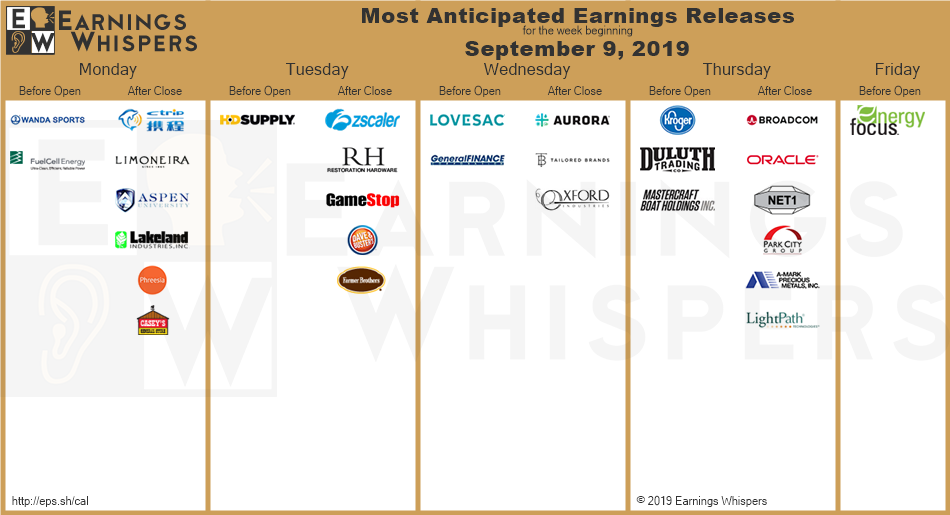

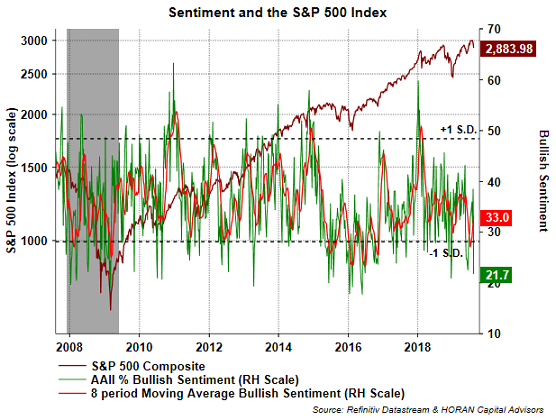

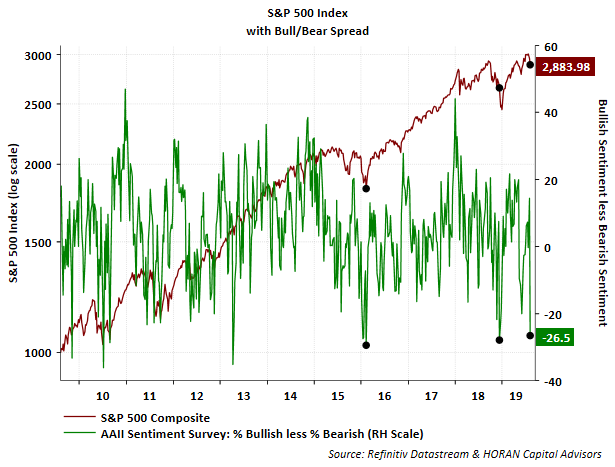

Week of Sept 7 2019 Weekly Recap & The Week Ahead

Monday, September 9th, 2019“One of the funny things about the stock market is that every time one person buys, another sells, and both think they are astute” – William Feather

1. Trade War Between the U.S. and China Rippling Effect — new U.S. tariffs on clothing and other imports from China that went into effect Sunday are expected to hit consumers. President Trump has since told U.S. companies to look for alternatives to China. A round of retaliatory Chinese tariffs has now also taken effect, targeting imports of U.S. soybeans, crude oil and pharmaceuticals. It is crimping growth in Asian industrial giants such as Japan and South Korea and hitting factories as far from the front line as Germany. Global industrial production fell in the three months through June, as did trade flows, and a series of surveys of manufacturing companies in Asia and Europe suggests a rebound is unlikely over the coming months.

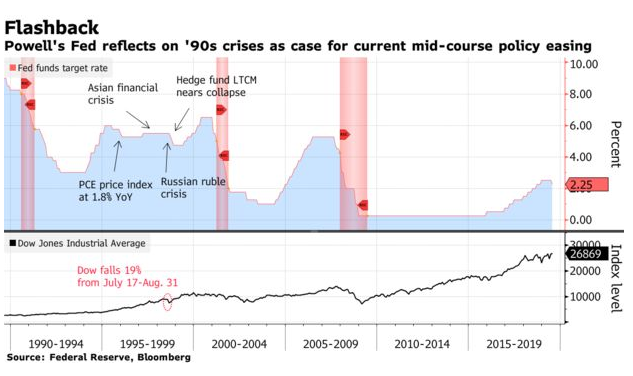

2. U.S., China Agree to Renew Trade Talks — China’s Ministry of Commerce says leaders of the U.S. and Chinese trade talks held a phone call and agreed to meet early next month in Washington, D.C., for another round of negotiations. Deputy-level officials will work together in mid-September to lay the groundwork for the meeting. On a related note, the markets already expect the Fed to cut interest rates modestly at the Sept. 17-18 policy meeting. Investors place a 90% probability on a quarter-percentage-point rate cut and a 10% probability on a larger, half-point cut, according to CME Group.

3. Apple Returns to Bond Market— taking advantage of the steep decline in benchmark interest rates, Apple (NASDAQ:AAPL) is joining U.S. companies including Deere (NYSE:DE) and Disney (NYSE:DIS) by launching its first bond deal since 2017 and selling $7B of debt. All three companies issued 30-year bonds with yields below 3%, a first for the corporate debt market. Bonds issued by big-name corporations give investors a relatively safe alternative that still pays more than government bonds.

4. Argentina Imposes Currency Controls — The spiraling economic crisis in Argentina has prompted the central bank to slap capital controls on businesses as the peso lost more than a quarter of its value since primary elections last month. Exporters will face limits of five days to repatriate foreign currency, while institutions will need authorization of the bank to buy dollars in the forex market, except in the case of foreign trade. The decision reverses one of the first big achievements of President Macri who removed strict capital controls after taking power in December 2015 (the restrictions had prompted the MSCI index to strip Argentina of its status as an emerging market, demoting it to a frontier market).

The week ahead — Economic data from Econoday.com: