July 5th, 2022

“In my view, the greatest way to optimize the positioning of a portfolio at a given point in time is through deciding what balance it should strike between aggressiveness and defensiveness. And I believe the aggressiveness/defensiveness balance should be adjusted over time in response to changes in the state of the investment environment and where a number of elements stand in their cycles.” ― Howard Marks

1. Russia Defaults on Foreign Debt for First Time Since Communist Revolution — the Russian government was unable to compensate creditors on about $100 million of interest denominated in dollars and euros after a 30-day grace period following the May 27 deadline expired. Although President Vladimir Putin’s administration has the funds, reserves at Russia’s central bank are frozen and the biggest commercial banks are unable to trade in international markets under sanctions following Moscow’s invasion of Ukraine in February. Bondholders themselves will probably want to wait before formally starting default proceedings in the hope of being paid back after the war is over. Declaring default now would force Russia to pay back the principle on the loans immediately, but the same sanctions preventing interest payments would also stop those payments as well.

2. U.S. Bans Russian Gold Imports, Blacklists State-Owned Rostec — the U.S. has banned imports of Russian gold, broadening sanctions against the country following the Kremlin’s invasion of Ukraine in February, the U.S. Treasury Department said Tuesday. The Treasury on Tuesday also blacklisted 70 groups, many of which the U.S. said are critical to Russia’s defense industrial sector, including state-owned defense conglomerate Rostec, as well as 29 Russians. The official ban on new imports of Russian gold comes as Moscow’s invasion of Ukraine continues into its fourth month. The U.S. and the U.K. announced the move on Sunday during a Group of Seven meeting in the Bavarian Alps, with the rest of the G-7 joining the ban. Gold is Russia’s second most valuable export after energy and “rakes in tens of billions of dollars,” President Biden tweeted.

3. Powell Says Fed Must Accept Higher Recession Risk to Combat Inflation — Federal Reserve Chairman Jerome Powell said he was more concerned about the risk of failing to stamp out high inflation than about the possibility of raising interest rates too high and pushing the economy into a recession. Mr. Powell said the central bank had to raise rates rapidly, even if that raises the risk of recession, to avoid a worse danger for the economy—of higher inflation becoming entrenched. He said the Fed didn’t have the luxury of moving rates up gradually because of concern that the recent period of high inflation may lead consumers and price setters to expect elevated prices to persist. Central banks across the globe are in a hurry to raise interest rates amid surging price pressures. Rising fuel costs and supply-chain disruptions from Russia’s war against Ukraine have sent prices higher in recent months. In the U.S., such increases are adding to inflation that was already high as demand surged last year from the reopening of the economy and aggressive government stimulus.

4. Markets Post Worst First Half of a Year in Decades — Accelerating inflation and rising interest rates fueled a monthslong rout that left few markets unscathed. The S&P 500 fell 21% through Thursday, suffering its worst first half of a year since 1970, according to Dow Jones Market Data. Investment-grade bonds, as measured by the iShares Core U.S. Aggregate Bond exchange-traded fund, lost 11%—posting their worst start to a year in history.

Stocks and bonds in emerging markets tumbled, hurt by slowing growth. And cryptocurrencies came crashing down, saddling individual investors and hedge funds alike with steep losses. investors seem to be in agreement about only one thing: More volatility is ahead. That is because central banks from the U.S. to India and New Zealand plan to keep raising interest rates to try to rein in inflation. The moves will likely slow down growth, potentially tipping economies into recession and generating further tumult across markets.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 27th, 2022

“When the demand for goods increases relative to the supply, there can be “demand-pull” inflation. When inputs to production such as labor and raw materials increase in price, there can be “cost-push” inflation. Finally, when the value of an importing country’s currency declines relative to that of an exporting country, the cost of the exporter’s goods can rise in the importing country.” ― Howard Marks

1. Fed Chair Jerome Powell Says Higher Interest Rates Could Cause a Recession — Federal Reserve Chairman Jerome Powell said the central bank’s battle against inflation could lead it to raise interest rates high enough to cause an economic downturn. His remarks underscore the challenge facing the central bank as it raises interest rates at the most rapid clip since the 1980s to slow the economy and cool inflation. Mr. Powell said the Fed plans to continue raising interest rates until it sees clear proof that inflation is slowing to the central bank’s 2% target. Officials raised interest rates by 0.75 percentage point last week, the largest increase since 1994, and Mr. Powell and several colleagues have signaled that another such increase could be warranted at their next meeting, July 26-27.

2. FDA to Order Juul E-Cigarettes Off U.S. Market — the Food and Drug Administration is preparing to order Juul Labs Inc. to take its e-cigarettes off the U.S. market, according to people familiar with the matter. Uncertainty has clouded Juul since it landed in the FDA’s sights four years ago, when its fruity flavors and hip marketing were blamed for fueling a surge of underage vaping. The company since then has been trying to regain the trust of regulators and the public. It limited its marketing and in 2019 stopped selling sweet and fruity flavors. Juul’s sales have tumbled in recent years.

3. U.S., European Economies Slow Sharply as Recession Risks Grow — the U.S. and European economies slowed sharply in June as surging prices of energy and food weakened demand for other goods and services, business surveys showed, increasing the risk of recessions around the world. Data firm S&P Global said on Thursday that its U.S. composite purchasing managers index—which measures activity in both the manufacturing and services sectors—fell to 51.2 in June from 53.6 the previous month to reach a five-month low. In the eurozone, the index fell to 51.9 in June from 54.8 in May, a 16-month low. A reading above 50.0 points to an expansion in activity, while a figure below that threshold points to a contraction.

4. Supreme Court Overturns Roe v. Wade, Eliminates Constitutional Right to Abortion — a deeply divided Supreme Court eliminated the constitutional right to an abortion, overruling the 1973 Roe v. Wade decision and leaving the question of abortion’s legality to the states.

The court’s decision in Dobbs v. Jackson Women’s Health Organization upheld a law from Mississippi that bans abortion after 15 weeks of pregnancy, roughly two months earlier than what has been allowed under Supreme Court precedent dating back to Roe. In siding with Mississippi, the court’s conservative majority said the Roe decision was egregiously wrong in recognizing a constitutional right to an abortion, an error the court perpetuated in the decades since. “The Constitution makes no reference to abortion, and no such right is implicitly protected by any constitutional provision,” Justice Samuel Alito wrote for the court.

5. CDC Recommends Moderna’s Covid-19 Vaccine for Kids 6 to 17 Years — the Centers for Disease Control and Prevention recommended use of Moderna Inc.’s Covid-19 vaccine in children ages 6 to 17 years. The CDC’s move on Friday means the youths, who have been able to get the Covid-19 vaccine made by Pfizer Inc. and its partner BioNTech SE, will also have the choice of Moderna’s shot. Uptake of Moderna’s shot in the age group might be limited, however, since many eligible children have gotten the Pfizer-BioNTech shot. About 60% of 12- to 17-year-olds and 30% of children ages 5 to 11 are fully vaccinated against Covid-19, according to the American Academy of Pediatrics.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 21st, 2022

“We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.” — Warren Buffett

1. Fed Hikes 75 Basis Points, Powell Says 75 or 50 Likely in July — the Federal Reserve raised interest rates by 75 basis points — the biggest increase since 1994 — and Chair Jerome Powell signaled another big move next month, intensifying a fight to contain rampant inflation. He said another 75 basis-point hike, or a 50 basis-point move, was likely at the next meeting of policy makers. They forecast interest rates would rise even further this year, to 3.4% by December and 3.8% by the end of 2023.

2. Bitcoin Price Falls Toward $20,000 as Cryptocurrency Rout Deepens — Cryptocurrencies extended their slide, with bitcoin on the verge of falling below $20,000 for the first time since December 2020. The rout in cryptocurrencies has wiped out roughly 1½ years of gains for bitcoin, which started to soar at the end of 2020 as speculative fervor washed over financial markets. Two high-profile incidents in recent weeks have accelerated cryptocurrencies’ fall. In May, the collapse of stablecoin TerraUSD and its sister token Luna prompted a selloff across cryptocurrencies.

3. Celsius Is Crashing, and Crypto Investors Are Spooked — late last week, Celsius said it was no longer allowing customers to withdraw cash from their accounts. Last Tuesday night, The Wall Street Journal reported that Celsius hired restructuring attorneys to help handle its mounting financial problems. Prices for bitcoin and other cryptocurrencies have been plummeting as interest rates rise and risky assets turn unpopular. The difficult market is forcing once-highflying digital-currency companies to slash jobs, halt mergers and bar clients from withdrawing digital investments, shocking investors. Individual investors might not have realized when they put money in Celsius that they were giving the company an unsecured loan with little legal protection. Crypto companies such as Celsius look like banks in some ways, but they lack the investor oversight and legal protections built into banks and brokerages.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 14th, 2022

“Patient opportunism, buttressed by a contrarian attitude and a strong balance sheet, can yield amazing profits during meltdowns.” ― Howard Marks

1. World Bank Warns of Stagflation Risk, Cuts Global Growth Forecast to 2.9% — the World Bank sharply lowered its growth forecast for the global economy for this year, warning of several years of high inflation and tepid growth reminiscent of the stagflation of the 1970s.

Citing the damage from the war in Ukraine and the Covid-19 pandemic, the bank said global growth is expected to slump to 2.9% in 2022 from 5.7% in 2021, significantly lower than its January forecast for 4.1% growth. Furthermore, growth is expected to hover around the reduced pace over 2023 and 2024 as the war disrupts human activity, investment and trade while governments withdraw fiscal and monetary support.

2. Moderna Booster Targeting Omicron Shows Stronger Immune Response Than Original Vaccine — Moderna modified Covid-19 booster shot that targets the Omicron coronavirus variant showed a stronger immune response than the original vaccine. The modified “bivalent” booster shot—mRNA-1273.214—targets both Omicron and the original variant, and was well-tolerated in a study with 437 participants, according to preliminary data. The company’s updated vaccine had side effects comparable to the original booster dose but produced eight times more antibodies, the press release stated. Moderna (ticker: MRNA) will submit the analysis to U.S. regulators in the coming weeks, with the hope that the booster dose will be available in the late summer.

3. U.S. Considering Reducing Tariffs on China to Ease Inflation — treasury Secretary Janet Yellen said the Biden administration is considering ways to reconfigure tariffs on imports from China as a means of helping to ease decades-high inflation. The Biden administration has been split on whether to pare back tariffs on imports from China in an effort to cut consumer costs and reduce inflation. The administration has been engaged in a legally required review of the Trump-era tariffs. Easing the tariffs could take the form of expanding the list of items excluded from the duties.

4. ECB Plans July Rate Increase as Inflation Problem Deepens — in an unusually detailed statement, the ECB said it intends to raise its key rate by a quarter percentage point at its next policy meeting in July to minus 0.25%, and increase it again in September, possibly by more than 0.25 percentage point. It said it would end its large-scale bond-buying program on July 1. After September, the ECB said it expects a “gradual but sustained path of further increases in interest rates.” Unusually, the bank published its new staff inflation forecasts in its policy statement. They show eurozone inflation of 3.5% in 2023 and 2.1% in 2024, both above the ECB’s target rate.

5. U.S. Inflation Hit 8.6% in May — the Labor Department on Friday said that the consumer-price index increased 8.6% in May from the same month a year ago, marking its fastest pace since December 1981. That was also up from April’s CPI reading, which was slightly below the previous 40-year high reached in March. The CPI measures what consumers pay for goods and services. May’s increase was driven in part by sharp rises in the prices for energy, which rose 34.6% from a year earlier, and groceries, which jumped 11.9% on the year, the biggest increase since 1979. But inflation pressures were distinctly broad-based in May, said Sarah House, senior economist at Wells Fargo Securities.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 6th, 2022

THERE WILL NOT BE ANY POSTING FOR THE WEEK OF JUNE 3RD 2022 — WE ARE AWAY FOR SOME NEEDED R&R

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

June 3rd, 2022

1. Fed Sees Half-Point Rate Hikes at the ‘Next Couple of Meetings. — minutes from the Fed’s May 3-4 meeting, at which the central bank raised interest rates by a half point to a range of 0.75%-1% and unveiled plans to begin reducing the size of its balance sheet, echoed an urgency to tackle inflation that Fed Chairman Jerome Powell said was a priority in his postmeeting press conference. But they also show that the Fed hopes to become more “data dependent” at future meetings amid an uncertain economic outlook. The Fed’s policy-making arm, the Federal Open Market Committee, meets next on June 14-15 and then July 26-27.

2. ECB Signals Delayed Bond Runoff, Diverging From Fed — the European Central Bank is likely to hold on to its mammoth portfolio of sovereign debt as it starts to raise interest rates, ECB officials said, underlining the fine line it is walking as it tightens monetary policy to battle inflation while trying not to weaken the bloc’s most fragile economies. The Fed, the ECB and other major central banks sucked up trillions of dollars of government and private debt during the pandemic to support financial markets and the economy. Now, investors are focusing on whether and how central banks unload those assets, which will have big repercussions for asset prices and bond yields.

3. US Home Sellers Cutting Prices Hits Highest Level Since 2019 — nearly one in five sellers dropped prices during the four week period ended May 22, Redfin Corp. said in a report Thursday. Other measures of how hot the market is, including a house’s time on market and the percentage of homes selling above listing price, have also plateaued. Consumers are contending with some of the highest mortgage rates in years, despite the dip in those figures in the past two weeks. Higher rates, coupled with economic uncertainty, are raising questions about whether the US housing boom has met its limit with signs emerging that the once-intense pace of the market could be decelerating.

4. Inflation Eased Slightly in April — Consumer prices rose 6.3% in April from a year earlier, down from 6.6% in March, as measured by the Commerce Department’s personal-consumption expenditures price index, which it reported Friday. The March rise was the fastest since January 1982. April’s reading was the first time the measure eased since late 2020. The so-called core PCE index—which excludes volatile food and energy prices—increased 4.9% in April from a year ago, down from 5.2% in the year through March. On a monthly basis, core prices rose a seasonally adjusted 0.3%, the same as in February and March. That pace marked a moderate slowdown from the average monthly pace for the previous four months. Minutes from the Fed’s May 3-4 meeting, released Wednesday, show that officials discussed the possibility that they would raise interest rates to levels high enough to slow economic growth deliberately as the central bank races to combat high inflation.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 24th, 2022

“Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” — Warren Buffett

1. Pfizer’s Covid-19 Booster Cleared for 5- to 11-Year-Olds — the Food and Drug Administration reported that children between the ages of 5 and 11 years old can get a booster dose of BioNTech SE and Pfizer Inc.’s PFE, 1.32% COVID-19 vaccine. Children in this age group should wait at least five months after getting the primary series of shots. The regulator authorized a booster of the BioNTech/Pfizer vaccine for teens back in January. The FDA’s advisory committee did not meet to discuss whether the benefits of a third dose of the BioNTech/Pfizer vaccine outweigh the risks for this age group because the companies’ request for authorization in 5 to 11 year olds “did not raise questions that would benefit from additional discussion by committee members,” according to the regulator.

2. U.S. Retail Sales Grew 0.9% in April — Retail sales—a measure of spending at stores, online and in restaurants—rose a seasonally adjusted 0.9% last month compared with March, the Commerce Department said Tuesday. That marked the fourth straight month of higher retail spending. Consumers spent more at restaurants and bars and boosted expenditures on vehicles, furniture, clothing, and electronics. They cut spending sharply on gasoline in April as pump prices pulled back briefly from a run-up related to the war in Ukraine. In another sign of economic momentum, the Federal Reserve said industrial production, a measure of factory, mining and utility output, increased a seasonally adjusted 1.1% in April—also a fourth month of gains.

3. Treasury Likely to Prevent U.S. Investors From Receiving Russian Debt Payments — the U.S. has carved out an exemption, set to expire on May 25, in its sanctions campaign against Russia to allow for sovereign debt payments. Without it in place, banks and investors won’t be able to process and receive bond payments made by the Kremlin, likely prompting Russia’s first default on its foreign debts since 1918. Russia has managed to stay current on over $2.5 billion in foreign debt payments since the onset of the war with Ukraine, largely thanks to the sanctions carve-out, although the U.S. has steadily tightened Russia’s ability to make payments, including new sanctions in April that cut off the Kremlin’s access to U.S. bank accounts for sovereign debt payments.

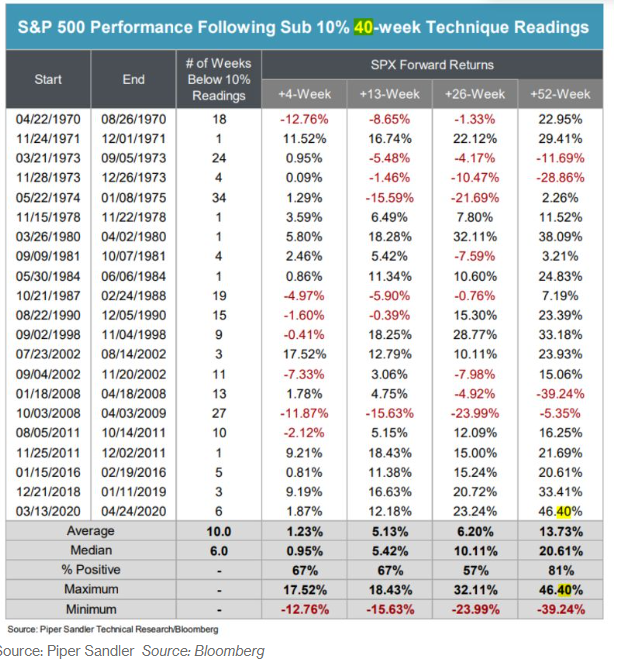

4. S&P 500 Pares Losses After Hitting Bear-Market Territory — the S&P 500 slid so far it was on track to close at least 20% below its January peak—what would have been considered a bear market. A comeback in the final hour of the trading day pushed the index higher. It has been decades since stocks have fallen for such a prolonged period. The Dow industrials notched their eighth straight weekly loss, their longest such streak since 1932, near the height of the Great Depression. The S&P 500 and Nasdaq had their seventh straight weekly loss, their longest such streak since 2001, after the dot-com bubble burst. All three indexes finished the week down at least 2.9%. Below is a chart of SPX performance following Sub 10% corrections.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 16th, 2022

“Only when the tide goes out do you discover who’s been swimming naked.” — Warren Buffett

1. Powell Reiterates Half-Point Hikes Are Likely in June and July — Federal Reserve Chair Jerome Powell reaffirmed that the central bank is likely to raise interest rates by a half percentage point at each of its next two meetings, while leaving open the possibility it could do more. Asked if he was taking a larger 75 basis-point increase off the table, he restated his comment from a May 4 press conference that the Fed wasn’t “actively considering” such a move, according to a transcript of the interview released by Marketplace.

2. US Producer Prices Rise More Than Forecast in Sign of Persistent Inflation — The producer price index for final demand increased 11% from April of last year and 0.5% from the prior month, driven by goods, Labor Department data showed Thursday. That followed sizable upward revisions to the March figures. Excluding the volatile food and energy components, the so-called core PPI increased 0.4% from a month earlier and was up 8.8% from a year ago. While that measure rose at a softer-than-expected monthly pace, March was revised up to a 1.2% advance. The data, while moderating somewhat from March, suggest persistent inflation in the production pipeline will continue to filter through to consumer prices, which also slowed from the prior month. Producers are likely to continue facing higher costs as Russia’s war in Ukraine and Covid-related lockdowns in China further strain supply chains, adding to the probability they’ll pass those expenses onto consumers.

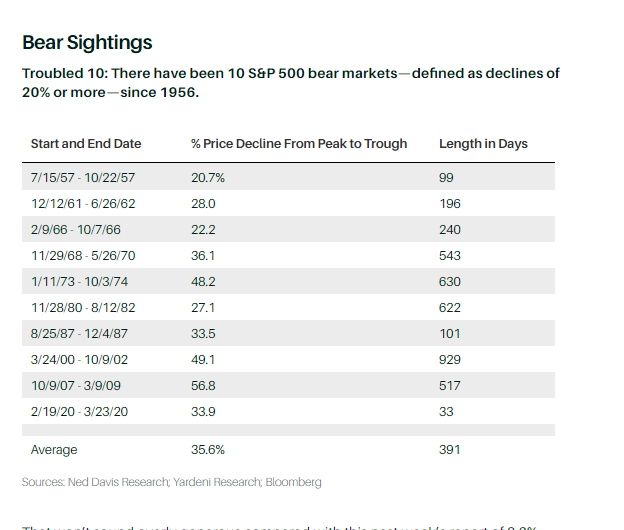

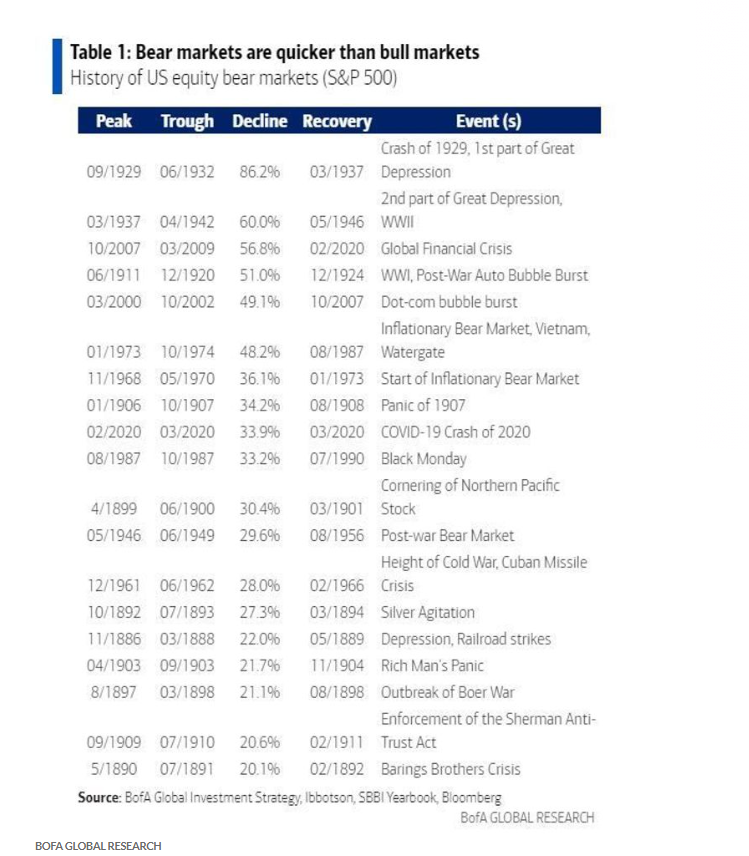

3. Bear Market Stats — according to Ned Davis Research, there have been 10 S&P 500 bear markets—defined as declines of 20% or more—since 1956, the average drop was 36.6% and last an average of 391 days. Below is the chart of the last 10-Bear Market going back to 1957.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 10th, 2022

“Seen through the lens of human perception, cycles are often viewed as less symmetrical than they are. Negative price fluctuations are called “volatility,” while positive price fluctuations are called “profit.” Collapsing markets are called “selling panics,” while surges receive more benign descriptions (but I think they may best be seen as “buying panics”; see tech stocks in 1999, for example). Commentators talk about “investor capitulation” at the bottom of market cycles, while I also see capitulation at the top, when previously prudent investors throw in the towel and buy.” ― Howard Marks

1. 10-Year Treasury Yield Hits 3% for First Time Since 2018 — the yield on the benchmark 10-year Treasury note, which rises when bond prices fall, surged at the start of U.S. trading and reached as high as 3.008% in the afternoon, as traders braced for the outcome of this week’s Federal Reserve meeting. Yields on Treasurys largely reflect investors’ expectations for short-term interest rates over the life of a bond. Rising yields are often associated with a strengthening economy because faster growth and a tighter labor market can lead central banks to crack down on inflation.

2. Fed Lifts Rates by Half Point in Biggest Hike Since 2000 — the Federal Reserve approved a rare half-percentage-point interest rate increase and announced plans to shrink its $9 trillion asset portfolio starting next month in a double-barreled effort to reduce inflation that is running at a four-decade high. The moves, announced after a two-day policy meeting Wednesday, will raise the central bank’s benchmark federal-funds rate to a target range between 0.75% and 1%.

Together, the steps mark the most aggressive Fed tightening of monetary policy at one meeting in decades, aimed at rapidly reducing the economic stimulus that has contributed to rising price pressures. The Fed, which usually lifts interest rates in quarter-percentage-point increments, last raised rates by a half point in 2000.

3. U.S. Mortgage Rates Jump to 5.37%, Highest Since 2009 — The average for a 30-year loan jumped to 5.27% from 5.10% last week, Freddie Mac said in a statement Thursday. The Federal Reserve yesterday raised its benchmark rate by a half point, the biggest bump since 2000, and signaled further hikes to come in its effort to cool inflation and the overheated housing market. Higher mortgage costs — already up more than 2 percentage points this year — may increasingly push out would-be homebuyers and ease competition for a scarce supply of listings. At the current 30-year average, a borrower with a $300,000 mortgage would pay $1,660 a month, $377 more than at the end of last year.

4. Bitcoin Slides Below $37,000 as Investors Unwind Risky Bets — apart from a brief selloff in January, bitcoin’s price hasn’t been this low since last July, when it traded as low as $29,000. The largest cryptocurrency is now down about 47% from its November record high of $68,991. On Wednesday, the central bank announced a half-point rate increase. Fed Chairman Jerome Powell said there may be half-point rate increases in the summer months, but that officials aren’t considering a three-fourths of a percentage point increase. The widespread unwinding of risk assets has hit the cryptocurrency market particularly hard, driving down everything from bitcoin to NFTs. It has also started to have an effect on companies in the industry. Crypto companies were surging early in the year, capped when several paid millions of dollars to run ads during the Super Bowl. But the momentum has faded sharply since then.

5. Past Bear Market Statistics — based on a BAC ‘s strategist Michael Harnett, Looking at a history of 19 bear markets over the past 140 years, they found the average price decline was 37.3% and the average duration about 289 days. While “past performance is no guide to future performance,” Hartnett and the team say the current bear market would end Oct. 19 of this year, with the S&P 500 at 3,000 and the Nasdaq Composite at 10,000. Check out their chart below:

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

May 2nd, 2022

“In investing, there is nothing that always works, since the environment is always changing, and investors’ efforts to respond to the environment cause it to change further ― Howard Marks

1. Russia to Cut Gas to Poland and Bulgaria, Making Energy a Weapon — Russia will cut off the gas to Poland and Bulgaria on Wednesday in a major escalation in the standoff between Moscow and Europe over energy supplies and the war in Ukraine. Moscow is making good on a threat to halt gas flows to countries that refuse President Vladimir Putin’s new demand to pay for the fuel in rubles. The European Union has rejected the move in principle but now payment deadlines are starting to fall due, governments across Europe need to decide whether to accept Putin’s terms or lose crucial supplies — and face the prospect of energy rationing.

2. Fidelity to Allow Retirement Savers to Put Bitcoin in 401(k) Accounts — employees won’t be able to start adding cryptocurrencies to their nest eggs right away, but later this year, the 23,000 companies that use Fidelity to administer their retirement plans will have the option to put bitcoin on the menu. The endorsement of the nation’s largest retirement-plan provider suggests crypto investing is moving further into the mainstream, but it remains to be seen whether employers will embrace it for their workers. Under the plan, Fidelity would let savers allocate as much as 20% of their nest eggs to bitcoin, though that threshold could be lowered by plan sponsors. Mr. Gray said it would be limited to bitcoin initially, but he expects other digital assets to be made available in the future.

3. U.S. GDP Drops 1.4% as Economy Shrinks for First Time Since Early in Pandemic — U.S. gross domestic product shrank at a 1.4% annual rate in the first quarter as supply disruptions weighed on the economy, though solid consumer and business spending suggest growth will resume. The decline in U.S. gross domestic product marked a sharp reversal from a 6.9% annual growth rate in the fourth quarter. The drop also marked the weakest quarter since spring 2020, when the Covid-19 pandemic and related shutdowns drove the U.S. economy into a deep—albeit short—recession. The drop in GDP stemmed from a widening trade deficit, with the U.S. importing far more than it exports. A slower pace of inventory investment by businesses in the first quarter—compared with a rapid buildup of inventories at the end of last year—also pushed growth lower. In addition, fading government stimulus spending related to the pandemic weighed on GDP.

4. Russia Makes Bond Payment In Dollars To Avoid Default — Russia said it had made payments on two dollar-denominated bonds, potentially staving off a default on the country’s foreign debt. The nearly $650 million in payments were made in dollars to a London branch of Citigroup Inc. that processes payments on behalf of bondholders, Russia’s finance ministry said Friday.

The money from Russia’s bond payments must land in bondholders’ accounts by Wednesday, the end of a 30-day grace period after Russia missed a payment in early April. Otherwise, the country can officially be called in default by its creditors.

5. Inflation Rises to Four-Decade High — Consumer prices rose 6.6% in March from a year before, up from February’s revised 6.3% increase, as measured by the Commerce Department’s personal-consumption expenditures price index. The March rise was the fastest since January 1982. The so-called core PCE index—which excludes volatile food and energy prices—increased 5.2% in March from a year earlier, down from a revised 5.3% in the year through February. On a monthly basis, core prices rose a seasonally adjusted 0.3% in March from the prior month, the same as the revised 0.3% increase in February. That was down from the 0.5% monthly pace in each of the prior four months—a mild slowdown that hinted broad price pressures might be starting to ease.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »