Week of Apr 5 2019 Weekly Recap & The Week Ahead

Monday, April 8th, 20191. Boeing Admits MCAS Played Role in 737 Max Crashes — “With the release of the preliminary report of the Ethiopian Airlines flight 302 accident investigation it’s apparent that in both flights the Maneuvering Characteristics Augmentation System, known as MCAS, activated in response to erroneous angle of attack information,” Boeing (NYSE:BA) CEO Dennis Muilenburg said in a statement. However, an update will “add additional layers of protection and will prevent erroneous data from causing MCAS activation. Flight crews will always have the ability to override MCAS and manually control the airplane.”

2. Tesla Deliveries Tumble 31% — the EV maker reported a 31% drop in Q1 deliveries to 63K vehicles (51K Model 3 and 12K Model S and X). While sales were hit by a reduction in U.S. federal tax credits and by difficulties in delivering to Europe and China, Tesla said it finished the quarter with “sufficient” cash. The automaker also reaffirmed its full-year forecast of 360K to 400K deliveries, but investors are asking if that big increase will be possible.

3. 5G Era for Smartphones Has Begun — Verizon (NYSE:VZ) has launched 5G wireless service in parts of Chicago and Minneapolis, while carriers in South Korea – SK Telecom (NYSE:SKM) and KT Corp. (NYSE:KT) – deployed their service in the Seoul metropolitan area. To access the network, Verizon subscribers for now will be limited to the Motorola Z3 (with an accessory clip-on), while Korean early adopters will have to use Samsung’s Galaxy S10. 4G helped reshape the way people hail taxis and order takeout and the mobile industry is hoping the faster speeds provided by 5G will enable self-driving cars, smart cities and will birth immersive digital worlds.

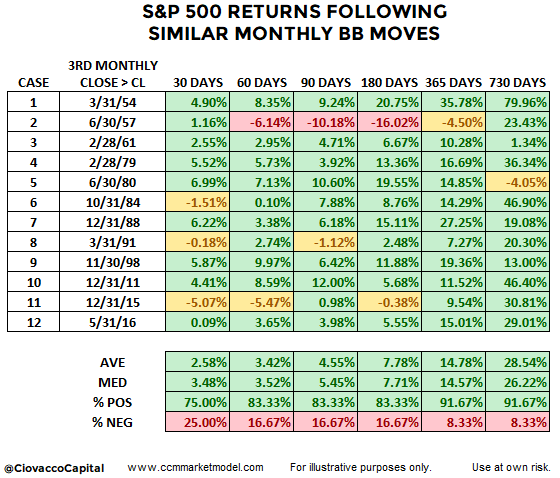

4. Third Consecutive Monthly Close Statistics — the S&P 500 (SPY) closed above the monthly Bollinger Band centerline at the end of January, it aligned the present day with favorable historical probabilities and also provided some distance from setups in the 1974, 2001, and 2008 bear markets. Twelve of the 13 similar historical cases, covered on Feb. 20, also went on to print three consecutive closes above the monthly Bollinger Band centerline. The exception was the 6/30/1960 case, which gave up the centerline in the second month. The table below shows S&P 500 (VOO) performance in the remaining 12 historical cases following the third consecutive close above the monthly Bollinger Band centerline (similar to what occurred at the end of March 2019).

The week ahead — Economic data from Econoday.com: