“The game of speculation is the most uniformly fascinating game in the world. But it is not a game for the stupid, the mentally lazy, the person of inferior emotional balance, or the get-rich-quick adventurer. They will die poor.” – Jesse Livermore

1. Turkey Retaliated With Tariffs on U.S. Cars, Alcohol, Tobacco — a reeling Turkey has responded to U.S. tariffs with retaliatory duties on U.S. passenger cars, alcohol, tobacco, cosmetics and other products. Tariffs on cars are set to rise by 120% and those on made-in-the-U.S. alcoholic drinks by 140%, alongside a 60% increase on tobacco products. The move comes amid increasing fears of contagion from Turkey’s collapse.

2. China, U.S. to Resume Trade Talks This Month — China will send a delegation to the United States later in August to resume trade talks that largely broke down a couple of months ago. Vice Commerce Minister Wang Shouwen will discuss economic and trade issues with U.S. counterpart David Malpass in a new attempt at defusing a trade war that has resulted in billions of dollars in tariffs so far, with threats of more. Formal talks between the U.S. and China broke down last month and led to dueling tariffs.

3. Amazon Eyes Online U.K. Healthcare Market — Major insurance firms in Europe have been invited by Amazon (NASDAQ:AMZN) to participate in a U.K. price comparison website. While there are no firm details on a launch by Amazon into financial services in the region, online insurance comparison players such as AXA (OTCQX:AXAHF), Hastings (OTC:HNGGF), Esure (OTC:ESXRY) and GoCompare are on watch.

4. Federal Probe Focuses On Apartment Mortgage Fraud — WSJ reported the investigation, still in its early stages, has so far resulted in a fraud-conspiracy indictment against four real-estate executives in upstate New York for falsifying information that helped them secure loans multi-family properties. The indictments made fraud-conspiracy charges against Todd Morgan and Kevin Morgan, a son and nephew of Robert Morgan, and charged their mortgage brokers, Frank Giacobbe and Patrick Ogiony of Aurora Capital Advisors. One owner of properties investigators reviewed is Robert C. Morgan, who ran a firm called Morgan Management LLC, but changed its name in June to Grand Atlas Property Management.

5. Q2 Latest Hedge Fund 13F — Hedge funds have finished up reporting on the investments they held at the end of Q2. New portfolio additions such as Keurig Dr Pepper (NYSE:KDP) by Citadel, Groupon (NASDAQ:GRPN) by Engaged Capital and GrubHub (NYSE:GRUB) by Jana Partners. Perhaps not a surprise, Alibaba (NYSE:BABA) was one of the names that cropped up the most times in the portfolio updates. Facebook (NASDAQ:FB) was added by at least six funds in Q2 as a new addition, while ten funds dropped the tech stock or trimmed exposure. In addition, Berkshire boosts stakes in Apple, US Bank, Teva, BNY Mellon, Delta in Q2 — in the latest 13F from Berkshire Hathaway (BRK.A, BRK.B) showed its stake in Apple (AAPL) as boosted to about 252M shares as of June 30 – up roughly 5% from three months earlier. The Oracle and company also added to holdings in U.S. Bancorp (NYSE:USB), Teva Pharmaceuticals (NYSE:TEVA), Bank of New York Mellon (NYSE:BK), General Motors (NYSE:GM), and Goldman Sachs (NYSE:GS). Among those showing trimmed stakes were American Airlines (NASDAQ:AAL), Phillips 66 (NYSE:PSX), Charter Communications (NASDAQ:CHTR), and Wells Fargo (NYSE:WFC).

6. U.S. Seen Near Deal with Mexico On Revised NAFTA But Canada Remains Apart — the U.S. is close to reaching a deal with Mexico on a revamped North American Free Trade Agreement, but thorny issues are yet to be resolved with Canada, according to reports. Both Mexico and the U.S. are seen as having strong incentives to push through a deal quickly: Mexico wants to lock in an agreement before its new leftist president takes office, and the Trump administration wants a win on trade ahead of the midterm elections. U.S. negotiators this week have been meeting with senior Mexican officials in Washington, and the two sides are said to have largely agreed to new rules on auto trade – a top White House priority – that could boost investment in the U.S. President Trump says he is “in no hurry” to complete a NAFTA deal, remarks seen mostly as an attempt to put pressure on Canada.

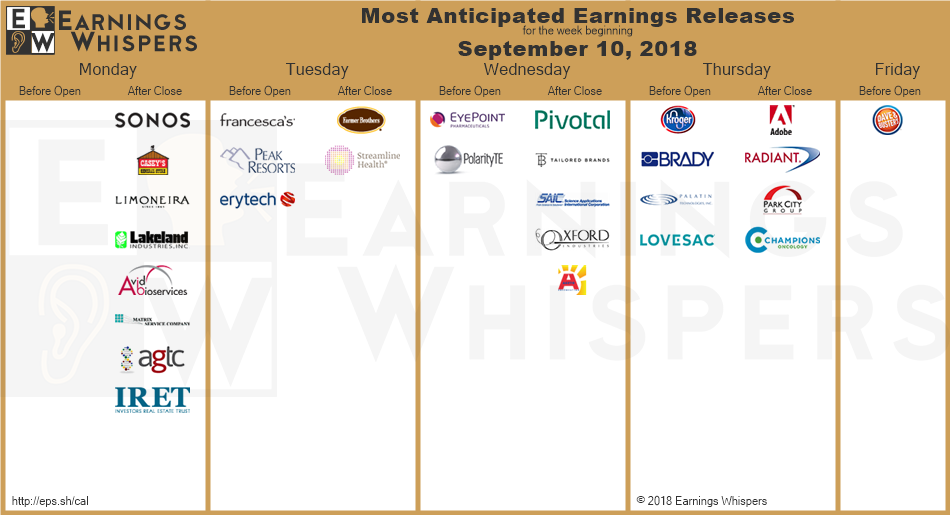

The week ahead — Economic data from Econoday.com: