Week of Oct 13, 2023 Weekly Recap & The Week Ahead

Tuesday, October 17th, 2023“ be fearful when others are greedy and to be greedy only when others are fearful.” — Warren Buffett

1. Producer Prices Came in Slightly Hotter than Expected — The producer-price index increased 0.5% from the prior month, a slowdown from August’s 0.7% increase, but still above economists’ expectations for 0.3% growth, according to FactSet. Excluding food and energy, core producer prices rose 0.3% for the month, slightly above expectations for a 0.2% gain. Leading the increase in September were prices for final demand goods, which increased 0.9%, and services, which were up 0.3%. For final demand goods, the increase can be attributed to higher energy prices, including a 5.4% rise in the index for gasoline.

2. Fed Minutes Show Officials Divided on Future Rate Rise — Federal Reserve officials were split over whether they would need to raise interest rates again this year when they decided last month to hold their benchmark policy rate steady. Officials most recently raised their benchmark federal-funds rate in July to a range between 5.25% and 5.5%, a 22-year high. They began lifting rates from near zero in March 2022. A run-up in long-term Treasury yields that began in August accelerated after last month’s meeting. If sustained, the rise in yields could moot the need for Fed officials to raise rates again this year. Economic projections released last month showed most officials had penciled in one more rate rise this year. But they made those projections before a further jump in long-term yields, which is raising rates on mortgages, auto loans and business debt.

3. US Consumer Prices Rise at Brisk Pace for Second Straight Month — The so-called core consumer price index, which excludes food and energy costs, increased 0.3% in September, Bureau of Labor Statistics data showed Thursday. Economists favor the core gauge as a better indicator of underlying inflation than the overall CPI. That measure climbed 0.4%, boosted by energy costs. Recent inflation data underscore how a strong labor market is underpinning consumer demand, which risks keeping price pressures above the Fed’s target. At their meeting last month, a majority of officials saw a need for one more interest rate hike this year, and they may maintain that bias — despite a recent surge in bond yields — if inflation doesn’t cool further.

4. JPMorgan Posts Big Earnings Beat, Setting Bar High for Other Banks — JPMorgan Chief Executive Jamie Dimon celebrated the results but also urged caution amid a challenging macroeconomic and geopolitical backdrop, which includes quantitative tightening and wars in Ukraine and Israel. Bank stocks have been punished this year as rapidly rising interest rates have caused many problems for lenders. At first, banks could delight in the fact that higher rates allowed them to earn more interest on the loans they issue. But high rates also have the tendency to keep potential borrowers on the sidelines and pressure current borrowers into delinquencies. The jump in rates has also meant savers now have more options for where to park their nest eggs and earn yield, putting pressure on banks’ funding costs.

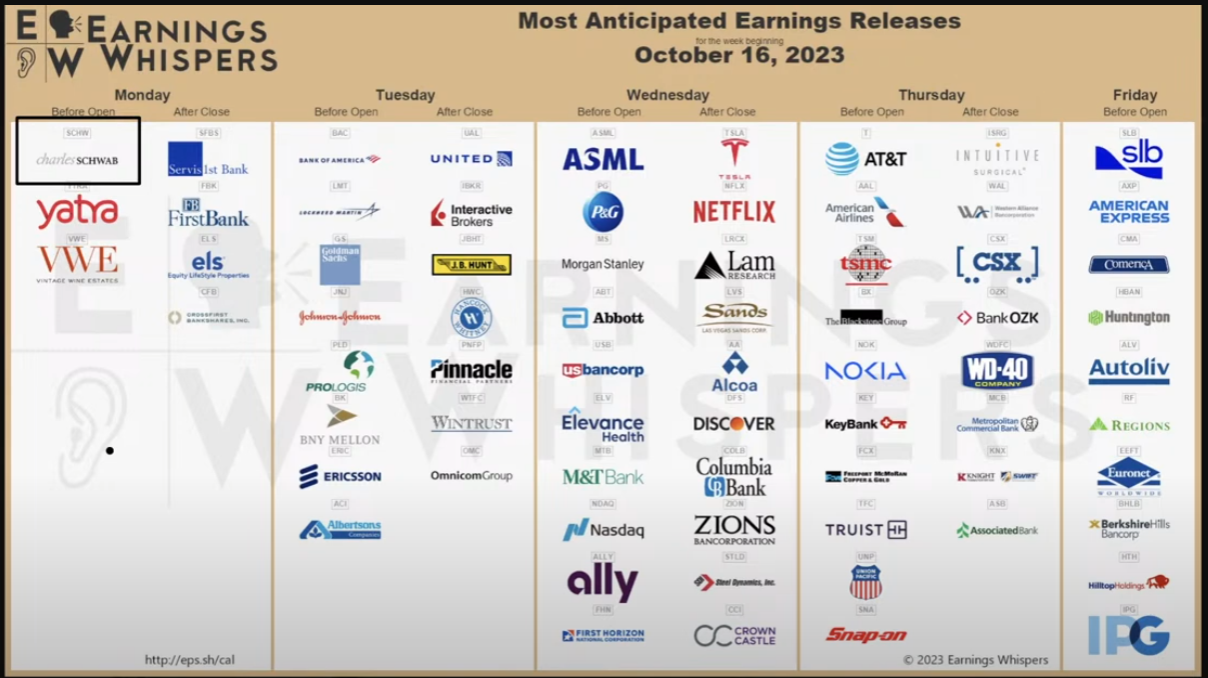

The week ahead — Economic data from Econoday.com: