Week of April 15, 2022 Weekly Recap & The Week Ahead

Monday, April 18th, 2022“Patient opportunism, buttressed by a contrarian attitude and a strong balance sheet, can yield amazing profits during meltdowns.” ― Howard Marks,

1. U.S. Inflation Accelerated to 8.5% in March, Hitting Four-Decade High — U.S. inflation surged to a new four-decade high of 8.5% in March from the same month a year ago, driven by skyrocketing energy and food costs, supply constraints and strong consumer demand. The Labor Department reported the consumer-price index—which measures what consumers pay for goods and services—last month rose at its fastest annual pace since December 1981, up from the 7.9% annual rate in February. Rising prices have been unrelenting, with six straight months of inflation above 6% that is well above the Federal Reserve’s average 2% target.

2. Chinese Stockpile Food as Covid-19 Concerns Ripple Out From Shanghai — As Shanghai battles the country’s worst Covid-19 outbreak in two years, people across the rest of China are stockpiling necessities as they brace for the prospect of similar lockdowns. In Beijing, where some residential districts have been closed in recent weeks as infections have been discovered, supermarket shelves in some parts of the city have been picked clean of toilet paper, canned foods, instant noodles and rice in recent days.

In Suzhou, an industrial hub roughly two hours’ drive west of Shanghai, residents swarmed supermarkets to fill their grocery baskets with instant noodles and other food on Tuesday morning, hours after local officials said they would conduct districtwide testing in one section of the city.

3. Supplier Prices Rose Sharply in March — the Labor Department on Wednesday said the producer-price index, which generally reflects supply conditions in the economy, increased a seasonally adjusted 1.4% in March from the prior month, a pickup from an upwardly revised 0.9% gain in February. Producer prices rose 11.2% on a 12-month basis, compared with an upwardly revised 10.3% increase in February. That marked the fourth consecutive month with a double-digit gain and was the highest since records began in 2010.

4. Mortgage Rates Hit 5% for First Time Since 2011 — the interest rate on America’s most popular mortgage hit 5% for the first time in more than a decade, extending a sharp rise that has yet to significantly slow the red-hot housing market. Rates’ fastest three-month increase since 1987 has made the housing market ground zero for the Federal Reserve’s efforts to tame inflation. Home buyers, already facing surging house prices, are now contending with a substantial increase in financing expenses, further lifting monthly payments. A year ago, buying the median American home at prevailing rates meant a monthly mortgage bill of about $1,223 after a 20% down payment, according to calculations by George Ratiu, an economist at Realtor.com. At recent rates, such a purchase would require a monthly payment of nearly $1,700—a 38% increase, he estimated.

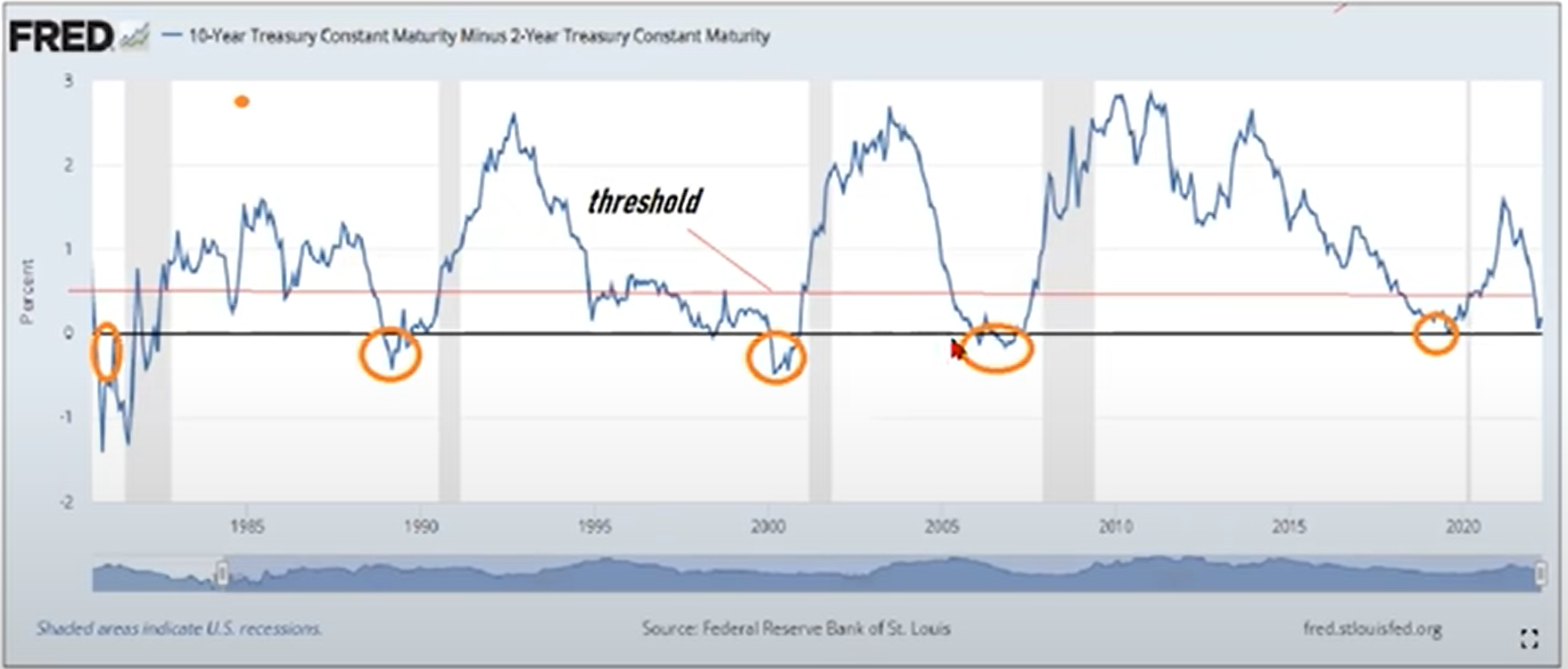

5. Inverted Yield Curve Follows by Recession — chart below from the Fed Reserve Bank of St. Louis shows the yield curve inversion follows by the recession usually precedes the market lead in the range of 10 to 34 months.

The week ahead — Economic data from Econoday.com: