Week of June 10, 2022 Weekly Recap & The Week Ahead

Tuesday, June 14th, 2022“Patient opportunism, buttressed by a contrarian attitude and a strong balance sheet, can yield amazing profits during meltdowns.” ― Howard Marks

1. World Bank Warns of Stagflation Risk, Cuts Global Growth Forecast to 2.9% — the World Bank sharply lowered its growth forecast for the global economy for this year, warning of several years of high inflation and tepid growth reminiscent of the stagflation of the 1970s.

Citing the damage from the war in Ukraine and the Covid-19 pandemic, the bank said global growth is expected to slump to 2.9% in 2022 from 5.7% in 2021, significantly lower than its January forecast for 4.1% growth. Furthermore, growth is expected to hover around the reduced pace over 2023 and 2024 as the war disrupts human activity, investment and trade while governments withdraw fiscal and monetary support.

2. Moderna Booster Targeting Omicron Shows Stronger Immune Response Than Original Vaccine — Moderna modified Covid-19 booster shot that targets the Omicron coronavirus variant showed a stronger immune response than the original vaccine. The modified “bivalent” booster shot—mRNA-1273.214—targets both Omicron and the original variant, and was well-tolerated in a study with 437 participants, according to preliminary data. The company’s updated vaccine had side effects comparable to the original booster dose but produced eight times more antibodies, the press release stated. Moderna (ticker: MRNA) will submit the analysis to U.S. regulators in the coming weeks, with the hope that the booster dose will be available in the late summer.

3. U.S. Considering Reducing Tariffs on China to Ease Inflation — treasury Secretary Janet Yellen said the Biden administration is considering ways to reconfigure tariffs on imports from China as a means of helping to ease decades-high inflation. The Biden administration has been split on whether to pare back tariffs on imports from China in an effort to cut consumer costs and reduce inflation. The administration has been engaged in a legally required review of the Trump-era tariffs. Easing the tariffs could take the form of expanding the list of items excluded from the duties.

4. ECB Plans July Rate Increase as Inflation Problem Deepens — in an unusually detailed statement, the ECB said it intends to raise its key rate by a quarter percentage point at its next policy meeting in July to minus 0.25%, and increase it again in September, possibly by more than 0.25 percentage point. It said it would end its large-scale bond-buying program on July 1. After September, the ECB said it expects a “gradual but sustained path of further increases in interest rates.” Unusually, the bank published its new staff inflation forecasts in its policy statement. They show eurozone inflation of 3.5% in 2023 and 2.1% in 2024, both above the ECB’s target rate.

5. U.S. Inflation Hit 8.6% in May — the Labor Department on Friday said that the consumer-price index increased 8.6% in May from the same month a year ago, marking its fastest pace since December 1981. That was also up from April’s CPI reading, which was slightly below the previous 40-year high reached in March. The CPI measures what consumers pay for goods and services. May’s increase was driven in part by sharp rises in the prices for energy, which rose 34.6% from a year earlier, and groceries, which jumped 11.9% on the year, the biggest increase since 1979. But inflation pressures were distinctly broad-based in May, said Sarah House, senior economist at Wells Fargo Securities.

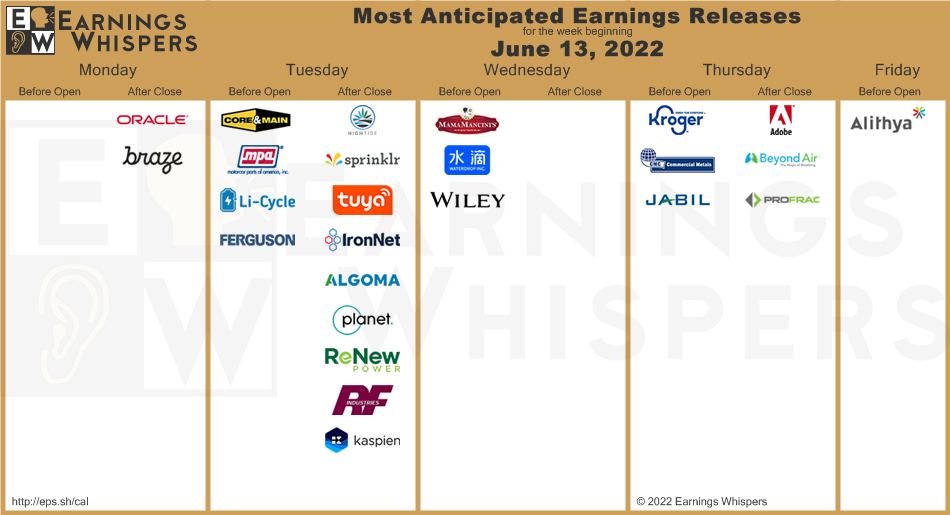

The week ahead — Economic data from Econoday.com: