Week of Feb 3, 2023 Weekly Recap & The Week Ahead

Monday, February 6th, 2023“Don’t look for the needle in the haystack. Just buy the haystack.” — John Bogle,

1. Worker Pay Gains Cooled Modestly Late Last Year as Fed Weighs Inflation — employers spent 1% more on wages and benefits last quarter versus the prior three months, a slowdown from a 1.2% increase in the third quarter, the Labor Department said Tuesday. From a year earlier the employment-cost index advanced 5.1%, in line with the 5% annual gain in the third quarter. The compensation report confirms other recent signs that wage growth has slowed, and comes as Fed officials start a two-day policy meeting. They are likely on Wednesday to approve raising their benchmark federal-funds rate by a quarter percentage point, down from their half-point increase in December, which followed four straight increases of 0.75 point.

2. Fed Approves Quarter-Point Rate Hike, Signals More Increases Likely — the Federal Reserve approved an interest-rate increase of a quarter-percentage-point and signaled plans to raise rates again next month to continue lowering inflation. The decision Wednesday followed six consecutive rate rises that were larger, including an increase of a half-point in December and a 0.75-point increase in November. The latest increase caps a year in which the Fed lifted its benchmark federal-funds rate from near zero to a range between 4.5% and 4.75%, a level last reached in 2007. That extends the central bank’s most rapid pace of rate increases since the early 1980s to fight inflation, which hit a 40-year high last year.

3. ECB Hikes by Half-Point and Signals Same Again in March — the European Central Bank lifted interest rates by a half-point, with President Christine Lagarde saying another such move is almost certain next month, despite conceding that the inflation outlook is improving.

Policymakers, as expected, raised the deposit rate to 2.5%, the highest since 2008. Lagarde warned that the most aggressive bout of monetary tightening in ECB history isn’t done — even as energy prices plunge and the Federal Reserve moderates the pace of its own hikes.

4. Unemployment Falls to 3.4%, Lowest in 53 Years, Jobs Report Shows — the U.S. labor market accelerated at the start of the year as broad-based hiring added a robust 517,000 jobs and pushed the unemployment rate to a 53-year low. January’s payroll gains were the largest since July 2022 and snapped a string of five straight months of slowing employment growth, the Labor Department said Friday. The unemployment rate was 3.4% last month, its lowest level since May 1969. Wage growth continued to soften last month, despite the strong job gains. Average hourly earnings grew 4.4% in January from a year earlier, down from a revised 4.8% in December. Annual revisions to employment and pay data suggest that wage growth has been cooling—but at a slower pace than previously thought.

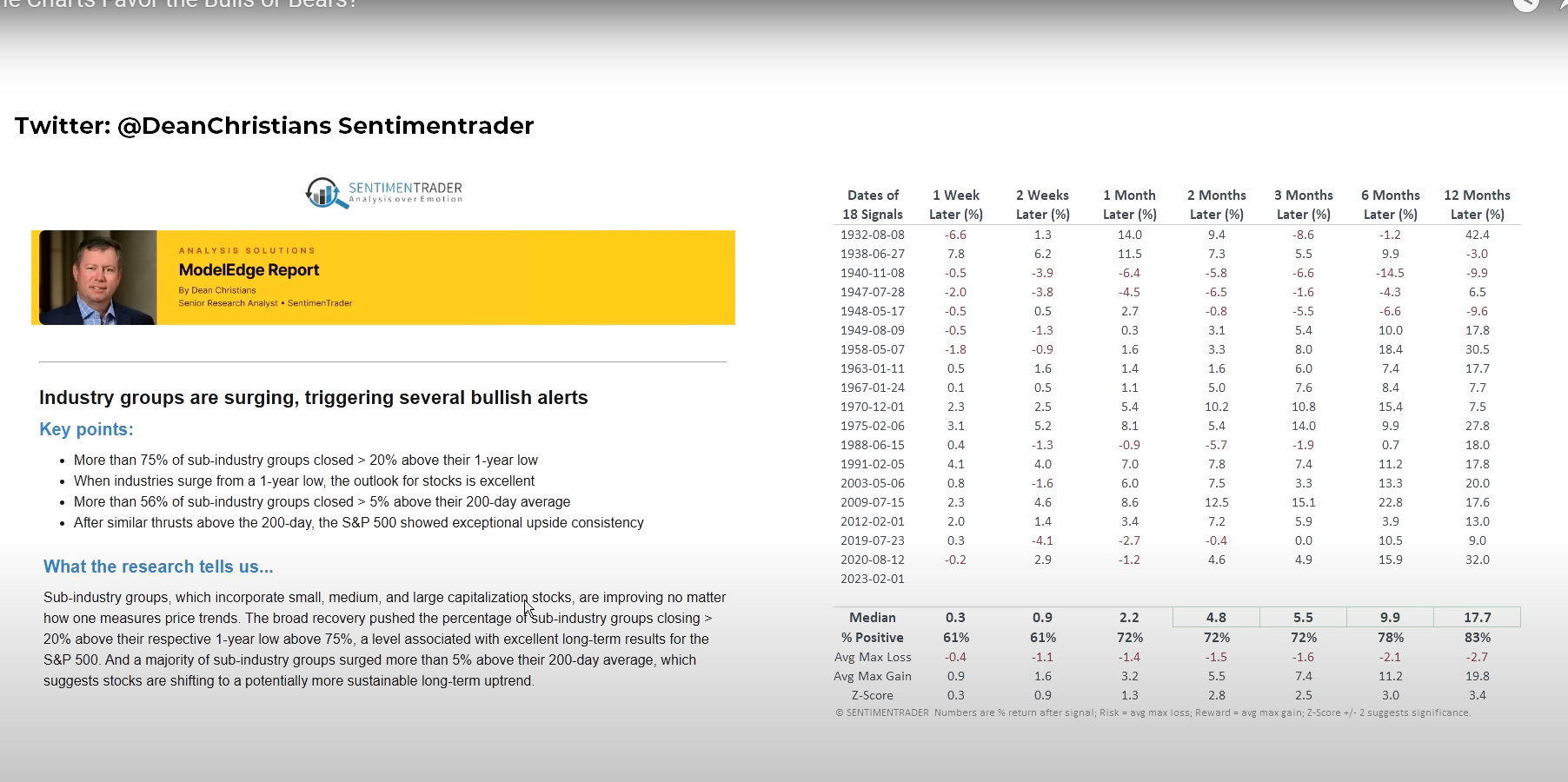

5. Industry Group Surged – Shows Bullish Patterns — courtesy of Sentiment Trader, several industry groups surges — see below chart for more details.

The week ahead — Economic data from Econoday.com: