’s average of 30.04%.

The week ahead — Economic data from Econoday.com:

Tags: Corona Virus

Posted in Weekly Summary | No Comments »

January 20th, 2020

“When you learn to let go of the need to be right, being wrong gradually lose its power to disturb you.” — unknown

1. Big Tech Dominates the S&P 500 — the recent Big Tech surge is good news for anyone chasing the sector higher, but several strategists highlight it’s a sign investors have lost their risk appetite. The top five publicly traded American companies – Apple (NASDAQ:AAPL), Microsoft (NASDAQ:MSFT), Alphabet (GOOG, GOOGL), Amazon (NASDAQ:AMZN) and Facebook (NASDAQ:FB) – now make up a record 18% share of the S&P 500 Index’s capitalization. That ratio is higher than the tech bubble, according to Morgan Stanley, amid fears the economic cycle will slow.

2. The U.S. and China signed a trade deal, calling a cease-fire in a two-year trade war — Officials said the eight-part agreement will lead to an increase in sales of U.S. goods and services to China, further open Chinese markets to foreign firms—especially in financial services—and provide strong new protections for trade secrets and intellectual property. But it leaves in place U.S. tariffs on about $370 billion in Chinese goods, and possible tariff reductions will be left to later negotiations that will also cover a host of difficult issues. U.S. business leaders generally applauded the pact, but stressed the need to keep negotiations going.

3. Change in Media Access to Market Data — the Trump administration plans to restrict the news media’s ability to prepare advance stories on sensitive U.S. economic data such as inflation and employment, Bloomberg reports. “Lockups” lasting 30 to 60 minutes are currently hosted in Washington for major reports, where journalists receive data in a secure room and transmit them when connections are restored at release time. The change, which could remove computers from the lockup room, would transform how critical market-moving information is distributed to investors and the public.

4. Nestle Spending Big on Recycled Plastic — vowing to make 100% of its packaging recyclable or reusable by 2025, Nestle (OTCPK:NSRGY) is investing as much as 2B Swiss francs to source more recycled plastics to package its products. It will also try to keep the plastic purchasing neutral on earnings through efficiencies. Rival Unilever (NYSE:UN) has further pledged to halve its use of newly made plastic by 2025 as food and beverage makers increasingly come under fire for polluting oceans and landfills.

5. Google parent Alphabet became the fourth U.S. company to achieve a $1 trillion market value — The milestone punctuated a powerful rally in shares of large internet stocks to start 2020. The search-engine giant joins tech peers Apple, Amazon and Microsoft as the only companies to reach the threshold during intraday trading. The biggest tech companies have continued to soar in value, highlighting how investors favor companies that steadily improve sales despite tepid global economic growth.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 13th, 2020

“Commodities tend to zig when the equity markets zag.” – Jim Rogers

1. Boeing Eyes Raising More Debt as 737 MAX Costs Rise — Boeing is examining plans to issue more debt to bolster finances strained by the mounting fallout from the grounding and halted production of its 737 MAX, according to people familiar with the matter. The aerospace giant had about $20 billion in available funds at the end of the September quarter, but costs associated with the MAX crisis are rising. Analysts expect Boeing to raise as much as $5 billion to help cover expenditures that could top $15 billion in the first half of this year. In addition to spending on maintenance for the grounded MAX fleet and finished planes, the company plans to close its $4 billion acquisition of an 80% stake in the Brazilian plane maker Embraer’s commercial airliner business. Boeing also has to repay some existing debt and fund shareholder dividends. In addition, Boeing (NYSE:BA) is reassigning 3,000 workers to other jobs, but does not expect to furlough any staff, as it halts production of its grounded 737 MAX in mid-January. Major supplier Spirit AeroSystems (NYSE:SPR) meanwhile said it would offer voluntary layoffs to some employees due to a lack of “clarity on the timing for resuming MAX production.” The announcements come after American Airlines (NASDAQ:AAL) and Mexico’s Aeromexico disclosed they were the latest carriers to reach settlements with Boeing over losses resulting from the 737 MAX crisis.

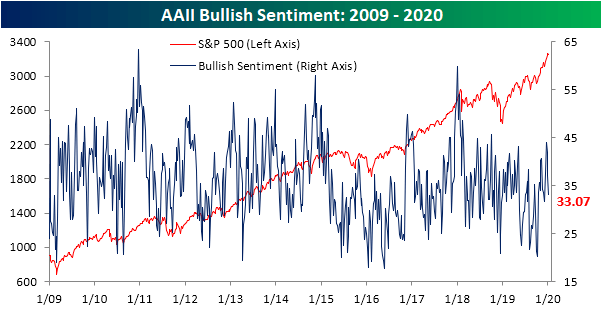

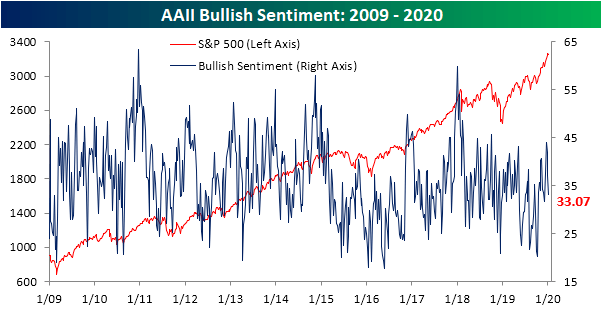

2. AAII Sentiment Survey — In the latest survey, the percentage of bullish investors in the weekly AAII survey has fallen for a third straight week down to 33.07%. This is the lowest level of bullish sentiment since the first week of December, when 31.72% of respondents were bullish. Granted, these declines have not brought bullish sentiment to any sort of extremely low level. In fact, it is now just about in line with the average reading of the past year, 33.41%.

Meanwhile, Nearly 30% of investors reported as bearish this week, which was an 8.01 percentage point increase from last week. That marked the third-largest one week jump in bearish sentiment of the past year. Granted, this increase was also about a third and half the size, respectively, of the past two larger increases of 24.14 percentage points in August and 16.11 percentage points in May. Despite the relatively large move higher, bearish sentiment is now right in line with its average of 30.3% over the past year.

3. Iran Admits to Shooting Down Jetliner — For days, Iran’s government had denied responsibility for the crash of a Boeing (NYSE:BA) 737-800 near Tehran, though it’s now calling the incident that killed 176 people a “disastrous mistake.” The country’s air defenses were fired in error while on alert after Iranian missile strikes targeted U.S. bases in Iraq. Local officials had previously pointed to an engine failure as the cause of the crash. The plane’s turbines were made by CFM International, a joint venture between General Electric (NYSE:GE) and France’s Safran (OTCPK:SAFRY).

4. SEC to Propose Exchanges Revamp Data Feed Policies — a proposal advanced by the SEC takes aim at a two-tier system that allows trading platforms like the New York Stock Exchange (NYSE:ICE) and Nasdaq (NASDAQ:NDAQ) to charge their largest customers higher fees for faster proprietary feeds, leaving smaller players to rely on a slower public stream. If the regulator decides to issue an order after receiving public input, the exchanges and FINRA would have to create a new governance plan, which would also be published for public comment before the SEC takes it into consideration.

5. Consumer Electronics Show 2020 Recap — Uber (NYSE:UBER) and Hyundai Motor (OTCPK:HYMLF) are partnering to develop electric air vehicles, joining the global race to make small self-flying cars to ease urban congestion. Samsung Electronics (OTC:SSNLF) demonstrated what it called the world’s first artificial human, Qualcomm (NASDAQ:QCOM) launched an autonomous driving computer and Toyota (NYSE:TM) said it’s building the prototype city of the future in Japan. Amazon (NASDAQ:AMZN) is also teaming up with Lamborghini and Rivian to offer its Alexa voice assistant in vehicles.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

January 7th, 2020

“Don’t blindly follow someone, follow market and try to hear what it is telling you.” “You never know what kind of setup market will present to you, your objective should be to find opportunity where risk reward ratio is best.” — unknown

1. Market Highlights from 2019 — it was another exciting year for investors in 2019 amid a stock market rally that saw the S&P 500 surge 28%, for the biggest gain since 2013. Easing trade tensions with China, a shift in monetary policy at the Fed, and improving economic outlook all renewed investors’ faith, while safer assets like gold and bonds also soared. Other notable highlights: Tech domination, M&A activity, streaming wars, vaping crackdown, American energy independence, hot IPO market, the EV revolution, 737 MAX crisis, record holiday shopping and getting Brexit over the line.

2. Oil Service Firm McDermott in Bankruptcy Talks with Lenders — WSJ reported that the engineering firm is in talks with its lenders to file for bankruptcy within weeks. The group may provide an approximately $2B loan to keep the company’s operations running during bankruptcy, while the financing would afford McDermott the ability to provide letters of credit, most of which expire within a year and need to be renewed for the firm to continue its work on projects.

3. People’s Bank of China’s Injection of Fresh Liquidity into Banking System to Start the New Year — the festivities kicked off in Asia in the new year, where the PBOC slashed its required cash reserve ratio for commercial lenders by 50 basis points, unleashing about 800B yuan ($115B) of liquidity into the financial system. The move to shore up the local economy saw the Shanghai Composite Index end the session up 1.2%, adding to the overall positive sentiment ahead of the signing of a ‘Phase One’ U.S.-China trade deal on Jan. 15.

4. More Drugmakers Hike U.S. Prices as 2020 Begins — the drug price hike of 2020 has commenced, with costs rising for more than 250 medications, according to data analyzed by 3 Axis Advisors. Bristol-Myers Squibb (NYSE:BMY), Gilead Sciences (NASDAQ:GILD), and Biogen (NASDAQ:BIIB) hiked U.S. list prices on more than 50 drugs on New Year’s Day, adding to the couple hundred increases from drugmakers including Pfizer (NYSE:PFE), GlaxoSmithKline (NYSE:GSK) and Sanofi (NASDAQ:SNY). While nearly all of the price increases are below 10% and the median price increase is around 5%, more early year price increases could still be announced.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »