Week of July 5 2019 Weekly Recap & The Week Ahead

Tuesday, July 9th, 2019“Obviously the thing to do was to be bullish in a bull market and bearish in a bear market… I came to learn that even when one is properly bearish at the very beginning of a bear market it is not well to begin selling in bulk until there is no danger of the engine back-firing.” – Jesse Livermore

1. U.S. Proposes More tariffs on EU Goods — Washington has turned its attention back to the EU. The U.S. Trade Representative has released a $4B list of additional goods that may be targeted with retaliatory tariffs as part of a long-running battle at the WTO over subsidies given to Airbus (OTCPK:EADSY) and Boeing (NYSE:BA). The list, which includes Italian cheese, Scotch whisky, chemicals and metals, adds to products valued at $21B that the USTR had identified in April as facing possible tariffs.

2. EU Open to Talks on Subsidies Dispute — the EU is open to talks with Washington in a dispute over aircraft subsidies, but it is also preparing retaliation after the U.S. added Italian cheese, Scotch whisky and other products to a list of goods in line for hefty tariffs. The WTO has found that Airbus (OTCPK:EADSY) and Boeing (NYSE:BA) received billions of dollars of harmful subsidies in a pair of cases marking the world’s largest-ever corporate trade dispute. Billions of dollars of tit-for-tat tariffs are on the line, with Washington first to seek the duties under the WTO timetable.

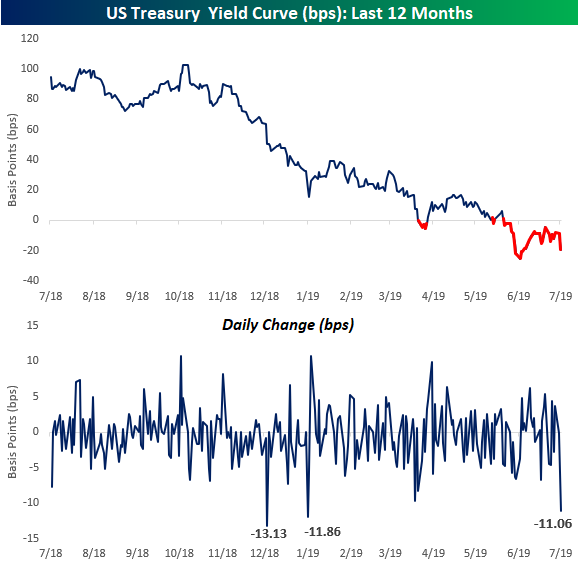

3. 10-year Yield Plummeting Below 2% — with the 10-year plummeting below 2% again and the 3-month yield spiking up by over 7 basis points, which is its biggest one day gain since December 2017. The 11-bps move further into inverted territory is the biggest one-day move since January 2nd (see second chart). While not back at new lows, today marks the 29th day that the curve has now been inverted. In Fedspeak news, Cleveland Fed President Loretta Mester (who leans hawkish but isn’t a voter) just noted in a speech that she’s in no hurry to cut. She argues that “Cutting rates at this juncture could reinforce negative sentiment about a deterioration in the outlook even if this is not the baseline view, and could encourage financial imbalances given the current level of interest rates, which would be counterproductive.”

Tuesday’s 11-bps move further into inverted territory is the biggest one-day move since January 2nd.

The week ahead — Economic data from Econoday.com: