April 11th, 2023

‘Every morning in Africa, a gazelle wakes up; it knows it must run faster than the fastest lion or it will be killed.” — Leon Cooperman

1. U.S. Job Openings Dropped in February — the number of job openings fell in February, dropping below 10 million for the first time in nearly two years in a sign that employers’ demand for workers eased amid a still strong labor market. That fits the overall picture of a solid but slightly cooler labor market in February. Employers added 311,000 jobs—fewer than in January but a still robust gain—while the unemployment rate edged higher but remained low at 3.6%.

“We’re finally seeing companies cutting back their openings, which is the first step towards easing the tightness of the labor market,” said Lightcast Senior Economist Ron Hetrick. “This could be what a soft landing looks like in today’s economy.”

2. US Service Gauge Falls More Than Expected as Demand Moderates — The group’s index of new orders at service providers dropped more than 10 points to a three-month low of 52.2. While still consistent with expansion, the scale of the drop suggests a significant slowing in the pace of bookings growth. The business activity measure, which mirrors the ISM’s factory production index, slipped to 55.4. “There has been a pullback in the rate of growth for the services sector, attributed mainly to a cooling off in the new orders growth rate, an employment environment that varies by industry and continued improvements in capacity and logistics,” Anthony Nieves, chair of the ISM Services Business Survey Committee, said in a statement.

3. Fed’s Emergency Loans to Banks Fall, But Remain High — Banks once again reduced their borrowings from two Federal Reserve backstop lending facilities in the most recent week, a sign the financial stresses that emerged following a string of bank collapses last month may be stabilizing. Emergency borrowing retreated for the third straight week, suggesting liquidity demand continues to ease following the second-largest bank failure in US history. Over the past few weeks, banks appear to have shifted a larger share of their borrowing out of the discount window, the Fed’s traditional backstop lending program, and into the new emergency lending facility it launched last month to help stem contagion in the bank sector.

4. March Jobs Report Shows Hiring Gradually Cooling — Employers added 236,000 workers last month, a historically strong gain but the smallest in more than two years, the Labor Department reported. The unemployment rate ticked down to 3.5%. More Americans jumped into the labor market in March, helping take pressure off wage increases. Average hourly earnings rose 4.2% last month from a year earlier, the smallest annual gain since mid-2021 when inflation was surging.

Steady hiring growth last month could keep the Federal Reserve on track to consider raising interest rates again at its meeting in early May. But slower wage gains could also allow officials to hint at a pause after that. Fed officials have signaled they will pay close attention to other measures of economic activity including bank lending conditions as they debate their next move.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

April 4th, 2023

Sir John Templeton: “Bull markets are born on despair, grow on skepticism, mature on optimism and die on euphoria.”

1. Consumer Spending Growth Moderated in February and Core Inflation Eased — Consumer spending increased a seasonally adjusted 0.2% in February, from January’s revised 2% increase, which was the largest one-month gain in nearly two years, the Commerce Department said Friday. When adjusted for rising prices, spending fell 0.1% in February from the prior month, after rising a revised 1.5% in January.

The core personal-consumption expenditures price index—one of the Fed’s preferred gauges of inflation—climbed 4.6% in February from a year earlier, down from 4.7% the prior month. Many economists see the core measure, which omits volatile food and energy prices, as a better predictor of future inflation.

2. White House Calls for Tougher Midsize Bank Rules — The recommendations call for new rules from the Federal Reserve and other banking regulators that would apply to banks with $100 billion to $250 billion in assets. There were approximately 20 firms in that asset range as of the end of 2022, according to the Federal Financial Institutions Examination Council.

The Fed is already rethinking a number of its rules related to those banks after Silicon Valley Bank and Signature Bank failed. Changes could include tougher capital and liquidity requirements, as well as steps to strengthen stress tests that assess banks’ ability to weather a hypothetical severe downturn.

3. New EV Rules Mean Fewer Models Eligible for Tax Credit — The new rules, issued by the Treasury Department Friday, aim to make the U.S. less reliant on batteries and critical minerals shipped from China. For car buyers to claim the full $7,500 tax credit, the batteries must contain set amounts of components made in North America and critical minerals sourced in the U.S. or from certain friendly countries.

The criteria will take effect on April 18, when a list of models that qualify for the tax credit will be issued. Until then, consumers can claim the full tax credit when they buy vehicles that are currently eligible, before some are expected to drop off the list.

4. Nasdaq turns in best performance since 2020 — The S&P 500 rose 7% in the first quarter, while the Dow Jones Industrial Average added 0.4%. The Nasdaq Composite soared. The technology-heavy index jumped 17%, outperforming the Dow industrials by the widest margin since 2001. Overall, it was Nasdaq’s best quarter since the second quarter of 2020. Recent projections show Fed officials expect the federal-funds rate to rise to at least 5.1% from its current range of 4.75% to 5%. That suggests the Fed could push through one more quarter-point interest-rate increase and then hold rates at that level for the remainder of the year.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

March 27th, 2023

“The stock market is never obvious. It is designed to fool most of the people, most of the time”- Jesse Livermore —

1. Yellen Says US Will Intervene If Needed to Protect Smaller Banks — Treasury Secretary Janet Yellen said on last week the US government could repeat the drastic actions it took recently to protect bank depositors if smaller lenders are threatened. US authorities took extraordinary steps earlier this month to bolster that confidence following the collapses of Silicon Valley Bank and Signature Bank. Regulators guaranteed insured and uninsured deposits at the two institutions. The Federal Reserve also launched a new backstop for lenders and altered rules at its emergency lending facility — the so-called discount window — to help them meet deposit withdrawals.

2. Rent Inflation for US Single-Family Homes Drops Near Two-Year Low — rent increases for US single-family homes eased for a ninth straight month in January, pushing the annual rate to the lowest since the spring of 2021, according to CoreLogic. Nationwide, the typical rent for a single-family home rose 5.7% from a year earlier, data from the real estate analytics provider show. All 20 major metro areas tracked by CoreLogic posted single-digit annual rent increases, for the first time since late 2020.

3. Fed Raises Rates but Nods to Greater Uncertainty After Banking Stress — the Federal Reserve approved another quarter-percentage-point interest-rate increase but signaled that banking-system turmoil might end its rate-rise campaign sooner than seemed likely two weeks ago.

The decision Wednesday marked the Fed’s ninth consecutive rate increase aimed at battling inflation over the past year. It will bring its benchmark federal-funds rate to a range between 4.75% and 5%, the highest level since September 2007. The policy statement said it was too soon to tell how much recent banking stress would slow the economy. “The U.S. banking system is sound and resilient,” the statement said. “Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain.”

4. Deutsche Bank Stock Tumbles on Contagion Fears — Investors sparked a selloff in Deutsche Bank AG DB -4.20%decrease; red down pointing triangle and thrust one of Europe’s most important lenders into the center of concerns about the health of the global financial system. The concern over Deutsche Bank emerged days after Credit Suisse Group AG was forced into a takeover by its larger and more stable rival UBS Group AG. Since the collapse of Silicon Valley Bank in the U.S. earlier this month, investors have scoured the globe for institutions perceived as vulnerable. Deutsche Bank sits at the heart of the German economy. Despite years of retrenchment to make the bank smaller and safer, it remains a globally vital bank, with a major footprint on Wall Street trading bonds, derivatives and currencies. It serves multinational companies with bread-and-butter basics of lending, managing money and corporate accounts.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

March 20th, 2023

“Markets can remain irrational longer than you can remain solvent” — John Maynard Keynes

1. Biggest U.S. Banks Race to Rescue First Republic — Eleven banks have deposited $30 billion in First Republic Bank, according to a joint statement from the heads of the Treasury, Federal Reserve, Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency. JPMorgan Chase & Co., Citigroup Inc., Bank of America Corp.; gand Wells Fargo WFC ; are each making a $5 billion uninsured deposit into First Republic, the banks said in a statement Morgan Stanley and Goldman Sachs Group Inc. are kicking in $2.5 billion apiece, while five other banks are contributing $1 billion each.

2. ECB Delivers Half-Point Hike But Offers Little on Next Move — the European Central Bank went ahead with a planned half-point increase in interest rates but offered few clues on what may follow amid market turmoil that roiled Credit Suisse Group AG. The deposit rate was lifted to 3% on Thursday — as officials have been flagging since their last meeting six weeks ago and as the majority of economists anticipated, but dropped language from its statement indicating where borrowing costs are headed.

3. SVB Financial Files for Chapter 11 Bankruptcy Protection — SVB Financial Group filed for chapter 11 protection on Friday in New York bankruptcy court, the largest bankruptcy filing stemming from a bank failure since Washington Mutual Inc. in 2008. Silicon Valley Bank, the technology-focused lender and SVB Financial’s primary business, was taken over by federal regulators after it was crippled by a dash for the exits by depositors. The Federal Reserve stepped in to make depositors whole and reassure markets, although a number of other regional banks in the U.S. have seen their credit ratings cut and depositors pull cash.

4. Microsoft Adds the Tech Behind ChatGPT to Its Business Software — Microsoft Corp. MSFT 1.17%increase; green up pointing triangle is infusing its popular workplace software with the technology behind the viral chatbot ChatGPT, upgrading PowerPoint, Word, Excel and Outlook with new abilities in its latest move to try to stay ahead in the artificial-intelligence race. The software giant has gone all-in on generative AI, following its multibillion-dollar investment in ChatGPT’s creator OpenAI. In February, Microsoft rolled out a new version of its search engine Bing that used generative AI to give direct answers to questions and had a sophisticated chat tool. It announced Thursday that it is bringing the technology to its Microsoft 365 suite of software to enable users to create presentations, write documents and summarize emails—all from natural-language prompts.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

March 16th, 2023

There will not be any re-cap for the week of March 10th, 2023. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

Posted in Weekly Summary | No Comments »

March 6th, 2023

…“People somehow think you must buy at the bottom and sell at the top to be successful in the market. That’s nonsense! The idea is to buy when the probability is greatest that the market is going to advance”… Jesse Livermore

1. Home-Price Growth Slowed in 2022 — home-price growth decelerated in 2022 after a rapid rise in mortgage rates priced many buyers out of the market.

The S&P CoreLogic Case-Shiller National Home Price Index, which measures home prices across the nation, rose 5.8% in the year ended in December, down from a 7.6% annual rate the prior month. The increase was the lowest December-to-December change since 2019. On a monthly basis, the index fell 0.8% in December compared with November, the sixth straight month-over-month decline. Existing-home sales dropped 17.8% in 2022 to the lowest level since 2014, as the surge in mortgage rates brought the pandemic-driven housing boom to an abrupt halt.

2. Long-Robust U.S. Labor Market Shows Signs of Cooling — demand for U.S. workers shows signs of slowing, a long-anticipated development that is appearing in private-sector job postings even while government reports indicate the labor market is running hot. Figures from ZipRecruiter Inc. and Recruit Holdings Co., two large online recruiting companies, show the number of job postings on their sites declined more late last year than the Labor Department report on job openings for that period indicated. The companies report available jobs fell further this year, potentially foretelling a decrease in openings in coming Labor Department reports, and a slowdown in hiring this year.

3. 10-Year Treasury Yield Tops 4% for First Time Since November — lingering inflation and fears of higher interest rates lifted the 10-year Treasury yield above 4% on Wednesday, marking a fresh acceleration for a historic bond-market rout.

The climb carried the key measure of borrowing costs back toward the decade-plus highs reached last year. Spurring the most recent leg: a run of strong economic data that dashed hopes inflation will rapidly slow to near the Federal Reserve’s 2% target. Yields topped 4% Wednesday morning after a slightly stronger-than-expected survey of manufacturing activity. Rising yields lift borrowing costs for consumers and companies, and hurt the prices of other investments by offering steady payouts with lower risk. The climb in yields has buffeted major stock indexes, with the S&P 500 losing around 2.6% in February.

4. Fed Official Says Hotter Data Will Warrant Higher Rates — the Federal Reserve will need to raise rates to higher levels than previously anticipated to prevent inflation from picking up if the recent strength in hiring and consumer spending continues, a central bank official said Thursday. Mr. Waller didn’t say in his prepared remarks whether he would continue to favor raising interest rates by a quarter-percentage point, which was his preference at the Fed’s last meeting, or whether he would instead support a larger half-point increase at its next gathering, March 21-22. The Fed’s rate-setting committee voted unanimously last month to slow rate increases by lifting their benchmark federal-funds rate by a quarter percentage point—to a range between 4.5% and 4.75%—following larger moves of a half point in December and 0.75 point in November.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

February 27th, 2023

“Stock market doesn’t only teaches to make money but it also teaches lot about life, patience, persistence and wisdom.” ― Raj Mishra

1. U.S. Home Sales Fall for 12th Straight Month — Sales of previously owned homes, which make up most of the housing market, fell 0.7% in January from the prior month to a seasonally adjusted annual rate of 4 million, the slowest since October 2010, the National Association of Realtors said Tuesday. January sales fell 36.9% from a year earlier.

January’s decline marked the longest streak of back-to-back monthly declines on record in figures going back to 1999, NAR said. Surprisingly strong inflation, jobs and retail spending figures in recent weeks have fueled expectations that the Federal Reserve could raise interest rates more than investors anticipated. The Fed has aggressively raised its benchmark federal-funds rate to cool the economy and bring down high inflation, hitting the rate-sensitive housing market particularly hard.

2. Fed Minutes Show Most Officials Favored Quarter-Point Rate Rise — Officials at their meeting earlier this month agreed to slow rate increases by lifting their benchmark federal-funds rate by a quarter-percentage point, following larger moves of a half point in December and 0.75 point in November. Minutes from that meeting, showed most thought a slower pace provided the best way to manage the risks of raising rates too much or too little. But the minutes also revealed some officials were concerned about stopping or slowing their inflation-fighting campaign too soon. The latest increase brought the fed-funds rate to a range between 4.5% and 4.75%, extending the fastest series of rate rises since the early 1980s. While the quarter-point rate rise was backed unanimously by the rate-setting committee, the minutes said a few officials favored or would have also agreed to support a half-point increase.

3. Economy Showing Strength in Early 2023 After Last Quarter’s GDP Gain Revised Modestly Lower — gross domestic product, a broad measure of the goods and services produced across the U.S., rose at a 2.7% annual rate in the fourth quarter, adjusted for seasonality and inflation, the Commerce Department said Thursday. That was down from a previous estimate of 2.9% growth, and slower than the third quarter’s 3.2% growth. Entering this year, forecasters had projected the economy to cool, but recent data shows a strong labor market and improved spending. Worker claims for unemployment benefits, a proxy for layoffs, ticked down last week, the Labor Department said Thursday. Hiring accelerated last month and the unemployment rate fell to a 53-year low. Retail sales jumped 3% in January, reversing two consecutive months of decline, a separate Commerce Department report showed. Business activity, particularly in the services sector, picked up in February, according to surveys of manufacturers and service providers released last week.

Posted in Weekly Summary | No Comments »

February 20th, 2023

1. US Inflation Stays Elevated, Adding Pressure for More Fed Hikes — US consumer prices rose briskly at the start of the year, a sign of persistent inflationary pressures that could push the Federal Reserve to raise interest rates even higher than previously expected.

The overall consumer price index climbed 0.5% in January, the most in three months and bolstered by energy and shelter costs, according to data out Tuesday from the Bureau of Labor Statistics. The measure was up 6.4% from a year earlier. Excluding food and energy, the so-called core CPI advanced 0.4% last month and was up 5.6% from a year earlier. Economists see the gauge as a better indicator of underlying inflation than the headline measure.

2. U.S. Retail Sales Rebounded Sharply in January — U.S. retail sales jumped 3% in January as consumers broadly boosted spending on vehicles, furniture, clothing and dining out, adding to signs that economic growth picked up at the start of the year. The unexpectedly strong January employment report and still solid wage gains bode well for consumer spending, and some economists think economic growth could be picking up. The Federal Reserve has raised interest rates aggressively since last March in an attempt to slow the economy and bring down inflation. The consumer-price index climbed 6.4% in January from a year earlier, down slightly from 6.5% in December but still well above the Federal Reserve’s 2% inflation target. Retail sales grew broadly across the economy in January, including at restaurants, car dealerships, department stores and furniture and appliance sellers.

3. January PPI Report Shows Producer Prices Rose — U.S. supplier prices rose 6% in January from a year earlier, a sign of still stubborn inflation pressures in the economy.

That increase in the producer-price index, which generally reflects supply conditions in the economy, was slower than December’s 6.5% gain, the Labor Department said Thursday. And it was down markedly from the 11.7% rise in March 2022, the recent peak. The PPI increased 0.7% in January from the prior month, compared with a revised 0.2% drop in December, and significantly faster than the 0.2% average monthly rise in the year before the pandemic. Fed officials in recent public appearances have steeled themselves for a long inflation fight. Earlier this month policy makers raised their benchmark federal-funds rate by 0.25 percentage point, bringing it to a range between 4.5% and 4.75%, the highest level since 2007. Officials are on track to raise interest rates at their meeting in March and to signal further increases will be likely.

4. Two Fed Officials Would Have Supported Larger Rate Increase This Month — two Federal Reserve officials said they would have supported raising interest rates by a half percentage point at the central bank’s meeting earlier this month given the strength of economic demand and inflation. Ms. Mester said it was too early to specify the size of the rate increase that would be appropriate at the Fed’s next meeting, on March 21-22. But she said that the central bank wasn’t locked in to raising rates by a quarter point at coming policy meetings. “It’s not always going to be, you know, 25 [basis points],” she said during a question-and-answer session at a conference in Sarasota, Fla. “As we showed, when the economy calls for it, we can move faster. And we can do bigger [increases] at any particular meeting. St. Louis Fed President James Bullard also said Thursday he would have favored a half-point rate increase at the last meeting and that he would support moving as quickly as possible to raise rates to just below 5.5%.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

February 14th, 2023

There will not be any re-cap for the week of February 10th, 2023. We are away for some needed R&R.

Have a good week.

The staffs at EGS.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »

February 6th, 2023

“Don’t look for the needle in the haystack. Just buy the haystack.” — John Bogle,

1. Worker Pay Gains Cooled Modestly Late Last Year as Fed Weighs Inflation — employers spent 1% more on wages and benefits last quarter versus the prior three months, a slowdown from a 1.2% increase in the third quarter, the Labor Department said Tuesday. From a year earlier the employment-cost index advanced 5.1%, in line with the 5% annual gain in the third quarter. The compensation report confirms other recent signs that wage growth has slowed, and comes as Fed officials start a two-day policy meeting. They are likely on Wednesday to approve raising their benchmark federal-funds rate by a quarter percentage point, down from their half-point increase in December, which followed four straight increases of 0.75 point.

2. Fed Approves Quarter-Point Rate Hike, Signals More Increases Likely — the Federal Reserve approved an interest-rate increase of a quarter-percentage-point and signaled plans to raise rates again next month to continue lowering inflation. The decision Wednesday followed six consecutive rate rises that were larger, including an increase of a half-point in December and a 0.75-point increase in November. The latest increase caps a year in which the Fed lifted its benchmark federal-funds rate from near zero to a range between 4.5% and 4.75%, a level last reached in 2007. That extends the central bank’s most rapid pace of rate increases since the early 1980s to fight inflation, which hit a 40-year high last year.

3. ECB Hikes by Half-Point and Signals Same Again in March — the European Central Bank lifted interest rates by a half-point, with President Christine Lagarde saying another such move is almost certain next month, despite conceding that the inflation outlook is improving.

Policymakers, as expected, raised the deposit rate to 2.5%, the highest since 2008. Lagarde warned that the most aggressive bout of monetary tightening in ECB history isn’t done — even as energy prices plunge and the Federal Reserve moderates the pace of its own hikes.

4. Unemployment Falls to 3.4%, Lowest in 53 Years, Jobs Report Shows — the U.S. labor market accelerated at the start of the year as broad-based hiring added a robust 517,000 jobs and pushed the unemployment rate to a 53-year low. January’s payroll gains were the largest since July 2022 and snapped a string of five straight months of slowing employment growth, the Labor Department said Friday. The unemployment rate was 3.4% last month, its lowest level since May 1969. Wage growth continued to soften last month, despite the strong job gains. Average hourly earnings grew 4.4% in January from a year earlier, down from a revised 4.8% in December. Annual revisions to employment and pay data suggest that wage growth has been cooling—but at a slower pace than previously thought.

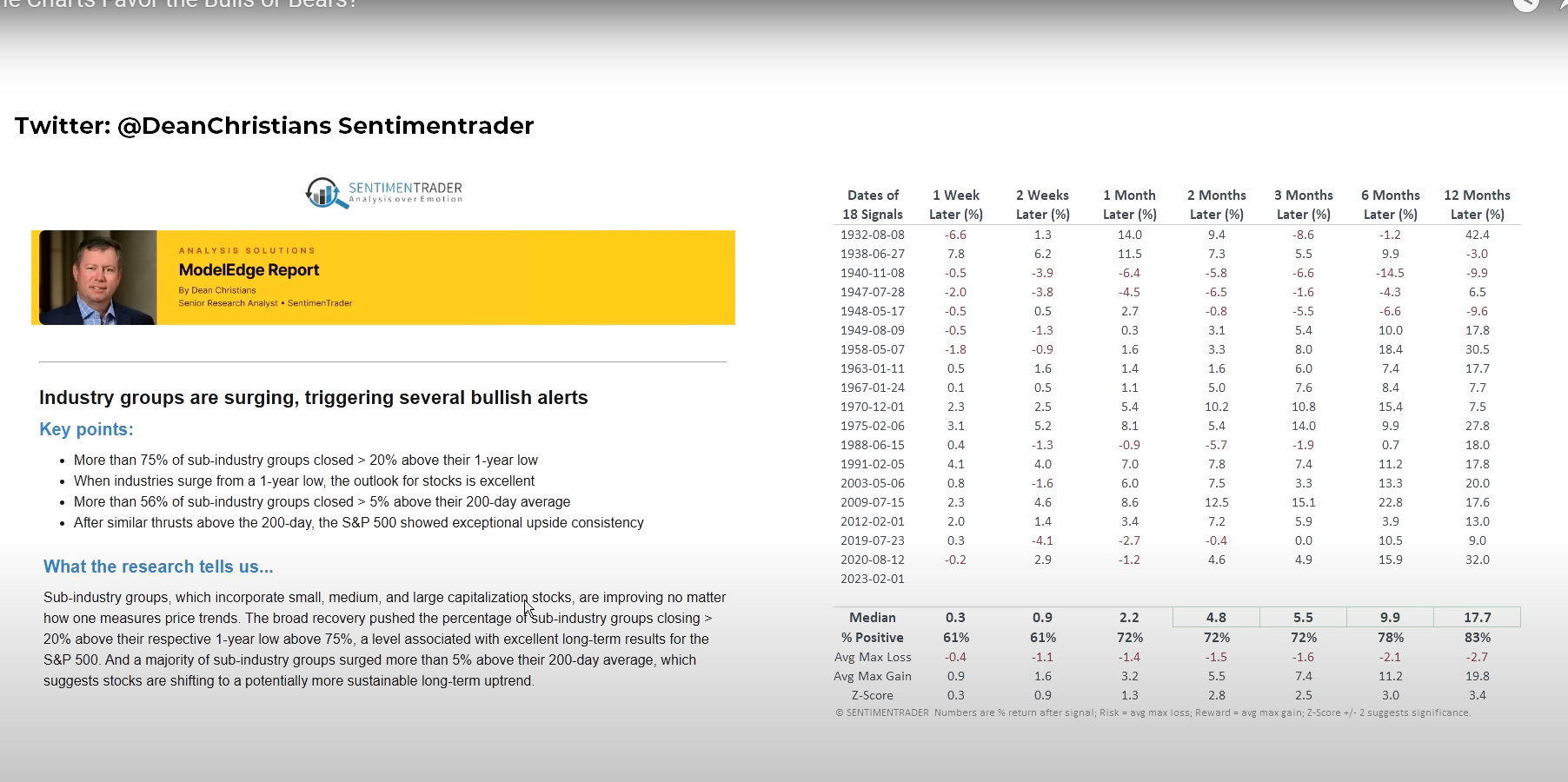

5. Industry Group Surged – Shows Bullish Patterns — courtesy of Sentiment Trader, several industry groups surges — see below chart for more details.

The week ahead — Economic data from Econoday.com:

Posted in Weekly Summary | No Comments »