Week of Jan 6, 2023 Weekly Recap & The Week Ahead

Monday, January 9th, 2023“Be who you are and say what you feel, because those who mind don’t matter and those who matter don’t mind.” — Bernard Baruch

1. Amazon to Lay Off Over 17,000 Workers, More Than First Planned — the Seattle-based company in November said that it was beginning layoffs among its corporate workforce, with cuts concentrated on its devices business, recruiting and retail operations. At the time, the company expected the cuts would total about 10,000 people, but a person with knowledge of the issue said the number could change, The Wall Street Journal reported. Thousands of those cuts began last year.

2. Fed Minutes Show Officials Feared Markets’ Rallies Could Hinder Inflation Fight –minutes of the Fed’s policy meeting last month, highlighted the tricky communications task that has vexed the central bank over the past six months. The Fed’s rapid rate increases last year have fanned investors’ hopes that inflation will slow quickly over the coming year. In the run-up to the December meeting, longer-term bond yields tumbled, reflecting both optimism about a speedy decline in inflation and fears of a recession this year.

But many Fed officials are anxious they won’t be able to defeat inflation unless they can slow the economy by tightening financial conditions, such as by raising borrowing costs or lowering stock prices.

3. Hiring, Wage Gains Eased in December, Pointing to a Cooling Labor Market in 2023 — after two straight years of record-setting payroll growth following the pandemic-related disruptions, the labor market is starting to show signs of stress. That suggests 2023 could bring slower hiring or outright job declines as the overall economy slows or tips into recession.

Employers added 223,000 jobs in December, the smallest gain in two years, the Labor Department said Friday. Average hourly earnings were up 4.6% in December from the previous year, the narrowest increase since mid-2021, and down from a March peak of 5.6%. All told, employers added 4.5 million jobs in 2022, the second-best year of job creation after 2021, when the labor market rebounded from Covid-19 shutdowns and added 6.7 million jobs. Last year’s gains were concentrated in the first seven months of the year. More recent data and a wave of tech and finance-industry layoffs suggest the labor market, while still vibrant, is cooling.

4. New Alzheimer’s Drug Approved by FDA, Promises to Slow Disease — U.S. health regulators gave early approval to a new Alzheimer’s drug from Eisai Co. and Biogen Inc., the most promising to date in a new class of medicines that may help slow cognitive decline caused by the disease.

The Food and Drug Administration granted conditional approval to the drug, called lecanemab, based on an early study finding it reduced levels of a sticky protein called amyloid from the brains of people with early-stage Alzheimer’s. The companies will sell it under the brand name Leqembi.

Eisai said it would sell the drug at a price of $26,500 a year for the average patient, and that it would be available commercially by Jan. 23. A preliminary report by the Institute for Clinical and Economic Review, a nonprofit that works with drugmakers and insurers to evaluate drug prices, said a fair price would be in the range of $8,500 to $20,600 a year.

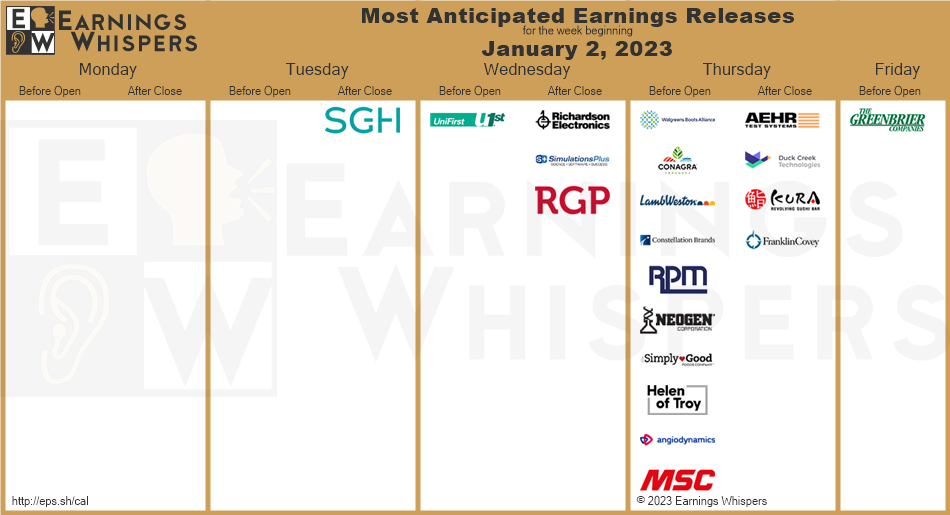

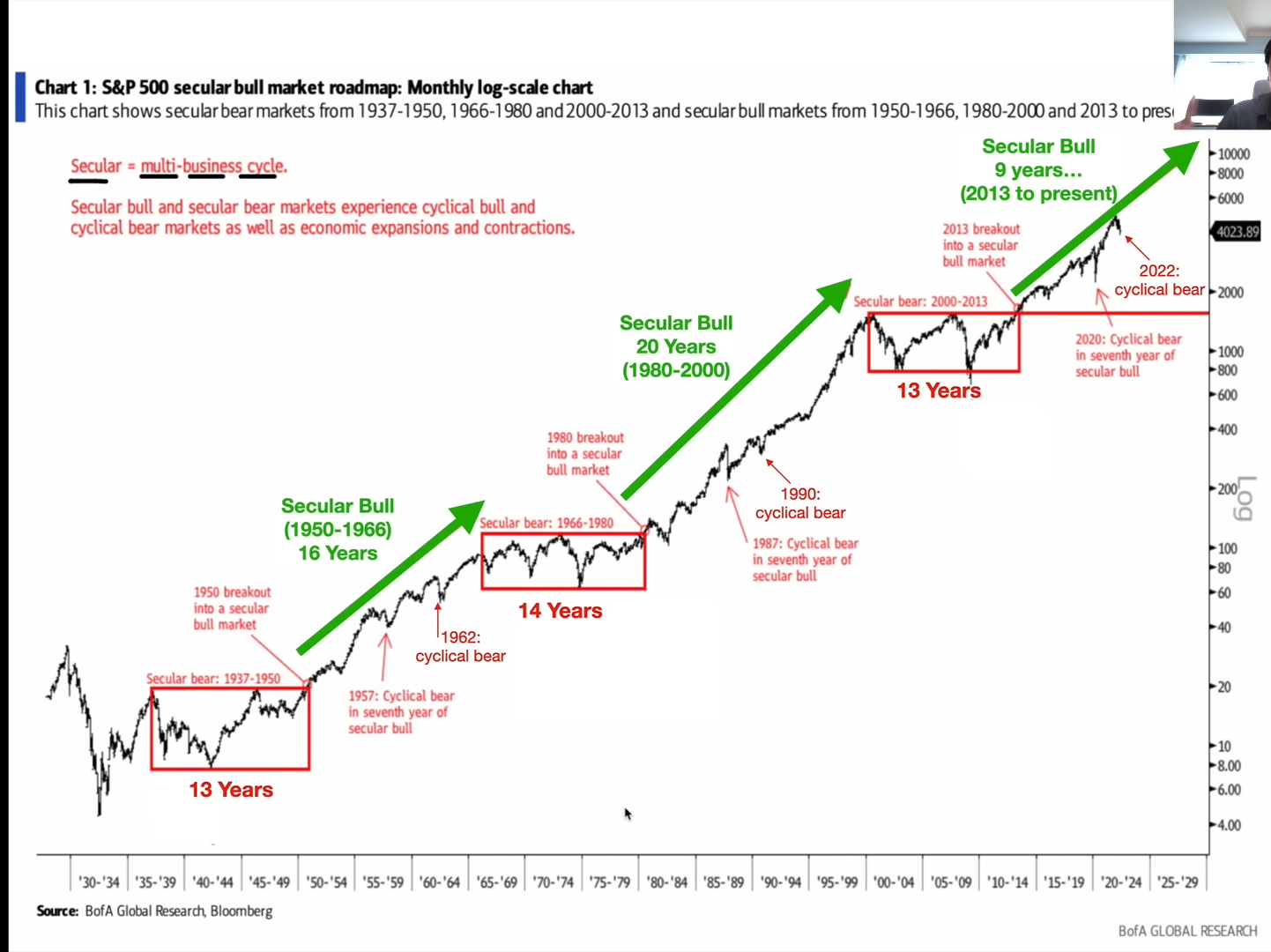

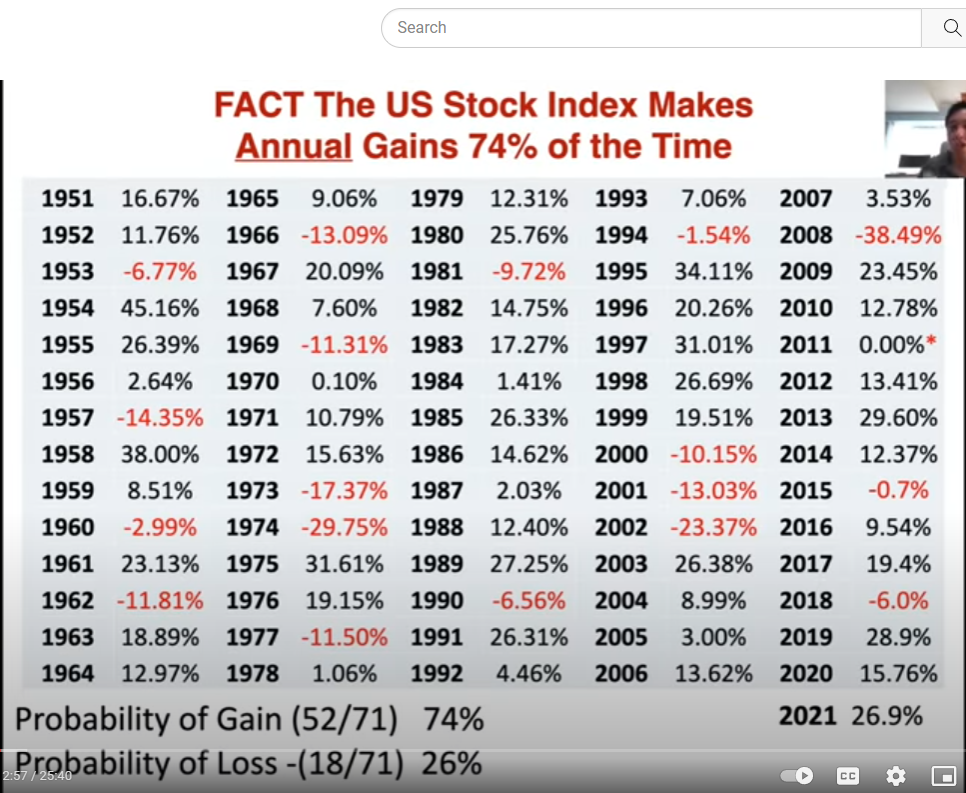

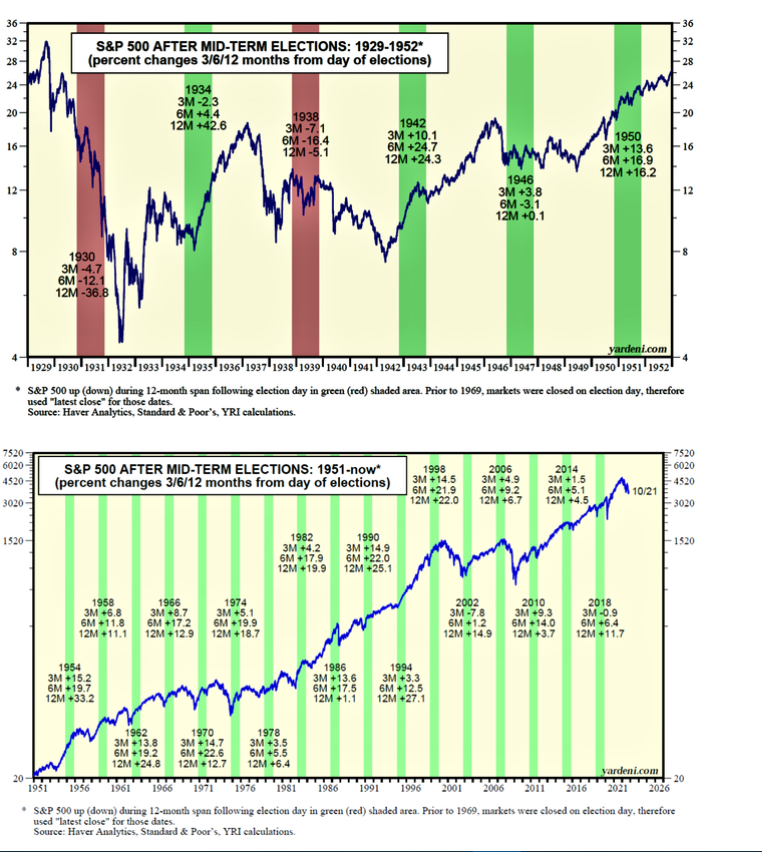

2022 Market Recap — below is the highlight of events happened in 2022

2022_Recap_1

2022_Recap_2

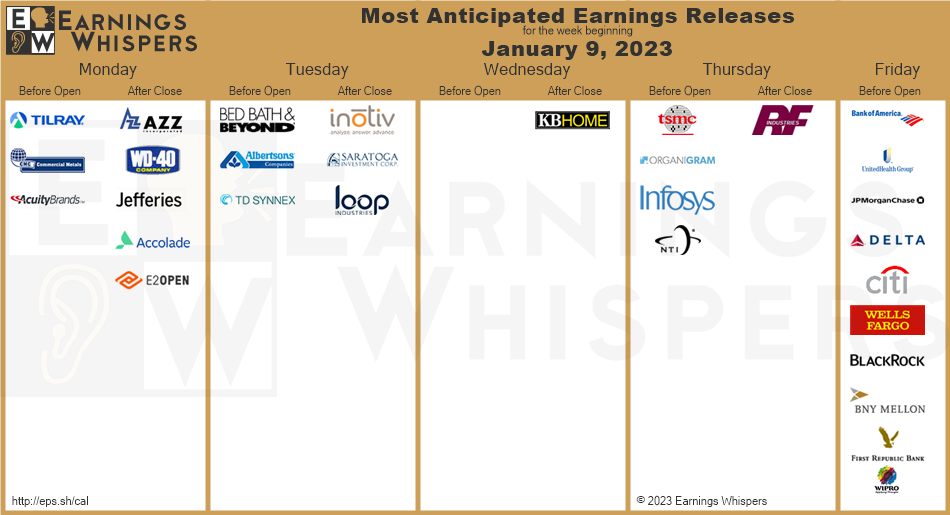

The week ahead — Economic data from Econoday.com: