Week of Aug 11, 2023 Weekly Recap & The Week Ahead

Monday, August 14th, 2023I know where I’m getting out before I get in. — Bruce Kovner

1. Chinese Exports Fall at Steepest Pace Since February 2020 — China’s exports to the rest of the world tumbled in July, adding to the challenges for the world’s second-largest economy and offering fresh evidence that a drying up of Western demand is hurting Beijing’s attempts to rekindle growth.

After a short-lived rebound in the spring, goods exports from China resumed a long-term slide that dates to October last year, when consumers in Western developed countries began shifting their spending away from buying furniture and electronic gadgets, and instead diverted it toward services such as entertainment and dining out.

Worsening geopolitical tensions between Beijing and the U.S.-led West have also prompted some Western manufacturers to reduce their reliance on China’s supply chain, which in turn is expected to erode trade ties between the two sides.

2. Biden Restricts U.S. Investment in China — the U.S. will prohibit Americans from investing in some Chinese companies developing advanced semiconductors and quantum computers starting next year, escalating Washington’s efforts to prevent Beijing from producing cutting-edge technology for its military.

President Biden on Wednesday issued an executive order creating the rules after months of deliberations. The move could unsettle fragile efforts to rekindle diplomatic relations with China. Officials in Beijing have railed against U.S. policies restricting access to advanced technology, as tensions between the two superpowers have contributed to slowing U.S. direct investment in China.

3. Inflation Picks Up but Modest Price Pressures Could Encourage Fed to Hold Rates Steady — The consumer-price index, a measure of goods and services prices across the economy, rose 3.2% in July from a year earlier, up from 3% in the year through June, the Labor Department said Thursday. So-called core prices, which exclude volatile food and energy categories, rose by 4.7% in July from a year earlier, a slight cooling from June’s 4.8% increase.

The monthly figures, however, offered a more encouraging picture of current price trends. The CPI rose a mild 0.2% in July, same as in June. Even better, the core CPI also increased just 0.2% in both months, suggesting inflation isn’t starting to resurge. Fed officials focus on core inflation because they see it as a better predictor of future inflation than the overall inflation rate.

4. Wholesale prices rose 0.3% in July, higher than expected — The producer price index, which gauges the costs that goods and services producers receive for their products as opposed to those that consumers pay, rose 0.3% for the month, the Bureau of Labor Statistics reported Friday. That was the biggest monthly gain since January and up from a unchanged reading in June. Excluding food and energy, core PPI also increased 0.3%, the biggest monthly increase since November 2022 after falling 0.1% in June. Core PPI rose 2.4% on a 12-month basis, tied for the lowest since January 2021. On a year-over-year basis, headline PPI was up just 0.8%. Prices excluding food, energy and trade services moved up by 2.7% on an annual basis, unchanged from June.

The week ahead — Economic data from Econoday.com:

Posted in

Posted in Week of Aug 4, 2023 Weekly Recap & The Week Ahead

Tuesday, August 8th, 2023In this business if you’re good, you’re right six times out of ten. You’re never going to be right nine times out of ten. –– Peter Lynch

1. Fitch Downgrades U.S. Credit Rating — the downgrade, the first by a major ratings firm in more than a decade, is evidence that increasingly frequent political skirmishes over the U.S. government’s finances are clouding the outlook for the $25 trillion global market for Treasurys. Fitch’s rating on the U.S. now stands at “AA+”, or one notch below the top “AAA” grade. America’s reputation for reliably making good on its IOUs has cast Treasury bonds in an indispensable role in global markets: a safe-haven security offering nearly risk-free returns. Treasurys serve as a critical benchmark for returns on stocks and other bonds, because investors generally demand greater yields on any other securities that they buy.

2. Warren Buffett Is Buying Treasuries Regardless of US Downgrade by Fitch — “Berkshire bought $10 billion in US Treasuries last Monday. We bought $10 billion in Treasuries this Monday. And the only question for next Monday is whether we will buy $10 billion in 3-month or 6-month” T-bills, Buffett said on CNBC. “There are some things people shouldn’t worry about,” he said. “This is one.” Fitch cut the US’s sovereign rating to AA+ from AAA earlier this week, citing the nation’s growing deficit and increasing political brinkmanship around the periodic efforts needed to raise the debt ceiling. The timing was apt — less than 24 hours later, the government boosted its quarterly borrowing plans for the first time in two-and-a-half years.

3. US Wage Growth, Lower Unemployment Underpin Solid Jobs Market — US employment increased at a solid pace in July while wages rose at a faster-than-expected clip, consistent with sustained labor demand that’s at the root of renewed momentum in the economy. Nonfarm payrolls increased 187,000 last month following a similar advance in June, a Bureau of Labor Statistics report showed Friday. The unemployment rate unexpectedly dropped to 3.5%, one of the lowest readings in decades. Average hourly earnings were up 0.4% from June and 4.4% from a year earlier, both stronger than forecast. That said, pay growth has been showing signs of slowing, as the supply and demand for workers comes more into balance following years of pandemic-induced labor shortages.

Here is a summary of the stock market last week (August 1-5, 2023):

The S&P 500 fell 1.9% for the week, marking its fifth consecutive weekly decline.

The Dow Jones Industrial Average fell 1.6%, and the Nasdaq Composite fell 2.3%.

The declines were driven by concerns about inflation and the pace of interest rate hikes by the Federal Reserve.

On Tuesday, ratings agency Fitch downgraded the U.S. credit rating from AAA to AA+, citing concerns about the country’s high debt levels.

On Friday, the U.S. Labor Department released its monthly jobs report, which showed that the economy added 187,000 jobs in July, below expectations.

The report also showed that wage growth remained strong, which could add to inflationary pressures.

Despite the declines, there were some positive signs last week.

Earnings season continued to be strong, with 84% of the companies in the S&P 500 reporting earnings that beat analyst expectations.

The week ahead — Economic data from Econoday.com:

Posted in

Posted in Week of July 28, 2023 Weekly Recap & The Week Ahead

Tuesday, August 1st, 2023The key to trading success is emotional discipline. If intelligence were the key, there would be a lot more people making money trading… I know this will sound like a cliché, but the single most important reason that people lose money in the financial markets is that they don’t cut their losses short. — Victor Sperandeo

1. Banc of California Agrees to Buy PacWest as Regional Lenders Seek Strength Together — Banc of California in a move by the lenders to further shore themselves up following a regional-banking crisis earlier this year. Warburg Pincus and Centerbridge plan to invest a total of $400 million in newly issued equity, giving them about a 19% stake in the combined business. The private-equity firms, each with a history of investing in financial companies, will provide the only external source of funding for the acquisition.

2. Federal Reserve Raises Interest Rates to 22-Year High — the Federal Reserve resumed lifting interest rates Wednesday with a quarter-percentage-point increase that will bring them to a 22-year high. The unanimous decision to raise the benchmark federal-funds rate to a range between 5.25% and 5.5% ended a brief pause in rate increases last month as officials debate whether they have done enough to combat inflation. It is the 11th increase since March 2022, when they lifted rates from near zero. At a news conference after the meeting, Fed Chair Jerome Powell didn’t rule out another rate rise at the central bank’s next meeting, but he emphasized how much the central bank had already done and the amount of time it can take for monetary policy to cool inflation.

3. GDP grew at a 2.4% pace in the second quarter, topping expectations despite recession calls — GDP, the sum of all goods and services activity, increased at a 2.4% annualized rate for the April-through-June period, better than the 2% consensus estimate from Dow Jones. GDP rose at a 2% pace in the first quarter. Consumer spending powered the solid quarter, aided by increases in nonresidential fixed investment, government spending and inventory growth. inflation was held in check through the period. The personal consumption expenditures price index increased 2.6%, down from a 4.1% rise in the first quarter and well below the Dow Jones estimate for a gain of 3.2%.

4. Inflation and Wage Growth Ease as Fed Considers Next Move — the personal-consumption expenditures price index, the Fed’s preferred inflation measure, rose 3% in June from a year earlier, the Commerce Department said separately Friday, down from a 3.8% rise the prior month. Employers spent 4.5% more on wages and benefits in April to June from a year earlier, the Labor Department said Friday. That marked a slowing from a 4.8% increase the prior quarter. The employment-cost index, a measure of compensation growth closely watched by Fed officials, also posted its smallest quarterly increase in two years.

Here is a summary of the stock market last week:

The S&P 500 rose 0.7% for the week, closing at 3,899.38.

The Dow Jones Industrial Average rose 0.3%, closing at 31,384.55.

The Nasdaq Composite rose 1.3%, closing at 11,635.31.

The VIX volatility index fell 11.3%, closing at 22.05.

The market was largely positive last week, with all three major indexes closing higher. The S&P 500 and Nasdaq Composite both closed at their highest levels since June 13. The Dow Jones Industrial Average also closed at its highest level since June 8.

There were a few factors that contributed to the positive market sentiment last week. First, investors were encouraged by the strong earnings reports that were released. Second, there was some relief that the Federal Reserve was not planning to raise interest rates as aggressively as some had feared. Third, there was some optimism that the economy was starting to slow down, which could help to ease inflation.

The week ahead — Economic data from Econoday.com:

Posted in

Posted in Week of July 21, 2023 Weekly Recap & The Week Ahead

Monday, July 24th, 2023“We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.” — Warren Buffett

1. Retail Sales Rose in June as Inflation Eased — Retail sales—a measure of spending at stores, online and in restaurants—rose a seasonally adjusted 0.2% last month from the month before, the Commerce Department said Tuesday. That was a slower pace than in May and April and matched the 0.2% increase in consumer prices last month, a sign that Americans’ spending is keeping up with, but not outpacing, inflation. In June, shoppers picked up their spending on furniture, electronics and online shopping. Sales at grocery stores, gasoline stations, hardware and sporting goods stores dropped. Dining out at bars and restaurants was broadly flat.

2. High Rates, Low Supply Hinder Home Buying This Summer — Elevated mortgage rates resulting from the Federal Reserve’s actions since early last year are keeping many buyers out of the market and reducing demand. At the same time, the rates are discouraging homeowners from selling, limiting the supply of homes for sale. Existing home sales, which make up most of the housing market, decreased 3.3% in June from the prior month to a seasonally adjusted annual rate of 4.16 million, the National Association of Realtors said Thursday. That was the slowest sales pace since January. June sales fell 18.9% from a year earlier.

3. White House Says Amazon, Google, Meta, Microsoft Agree to AI Safeguards — the White House said seven major AI companies—Amazon.com AMZN 0.03%increase; green up pointing triangle, Anthropic, Google, Inflection, Meta Platforms META -2.73%decrease; red down pointing triangle, Microsoft MSFT -0.89%decrease; red down pointing triangle and OpenAI—are making voluntary commitments that also include testing their AI systems’ security and capabilities before their public release, investing in research on the technology’s risks to society, and facilitating external audits of vulnerabilities in their systems. Before OpenAI launched its GPT-4 model in late March, the company spent roughly six months working with external experts who tried to provoke it to produce harmful or racist content. Most companies also developing large language models rely heavily on humans who teach these models to be engaging and helpful and avoid generating toxic responses through a process called reinforcement learning with human feedback.

The week ahead — Economic data from Econoday.com:

Posted in

Posted in Week of July 14, 2023 Weekly Recap & The Week Ahead

Monday, July 17th, 20231. CPI Report Shows Inflation Eased to 3% in June — the consumer-price index climbed 3% in June from a year earlier, the Labor Department said Wednesday, sharply lower than the recent peak inflation rate of 9.1% in June 2022, when gasoline prices hit a U.S. record average of $5 a gallon. The June rate declined from 4% in May. Inflation was last close to 3% in March 2021. Consumers paid less last month for used cars and airline fares, and their rent increased at the slowest one-month pace since early 2022. Prices for car insurance and recreation services rose. Fed officials are on track to raise rates to a 22-year high at their July 25-26 meeting because economic activity hasn’t slowed down as much as anticipated. But the inflation report calls into question whether the Fed will lift rates after that, as most officials projected last month.

2. The Rapid Rise of Threads Appears to Be Hurting Twitter — Mark Zuckerberg, chief executive of Threads parent Meta Platforms said the new microblogging platform hit 100 million sign-ups less than a week after launching. At least two third-party estimates suggest Twitter traffic has been falling in tandem, an indication that its users may be leaving it for Threads rather than attempting to juggle both. The two products look and function in similar ways. Both focus on sharing short snippets of text but also allow users to post photos and videos. One distinction is that joining Threads requires having an account with Meta’s Instagram, which has more than 2 billion monthly users. That has made signing up easy and fast, though deleting a Threads account means also having to delete one’s Instagram account.

3. U.S. Takes Third Shot at Shoring Up Money-Market Funds — The Securities and Exchange Commission voted 3-2 Wednesday to change the rules governing money-market funds, which the Federal Reserve had to backstop with emergency lending facilities in 2008 and 2020. Two previous overhauls by the SEC failed to stop investors from fleeing certain funds en masse when markets faced extreme stress. Following criticism from mutual-fund lobbyists and some lawmakers, the SEC dialed back Wednesday’s rules from a version it proposed in 2021. That had included a requirement for some funds to implement so-called swing pricing, a mechanism used in Europe that aims to keep investors in the funds from seeing their shares diluted when others pull out in times of stress.

Instead, the final rule requires certain money-market funds used by institutional investors to impose fees when a fund sees daily net redemptions that exceed 5% of net assets.

4. Google’s Bard AI Chatbot Adds More Languages to Take On ChatGPT — The Alphabet GOOG 4.36%increase; green up pointing triangle unit plans Thursday to add several new features to Bard, its generative-AI chatbot, including the ability to converse in 43 additional languages, from Arabic to Vietnamese. The company will also make Bard available across much of Europe and in Brazil, territories that are home to hundreds of millions of people. The rollout also includes additional privacy features that were requested by European Union regulators last month, delaying the chatbot’s release in the region.

Here is a summary of the market last week:

Inflation data: The main event of the week was the release of inflation data on Wednesday. Both headline and core inflation came in lower than expected, with headline inflation falling to 3.0% and core inflation falling to 4.8%. This was seen as a sign that inflation is starting to cool, which helped to boost stocks.

Fed meeting: The Fed also met last week and hinted that they may be slowing the pace of interest rate hikes in the coming months. This was also seen as positive for stocks, as it reduced the risk of a recession.

Stocks: As a result of these factors, stocks had a strong week, with the S&P 500 and the NASDAQ Composite both gaining more than 2%. The NASDAQ Composite had its best week in four months.

Bonds: Bonds also performed well last week, with yields falling across the board. This was due to the combination of lower inflation and the expectation of slower Fed rate hikes.

Overall, it was a positive week for the markets, as investors welcomed the signs that inflation is starting to cool. However, it is important to note that inflation is still well above the Fed’s target, so there is still some risk that the central bank will need to continue raising rates.

Here are some additional details:

The S&P 500 closed the week at 3,902.06, up 2.04%.

The NASDAQ Composite closed the week at 11,607.62, up 3.11%.

The 10-year Treasury yield closed the week at 3.12%, down 11 basis points.

The week ahead — Economic data from Econoday.com:

Posted in

Posted in Week of July 7, 2023 Weekly Recap & The Week Ahead

Tuesday, July 11th, 2023“If you have an approach that makes money, then money management can make the difference between success and failure… … I try to be conservative in my risk management. I want to make sure I’ll be around to play tomorrow. Risk control is essential.” – Monroe Trout

1. China’s Export Curb on Chip-Making Metals Prompt Countries to Explore Supply-Chain Diversification — China produces around 60% of the world’s germanium and around 80% of its gallium, according to the Critical Raw Materials Alliance, an industry body. China mines and exports large quantities of gallium and germanium, providing the raw materials to countries such as the U.S. and Japan that process them into high-end products, which can then be used in manufacturing advanced semiconductors, military radars, LED panels, solar panels, electric vehicles and wind turbines. By contrast, China processes other minerals like cobalt, which are mined elsewhere. More export control measures are likely to come. The U.S. is likely to release in the coming weeks final and upgraded regulations related to export curbs of advanced chips and equipment that it announced in October, The Wall Street Journal has reported.

2. US Services Activity Expand by Most in Four Months on Stronger Demand — The Institute for Supply Management’s overall gauge of services increased 3.6 points — the most since the start of the year — to 53.9 last month. Readings above 50 represent expansion, and the index exceeded all forecasts in a Bloomberg survey of an economists. In a welcome sign on inflation, the group’s measure of prices paid for materials and services dropped to the lowest level since March 2020.

3. Wage Gains, Low Unemployment Keep Pressure on Fed; Hiring Cooled in June — U.S. employers added 209,000 workers in June, a solid monthly gain but down from May’s revised 306,000. In the first half of this year, payrolls grew by an average of 278,000 a month, down from nearly 400,000 last year.

The unemployment rate fell to 3.6% last month from 3.7% in May. Employers ramped up wages as they competed for a limited pool of workers. Average hourly earnings grew 4.4% in June from a year earlier, matching gains in the preceding two months and remaining well above the prepandemic pace. The latest jobs and wage data add to evidence that economic activity hasn’t slowed as much as Fed officials expected, and leaves them likely to lift interest rates to a 22-year high at their July 25-26 meeting. Inflation has eased from its recent peak a year ago, but remains roughly double the Fed’s 2% target.

The week ahead — Economic data from Econoday.com:

Week of June 30, 2023 Weekly Recap & The Week Ahead

Wednesday, July 5th, 2023“Do more of what works and less of what doesn’t”. — unknown

1. U.S. Home Prices Posted First Annual Decline Since 2012 in April — Home prices posted their first year-over-year price decline in 11 years in April, as higher mortgage rates made home purchases more expensive for buyers. The S&P CoreLogic Case-Shiller National Home Price Index, which measures home prices across the nation, fell 0.2% in April, compared with a 0.7% annual growth rate the prior month. The annual decline was the first for the index since April 2012. The average rate for a 30-year fixed mortgage was 6.67% in the week ended June 22, up from 5.81% a year earlier, according to Freddie Mac.

2. First-quarter economic growth was actually 2%, up from 1.3% first reported in major GDP revision — The U.S. economy showed much stronger-than-expected growth in the first quarter than previously thought, according to a big upward revision Thursday from the Commerce Department. Gross domestic product increased at a 2% annualized pace for the January-through-March period, up from the previous estimate of 1.3% and ahead of the 1.4% Dow Jones consensus forecast. This was the third and final estimate for Q1 GDP. The growth rate was 2.6% in the fourth quarter.

The upward revision helps undercut widespread expectations that the U.S. is heading toward a recession. A separate economic report released Thursday showed layoffs running well below expectations, indicating that labor market strength has held up even in the face of the Federal Reserve’s 10 interest rate hikes totaling 5 percentage points.

3. Polestar is the latest EV maker to announce a move to Tesla’s North American charging standard — new Polestar vehicles sold in North America will come standard with the Tesla-designed North American Charging Standard, or NACS, plug starting in 2025. Owners of existing Polestars will be able to charge at Tesla’s Supercharger stations with an adapter starting in mid-2024. Polestar’s deal follows an identical one announced by corporate sibling Volvo Cars on Tuesday. Ford Motor , General Motor and Rivian have also announced similar deals with Tesla in recent weeks.

4. Consumer Spending Streak Extended in May, Inflation Cooled — consumer spending, the primary driver of economic growth, rose 0.1% in May from the prior month, the Commerce Department said on Friday, compared with a revised 0.6% increase in April. Americans spent more on services such as healthcare and air travel, while spending on goods such as autos declined. Spending was flat in May when adjusted for inflation. The Fed’s preferred gauge of consumer prices, the personal-consumption expenditures price index, rose 3.8% from a year earlier, down from 4.3% in April. So-called core prices, which exclude volatile food and energy categories, rose 4.6% in May from a year earlier, down slightly from 4.7% in April. Economists see core inflation as a better predictor of future inflation than overall inflation. From the prior month, overall prices increased 0.1%, easing from a 0.4% rise in April.

The week ahead — Economic data from Econoday.com:

Week of June 23, 2023 Weekly Recap & The Week Ahead

Tuesday, June 27th, 2023“Soros is the best loss taker I’ve ever seen. He doesn’t care whether he wins or loses on a trade. If a trade doesn’t work, he’s confident enough about his ability to win on other trades that he can easily walk away from the position.” — Druckenmiller

1. Fed’s Powell Says Interest-Rate Pause Is Expected to Be Temporary — Fed officials left rates unchanged last week after lifting them at 10 straight policy meetings to combat inflation. But investors, consumers and borrowers shouldn’t think they were done, Powell told the House Financial Services Committee on Wednesday. Inflation and economic activity haven’t slowed as much as many officials anticipated this year, casting more uncertainty over how high they might lift rates this year.

Fed officials see a risk that their past rate increases, together with recent banking-industry stresses, will eventually create a sharper-than-anticipated slowdown. They are trying to balance that against the risk that the economy proves more resilient than expected and inflation stays too high, requiring them to increase rates higher than otherwise.

2. Submersible Passengers Died in Implosion — the five men onboard the missing submersible in the North Atlantic died in a catastrophic implosion, the U.S. Coast Guard said, after searchers found debris from the craft near the Titanic shipwreck that ended a desperate search to find them alive. The submersible, known as the Titan, had left Sunday morning for what was supposed to be an hours long excursion to the Titanic site more than 2 miles underwater, but it lost contact with the outside world. The disappearance set off an urgent international search effort to find them alive. The Coast Guard said earlier Thursday that crews had identified debris near the Titanic shipwreck about 900 miles off Cape Cod.

3. Bank of England Outpaces Peers With Rate Rise of Half Percentage Point — The Bank of England raised its key interest rate by half a percentage point Thursday, a more aggressive rate rise than its peers as it seeks to curb the highest inflation rate in the Group of Seven wealthy countries.

The move to raise the lending rate to 5%, its highest level since April 2008, revived fears that the central bank may have to push the U.K. economy into a recession later this year in an effort to contain price increases. Across rich economies, inflation has proved tougher to tame than central banks had expected only months ago, dashing hopes that borrowing costs might stop rising soon. Norway’s central bank also increased its core lending rate by half a percentage point Thursday, while Switzerland hiked its benchmark rate by a quarter point. Both warned of further increases in the coming months.

4. Higher Interest Rates Hit Home Prices Again — U.S. existing-home prices posted their biggest year-over-year decline in more than 11 years last month as rising interest rates continued to weigh on the housing market. The national median existing-home price fell 3.1% in May from a year earlier to $396,100, the largest drop since December 2011, the National Association of Realtors reported.

Existing-home sales, which make up most of the housing market, increased 0.2% in May from the prior month to a seasonally adjusted annual rate of 4.3 million, the National Association of Realtors reported. May sales fell 20.4% from a year earlier.

The week ahead — Economic data from Econoday.com:

Week of June 16, 2023 Weekly Recap & The Week Ahead

Tuesday, June 20th, 2023“Success if getting what you want. Happiness is wanting what you get.” — Dale Carnegie

1. Inflation rose at a 4% annual rate in May, the lowest in 2 years — The consumer price index, which measures changes in a multitude of goods and services, increased just 0.1% for the month, bringing the annual level down to 4%. That 12-month increase was the smallest since March 2021, when inflation was just beginning to rise to what would become the highest in 41 years. A 3.6% slide in energy prices helped keep the CPI gain in check for the month. Food prices rose just 0.2%.

However, a 0.6% increase in shelter prices was the biggest contributor to the increase for the all-items, or headline, CPI reading. Housing-related costs make up about one-third of the index’s weighting.

2. Fed Holds Rates Steady but Expects More Increases — Federal Reserve officials agreed to hold interest rates steady after 10 consecutive increases, but signaled they are leaning toward raising them next month if the economy and inflation don’t cool more. In a statement, the Fed said the decision to maintain the benchmark federal-funds rate in a range between 5% and 5.25%, a 16-year high, might be short-lived. “Holding the target range steady at this meeting allows the committee to assess additional information,” the committee said in the statement. Officials approved the rate decision unanimously.

3. European Central Bank Raises Rates, Signals More Hikes to Come — The European Central Bank nudged up interest rates by a quarter percentage point and indicated it will continue to push them higher, sending the euro surging higher. The ECB’s assertiveness, which took markets aback, stands in contrast to the Federal Reserve’s decision on Wednesday to keep interest rates steady. At a news conference, ECB President Christine Lagarde said officials are unhappy with the outlook for inflation and will continue to raise rates unless economic data change substantially. The ECB said in a statement it would increase its key deposit rate to 3.5%, the highest level in more than 20 years. That move, the bank’s eighth consecutive rate increase, was widely anticipated by investors. But in an unexpected hawkish twist, Lagarde strongly indicated it will raise rates again next month, and the bank sharply raised its forecasts for underlying inflation through 2025.

4. Retail sales rose 0.3% in May after a strong April gain — consumers spent a seasonally adjusted 0.3% more in May at retail stores, restaurants and online, following April’s strong 0.4% advance, the Commerce Department said Thursday. That growth reflected robust hiring and rising wages that pumped up incomes in recent months, further defying recession predictions in early 2023. Consumers spent more at grocery, furniture and electronics stores last month, Tuesday’s report showed. They also appeared to shrug off higher interest rates in May. Sales climbed at auto dealerships and home-improvement stores, places where customers often borrow to pay for big-ticket purchases.

The week ahead — Economic data from Econoday.com:

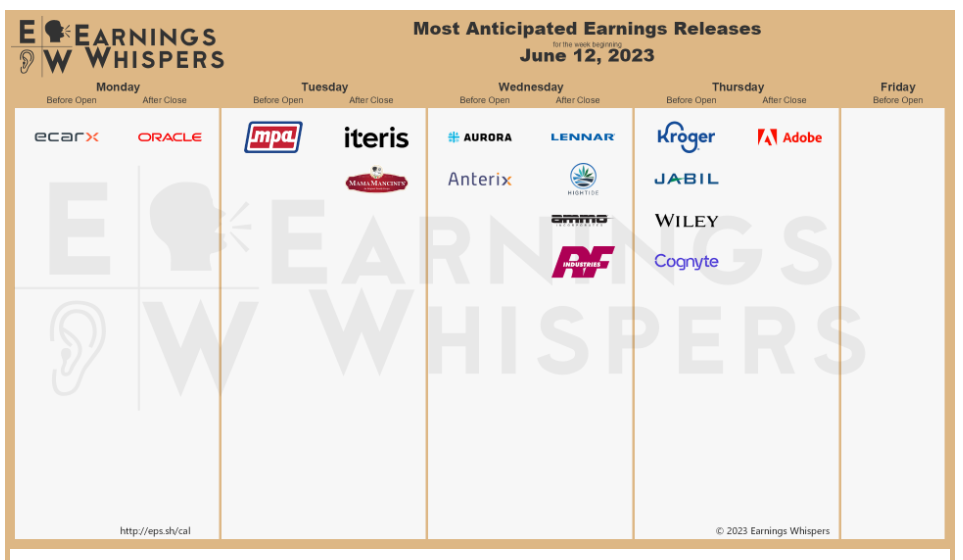

Week of June 9, 2023 Weekly Recap & The Week Ahead

Monday, June 12th, 2023“The whole secret to winning and losing in the stock market is to lose the least amount possible when you’re not right.” – William J. O’Neil

1. Treasury’s $1 Trillion Debt Deluge Threatens Market Calm — Investors are bracing for a flood of more than $1 trillion of Treasury bills in the wake of the debt-ceiling fight, potentially sparking a new bout of volatility in financial markets.

Some on Wall Street fear that roughly $850 billion in bond issuance that was shelved until a debt-ceiling deal was passed—sales expected between now and the end of September, according to JPMorgan analysts—will overwhelm buyers, jolting markets and raising short-term borrowing costs.

2. China’s Share of U.S. Goods Imports Falls to Lowest Since 2006 — The share of goods shipments the U.S. receives from China has declined to the lowest level since 2006. In recent years, imports from other countries in Asia have grown to meet the healthy demand for foreign products.

In April, U.S. businesses brought in more cars, cell phones and industrial supplies, the Commerce Department said Wednesday. Exports decreased as global growth ebbed. China’s share of trade with the U.S. dipped again, continuing a downward trend. China accounted for 15.4% of U.S. goods imports for the 12 months ended April, the smallest share since October 2006.

U.S. companies have been looking for alternatives to Chinese manufacturers in recent years. Amid geopolitical tensions between the two world powers, the Trump administration imposed tariffs on thousands of goods from China, which the Biden administration has continued.

3. GM EV Owners to Tap Tesla’s Supercharger Network — General Motors said its future electric vehicles will use the same charging hardware as Tesla TSLA a move aimed at giving GM owners more access to charging and further endorsing Tesla’s charging-port technology as the industry standard. GM reported that Tesla agreed to give GM customers access to 12,000 of Tesla’s fast chargers, known as Superchargers, starting next year. Those GM customers will need an adapter to use the chargers, because the GM vehicles use a different charge port. Starting in 2025, GM will start making EVs with the Tesla charge port instead. GM Chief Executive Mary Barra said that giving the company’s customers access to Superchargers will accelerate EV adoption and that switching to the Tesla charge port on future models “could help move the industry toward a single North American charging standard.”

4. Democrats Push for Debt-Ceiling Overhaul Bill After Default Scare — Democrats in the House and Senate introduced a bill Friday that would overhaul the debt-ceiling process, eager to capitalize on widespread anxiety in the party regarding the regular brinkmanship over the country’s borrowing limit.

Backers argue that using the full faith and credit of the U.S. as leverage is irresponsible and tantamount to taking the U.S. economy hostage. But many Republicans in Congress see the debt limit as a pressure point that can be used to extract concessions from Democrats on spending.

The week ahead — Economic data from Econoday.com: