Week of Dec 26 ’25 Weekly Recap & The Week Ahead

Tuesday, December 30th, 2025Happy Holidays and Wishing Everyone a Healthy and Prosperous New Year

1. US Economy Grows at Fastest Pace in Years With 4.3% GDP Gain — Inflation-adjusted gross domestic product, which measures the value of goods and services produced in the US, increased at a 4.3% annualized pace, a Bureau of Economic Analysis report showed Tuesday. That was higher than all but one forecast in a Bloomberg survey and followed 3.8% growth in the prior period.

The BEA was originally due to publish an advance estimate of GDP on Oct. 30, but the report was canceled due to the government shutdown. The agency typically releases three estimates of quarterly growth — fine-tuning its projections as more data comes in — but it will only release two for the period leading up to the longest shutdown on record.

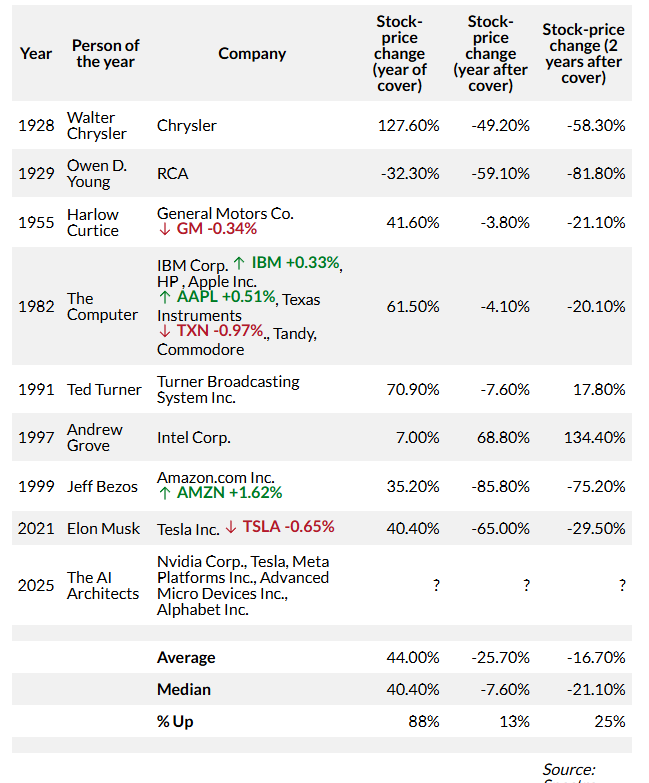

2. Time just jinxed the AI stock-market rally with its 2025 person of the year — Pioneered by analyst Paul Macrae Montgomery in his newsletter “Universal Economics,” the Time Magazine Cover Indicator — also known more generally as the Magazine Cover Indicator — posits that if a popular investment theme makes it to the cover of a general-interest publication like Time magazine, then the end is probably near. Time magazine announced its selection for person of the year. For 2025, it awarded the honor to a group of people, as it sometimes does: “The Architects of AI.” Brent Donnelly, president of Spectra Markets, crunched the numbers, and found that the person-of-the-year track record as a counterindicator is actually quite remarkable. Although the sample size is small, by Donnelly’s count — there have only been nine instances so far, including this year’s, in which the Time cover represented an investable person, company or category — it has been surprisingly effective. Investments, whether in companies or trends, tied to a person-of-the-year pick were higher one year later just 13% of the time, according to Donnelly. After two years, that figure rose to 25%. The only example that didn’t sell off during the following year was Intel Corp., whose co-founder and then-CEO Andy Grove was tapped as 1997’s person of the year. Intel shares were hammered a few years later, when the dot-com bubble burst.