Week of Nov 15 2019 Weekly Recap & The Week Ahead

Monday, November 18th, 2019“When you learn to let go of the need to be right, being wrong gradually lose its power to disturb you.” Yvan Byeajee

1. Auto industry Seeks partnerships — Tata Group (NYSE:TTM), the owner of Jaguar Land Rover, has approached carmakers including China’s Geely (OTCPK:GELYY), the owner of Volvo Cars, and BMW (OTCPK:BMWYY) as it seeks partnerships to share the cost of a new generation of vehicles, Bloomberg reports. Scale has become increasingly critical in the auto industry as carmakers pool resources to tackle electrification and self-driving capabilities. Volkswagen (OTCPK:VWAGY) this year decided to team up with Ford (NYSE:F), while PSA Group (OTCPK:PEUGF) last month agreed to merge with Fiat Chrysler (NYSE:FCAU) to create the world’s fourth-largest automaker.

2. Boeing Announces MAX Deliveries Could Resume in December — the planemaker said deliveries of the 737 MAX could begin in December. The company has completed a test of flight control software with the FAA in a simulator, though regulators still must sign off on new pilot training and Boeing needs to conduct a certification flight with officials. Airlines have said they will need at least a month to complete training and install revised software before flights can resume.

3. Disney+ Finally Arrives in Streaming Wars — Disney+ has gone live, challenging the likes of Netflix (NASDAQ:NFLX), Apple TV Plus (NASDAQ:AAPL) and HBO Max (NYSE:T) with a low price of $6.99/month (or $69.99/year). It’ll also offer a triple bundle – including Hulu and ESPN Plus – for $12.99/month. Waves were already made after the Mouse House gave Verizon (NYSE:VZ) customers a free year of the service, as well as broadening device support to nearly every platform: Apple OS, Android, Fire TV, Roku, etc. Disney (NYSE:DIS) has called the service – which will be the exclusive home of Star Wars, Marvel and Pixar – the future of the company, and is building out a slate of original shows and movies based on those brands like The Mandalorian.

4. Goldman Faces ‘Sexist’ Probe Over Apple Card — New York’s Department of Financial Services has initiated a probe into the credit card practices of Goldman Sachs (NYSE:GS) following a series of tweets from David Heinemeier Hansson, the creator of Ruby on Rails. He slammed the Apple Card (NASDAQ:AAPL) for giving him 20x the credit limit than his wife – despite filing joint tax returns and his wife having a better credit score – and alleged that gender discrimination was present in algorithms that determined credit limits. Launched in August, the Apple Card is a joint venture between Apple and Goldman, which is responsible for all credit decisions related to the card.

5. U.S. to extend reprieve for Huawei — as the earlier reprieve expires, the Trump administration will issue another 90-day extension today of a license allowing U.S. companies to continue doing business with Huawei, sources told Reuters. The Chinese firm was added to an economic blacklist back in May on national security grounds. Out of $70B that Huawei spent buying components in 2018, some $11B went to U.S. firms including Qualcomm (NASDAQ:QCOM), Intel (NASDAQ:INTC) and Micron Technology (NASDAQ:MU).

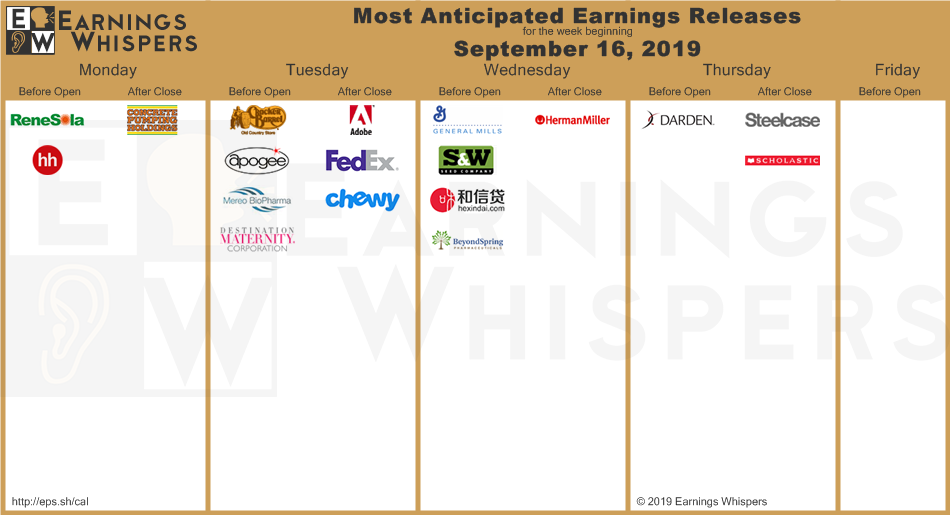

The week ahead — Economic data from Econoday.com: